Learning Outcomes

This article explains liability-driven and goal-based investing frameworks, including:

- The conceptual differences and practical connections between liability-driven investing (LDI) and goal-based investing (GBI) for both institutional and private clients

- How goals and liabilities are translated into hierarchies ranked by importance, time horizon, and required probability of achievement

- The design, rationale, and evaluation of multi-bucket portfolio structures that allocate assets across safety, lifestyle, and aspirational buckets

- Techniques for matching asset risk, duration, currency, and inflation exposure to specific goals or contractual liabilities

- Ways to integrate behavioral considerations—such as mental accounting, loss aversion, and changing preferences—into goal-setting and bucket design

- Methods for applying LDI and GBI frameworks to defined benefit pension plans, high-net-worth individuals, and typical private wealth scenarios

- Approaches to monitoring, rebalancing, and revising bucket allocations as market conditions, funding status, or client objectives change, with emphasis on minimizing shortfall risk, maintaining client adherence, and clearly articulating these structures in an exam setting through calculations, justifications, and concise written explanations

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand liability-driven and goal-based portfolio construction, with a focus on the following syllabus points:

- Recognizing and comparing liability-driven and goal-based investing objectives

- Describing and explaining goal hierarchy and its relevance for individual investors and institutions

- Designing and evaluating multi-bucket portfolio structures for different types of liabilities or goals

- Integrating behavioral, time horizon, and risk tolerance considerations into goal prioritization and portfolio construction

- Applying bucket and hierarchy structures to both DB pension funds and private wealth clients

- Explaining monitoring, rebalancing, and dynamic de-risking decisions within LDI and GBI frameworks

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

For a defined benefit pension plan, which portfolio construction approach best reflects a liability-driven investing framework?

- a) Maximizing expected return per unit of asset volatility using asset-only MVO

- b) Constructing a two-portfolio structure with a liability-hedging portfolio and a return-seeking portfolio

- c) Investing entirely in long-duration bonds to maximize current income

- d) Allocating equal weights to global equities, bonds, and alternatives

-

A retiree wants to ensure that 15 years of minimum living expenses are met with very high certainty, while also funding an aspirational legacy goal with remaining wealth. Which structure most closely reflects a goal-based, multi-bucket approach?

- a) A single balanced portfolio managed to a 60/40 strategic allocation

- b) Two separate portfolios: one invested aggressively for both needs and legacy

- c) A safety bucket for essential spending and a higher-risk aspirational bucket for legacy

- d) A ladder of term deposits for all assets regardless of goals

-

When constructing a goal hierarchy for a private client, which factor most directly determines the acceptable level of investment risk for a specific goal?

- a) The client’s marginal tax rate

- b) The client’s overall wealth relative to peers

- c) The assigned required probability of goal achievement and time horizon

- d) The expected correlation of goal funding assets with global equities

-

An individual client insists on keeping a large, concentrated stock position in the “aspirational” bucket while worrying about short-term volatility in her retirement income. Which behavioral bias is most likely influencing her preferences?

- a) Mental accounting leading her to treat the concentrated stock as “house money”

- b) Overconfidence in the manager of her diversified bond fund

- c) Regret aversion about realizing gains on diversified holdings

- d) Home bias in allocating to domestic fixed income

Introduction

Portfolio construction can be organized around two mutually reinforcing approaches: liability-driven investing (LDI) and goal-based investing (GBI). These methods structure asset allocation with explicit reference to future financial obligations—either through contractual liabilities for institutions or personal financial goals for individuals. Hierarchies of goals and multi-bucket portfolios allow investors and their advisers to better match asset risk to specific needs and timeframes, accommodate behavioral biases, and improve portfolio adherence in volatile markets.

Key Term: Liability-driven investing (LDI)

Liability-driven investing is an approach that focuses asset allocation and risk management on meeting future defined liabilities, typically by matching asset cash flows and risk attributes (e.g., duration, inflation, and currency exposure) to the size, timing, and nature of those obligations. Key Term: Goal-based investing (GBI)

Goal-based investing is a strategy that segments an investor’s portfolio into sub-portfolios ("buckets"), each dedicated to meeting a specific financial goal or set of goals, with investment risk tailored to the importance and time horizon of each goal. Key Term: Goal hierarchy

A goal hierarchy is the process of ranking objectives or liabilities by priority, urgency, and required probability of success, so that portfolio resources and risk levels are adjusted accordingly. Key Term: Multi-bucket portfolio

A multi-bucket portfolio is a structure in which portfolio assets are divided into distinct "buckets," each with its own risk/return profile and funding a specific goal, liability, or time period.

At Level 3, you are expected not only to define these concepts, but to use them in constructed-response answers: classifying goals, designing appropriate buckets, selecting asset classes that match liability characteristics, and explaining how to revise structures when conditions change.

Test Tip: When revising Goal hierarchies and multi-bucket portfolios, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Liability-driven and Goal-based Approaches: What Are They

Liability-driven and goal-based frameworks share a focus on structuring portfolios around future outflows. Both recognize that investors—whether pension plans or individuals—benefit from having distinct asset pools matched to the nature and timing of their required cash flows. However, the starting point and the constraints differ.

Liability-driven Investing: Institutional Focus

Liability-driven investing is most commonly associated with institutions like defined benefit (DB) pension funds, life insurers, and, in a broader sense, banks that must meet contractual claims. For these entities, the relevant future outflows are contractual and relatively well-defined: pension payments, annuity streams, or insurance claims. The institution’s mission is often stated in terms of paying these obligations in full and on time with very high probability.

LDI strategies usually follow one or more of these principles:

- Hedging the present value and risk exposures of liabilities with dedicated asset portfolios

- Matching the duration, currency, and inflation sensitivity of assets to those of liabilities (immunization)

- Prioritizing certainty of outcome and minimization of shortfall risk over pure return maximization

- Managing risk in terms of surplus volatility (assets minus liabilities) and the probability of funding shortfall

Key Term: Funding ratio

The funding ratio is the ratio of the market value of plan assets to the present value of liabilities. A funding ratio above 100% indicates a surplus; below 100% indicates a deficit.

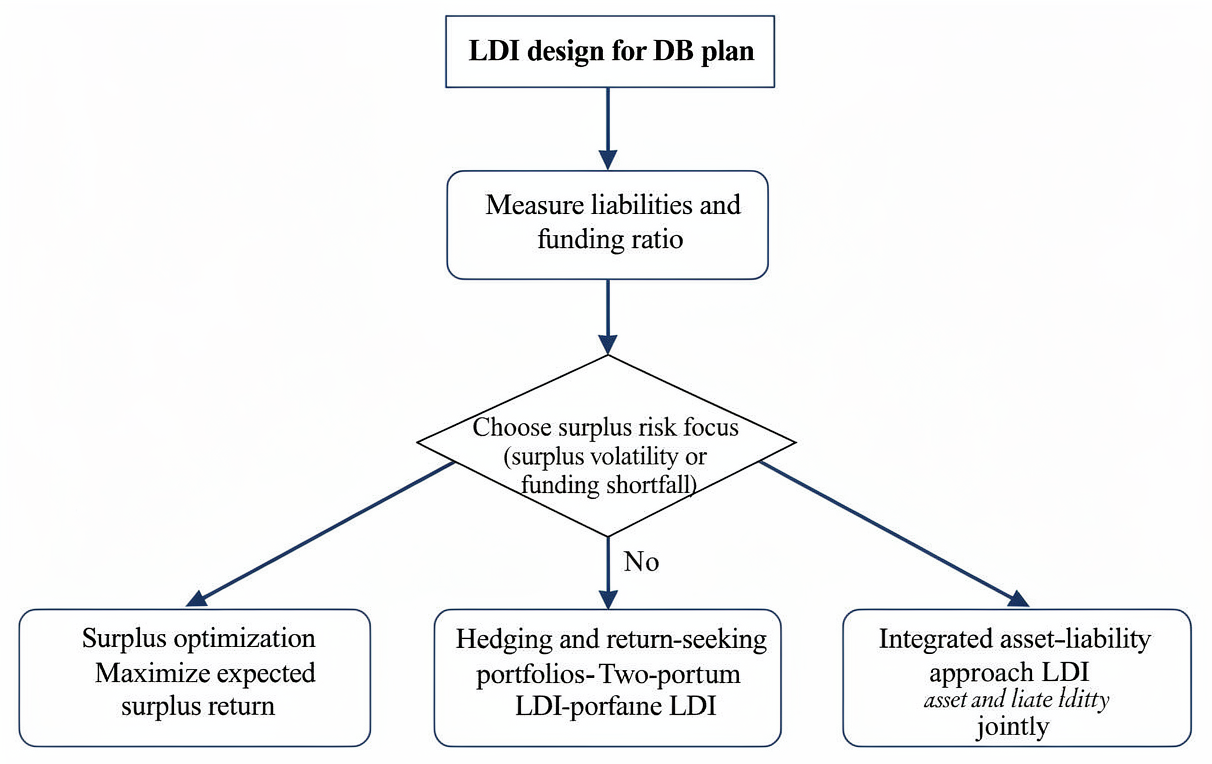

The Level 3 curriculum describes three main liability-relative allocation approaches inside an LDI framework:

- Surplus optimization:

Key Term: Surplus optimization

Surplus optimization adapts mean–variance optimization by replacing asset return with surplus return (asset return minus liability return) and using surplus volatility as the risk measure, seeking portfolios that maximize expected surplus return for a given level of surplus risk.

This explicitly incorporates the covariance between assets and liabilities. For example, in a DB plan, assets with negative correlation to liability returns (e.g., long-duration bonds) can substantially reduce surplus volatility.

- Hedging/return-seeking portfolios approach:

Key Term: Hedging/return-seeking portfolios approach

The hedging/return-seeking portfolios approach separates assets into a liability-hedging portfolio that closely tracks the present value of liabilities and a return-seeking portfolio aimed at generating surplus growth.Key Term: Hedging portfolio

A hedging portfolio is the asset segment designed to mirror the interest rate, inflation, and sometimes longevity exposure of the liabilities, aiming to stabilize the funding ratio.Key Term: Return-seeking portfolio

A return-seeking portfolio is the asset segment invested in growth-oriented assets (e.g., equities, private equity, credit, real assets) to increase expected surplus and potentially reduce sponsor contributions over time.

This is sometimes called the “two-portfolio” approach. Asset allocation between the two depends on the funding ratio and risk tolerance of the sponsor. As funding improves, LDI de-risking policies often shift assets from the return-seeking to the hedging portfolio.

- Integrated asset–liability approach:

Key Term: Integrated asset–liability approach

An integrated asset–liability approach jointly optimizes asset and liability decisions, recognizing that institutions such as banks and insurers can actively manage both sides of their balance sheet to control risk and profitability.

In exam questions, you may be asked to select which of these approaches is most suitable given data on funding status, risk tolerance, and regulatory constraints.

Key Term: Immunization

Immunization is a fixed-income strategy that seeks to lock in a specific return or funding objective by matching the duration and, ideally, convexity of assets to those of the liabilities, so that small parallel yield curve shifts have minimal impact on surplus.

LDI can also apply to high-net-worth individuals with contractually required outflows (e.g., debt repayments) or quasi-contractual obligations (e.g., required minimum spending), where part of the portfolio is managed with a liability-relative mindset.

Goal-based Investing: The Private Wealth Viewpoint

Goal-based investing segments an investor’s portfolio according to different personal objectives—retirement security, education, legacy, philanthropy, luxury purchases, and more. Each goal is distinct in importance, required time horizon, and desired probability of success.

GBI uses the concept of a goal hierarchy: critical or near-term goals (such as lifetime spending needs) are ranked above less essential or longer-term aspirational goals (such as leaving a large bequest or purchasing a second home). The portfolio is divided into "buckets"—each with tailored investments to maximize the chance of success for its goal.

Unlike LDI, GBI:

- Accepts that goals may not be contractual and can be revised as circumstances change

- Places explicit weight on behavioral comfort and client understanding

- Often uses probability of goal achievement as the primary risk metric, rather than variance of return

Key Term: Probability of goal achievement

The probability of goal achievement is the likelihood that a specific asset allocation and funding level will allow the investor to meet a defined financial objective without shortfall, usually estimated via simulation or long-term capital market assumptions.

GBI is typically embedded in an individual’s investment policy statement (IPS). Each goal has:

- A description and time horizon

- A priority ranking (essential, important, aspirational)

- A required probability of success (e.g., 90% for essentials, 70% for aspirational goals)

These inputs drive the risk level and asset allocation of the corresponding bucket.

Connecting LDI and GBI

Conceptually, GBI is the individual-investor analogue of LDI:

- For a DB plan, “essential” goals are contractual pension payments; for an individual, they are minimum retirement spending and debt service.

- The plan’s hedging portfolio is similar to the individual’s safety bucket; the plan’s return-seeking portfolio is analogous to the aspirational bucket.

- Both frameworks shift focus from maximizing return per unit of asset volatility to minimizing the risk of failing to meet specified spending or liability commitments.

Recognizing this parallel is useful in the exam: tools and language from the institutional LDI readings can often be applied, mutatis mutandis, to private wealth cases.

Building Goal Hierarchies: From Needs to Aspirations

The concept of a goal hierarchy is central to both LDI and GBI but takes a particularly practical form in private wealth.

Clients’ goals can be categorized, for example, as:

- Essential (basic needs): Retirement income to fund core living expenses, healthcare, and required debt repayments

- Important (lifestyle/extras): Private education for children, travel fund, home upgrades, discretionary consumption

- Aspirational: Large bequests, major charitable donations, funding multiple generations, luxury property

A goal hierarchy sets the order of funding and assigns required probabilities of success (for example, 95%+ for essentials, 75–85% for important goals, perhaps 60–70% for aspirations).

Key Term: Safety bucket

The safety bucket is the segment of a multi-bucket portfolio dedicated to funding essential, near- to medium-term goals with very high certainty, typically invested in low-risk, high-liquidity assets. Key Term: Lifestyle bucket

The lifestyle bucket is the portfolio segment that funds important but non-essential goals, usually with a medium-term horizon and moderate required probability of success, invested in balanced or moderate-risk assets. Key Term: Aspirational bucket

The aspirational bucket is the portfolio segment targeting discretionary, long-term, or legacy goals, where the investor is willing to accept higher volatility and a lower probability of success in exchange for higher expected returns.

In exam scenarios, constructing a hierarchy often requires you to:

- Identify all relevant goals from a case vignette (including implicit goals, such as maintaining real value of capital)

- Classify goals into essential, important, and aspirational based on description and consequences of failure

- Assign reasonable required probabilities and time horizons consistent with the client’s risk tolerance and capacity

Worked Example 1.1

Question: A retiree has $3,000,000 to fund her needs, desires $30,000 per year for basic living expenses (20-year horizon), $10,000 per year for travel (next 10 years), and hopes to leave a $1,000,000 bequest. How might a multi-bucket portfolio be constructed to support her goal hierarchy?

Answer:

A sensible hierarchy would treat minimum living expenses as essential, travel as important, and the bequest as aspirational.

- Bucket 1 (Safety – Essentials):

- Objective: Provide $30,000 per year (inflation-adjusted) for 20 years with high certainty (e.g., 95%+ probability).

- Implementation: Allocate sufficient capital—say, the present value of 20 years of spending—into low-risk fixed income: short- to intermediate-duration, high-quality bonds, TIPS, and possibly a laddered bond portfolio to match annual cash flows. This is analogous to an LDI hedging portfolio.

- Bucket 2 (Lifestyle – Important):

- Objective: Provide $10,000 per year for travel over 10 years, with moderate probability (e.g., 80%).

- Implementation: Invest the present value of expected travel spending in a diversified balanced portfolio (for example, 40–60% equities, 40–60% bonds) to balance growth and risk over the medium term.

- Bucket 3 (Aspirational – Bequest):

- Objective: Target a $1,000,000 bequest at death, accepting uncertainty about timing and success probability (e.g., 60–70%).

- Implementation: Allocate all remaining assets to a growth-oriented portfolio, dominated by global equities and possibly illiquid growth assets (private equity, real estate) if liquidity and client constraints permit.

The precise allocations would be determined by present value calculations and capital market assumptions, but the key is mapping each goal to a bucket with appropriate risk and instruments.

Worked Example 1.2

Question: A client has three goals: (1) maintain current living standards over retirement (30-year horizon), (2) fully fund a grandchild’s university tuition starting in 8 years, and (3) make a large charitable donation if markets perform very well. Assume her risk tolerance is average, and she has more than enough wealth to fund (1) and (2) comfortably. Rank the goals and suggest reasonable required probabilities of achievement.

Answer:

- Living standards over 30 years are essential; shortfall would materially damage her welfare. A required probability of achievement around 90–95% is reasonable.

- Funding tuition in 8 years is important, but failure might be mitigated with loans or partial funding. A required probability of 80–90% fits an average risk tolerance.

- The charitable donation is aspirational, dependent on market performance and surplus wealth. A required probability of 60–70% is typical, acknowledging that the donation may be scaled down or forgone if markets are weak.

This ranking drives bucket design: goal (1) primarily in the safety bucket, goal (2) partly in the lifestyle bucket with some growth, and goal (3) in the aspirational bucket with higher equity exposure.

Multi-bucket Portfolios: Segmenting Money with a Purpose

A multi-bucket portfolio divides client assets into distinct sub-portfolios ("buckets"), mapped to the specific goals and timeframes identified in the goal hierarchy. This leverages investors’ natural tendency toward mental segmentation while keeping the overall strategy coherent.

Key Term: Bucket approach

The bucket approach is the practice of dividing assets into separate pools, each matched to specific liabilities or goals, with distinct risk/return profiles and funding rules.

Common segmentation might include:

- Safety bucket: Low-risk assets to fund essential, near-term living expenses

- Lifestyle bucket: Moderately risky assets supporting important but non-essential goals with a medium-term horizon

- Aspirational bucket: Long-term, higher-risk investments targeting discretionary or legacy objectives

This structure enables a clear mapping between portfolio assets and client priorities, making it easier to explain trade-offs and to maintain discipline during market stress.

Asset Selection within Each Bucket

Aligning asset characteristics with each bucket’s objective is critical:

- Safety bucket:

- Asset types: cash, money market funds, high-quality short- and intermediate-term bonds, TIPS, and sometimes annuities.

- Risk characteristics: low volatility, short duration, high liquidity, strong negative or low correlation with equities.

- Techniques:

- Short duration matching to near-term spending

- Inflation protection via TIPS where real spending is the objective

- Currency matching when liabilities are denominated in a specific currency

Key Term: Laddered bond portfolio

A laddered bond portfolio spreads bond maturities roughly evenly across a range of years, providing diversified cash flows over time and balancing reinvestment risk against price risk.

Laddered portfolios are particularly useful in safety buckets: maturing bonds naturally fund spending, and reinvestment at the long end of the ladder maintains approximate duration.

-

Lifestyle bucket:

- Asset types: balanced portfolios combining equities and high-quality bonds, possibly including REITs or diversified alternatives.

- Risk characteristics: moderate volatility, diversified sources of return, greater growth potential than the safety bucket.

- Objective: maintain or improve lifestyle while being resilient to market shocks.

-

Aspirational bucket:

- Asset types: public equities, private equity, real estate, high-yield credit, and other growth assets; limited liquidity is more acceptable.

- Risk characteristics: higher volatility, drawdown risk, and potentially higher correlation with equities, but with higher expected returns.

- Objective: maximize expected value of aspirational outcomes, accepting lower probability of success.

Capital market history supports this segmentation. For example, government bonds have had negative or low correlation with equities over many periods, making them suitable for safety buckets, whereas private equity and hedge funds tend to have high correlation and higher beta to equities, making them more suitable for aspirational allocations.

Matching Asset Characteristics to Liabilities and Goals

For both LDI and GBI, an important step is matching asset risk and cash flow characteristics to specific liabilities or goals:

-

Duration matching: For a known liability at time , you can approximate the required present value:

where is an appropriate discount rate (e.g., the yield on a bond of similar maturity and credit quality). In institutional LDI, long-duration corporate or government bonds are used to hedge interest rate sensitivity of long-term pension liabilities.

-

Inflation matching: Real goals (e.g., maintaining living standards) are often best hedged with inflation-linked bonds or real assets (real estate, infrastructure, commodities) whose cash flows tend to rise with inflation.

-

Currency matching: Goals denominated in a specific currency (e.g., tuition in a foreign country) should be funded in that currency or hedged with derivatives to avoid uncompensated currency risk.

In a constructed-response question, you may need to recommend specific asset classes for each bucket and justify them by referencing duration, inflation sensitivity, correlation, and liquidity features.

Worked Example 1.3

Question: A DB pension plan has a duration of liabilities of 15 years and a funding ratio of 120%. The sponsor is risk-averse and wants to reduce the probability that the plan ever becomes underfunded. Which high-level LDI structure is most appropriate?

Answer:

With a strong funding ratio (120%) and a risk-averse sponsor focused on avoiding future underfunding, the plan should emphasize a liability-hedging structure.

- The core of the portfolio should be a hedging portfolio of long-duration, high-quality bonds (and possibly interest rate swaps) with approximate duration of 15 years to match liabilities.

- A smaller return-seeking portfolio can remain invested in growth assets, but its weight should be limited because the plan already has a surplus.

This is best described as a hedging/return-seeking portfolios approach within an LDI framework, possibly combined with surplus optimization to fine-tune the allocation along a surplus-efficient frontier. A pure asset-only approach would not align with the sponsor’s desire to minimize underfunding risk.

Key Steps in Goal-based and Multi-bucket Portfolio Construction

When designing a goal-based or multi-bucket portfolio, a structured process helps ensure internal consistency and exam-ready justifications.

Defined benefit pension liability management proceeds from liability and funding-ratio analysis to surplus optimization, two-portfolio construction, or integrated asset-liability management.

-

Identify and categorize all financial goals

- Specify each objective (amount, timing, currency, and whether amounts are real or nominal).

- Distinguish between one-off goals (e.g., home purchase) and ongoing goals (e.g., annual retirement spending).

- For individuals, recognize that the true time horizon for retirement goals extends beyond retirement date to expected life (or joint life) expectancy.

-

Rank and assign probabilities

- Classify goals by importance (essential, important, aspirational).

- Assign a minimum acceptable probability of goal achievement for each goal, consistent with the client’s risk tolerance and capacity.

- Remember that higher required probabilities imply lower feasible risk and often larger required funding.

-

Determine required assets

- For each goal or bucket, calculate the present value of required spending at the target probability.

- At Level 3, you may not be asked for detailed Monte Carlo calculations, but you should:

- Recognize that lower-risk portfolios reduce both expected return and the volatility of outcomes.

- Explain trade-offs: for example, funding an endowment’s 5% real spending rate may require a higher allocation to growth assets despite increased volatility.

-

Select asset allocation and instruments for each bucket

- Choose asset classes and risk levels based on time horizon, risk tolerance, and liquidity needs.

- Map short-horizon essential goals to low-risk, high-liquidity assets; longer-horizon aspirational goals to high-return, higher-volatility assets.

- Consider implementation vehicles (individual securities, mutual funds, ETFs, or derivatives) consistent with the client’s constraints and tax situation.

-

Implement funding rules and rebalancing policy

- Define which bucket receives new contributions and how withdrawals are prioritized (usually from the safety bucket first for near-term spending).

- Establish rebalancing guidelines between buckets—for example, periodically moving gains from aspirational to safety buckets when markets have been favorable, or temporarily suspending contributions to aspirational buckets when funding of essentials is threatened.

-

Monitor and revise

- Reassess goals, funding status, and risk tolerance periodically, and after major life or market events.

- Adjust bucket allocations when goals are added, dropped, or materially redefined, or when the funding ratio for essential goals changes significantly.

Articulating these steps clearly and concisely is often the difference between partial and full credit on constructed-response questions.

Behavioral and Practical Considerations

Behavioral biases affect goal prioritization and adherence to planned allocations. The multi-bucket framework, if used thoughtfully, can harness rather than fight these tendencies.

Key Term: Mental accounting

Mental accounting is the tendency of individuals to categorize and treat money differently depending on its source or intended use, often leading to separate “mental” portfolios rather than viewing wealth holistically. Key Term: Loss aversion

Loss aversion refers to investors’ tendency to experience losses more intensely than gains of the same magnitude, leading them to avoid strategies that have a high probability of short-term losses even when they improve long-term outcomes. Key Term: Hyperbolic discounting

Hyperbolic discounting is the behavioral bias whereby individuals disproportionately prefer immediate rewards over larger future rewards, causing them to underweight long-term goals relative to short-term consumption.

Common behavioral effects relevant for GBI include:

-

Mental accounting: Multi-bucket portfolios intentionally formalize mental accounts: clients can see a “retirement income bucket” separate from a “legacy bucket.” This often increases adherence because clients are less likely to raid essential spending assets for discretionary consumption.

-

Loss aversion: Clients may want more assets in the safety bucket than mathematically necessary because shortfalls in basic needs are intolerable. On the exam, it is usually appropriate to respect this preference within reason, as it reflects legitimate risk aversion and low tolerance for drawdowns in essential spending.

-

Hyperbolic discounting: Clients may overweight near-term lifestyle spending or luxuries at the expense of long-term retirement or legacy goals. A goal hierarchy helps counteract this by making the trade-offs explicit: funding aspirational short-term goals might visibly reduce funding for essential long-term goals.

Worked Example 1.4

Question: An individual is worried about market volatility eroding essential retirement income. How can a multi-bucket approach address this behavioral concern?

Answer:

The adviser can use a multi-bucket structure to separate essential spending from market volatility:

- Create a safety bucket that holds several years (for example, 5–10 years) of essential retirement expenses in low-volatility, high-quality fixed income and cash, possibly in a laddered bond portfolio.

- Clearly communicate that this bucket is dedicated solely to funding basic needs and is largely insulated from equity market swings.

- Invest the remaining assets in lifestyle and aspirational buckets with higher equity exposure, emphasizing that short-term fluctuations in these buckets do not threaten essential spending.

This design directly addresses loss aversion and mental accounting by giving the client a visible, stable pool of assets for essentials, reducing the temptation to panic-sell growth assets during downturns.

Exam Warning: In the exam, do not assume that all buckets must hold risk-free assets. The appropriate risk level and investment horizon should be matched to the specific goal, with higher-risk allocations reserved for lower-priority or long-term goals. Mislabeling aspirational goal buckets as needing high certainty is a common mistake. Equally, do not force a mathematically “optimal” solution that ignores the client’s stated low tolerance for volatility in essential goals.

Applying Buckets and Hierarchies: Institutional and Private Contexts

The goal hierarchy and bucket concepts apply, with appropriate adaptation, to both institutional and private clients.

Institutional LDI: Defined Benefit Pension Plans

For DB pension plans:

-

Goal hierarchy:

- Essential: meeting contractual pension payments.

- Important: maintaining an acceptable funding ratio and contribution stability.

- Aspirational: reducing sponsor contributions or allowing contribution holidays.

-

Buckets:

-

Hedging portfolio (safety bucket analogue):

- Long-duration government and corporate bonds, interest rate and inflation swaps designed to track liability behavior.

- Objective: stabilize the funding ratio and limit surplus volatility.

-

Return-seeking portfolio (aspirational bucket analogue):

- Global equities, private equity, real estate, credit, and other growth assets.

- Objective: increase expected surplus and reduce long-term contribution costs.

-

As the funding ratio improves or the plan closes to new members, many sponsors adopt glide paths that gradually shift assets from the return-seeking to the hedging portfolio, analogous to shifting wealth from aspirational to safety buckets for individuals nearing retirement.

Institutional LDI: Banks and Insurers

While banks and insurers are not usually framed in explicit “buckets,” the same logic applies:

- For insurers, the general account is invested to meet policyholder claims (essential) and grow surplus (aspirational). Their IPS explicitly mentions balancing short-term liquidity with long-term surplus growth, similar to funding essential and aspirational goals.

- For banks, liquidity regulations and deposit structures create short-horizon essential liabilities, requiring a substantial allocation to highly liquid, low-risk assets, while equity capital and retained earnings support more risk-taking in loans and trading activities.

In an exam context, you might be asked to recognize that these institutions effectively use LDI principles, even if they do not label them as goal-based or bucketed.

Private GBI: Individuals and Families

Individuals with multiple financial objectives can benefit from buckets mapped to their own goal priority:

-

Safety bucket:

- Essential living expenses, mortgage payments, health insurance premiums.

- Invested in cash, short-term bonds, TIPS, and possibly immediate annuities.

-

Lifestyle bucket:

- Travel, education funding, home renovation, moderate philanthropy.

- Invested in diversified multi-asset portfolios with moderate risk.

-

Aspirational bucket:

- Large charitable bequests, multi-generational wealth transfer, concentrated business holdings, high-risk investments.

- Invested in growth assets; may accommodate concentrated positions if the client accepts the associated risk.

Goal hierarchies and buckets are often integrated directly into the IPS for private clients, with time horizons, target allocations, and rebalancing rules specified for each bucket.

Monitoring, Rebalancing, and Revising Bucket Allocations

The design of goal hierarchies and buckets is not static. Ongoing monitoring and revision are essential to both LDI and GBI.

Key considerations:

-

Funding status and drift:

- For DB plans, track the funding ratio and surplus volatility. When the plan becomes better funded than targeted, shift some assets from return-seeking to hedging portfolios (de-risking).

- For individuals, track whether the safety bucket continues to cover a sufficient number of years of essential spending; if markets do well, top it up by crystallizing gains from aspirational buckets.

-

Market conditions:

- Large, persistent changes in interest rates, inflation expectations, or asset class valuations may warrant adjustment of hedging assets (e.g., duration) or growth allocations.

- However, avoid frequent tactical changes inconsistent with the IPS; the focus should remain on goal achievement, not short-term performance.

-

Changes in goals or constraints:

- Life events (retirement, inheritance, birth of children, health shocks) often change the hierarchy of goals.

- Behavioral changes—such as increased risk aversion after a large drawdown—may justify increasing safety bucket size, even if mathematically suboptimal.

-

Rebalancing policy:

- Establish threshold-based or time-based rebalancing rules for each bucket, and between buckets.

- For example, if equities in the aspirational bucket outperform and the bucket exceeds its target weight by more than a specified threshold, harvest gains and add to safety or lifestyle buckets.

In constructed-response answers, clearly linking changes in allocation to shifts in funding status, time horizon, and client preferences is essential for full credit.

Summary

A liability-driven or goal-based framework uses explicit goal hierarchies and bucketed portfolios to closely align asset allocation with the timing, importance, and risk tolerance of specific financial objectives. This approach is applicable to both institutions with known liabilities and individuals with prioritized goals. The bucket strategy improves risk management, behavioral adherence, and communication between adviser and client, supporting higher odds of meeting essential financial needs.

For Level 3, your task is to combine these ideas: classify goals, assign probabilities, design hedging and return-seeking buckets (or safety, lifestyle, and aspirational buckets), select appropriate assets based on risk characteristics and liability profiles, and explain how and why to adjust allocations over time.

Key Point Checklist

This article has covered the following key knowledge points:

- Liability-driven investing aligns portfolios to future defined liabilities or goals, measuring risk in terms of surplus volatility and funding status

- Goal hierarchies prioritize objectives by urgency, importance, and required confidence level

- Multi-bucket portfolios segregate assets into sub-portfolios matched to goal timing, importance, and risk tolerance

- Essential goals receive higher probability and lower risk allocation; aspirational goals accept more risk and lower required certainty

- Asset characteristics—duration, inflation sensitivity, currency, liquidity—should be matched to specific liabilities or goals

- Behavioral biases, such as mental accounting, loss aversion, and hyperbolic discounting, impact goal prioritization and can be addressed in bucket design

- Both institutional (e.g., pensions, insurers) and private client portfolios use structures analogous to safety/hedging and aspirational/return-seeking buckets

- Monitoring, rebalancing, and dynamic de-risking are essential to maintaining alignment between assets, liabilities, and changing client objectives

Key Terms and Concepts

- Liability-driven investing (LDI)

- Goal-based investing (GBI)

- Goal hierarchy

- Multi-bucket portfolio

- Funding ratio

- Immunization

- Probability of goal achievement

- Safety bucket

- Lifestyle bucket

- Aspirational bucket

- Bucket approach

- Mental accounting

- Loss aversion

- Hyperbolic discounting