Learning Outcomes

This article explains macroeconomic frameworks relevant to investment management, including:

- How to describe and compare the main phases of the business cycle and associated macro characteristics.

- How to link growth, the output gap, and potential output to inflation dynamics and policy objectives.

- How monetary policy tools influence short-term rates, longer-term yields, credit conditions, and risk premia across the cycle.

- How fiscal policy choices and constraints interact with monetary actions to shape the overall policy mix.

- How policy credibility, inflation expectations, and term premia transmit into the shape and shifts of the yield curve.

- How international linkages propagate shocks, policy moves, and business cycle turning points across economies and asset classes.

- How different cycle stages typically affect relative performance of equities, government bonds, credit, and real assets.

- How to incorporate business cycle analysis into capital market expectations, scenario design, and top‑down asset allocation.

- How to recognize common exam traps when interpreting macro data, policy announcements, and market reactions in vignette questions.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand macroeconomic foundations that underpin investment decisions, with a focus on the following syllabus points:

- Analyze the phases of the business cycle and their market implications

- Explain drivers of economic growth and long-term inflation

- Evaluate the effects of monetary and fiscal policies through the cycle

- Assess the role of policy mix and global interactions on yield curves and asset returns

- Interpret macroeconomic indicators for use in capital market forecasts

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- How does the phase of the business cycle typically influence equity and bond returns?

- Which economic variable acts as both an indicator and a target for central bank policy?

- What is the difference between a countercyclical and procyclical variable?

- Why are changes in the policy rate not always fully transmitted to longer-term bond yields?

Introduction

Macroeconomic analysis provides essential context for forecasting capital market returns and portfolio risk. Investment strategy must consider the business cycle, the drivers of long-term growth, the evolution of inflation, and the interactions of fiscal and monetary policies. A structured macro framework helps anticipate changes in return opportunities and risk premia over both cyclical and secular horizons.

Key Term: business cycle

The sequence of expansion, peak, contraction, and trough that characterizes fluctuations in aggregate economic activity and impacts asset returns. Key Term: monetary policy

Central bank actions—primarily interest rate changes and liquidity operations—aimed at influencing the level of economic activity and inflation. Key Term: fiscal policy

Government budget-setting and spending decisions used to affect overall demand and economic output.Test Tip: When revising Growth inflation and policy interactions, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Cyclical Growth Patterns and the Business Cycle

Economic growth is not linear. Instead, economies move through recurring business cycle phases:

- Expansion: Increasing growth, falling or low unemployment, and rising output. Investment demand, profits, and inflation pressures steadily increase. Risk assets usually outperform.

- Peak: The economy operates near capacity. Inflation pressures rise. Tight policy may trigger a slowdown.

- Contraction: Output declines or slows, unemployment rises, credit tightens, and risk assets typically underperform. Deflation or disinflation risks increase.

- Trough: The bottoming-out phase. Monetary and/or fiscal stimulus begin to support recovery. Once excess capacity declines, the next expansion starts.

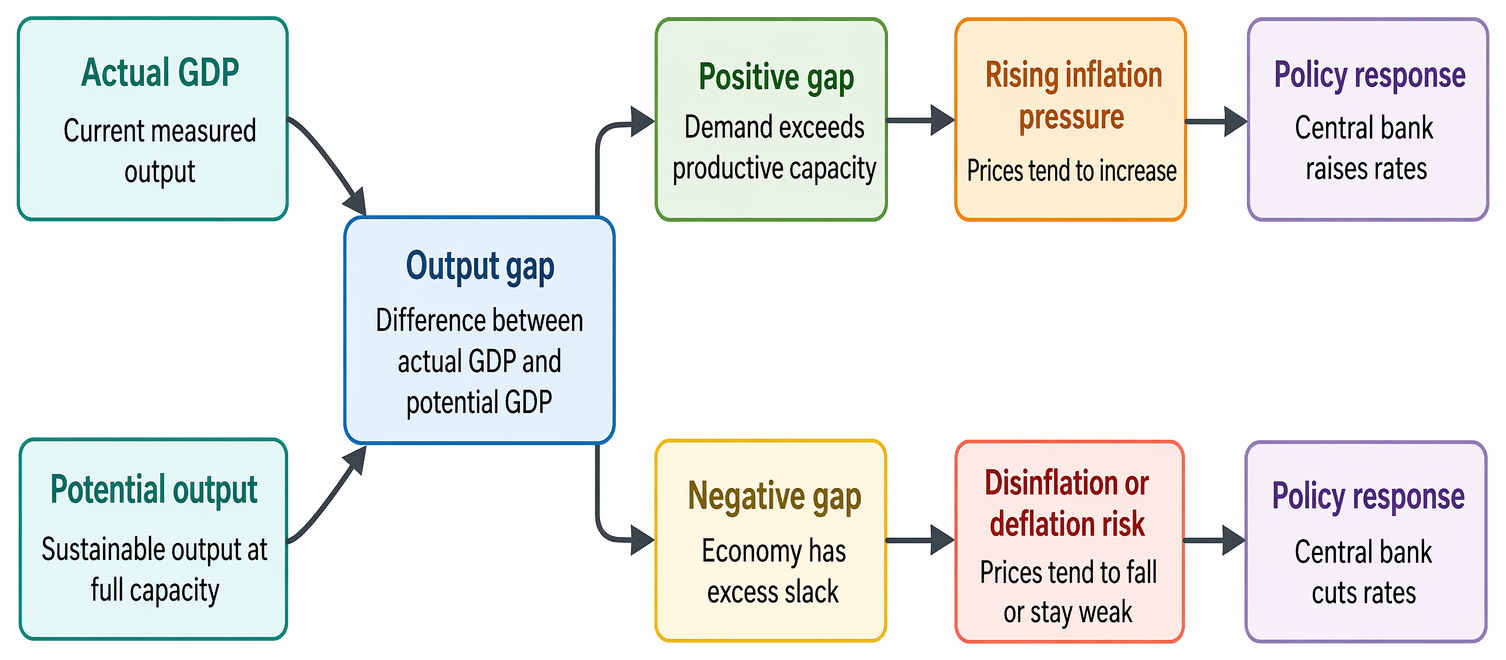

Key Term: output gap

The deviation of actual GDP from potential, signifying excess demand (positive gap) or excess supply (negative gap).

Growth, Inflation, and Long-Term Policy Objectives

Stable, sustainable per-capita growth is the main objective for long-term policy. However, economies are also subject to cyclical and structural shocks:

- Productivity growth and population determine the long-run trend, but in the shorter term, growth fluctuates as investment, employment, and inventories respond to changing expectations.

- Inflation arises when aggregate demand grows more quickly than productive capacity, especially late in an expansion.

Key Term: potential output

The level of output an economy can sustain at full employment without upward price pressures.

Macroeconomic Policy Interactions

Monetary and fiscal decisions interact dynamically with growth and inflation at every stage of the cycle.

Monetary Policy

Central banks adjust the policy rate (and other tools) to target low, stable inflation and support full employment:

- Easing (lower rates): Adopted in downturns or when growth is weak.

- Tightening (higher rates): Used when growth is strong and inflation is a threat.

The transmission from policy rate to long-term interest rates may be incomplete if markets anticipate policy reversals, fiscal changes, or external shocks.

Fiscal Policy

Governments use tax/spend decisions to complement, bolster, or offset monetary actions:

- Expansionary fiscal policy (increased spending, lower taxes): Stimulates demand, especially when private sector activity is weak.

- Contractionary policy (higher taxes, lower spending): Used in overheating or strong expansion to prevent an unsustainable rise in inflation or debt.

Policy Mix and Coordination

The combination of both policies—the overall policy mix—influences the steepness and timing of the economic cycle, as well as the shape of the yield curve, risk premia, and currency moves.

Key Term: policy mix

The combination of fiscal and monetary stances; can be reinforcing or opposing, shaping macro outcomes and financial market trends.

Inflation Trends and Yield Curve Implications

As the output gap narrows, inflation accelerates, particularly for inputs in short supply. When central banks are credible, inflation expectations remain anchored; if not, rising expectations lead to higher long yields and risk premia.

Actual GDP relative to potential output determines positive or negative output gaps, linking cyclical inflation dynamics to monetary tightening or easing.

- Early expansion: Falling real rates and rising risk appetite steepen the yield curve.

- Late expansion: Tightening policy and inflation risk flatten or invert curves as markets anticipate a slowdown.

- Recessions: Easing policy, falling inflation, and low term premia restore a steep curve.

Key Term: yield curve

The relationship between yields and maturities for government bonds; reflects expectations for policy, growth, and inflation.

Worked Example 1.1

Scenario: The central bank lowers its policy rate during a contraction, but the yield on 10-year government bonds falls only slightly, and corporate spreads widen.

Answer:

This outcome is typical of late contraction when risk aversion is high. Even as policy eases, investors demand more compensation for credit risk and are skeptical about the pace of recovery. The yield curve flattens if markets anticipate a slow exit from recession, or steepens if aggressive stimulus is expected to succeed.

International Transmission and Linkages

Open economies transmit shocks and policies across borders via trade, capital flows, and exchange rates. A country's cycle may lag or lead the global cycle, creating opportunities for asset allocators.

Key Term: international linkages

The mechanisms by which macro shocks, policy changes, and market returns transmit between economies, influencing global asset values.

Policy Constraints and Limitations

Constraints may restrict the effect of macro policy:

- At the zero lower bound, central banks use unconventional tools (e.g., quantitative easing).

- Fiscal space may be limited by high debt or political constraints.

- External shocks (commodity prices, geopolitics, pandemics) can overwhelm the influence of domestic policy.

Worked Example 1.2

Scenario: Policy rates are near zero, and fiscal stimulus is limited by debt. Growth is weak and inflation is below target.

Answer:

The economy may encounter a "liquidity trap." Non-standard tools (forward guidance, asset purchases) are used, but with diminished effects. The commitment and credibility of future policy, and the response of other economies, will heavily affect expectations and asset prices.Exam Warning: Overreliance on asset class mean returns from one cycle phase is a common error. Ensure you explicitly consider both the current stage and the expected transition when using business cycle analysis for forecasts.

Capital Market Expectations and Investment Implications

Asset returns are cyclical and linked to the macro environment:

- Equities: Tend to outperform early and mid expansion as growth and earnings accelerate, but underperform late cycle when tightening begins.

- Bonds: Outperform into and during contractions as rates fall and inflation eases, providing a hedge.

- Credit and yield curve: Credit spread compression is most pronounced early in recovery; late in expansion, spread widening and curve flattening typically precede recessions.

- Real assets: Real estate and commodities are inflation and growth-sensitive; performance depends on both phase and shock type.

Worked Example 1.3

Scenario: An investor shifts from a neutral to a defensive allocation, expecting a late-cycle slowdown with rising inflation and central bank tightening.

Answer:

The investor should consider reducing cyclical equity exposures, increasing weight to defensive sectors, favoring quality credit, and possibly extending fixed-income duration as a partial hedge. Real asset allocations may help if inflation risk is pronounced.

Summary

Macro frameworks enable CFA candidates to apply cycle analysis to market forecasts and investment strategy. Growth, inflation, and policy choices interact at every stage to create cyclical and structural opportunities and risks. Effective allocation requires recognizing the cycle phase, the likely interaction of fiscal and monetary actions, and global linkages.

Key Point Checklist

This article has covered the following key knowledge points:

- Describe main business cycle phases and their return implications

- Assess growth, potential output, and inflation risks in cycle analysis

- Evaluate monetary, fiscal, and policy mix effects through the cycle

- Understand yield curve shifts in response to macro policy and the cycle

- Apply linkages and macro analysis to capital market expectations and scenarios

Key Terms and Concepts

- business cycle

- monetary policy

- fiscal policy

- output gap

- potential output

- policy mix

- yield curve

- international linkages