Learning Outcomes

This article explains how to design and apply a robust manager selection and monitoring process for CFA Level 3–relevant portfolios. It defines the objectives and core components of investment and operational due diligence, distinguishing between strategy assessment, business risk review, and alignment of interests. It explains how to screen managers using performance, risk, and style metrics, and how to interrogate investment philosophy, portfolio construction, and risk controls in a structured meeting agenda. It details how to evaluate fee structures—base fees, performance fees, carried interest, and expense pass-throughs—quantify their impact on net returns, and compare competing managers on a like‑for‑like, net‑of‑fee basis. It discusses negotiation levers such as tiered fees, high‑water marks, and appropriate benchmarks, emphasizing exam‑relevant arguments for or against specific arrangements. It examines how to structure ongoing monitoring, including performance review, style‑drift analysis, governance and personnel tracking, and formal watch‑list and termination protocols. It highlights common red flags in due diligence and monitoring and shows how they should influence written recommendations in vignette-style questions.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand how to select and monitor external investment managers, with a focus on the following syllabus points:

- The objectives and components of manager due diligence (operational, investment, risk, compliance, firm culture)

- Key fee structures, their negotiation, and their implications for net performance

- The ongoing monitoring and review process for managers

- Warning signs and risk factors that require further investigation or possible termination

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the principal elements of a manager due diligence process, and why is each important?

- Which types of manager fees most directly erode investor net returns, and how can they be controlled?

- What are the warning signs that a hired manager may require closer review or even removal?

- Why is it necessary to analyze both operational and investment aspects when evaluating a manager?

Introduction

Selecting and continuously monitoring investment managers is a core responsibility for institutional and private investors who delegate investment decisions. The consequences of a poor manager choice or ineffective monitoring can be severe, including outsized losses, underperformance, reputational damage, or fraud. A robust due diligence process—covering both investment processes and business operations—is essential before hiring, and ongoing oversight is critical for accountability, risk management, and performance.

Key Term: due diligence

A structured process for investigating, verifying, and evaluating investment managers before engagement and while assets are assigned, examining investment process, operations, risk, compliance, controls, and culture. Key Term: performance fee

A variable fee paid to an investment manager that is based on the portfolio's realized performance, commonly structured as a percentage of profits above a hurdle or benchmark return. Key Term: base fee

The fixed portion of fees, typically charged as a percentage of assets under management, regardless of portfolio performance.

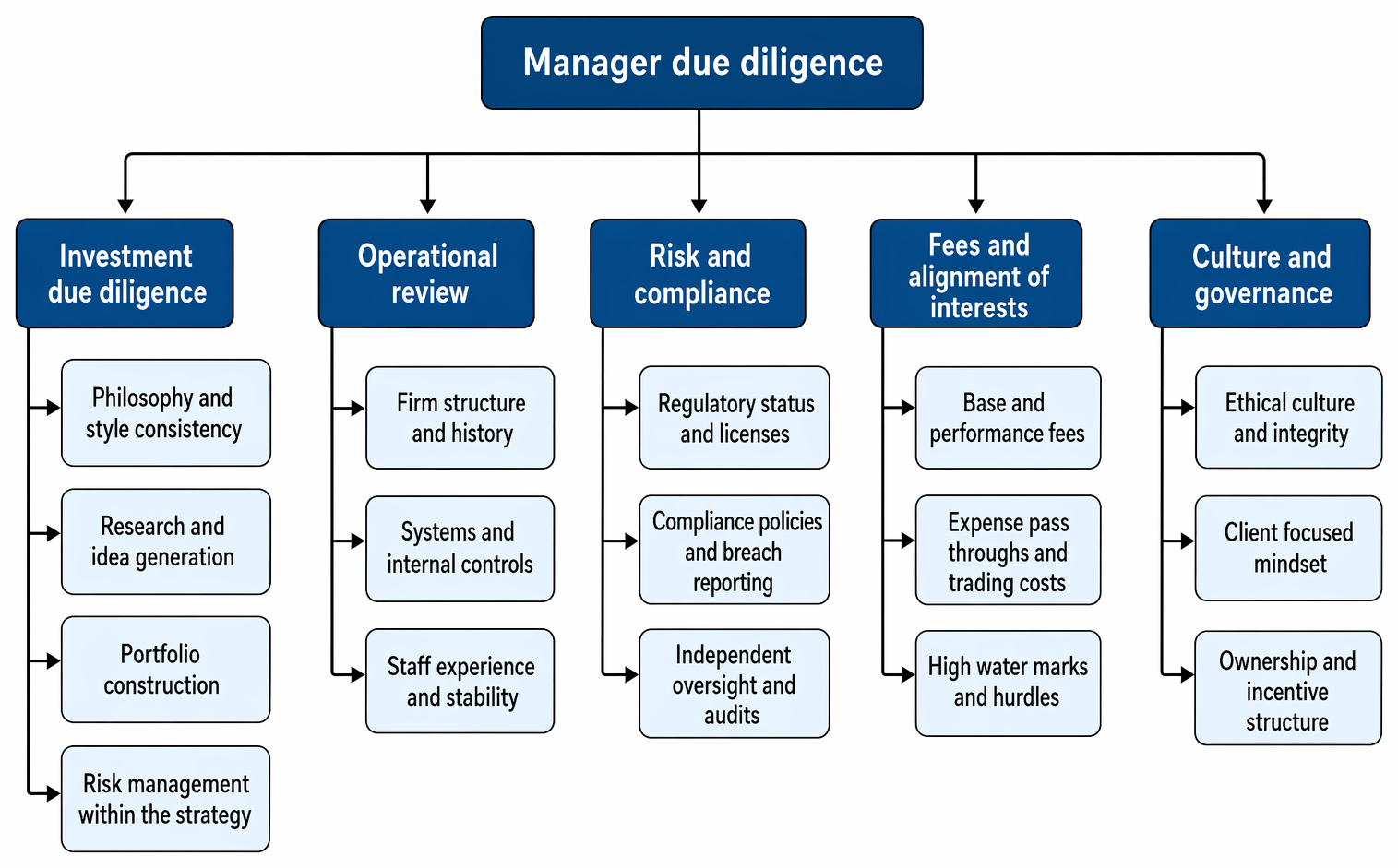

DUE DILIGENCE IN MANAGER SELECTION

Selecting a third-party manager requires careful appraisal of both quantitative and qualitative factors. A sound process is repeatable, objective, and minimizes biases. The due diligence evaluation is typically structured in the following steps:

1. Initial Screening

Short-list only those managers whose performance and style align with the investor’s objectives, constraints, and policy. This often involves comparing historic and risk-adjusted returns, assessing strategy fit, checking credentials, and confirming regulatory status.

2. Investment Process Review

Evaluate how the manager generates returns, including philosophy, process, people, and implemented controls. Confirm the decision-making approach, portfolio construction method, and risk controls.

3. Operational Due Diligence

Review the firm's structure, history, systems, compliance, disaster recovery procedures, client service arrangements, and controls over trading, valuation, and reporting. Check the experience and stability of senior staff.

Key Term: operational due diligence

A systematic review of a manager’s business infrastructure, operations, legal, and compliance capabilities to identify weaknesses, fraud risks, or conflicts of interest.

4. Fee Structure and Expense Analysis

Understand all fees and costs: management fees, performance fees, soft dollar arrangements, trading costs, fund-level expenses, and negotiation opportunities. Assess how much these fees impact net returns and whether they align interests appropriately.

Key Term: fee structure

The full schedule of charges—both fixed and incentive-based—that investors pay to an investment manager, including management fees, performance fees, and ancillary costs.

5. Risk Controls and Compliance

Assess whether the manager’s controls can effectively limit operational and investment risks. Confirm compliance policies and how breaches are reported to clients. Seek evidence of independent oversight, from either third-party audits or governance boards.

6. Client Reporting and Transparency

Determine the adequacy, timeliness, and clarity of periodic reporting, including performance attribution, risk exposures, and compliance status.

Worked Example 1.1

Question: Suppose you are evaluating two global equity managers. Both have five-year annualized returns within 25 basis points of each other. Manager X charges a 2% base fee and uses a high-water-marked 20% performance fee, while Manager Y charges only a 1% base fee with no incentive fee. Which manager is likely more cost-efficient for a long-term, index-oriented portfolio mandate, and why?

Answer:

Manager Y is likely more cost-efficient for a long-term, index-oriented mandate. The 2% base fee and performance fee charged by Manager X will likely erode net returns, especially if the strategy only tracks the benchmark with little alpha. Manager Y's lower base fee reduces the drag on returns. Performance fees can be justified if persistent alpha is high, but must be carefully linked to relevant benchmarks and hurdles. Investors must analyze both historic outperformance and fee structures to avoid paying excessively for beta.Exam Warning: Many CFA candidates incorrectly assume that a high historical return alone is sufficient for manager selection. For the exam, always emphasize the due diligence evaluation process, including operational review, fee evaluation, and alignment of interests, before recommending a manager.

FEE EVALUATION, NEGOTIATION, AND ALIGNMENT

Fees and expenses often have a greater impact on net performance than small differences in alpha. Investors should:

Manager due diligence is structured across investment, operations, risk and compliance, fees, and culture and governance, with representative review items.

- Thoroughly review the full fee schedule and ask for all-in estimates (including indirect costs).

- Seek performance-based fees that are carefully aligned—such as high-water marks, hurdles above cash or benchmark, and capped upside for the manager.

- Favor lower fixed base fees for strategies that mainly deliver market beta.

- Prefer fees calculated on net asset value, not committed or gross asset value (especially in private assets).

- Scrutinize expense pass-throughs, soft dollar arrangements, and undisclosed trading or research fees.

- Incorporate expected fees into performance projections and manager comparisons.

Key Term: high-water mark

A clause in performance fee structures that requires the manager to recoup prior losses before additional incentive fees are paid.

Worked Example 1.2

Question: A pension fund is offered two private equity fund investments. Fund A charges a 2% fee on committed capital for the first five years and 20% carried interest above an 8% annual preferred return. Fund B charges 1.5% only on invested capital and 15% carried interest above a 7% hurdle. How might these differences affect the pension’s net return profile?

Answer:

Fund A’s 2% fee on committed capital can result in high fees on uninvested ("dry powder") sums, eroding net returns, especially during slow deployment. Fund B only charges fees on invested capital, so fees are more closely aligned to deployed assets. The lower carried interest and hurdle further improve net returns if performance is strong, but investors must also evaluate historical returns and risk controls, not just headline fees.

ONGOING MANAGER MONITORING

Due diligence does not end at selection. Ongoing monitoring includes:

- Tracking performance net of fees versus benchmarks and peers.

- Confirming that the manager adheres to their stated investment style and risk profile.

- Reviewing changes in team composition, firm ownership, or risk controls.

- Monitoring client service, reporting timeliness, and transparency.

- Investigating significant compliance issues, trading errors, or audit qualifications.

- Applying documented protocols for escalation, watchlisting, or possible termination.

Key Term: watch list

A formal list of investment managers who require heightened scrutiny due to performance, style drift, compliance, or business risk concerns. Key Term: style drift

When a manager deviates materially from their stated investment approach or benchmark, potentially increasing portfolio risk relative to policy.

Worked Example 1.3

Question: You have selected a hedge fund that generated strong relative returns for three years. After a change in senior personnel, returns have lagged, with higher volatility and less transparency in risk reports. What action should you take as part of ongoing monitoring?

Answer:

The manager should be subject to further review and potentially placed on a watch list pending detailed investigation. The change in personnel, poorer risk-adjusted returns, and decreased transparency are warning signs requiring assessment of whether the issues are temporary or structural. If concerns persist or intensify, escalation to probation or replacement may be necessary.Revision Tip: When comparing two managers, always evaluate both net-of-fee performance and qualitative risk controls. Do not rely only on past outperformance. Regularly document monitoring decisions and clearly align manager guidelines with fund policies.

Summary

Effective manager selection and monitoring require a systematic approach to due diligence, focusing on both investment and operational capabilities. Fee analysis should emphasize alignment and net return impact. Ongoing monitoring must track both quantitative and qualitative signals, with clear actions for persistent concerns or breaches. Rigorous, repeatable processes help protect client capital and improve the likelihood of achieving portfolio objectives.

Key Point Checklist

This article has covered the following key knowledge points:

- Steps and considerations in manager due diligence (investment, operational, compliance, risk)

- Principles of evaluating, comparing, and negotiating manager fee structures

- Importance of net-of-fee performance and alignment of interests

- Ongoing monitoring protocols—performance, risk controls, personnel, style drift, compliance

- Actions to take upon warning signs, including watchlisting and termination procedures

Key Terms and Concepts

- due diligence

- performance fee

- base fee

- operational due diligence

- fee structure

- high-water mark

- watch list

- style drift