Learning Outcomes

This article explains how concentrated equity positions arising from employee stock options and restricted stock units affect private wealth management, including:

- identifying key sources of concentration, employment, liquidity, information, and tax risk in ESO- and RSU-based compensation packages

- distinguishing structural features of ISOs vs NSOs and RSUs, and how these features drive valuation, exercise behavior, and tax outcomes for employees and founders

- assessing regulatory, plan, and contractual constraints (vesting schedules, blackout periods, Rule 144, and clawbacks) that limit diversification, hedging, or sale

- evaluating diversification, monetization, and hedging techniques—such as staged exercise and sale, completion portfolios, collars, prepaid variable forwards, and exchange funds—for different client objectives and constraints

- analyzing how tax timing, alternative minimum tax exposure, and estate planning considerations influence optimal strategies for managing employee equity awards

- integrating these elements to formulate exam-quality recommendations that balance risk reduction, liquidity needs, and after-tax wealth preservation in CFA Level 3 case scenarios

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand how concentrated positions—especially those due to employee compensation—create unique challenges for managing wealth, with a focus on the following syllabus points:

- Discussing the risks of concentrated stock positions, including market, company, and liquidity risk

- Comparing employee stock options (ESOs) and restricted stock units (RSUs) and their implications for risk management and diversification

- Evaluating strategies to diversify, hedge, or monetize concentrated positions originating from ESOs and RSUs

- Analyzing relevant tax, vesting, and regulatory constraints affecting risk reduction and sale

- Recommending appropriate solutions considering client-specific objectives, tax status, and legal/contractual restrictions

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which risk is typically highest for an employee’s concentrated stock position—market risk, company risk, or liquidity risk?

- What are the main differences in tax treatment between incentive stock options (ISOs) and non-qualified stock options (NSOs)?

- Name two strategies (other than outright sale) for reducing the risk of a concentrated position arising from employee stock options.

- Why might restricted stock units (RSUs) present a “double risk” for the employee in terms of both employment and share value?

Introduction

Some private clients build significant wealth through compensation packages involving company shares. Such concentrated positions—most commonly arising from employee stock options or restricted stock units—create unique risks and planning challenges. These instruments can represent a substantial portion of an individual’s net worth, but their value is often highly correlated with the client’s income and is subject to strict legal, tax, and regulatory restrictions. Managing such concentrations effectively is an essential skill for CFA candidates working in wealth management.

Key Term: concentrated position

A client’s investment holding in a single security or related securities that is significantly larger relative to their diversified wealth and creates disproportionate risk. Key Term: employee stock option (ESO)

A form of compensation giving an employee the right to purchase company shares at a stated price within a specified period, typically subject to vesting and other restrictions. Key Term: restricted stock unit (RSU)

A grant of company shares (or the right to company shares) to an employee, subject to vesting requirements; shares are delivered only upon completion of specific conditions or a certain period.

Risk Characteristics of Employee Concentrated Positions

Individuals holding significant ESOs or RSUs face several types of risk:

- Company-specific risk: Value is wholly dependent on company performance. Poor performance, scandals, or regulatory actions can sharply reduce value.

- Employment risk overlap: Termination may cause forfeiture of unvested shares/options and, in some cases, expiry of vested ESOs or loss of unvested RSUs.

- Lack of diversification: A large share of net worth is subject to the same risks as salary, bonuses, and future career prospects.

- Liquidity and transfer restrictions: Sale or hedging is often restricted by law or internal policies, sometimes for multi-year periods.

- Tax planning complexity: Vesting, exercise, and sale typically trigger various capital gain and income tax events.

Key Term: vesting

The process by which rights to ESOs or RSUs become irrevocable after meeting specified conditions, such as time of service or performance targets. Key Term: blackout period

A time window during which employees are prohibited from trading company securities, often around earnings releases or significant corporate events.

Understanding Employee Stock Options (ESOs)

ESOs give employees the opportunity to purchase company stock at a fixed price, usually equal to the market value on the grant date. ESOs can be classified as either incentive stock options (ISOs) or non-qualified stock options (NSOs), each with distinct tax and regulatory features.

- ISOs: May offer favorable tax treatment, but subject to holding period and other requirements.

- NSOs: Do not meet ISO criteria; exercised value is treated as ordinary income.

Key risk features:

- Must be exercised before expiry, sometimes only within 90 days of employment termination.

- Value is highly sensitive to stock volatility and may become worthless ("out of the money").

- Hedging by sale or derivative is often restricted by securities law, internal policy, or blackout periods.

Key Term: incentive stock option (ISO)

A type of employee stock option qualifying for special tax treatment under US law, provided certain holding and exercise requirements are met. Key Term: non-qualified stock option (NSO)

An employee stock option that does not qualify for ISO tax benefits; income from exercise is generally taxable as ordinary income.

Restricted Stock Units (RSUs): Risks and Features

RSUs are typically granted as a fixed number of shares (or equivalent value) which vest over time or upon meeting performance objectives. RSUs differ from options: even if the stock falls in value, the employee receives vested shares (though they may be worth less).

- If the employee leaves before vesting, units are usually forfeited.

- Once vested, shares may be subject to additional holding or sale restrictions.

- RSUs expose employees to downside risk (stock depreciation) with limited upside participation compared to options.

- RSUs may carry dividend rights if specified.

Key Term: double risk

Exposure to loss of both employment income and concentrated stock value, since negative business developments can simultaneously jeopardize job and equity wealth.

Constraints: Tax, Regulatory, and Plan Restrictions

Key restrictions affecting ESOs and RSUs include:

- Vesting schedules: Often multi-year. Early exercise or sale may not be permitted.

- Securities law constraints (e.g., Rule 144): Limit sale volume and require holding periods for insiders.

- Blackout periods: Employees may be prohibited from trading around sensitive periods.

- Clawback provisions: Companies may reclaim options/RSUs upon misconduct or restatement.

- Tax events: Income and capital gains arise at exercise/vesting/sale, depending on jurisdiction and plan type.

Worked Example 1.1

Scenario: A CFA candidate’s client is granted 10,000 NSOs with an exercise price of $20 and a 4-year vesting schedule. In year 5, with shares trading at $70, the client wishes to diversify.

Answer:

If the options have not expired, the client may exercise up to the vested amount and sell the shares, generating a taxable gain (market price minus exercise price, taxed as ordinary income). Remaining unexercised options continue to provide equity upside. However, if the client is subject to a blackout period, sale may be delayed; market movements could erase the unrealized option value prior to exercise and diversification.

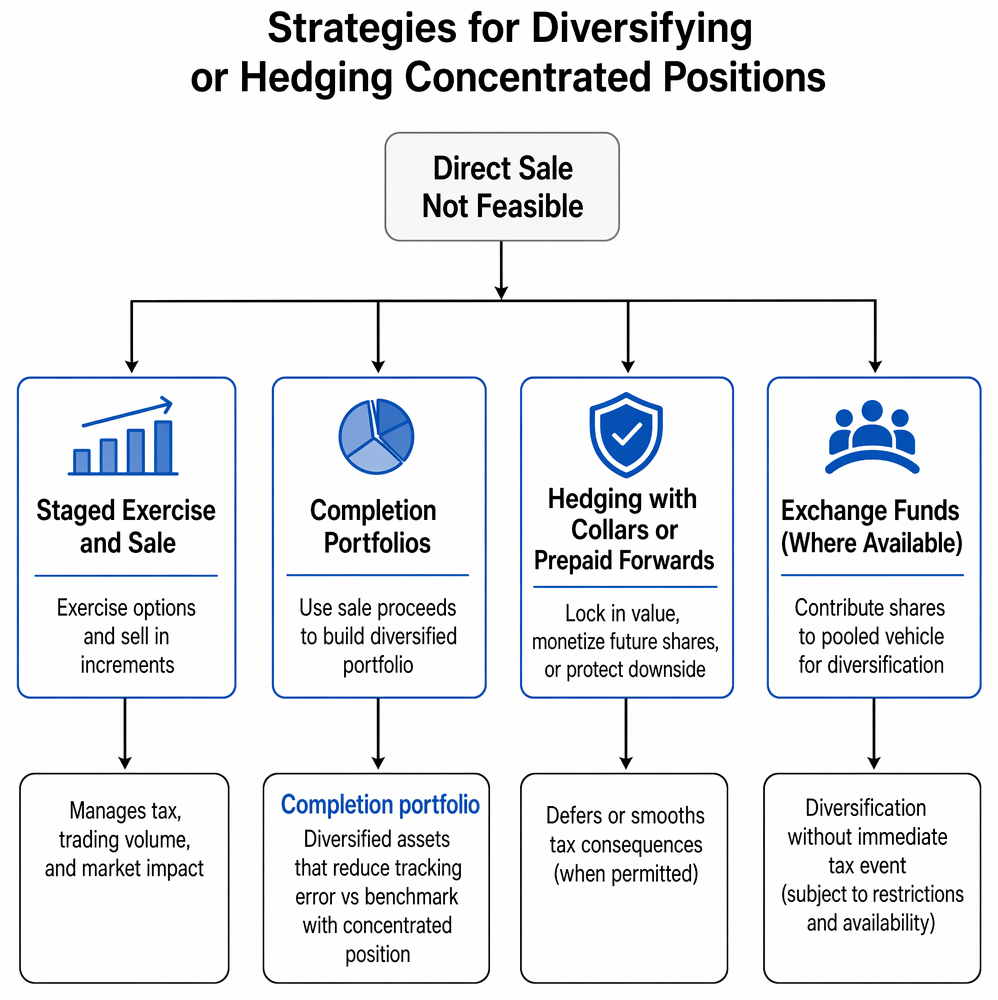

Strategies for Diversifying or Hedging Concentrated Positions

When direct sale is not feasible, several key approaches are used:

Employee equity compensation is classified into ISO and NSO option types and RSU characteristics, including vesting, income recognition, and transfer constraints.

- Staged exercise and sale: Exercise options and sell in increments to manage tax, trading volume, and market impact.

- Completion portfolios: Use proceeds from sales to build a diversified portfolio mimicking a benchmark and to gradually reduce risk.

- Hedging with collars or prepaid variable forwards: In some cases, clients can use derivatives (when permitted) to lock in value, monetize future shares, or protect downside while deferring or smoothing tax consequences.

- Exchange funds (where available): Contribute shares to a pooled investment vehicle with other investors, achieving diversification without triggering an immediate tax event (subject to restrictions and availability).

Key Term: completion portfolio

A portfolio of diversified assets constructed with the goal of reducing tracking error relative to a benchmark when combined with a concentrated position.

Worked Example 1.2

Scenario: A client with vested RSUs is subject to a Rule 144 restriction limiting sale to 1% of shares outstanding per quarter. The client is concerned about market risk during a lock-up.

Answer:

If derivatives or structured solutions are unavailable, the client can implement a "dribble-out" sale strategy matching the allowed volume, using proceeds to build a completion portfolio. Downside risk remains until shares are sold; taxes are due at vesting for RSUs, and at sale for post-vesting appreciation.Exam Warning: Employees often underestimate the combined risk of job loss and equity price decline—"double risk." CFA exam questions may require you to analyze both risks together when assessing client vulnerability.

Tax and Estate Planning Considerations for Employee Shares

Tax rules for ESOs and RSUs can be complex and highly jurisdiction-dependent. Some general considerations include:

- Exercising ISOs and holding shares may result in favorable capital gains tax rates if holding periods are met, but may also generate alternative minimum tax (AMT) liability.

- Exercising NSOs typically triggers ordinary income tax, with further capital gain or loss on subsequent sale.

- RSUs are taxed as ordinary income at vesting, based on the market value, with future appreciation taxed as capital gains.

Employees must also consider estate planning: unexercised or unvested awards may expire or be forfeited on death, and beneficiary rights depend on plan terms.

Revision Tip: Prepare concise tables comparing tax treatment and constraints of ESOs and RSUs to aid memory for exam questions requiring direct comparison.

Summary

Employee stock options and restricted stock units introduce significant concentration, company-specific, and liquidity risks to a client’s wealth. Planning must account for employment and equity risk overlap (double risk), limited liquidity windows, and tax triggers. Effective management may require staged diversification, hedging (when permitted), and careful attention to plan, tax, and legal constraints. CFA candidates should be ready to analyze these features and recommend strategies tailored to client circumstances for the Level 3 exam.

Key Point Checklist

This article has covered the following key knowledge points:

- Understand risk characteristics of ESOs and RSUs, including double risk and lack of diversification

- Compare tax and regulatory constraints of ESOs vs. RSUs

- Identify core strategies for diversifying or hedging concentrated positions when outright sale is restricted

- Evaluate suitability and process of staged exercise, completion portfolios, derivatives, and exchange funds

- Recognize key client-specific, tax, and estate planning issues for ESOs and RSUs

Key Terms and Concepts

- concentrated position

- employee stock option (ESO)

- restricted stock unit (RSU)

- vesting

- blackout period

- incentive stock option (ISO)

- non-qualified stock option (NSO)

- double risk

- completion portfolio