Learning Outcomes

This article explains risk-adjusted performance measurement for the CFA Level 3 exam, including:

- how the Sharpe, Treynor, and information ratios are defined in terms of excess return and the specific risk measure in the denominator;

- step‑by‑step calculation of each ratio from portfolio, benchmark, and risk-free returns, with attention to correct inputs and units;

- interpretation of ratio magnitudes when comparing portfolios, managers, and investment strategies, including what constitutes superior or inferior risk-adjusted performance;

- selection of the appropriate measure under different portfolio contexts—stand‑alone portfolios, well‑diversified equity mandates, and benchmark‑relative active strategies;

- comparison of the three ratios in terms of the type of risk captured (total, systematic, and active), their assumptions, and their practical strengths and weaknesses;

- typical CFA exam traps and misconceptions, such as confusing active risk with total risk, misreading the sign of excess returns, or comparing ratios across incompatible benchmarks;

- application of these measures to worked numerical examples and vignette-style questions to support accurate, time-efficient solutions under exam conditions.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand and compare key risk-adjusted measures of performance, with a focus on the following syllabus points:

- Understanding and calculating the Sharpe ratio, Treynor ratio, and information ratio

- Interpreting risk-adjusted performance relative to benchmarks

- Evaluating strengths and limitations of each measure for portfolio and manager assessment

- Applying these metrics to real-world CFA-style problems and identifying correct use cases

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which risk–adjusted return measure is most appropriate when comparing active funds to their respective passive benchmark?

- If Portfolio X has a Sharpe ratio of 0.8 and Portfolio Y has a Sharpe ratio of 0.5, which portfolio offered better risk-adjusted returns? Why?

- True or false? The information ratio penalizes a manager for taking on market (systematic) risk in excess of the benchmark.

- What is the Treynor ratio’s denominator, and why is it relevant?

Introduction

Investment performance measurement requires more than simply noting total returns. To assess manager skill and portfolio effectiveness, it is critical to evaluate return relative to risk. Risk-adjusted performance measures such as the Sharpe ratio, Treynor ratio, and information ratio are industry standards for evaluating the risk/return profile of portfolios and managers. This article will outline these measures, their calculation, interpretation, and applications, all with direct relevance to CFA Level 3 exam questions.

Key Term: risk-adjusted return

The return on an investment portfolio adjusted for the risk taken to achieve that return, enabling fairer comparison between portfolios with different risk profiles.Test Tip: When revising Risk-adjusted measures sharpe treynor and information ratio, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Risk-Adjusted Performance Measures Overview

Risk-adjusted measures standardize performance evaluation by relating excess return to risk exposures. The three principal measures on the CFA Level 3 syllabus for this purpose are Sharpe ratio, Treynor ratio, and information ratio.

Key Term: Sharpe ratio

A metric that quantifies excess return per unit of total risk, where total risk is measured as portfolio standard deviation. Key Term: Treynor ratio

A metric that expresses excess return per unit of systematic risk (portfolio beta), isolating returns attributable to market risk exposures. Key Term: information ratio

A measure that expresses average active return over a benchmark per unit of active risk (tracking error), isolating returns due to manager skill regardless of market direction.

The Sharpe Ratio

The Sharpe ratio evaluates returns relative to the total volatility (standard deviation) a portfolio experiences:

Where:

- = portfolio return

- = risk-free rate

- = standard deviation of portfolio return

The Sharpe ratio allows performance comparison between portfolios or funds, regardless of differences in asset allocation or risk exposures. It is most useful when evaluating the manager's skill in diversifying and managing total risk, particularly in multi-asset or unconstrained mandates.

Key Term: standard deviation

The statistical measure of the dispersion of returns around their mean, used to quantify total risk in portfolio return.

Worked Example 1.1

Portfolio A earns 8% with a standard deviation of 12%. The risk-free rate is 2%. What is Portfolio A’s Sharpe ratio?

Answer:

Portfolio A delivered 0.50 units of excess return per unit of total risk.

The Treynor Ratio

The Treynor ratio indicates the risk premium per unit of market risk (beta), useful for portfolios that are well-diversified and where unsystematic risk is negligible:

Where:

- = portfolio beta relative to the market

The Treynor ratio is best deployed when portfolios are part of a broader portfolio and only systematic risk is relevant (diversification assumed).

Key Term: beta

A measure of sensitivity to systematic (market) risk. Beta indicates the degree to which a portfolio’s returns move with those of the market.

Worked Example 1.2

Portfolio B has a return of 9%, a beta of 0.9, and the risk-free rate is 2%. What is its Treynor ratio?

Answer:

Portfolio B produced a risk premium of 7.8% per unit of systematic risk.

The Information Ratio

The information ratio expresses the manager’s proficiency at outperforming a benchmark, factoring in the volatility of their excess returns (tracking error):

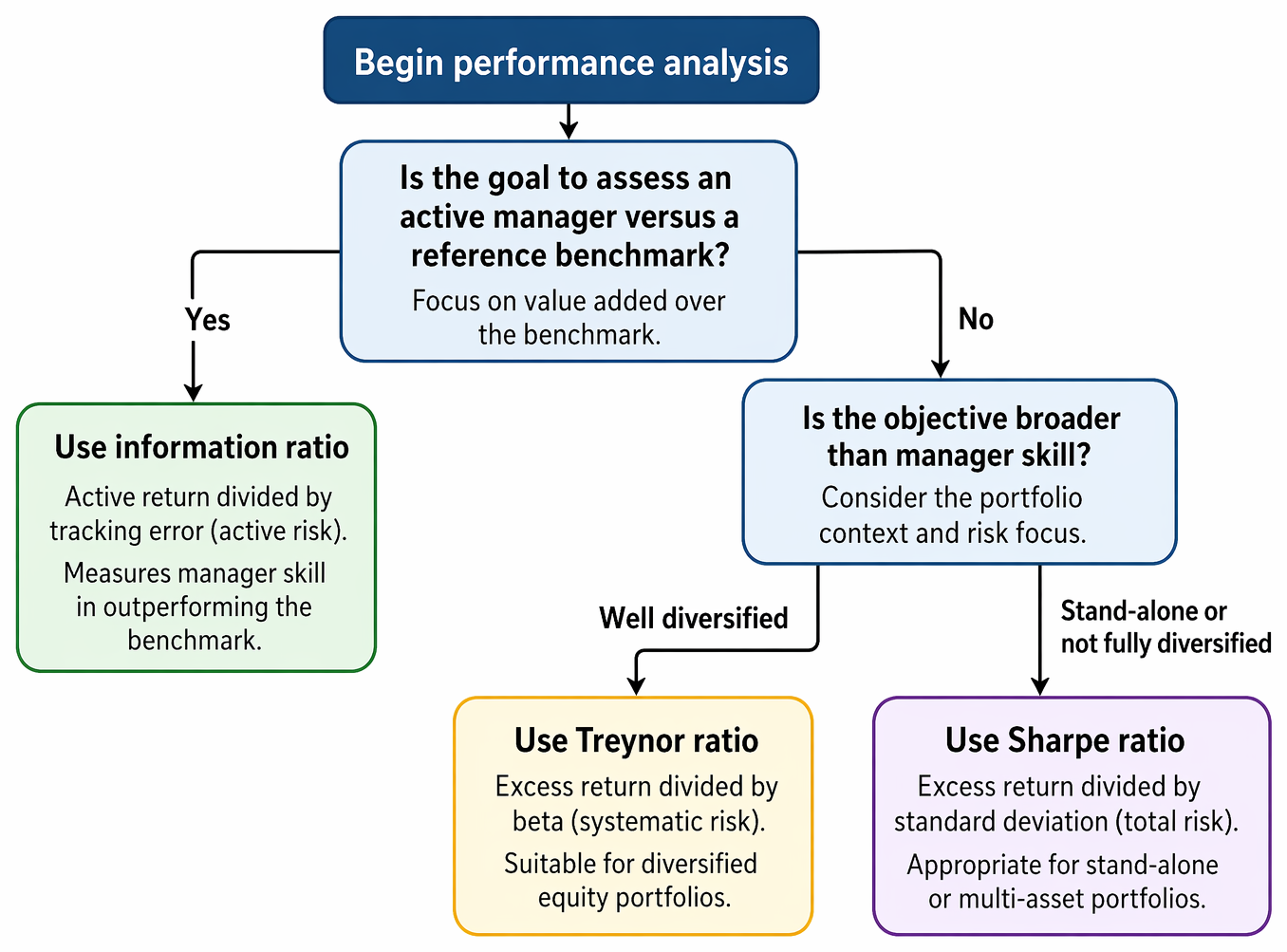

Performance evaluation decision rules assign the information ratio to active benchmark comparison, Treynor to diversified portfolios, and Sharpe to stand-alone portfolios.

Where:

- = benchmark return

- = tracking error (standard deviation of excess return over the benchmark)

The information ratio focuses on active return per unit of active risk. It is most relevant for evaluating the value added by active management, and for comparing managers whose portfolios are similar in overall risk to a benchmark.

Key Term: tracking error

The standard deviation of the difference between a portfolio’s returns and its benchmark’s returns, representing the level of active risk taken by a manager.

Worked Example 1.3

A manager’s portfolio returned 11%. The benchmark returned 8%. The tracking error is 4%. What is the information ratio?

Answer:

The manager achieved 0.75 units of active return for each unit of tracking error.

Comparing the Measures

- The Sharpe ratio assesses total risk; use it for stand-alone or unconstrained portfolios.

- The Treynor ratio assesses systematic risk; use it when portfolios are fully diversified.

- The information ratio assesses active risk; use it for comparing active managers with similar constraints and mandates.

Exam Warning: The Sharpe and information ratios are not directly comparable if portfolios have different benchmarks or risk profiles. For the CFA exam, ensure you match each measure to the right context. Do not use the Sharpe ratio as the primary tool for judging a closet index manager when tracking error (active risk) is very low; use the information ratio instead.

Limitations of Risk-Adjusted Measures

- Standard deviation (Sharpe) is meaningful only if returns are approximately normally distributed and risk isn’t concentrated.

- Beta (Treynor) assumes portfolios are well diversified and that the market index is an appropriate benchmark.

- The information ratio penalizes both upside and downside active risk, and may hide periods of poor absolute performance if the benchmark is also weak.

- None of these ratios provide judgment as to statistical significance or persistence of skill.

Summary

Risk-adjusted measures—the Sharpe ratio, Treynor ratio, and information ratio—allow a direct comparison of return with risk. Use the Sharpe ratio for total risk assessment, the Treynor for systematic risk among diversified portfolios, and the information ratio for evaluating active manager skill relative to tracking error. Correct interpretation and context are essential for effective performance evaluation.

Key Point Checklist

This article has covered the following key knowledge points:

- Sharpe ratio: excess return per unit of total risk (standard deviation)

- Treynor ratio: excess return per unit of systematic risk (beta)

- Information ratio: active return per unit of tracking error (active risk)

- When and how to apply each ratio in CFA exam scenarios

- Limitations and correct interpretation of the three measures

Key Terms and Concepts

- risk-adjusted return

- Sharpe ratio

- Treynor ratio

- information ratio

- standard deviation

- beta

- tracking error