Learning Outcomes

This article explains performance measurement for CFA Level 3 candidates, including:

- how to define and interpret active return, value-added alpha, and related terminology in an exam context;

- how to decompose active return into systematic factor contributions and residual alpha using multi-factor models;

- how to distinguish rewarded risk-factor exposures from genuine manager skill when assessing portfolio performance;

- how to interpret regression outputs, factor sensitivities (betas), and attribution results to identify the true sources of value-add;

- how to use information ratio, active risk, and tracking error to evaluate the efficiency and consistency of alpha generation;

- how to evaluate performance claims that rely on inappropriate benchmarks, incomplete factor models, or unstable alpha estimates;

- how to recognize and avoid common exam traps, such as over-attributing outperformance to skill, mislabeling factor bets as alpha, or ignoring benchmark specification;

- how to structure concise written responses that link numerical decompositions to clear conclusions about manager value-add and investment suitability.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand advanced principles of portfolio performance evaluation and, in particular, the attribution and decomposition of active return and value-added alpha, with a focus on the following syllabus points:

- Defining and interpreting value-added alpha in portfolio management.

- Breaking active return into systematic (factor) and idiosyncratic (alpha) sources.

- Comparing manager returns to appropriate benchmarks/factors to identify genuine skill.

- Recognizing practical challenges and common pitfalls in real-world and exam scenarios.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the key distinction between value-added alpha and exposures to rewarded risk factors?

- Given a portfolio with high active return but large factor tilts, how would you determine if the manager added true alpha?

- Briefly describe how active return can be decomposed.

- True or false? The sum of factor exposures always equals the portfolio’s total value-add.

Introduction

Performance measurement at Level 3 goes well beyond calculating returns. For top marks, you must show you can distinguish between value added by manager skill (alpha) and returns that simply result from systematic risk exposures (beta/factors). Decomposing active return into these components is essential for benchmarks, manager selection, and optimizing future strategies. This article covers the core methodology and key definitions tested in the CFA exam for this subtopic.

Key Term: active return

The difference between a portfolio's return and its benchmark return over a specified period. Key Term: alpha (value-added alpha)

The portion of active return attributed to manager skill after accounting for all systematic (factor) exposures. Key Term: factor exposures (beta)

Systematic return sources linked to broad market indices or risk premia (e.g., market, size, value, momentum factors). Key Term: active risk (tracking error)

The standard deviation of active returns; measures total variability of returns versus the benchmark.

Active Return and Value Added

Active return is the basis for performance analysis:

However, not all active return reflects manager skill. Most portfolios deviate from benchmarks in ways that systematically increase exposure to known risk premia (market, value, size, etc.). Only the residual—after accounting for these factors—can be attributed to true value added.

Key Term: active return decomposition

The process of separating total active return into factor (systematic) and alpha (skill-based) components.

Active Return Decomposition

Active return can be mathematically expressed as:

Performance measurement sequence derives active return, separates factor contributions from alpha, then assesses tracking error, information ratio, and manager suitability.

where:

- , = portfolio and benchmark exposure to factor

- = the realised return of systematic factor

- = manager skill (value-added alpha), the portion not explained by factor exposures

This approach separates systematic (factor) return—earned by assuming risk exposure—from idiosyncratic or value-added (“alpha”) return that indicates manager skill.

Key Term: value-added (true alpha)

The component of active return remaining after systematic (factor) returns are stripped out; reflects manager skill.

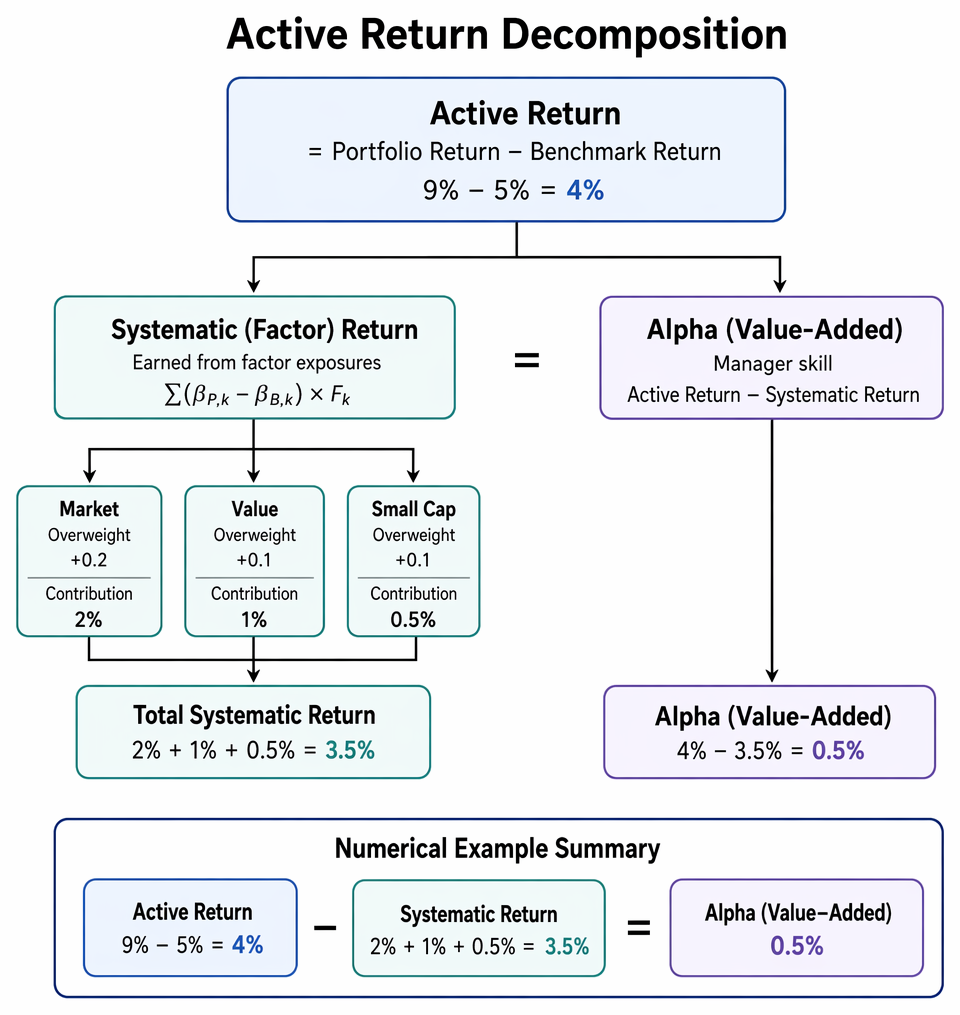

Worked Example 1.1

Question: A portfolio earns a return of 9% against its index benchmark return of 5%. Regression analysis shows overweight exposure to the market (beta +0.2), value (+0.1), and small cap (+0.1), with these factors contributing 2%, 1%, and 0.5%, respectively. What is the manager’s alpha?

Answer:

Calculate systematic (factor) return:

The manager’s value-added skill is 0.5%, with the remainder due to rewarded factor exposure.

Interpreting Value Added and Active Risk

Active risk (tracking error) captures the volatility of active returns. The information ratio (IR) assesses manager skill per unit of active risk:

A high IR signals effective alpha generation, after controlling for systematic risk.

Key Term: information ratio (IR)

Alpha divided by active risk; measures manager skill per unit of benchmark-relative volatility.

Factor Model Application and Pitfalls

It is essential to interpret “alpha” using a rigorous factor model:

- Use a comprehensive set of relevant factors.

- Ensure benchmarks are appropriate (style, region, size, risk exposures).

- Mis-specified or incomplete factor models may overstate or understate genuine alpha.

- Alpha is often small—most portfolios’ excess return is due to systematic exposures, not unique skill.

Worked Example 1.2

Question: A manager runs a US equity portfolio with persistent overweight to technology, achieving returns well above the S&P 500. When decomposed versus a style (sector-neutral) benchmark, the outperformance disappears. What does this indicate about their “alpha”?

Answer:

The outperformance was due to a persistent sector tilt (technology beta). When using a sector-neutral benchmark, the alpha vanishes, indicating no manager skill. Value added was due entirely to systematic sector exposure, not skillful stock selection.Exam Warning: The exam may present a portfolio with a high active return and ask whether the manager should be rewarded. If most active return comes from systematic exposures (factor bets), not alpha, do NOT describe this as skill-based value add. Use factor-based attribution as your evidence.

Real-World Challenges

- Many managers design portfolios intentionally tilted to rewarded factors, then claim outperformance as alpha.

- Only that part of the return unexplained by known factor exposures is genuine value added.

- Proper selection of factor models and benchmarks is essential for accurate measurement.

Worked Example 1.3

Question: A long-only portfolio posts 8% outperformance versus its benchmark and has an annual tracking error of 6%. Regression analysis using a four-factor model yields an alpha of 0.3% with a t-statistic of 0.7. What should you conclude about the manager’s value-add?

Answer:

The t-statistic for alpha is statistically insignificant. The manager’s outperformance comes almost entirely from factor tilts (market, size, value, momentum), not from skill-based security selection.Revision Tip: When evaluating manager value-add, cite factor attribution and residual alpha. Explain if outperformance is from factor exposures (beta) or genuine manager skill (alpha).

Summary

Distinguishing between value-added alpha and systematic factor return is fundamental to CFA Level 3 performance measurement. Decompose active return into (1) factor exposures reflecting systematic risks and (2) residual alpha reflecting skill. Recognize that most “outperformance” is due to broad risk factor bets, not unique skill.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and interpret value-added alpha and its role in performance measurement.

- Decompose active return into systematic (factor) exposures and alpha (skill).

- Apply multi-factor models to distinguish skill from rewarded risk taking.

- Recognize limitations of factor attribution and practical measurement pitfalls.

- Avoid common errors in interpreting manager outperformance on the exam.

Key Terms and Concepts

- active return

- alpha (value-added alpha)

- factor exposures (beta)

- active risk (tracking error)

- active return decomposition

- value-added (true alpha)

- information ratio (IR)