Learning Outcomes

This article explains how to select and evaluate investment benchmarks and design portfolio constraints for CFA Level 3–style portfolio management questions, including:

- Identifying the characteristics of a valid benchmark, assessing investability and appropriateness, and judging whether a proposed index or custom reference portfolio meets exam-standard criteria.

- Comparing alternative benchmark types—broad market, style, peer-group, and custom—and determining which is most suitable for a given mandate, risk profile, and investment style.

- Explaining how benchmark choice influences active risk, performance attribution, manager evaluation, and the interpretation of tracking error in both qualitative discussions and numerical exam problems.

- Classifying key constraint types—legal, regulatory, liquidity, asset allocation, concentration, risk, and ESG—and articulating their purpose and implications for feasible portfolios and trading flexibility.

- Evaluating whether a set of constraints is too tight or too permissive, and predicting its likely impact on diversification, active opportunity, and potential exam-case underperformance.

- Diagnosing misalignment between benchmarks and constraints in case vignettes, and formulating clear, exam-appropriate recommendations to correct policy weaknesses and improve performance measurement.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the role and selection of benchmarks and the effective implementation of constraints in portfolio construction, including how benchmarks set the standard for evaluating performance and how constraints determine the feasible set of portfolios, with a focus on the following syllabus points:

- The definition and characteristics of appropriate benchmarks for portfolios

- Steps and criteria for selecting and evaluating portfolio benchmarks

- The types and purposes of portfolio constraints (legal, regulatory, risk, liquidity, asset class, and others)

- How benchmark selection and constraints shape the investment policy statement and asset allocation decision

- The effects of constraints on portfolio risk, return, and active management

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the key properties that define an effective investment benchmark?

- Why is it important to align portfolio constraints with regulatory, legal, and client-specific requirements?

- Give two examples of how a poorly chosen benchmark can distort performance assessment.

- What potential risks arise if constraints are too restrictive or too loose for a portfolio manager?

Introduction

Constructing a suitable portfolio requires setting clear performance standards and boundaries for action. Benchmarks serve as performance comparators and risk anchors, while constraints define the operating limits for managing investments. For CFA Level 3, a practitioner must be able to recommend, justify, and evaluate benchmark selection and constraints in a portfolio management context. A well-chosen benchmark provides a meaningful reference for risk-adjusted performance, guides active management decisions, and supports accountability. Constraints, which flow from the investment policy statement, ensure investment activity matches client requirements, regulation, and prudent risk-taking.

Key Term: benchmark

A standard, such as an index or custom reference portfolio, against which the performance and risk of a portfolio are measured. A benchmark should reflect the portfolio’s investment universe and policy; it must be unambiguous, measurable, investable, reflective of current opinions, specified in advance, and appropriate. Key Term: constraint

A rule or limit set within the investment policy statement to restrict portfolio composition, risk, or manager activity—arising from client goals, regulation, or risk management needs.Test Tip: When revising Benchmark selection and constraints, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Benchmark Selection in Portfolio Construction

An effective benchmark is the basis of sound portfolio management and evaluation. The benchmark must match the portfolio’s investment objectives, strategy, and permissible universe.

Investment benchmark categories are matched to diversified passive, stable-style, hard-to-index, and liability-specific mandates.

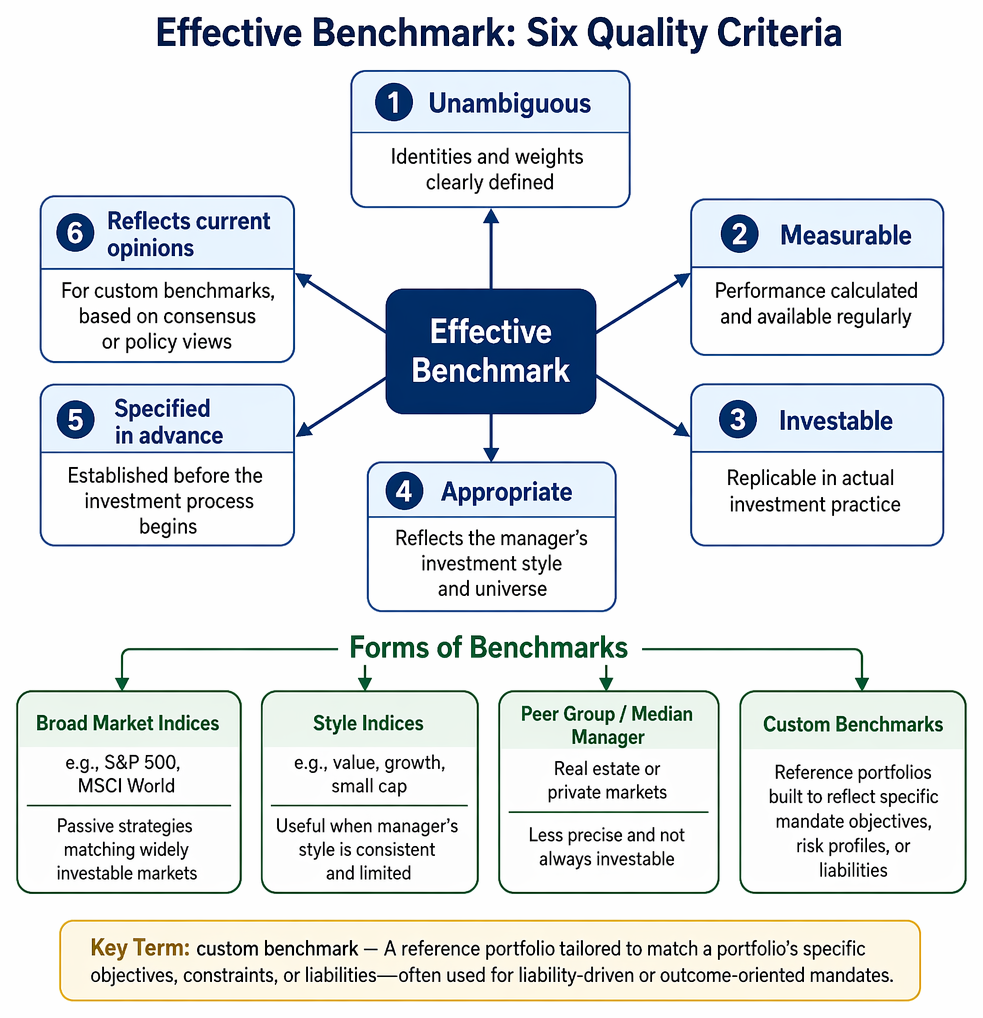

Benchmark Quality Criteria

A suitable benchmark must demonstrate six essential properties:

- Unambiguous: The identities and weights of benchmark components must be clearly defined.

- Measurable: The benchmark’s performance must be calculated and available regularly.

- Investable: It must be possible to replicate the benchmark in actual investment practice.

- Appropriate: The benchmark reflects the manager’s investment style and universe.

- Specified in advance: The benchmark is established before the investment process begins.

- Reflects current opinions: For custom benchmarks, should be based on consensus or policy views.

Benchmarks can take various forms:

- Broad market indices (e.g., S&P 500, MSCI World): Suitable for passive strategies matching widely investable markets.

- Style indices (e.g., value, growth, small cap): Useful when a manager’s style is consistent and limited.

- Peer group/median manager: Common in real estate or private markets, but less precise and not always investable.

- Custom benchmarks: Reference portfolios built to reflect specific mandate objectives, risk profiles, or liabilities.

Key Term: custom benchmark

A reference portfolio tailored to match a portfolio’s specific objectives, constraints, or liabilities—often used for liability-driven or outcome-oriented mandates.

Worked Example 1.1

Selecting a Benchmark for a Global Equity Fund

A fund manager runs an active global equity strategy. The portfolio invests in developed and emerging markets, and the client wants to evaluate performance without home bias. Which benchmark would be most appropriate?

Answer:

The MSCI All Country World Index (ACWI) is suitable, since it includes both developed and emerging markets, is investable, widely published, and not biased toward any single country—reflecting the fund’s investment universe.

Portfolio Constraints: Definition, Types, and Impact

Constraints limit the investment universe, portfolio composition, or behaviour. They are essential for controlling unintended risks and ensuring adherence to client goals, legal, or regulatory demands.

Key Types of Constraints

- Legal/regulatory: Minimum/maximum exposures (e.g., UCITS rules, ERISA prudence, insurance company restrictions)

- Liquidity: Mandated minimum cash balances; maximum allocation to illiquid assets

- Asset class and concentration: Limits on weights for sectors, geographies, or individual holdings; e.g., “no more than 5% per security”

- Risk limits: Tracking error, maximum volatility, VaR, sector or factor limits

- Ethical/ESG: Sector and company exclusions based on client’s ethical guidelines

Constraints must be well aligned with the investment mandate. Overly restrictive constraints may reduce return opportunity or add unintended risks (e.g., forced concentration or under-diversification); overly loose constraints can introduce unacceptable risk or non-compliance.

Worked Example 1.2

Impact of Constraints on a Portfolio Manager

A pension fund IPS specifies no more than 10% in illiquid private equity, no shorting, and maximum tracking error of 4% against the policy benchmark. How does this affect the manager’s choices?

Answer:

The manager will have to construct a portfolio using assets with high market liquidity, must avoid borrowing and derivatives that could create short exposure, and must carefully balance active bets so that tracking error remains at or below the 4% limit. The constraints ensure risk level is controlled and the portfolio stays compliant with investment policy and liquidity needs.

The Link Between Benchmark and Constraints

The benchmark provides the performance yardstick; constraints ensure the portfolio is managed within agreed parameters relevant to the reference point. For example, a portfolio benchmarked to a high-yield index but with investment-grade restrictions is mismatched—constraints must always be consistent with benchmark selection and stated objectives.

Exam Warning: Using a benchmark that cannot be fully replicated or is misaligned with constraints will invalidate performance comparisons and can mislead stakeholders about skill or risk exposures.

Benchmark Selection Pitfalls and Effective Monitoring

- Chosen benchmark must not be subject to frequent, arbitrary changes (avoid “retroactive” performance measurement).

- Investor and manager must agree ex-ante on the standards for success and accept how constraints affect performance versus the benchmark.

- Constraints may need to be reviewed and updated periodically as regulation or investment environments shift.

Worked Example 1.3

Evaluating Benchmark Appropriateness

A core bond portfolio is benchmarked to a government bond index but allows up to 25% in high-yield corporates. Is this an appropriate benchmark for performance assessment?

Answer:

No—the performance, risk, and trading characteristics of high-yield bonds differ significantly from government securities. The benchmark understates risk and return opportunity versus the mandate, distorting manager evaluation.

Summary

Selecting the right benchmark and applying coherent, relevant constraints is essential for setting clear, fair expectations for a portfolio. Benchmarks should be investable, measurable, appropriate for the mandate, and specified up front. Constraints must match risk controls, client objectives, and all regulatory requirements. Both work together to frame active management, manage stakeholder expectations, and ensure meaningful performance evaluation.

Key Point Checklist

This article has covered the following key knowledge points:

- The essential properties that define an effective portfolio benchmark

- The importance of alignment between the benchmark, constraints, and portfolio mandate

- Types of constraints: regulatory, liquidity, asset, risk, and ethical

- Benchmark and constraint roles in setting performance evaluation standards

- Impacts of misaligned benchmarks or constraints on risk, returns, and compliance

Key Terms and Concepts

- benchmark

- constraint

- custom benchmark