Learning Outcomes

This article explains how portfolio managers apply risk models in constructing and monitoring portfolios, highlighting differences between factor models, covariance-based models, and risk-budgeting frameworks. It explains how these models support strategic and tactical asset allocation, position sizing, and risk-control for institutional and individual portfolios. The article also explains how portfolio turnover is defined, decomposed into different sources (rebalancing, alpha-driven trades, and client-driven flows), and linked to trading costs, implementation shortfall, realized risk, and tax consequences. It examines how excessively high or excessively low turnover can distort style integrity, generate unintended tracking error, and erode expected alpha. In addition, the article analyzes portfolio capacity as a constraint on scaling active strategies, emphasizing the interaction between asset liquidity, market impact, and strategy characteristics such as turnover and crowding. It explains methods for assessing a strategy’s practical and theoretical capacity limits and for adjusting expected returns at larger asset sizes. Finally, the article discusses how risk models, turnover management, and capacity analysis must be integrated into an ongoing portfolio management process to maintain alignment with client objectives and mandate restrictions.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the implications of risk models, turnover, and capacity in portfolio management, with a focus on the following syllabus points:

- Evaluate and implement portfolio construction using risk models (including factor models and risk budgeting)

- Analyze how portfolio turnover affects trading costs, performance, and risk

- Assess how portfolio capacity constrains investment strategies and drives implementation challenges

- Apply these concepts for both institutional and individual investor portfolios

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the main differences between risk models used in portfolio construction and those used for risk reporting?

- How does high portfolio turnover impact strategy performance and risk control?

- Explain the relationship between portfolio capacity, asset liquidity, and the scalability of an investment strategy.

- What approaches might a portfolio manager use to manage the impact of turnover and capacity constraints?

Introduction

Effective portfolio management requires not only the selection of the right assets based on risk and return expectations, but also the careful construction and monitoring of the portfolio using risk models, controls on turnover, and an understanding of capacity limits. These factors are central to maintaining a portfolio’s intended risk profile, meeting investment objectives, and implementing strategies at scale with minimal performance drag.

Key Term: risk model

A quantitative framework (e.g., factor or risk budgeting model) used to estimate the sensitivity of portfolio returns to specific risk factors and to measure and allocate portfolio risks relative to desired levels. Key Term: turnover

The rate at which portfolio positions are bought and sold, often measured as the lesser of total purchases or sales divided by average portfolio value over a period. Key Term: capacity

The maximum level of assets a strategy can effectively manage before performance deteriorates, typically due to increased trading costs, lower liquidity, and reduced opportunity to place new trades.

THE ROLE OF RISK MODELS IN PORTFOLIO CONSTRUCTION

Risk models are essential tools for understanding, managing, and allocating portfolio risk. They provide structure for risk budgeting and inform asset allocation decisions, constrain position sizing, and help managers forecast the potential impact of market factors on the portfolio.

Risk-model governance allocates risk budgets, tests actual exposures against limits, and rebalances or adds positions to maintain portfolio constraints.

Types of Risk Models

Portfolio managers use several types of risk models:

- Factor models: Estimate exposures to systematic risk factors (market, size, value, sector, etc.).

- Covariance matrix models: Use historical asset-return relationships to model portfolio risk.

- Risk budgeting frameworks: Allocate total portfolio risk to subcomponents (asset classes, strategies, risk factors).

The risk model chosen should reflect the nature of the assets, portfolio objectives, and practical constraints.

Key Term: risk budgeting

The process of allocating the permitted total risk of a portfolio across asset classes, strategies, or individual positions with the objective of maximizing expected return for a given level of risk.

Practical Uses in Portfolio Management

Risk models are used to:

- Set bounds on total portfolio and per-asset risk

- Inform rebalancing and tactical asset allocation decisions

- Identify unintended concentrations of risk

- Support regulatory or client-level reporting

Risk models also provide critical feedback to ensure the portfolio remains consistent with client objectives and strategic asset allocation guidelines.

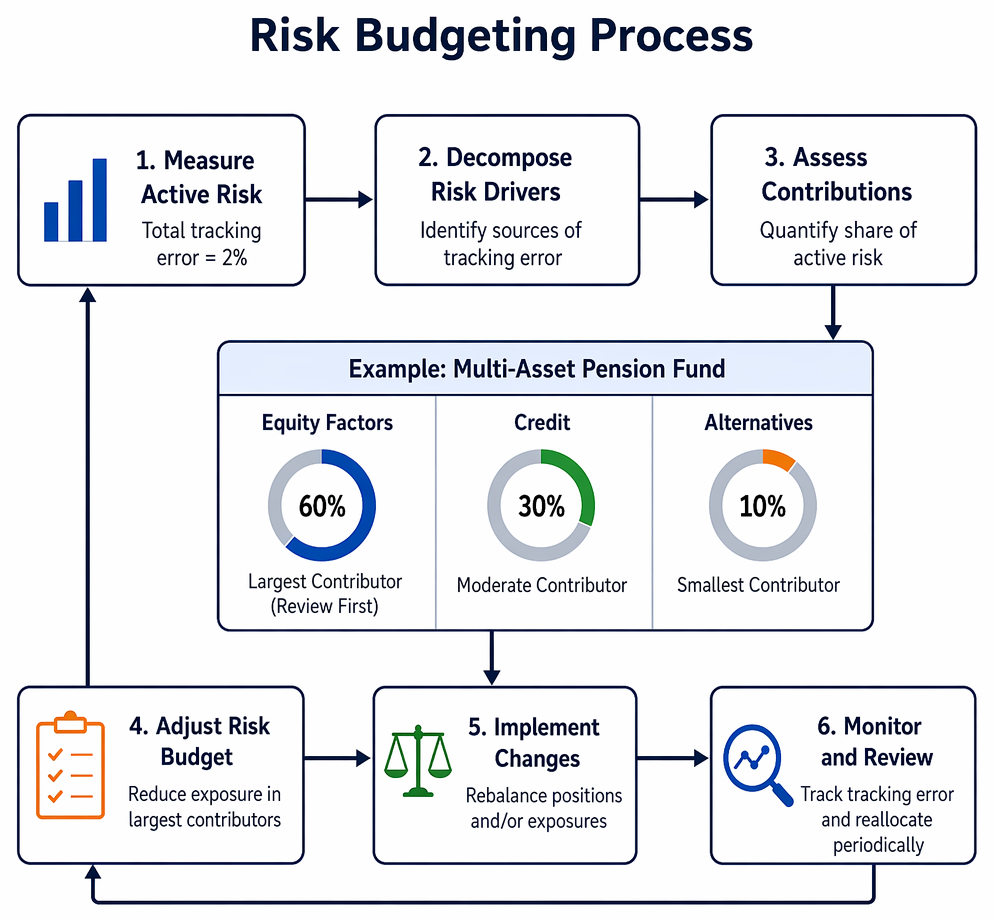

Worked Example 1.1

Question: A multi-asset pension fund restricts its active risk (tracking error) to 2%. Its risk model identifies 60% of tracking error from equity factors, 30% from credit, and 10% from alternatives. How should its risk budgeting process react?

Answer:

The risk budget should be reviewed to reduce active risk in the largest contributors. For example, the fund may lower equity factor exposure (e.g., reduce overweight to equities or diversify equity style tilts) to avoid exceeding the 2% tracking error limit. Monitoring and periodic reallocation are recommended to remain within the permitted risk.

PORTFOLIO TURNOVER: IMPACTS AND CONTROLS

Portfolio turnover is a critical implementation metric. Turnover can arise from rebalancing, changes in expected return, investment strategy adjustments, or client cash flows. High turnover generally increases trading costs, realized capital gains, and tracking error. Conversely, very low turnover may lead to portfolio drift and misalignment with intended risk exposures.

Turnover implications:

- High turnover increases explicit trading costs, potential tax drag for taxable accounts, and potential slippage from market impact.

- High turnover may imply style inconsistency, excessive responsiveness to short-term noise, and greater performance dispersion.

- Some strategies (e.g., arbitrage, momentum, or quantitative models) may require higher turnover to be effective, but must account for implementation costs in expected returns.

Low turnover does not automatically indicate higher efficiency. If turnover is too low, risk exposures may diverge from targets, or the portfolio may accumulate positions outside mandate limits.

Key Term: implementation shortfall

The performance loss arising from the difference between theoretical trade prices and actual execution, typically increased by excessive turnover or poor execution.

Worked Example 1.2

An equity portfolio has 100% turnover per year. If trading costs are estimated at 0.40% per turnover, and the expected gross alpha of the strategy is 1% per year, estimate the expected net alpha.

Answer:

Net expected alpha = 1.0% (gross) – 0.4% (trading costs) = 0.6%. The benefit of further turnover should be carefully weighed against cost.Exam Warning: High turnover in a strategy with thin alpha margins may offset expected value-added and increase tracking error. Always adjust gross expected return for all-in trading expense and tax drag for relevant accounts.

PORTFOLIO CAPACITY: DEFINING AND LIMITING SCALE

Capacity ultimately dictates the maximum asset size at which a strategy can be run efficiently without diluting its expected return. As asset size increases, trading becomes more difficult and costly, because large trades move the market and may not be absorbed at acceptable prices. Portfolio managers must consider both the theoretical and practical limits of strategy scale.

Factors affecting capacity: -Liquidity of the constituent assets: More liquid markets (e.g., US large-cap equities, government bonds) can absorb larger trades than less liquid assets (e.g., small caps, alternatives). -Style and turnover of the strategy: High-turnover, market-impact-sensitive strategies generally have lower capacity. Low-turnover strategies are less constrained. -Crowding and competition: If many managers use similar trades, the execution price and opportunity set for all can deteriorate sharply at scale.

Key Term: market impact

The adverse price movement caused by executing large trades in a security, a primary component of realized transaction cost as portfolio size grows. Key Term: liquidity

The ability to buy or sell an asset with minimal price change and low transaction costs, critical for sustaining high-capacity portfolio strategies.

Worked Example 1.3

Question: A global equity manager’s backtested high-turnover momentum strategy shows a strong excess return on $10 million AUM. If applied at $5 billion AUM, what considerations limit the validity of historical backtest results and the realized excess return?

Answer:

At $5 billion AUM, the strategy likely exceeds its natural capacity. Sourcing sufficient trade liquidity without significant market impact becomes difficult, and crowding may lead to eroded alpha and increased slippage. Managers should scale expected return downward for higher trading cost and implementation loss.

TURNOVER, RISK AND CAPACITY IN PRACTICE

Managers must monitor turnover and capacity in conjunction with the risk model and implementation data. This involves:

- Ongoing assessment of trade size relative to market volume and daily liquidity

- Careful attribution of performance slippage to capacity effects versus model drift

- Forecasting and stress-testing capacity under scenarios of increased AUM or reduced opportunity set

- Coordination with compliance and operational teams to ensure exposures do not breach client or regulatory limits under scaling

Revision Tip: When considering new strategies or increases in AUM, always analyze historical returns net of realistic trading cost and market impact at prospective scale. Question the persistence of alpha at larger capacity.

Summary

Risk models, turnover and capacity are key operational components of successful portfolio management. Portfolio managers use quantitative risk models to allocate risk, guide investment decisions, and control exposures within mandate limits. Turnover affects costs, risk, and style consistency, and must be optimized for both return and implementation constraints. Portfolio capacity imposes natural and practical limits on the scalability of active strategies. All three factors interact to shape investment performance, efficiency, and risk control.

Key Point Checklist

This article has covered the following key knowledge points:

- Understand the function and construction of portfolio risk models in asset allocation and monitoring

- Realize the implications of turnover for trading costs, implementation shortfall, and investment style

- Recognize the practical limitations imposed by portfolio capacity and market liquidity when scaling strategies

- Manage risk, turnover, and capacity together for effective portfolio construction and ongoing monitoring in institutional and private wealth portfolios

Key Terms and Concepts

- risk model

- turnover

- capacity

- risk budgeting

- implementation shortfall

- market impact

- liquidity