Learning Outcomes

This article explains how to analyze and model private equity and venture capital cash flows for CFA Level 3 exam-style questions. It develops your ability to construct time‑series cash flow schedules from commitments, capital calls, and distributions; compute internal rates of return (IRR) using calculator or spreadsheet functions; and interpret IRR in terms of annualized performance on committed and invested capital. It distinguishes IRR from money‑multiple and wealth‑creation measures, emphasizing why IRR alone can mislead when comparing funds with different cash flow patterns, reinvestment assumptions, or fund lives. The article also explains the logic, calculation, and interpretation of public market equivalent (PME) measures, including how to map each cash flow into a public index and derive a PME ratio. You practice interpreting PME values above and below 1.0, commenting on relative outperformance versus a stated benchmark. Finally, the article highlights key limitations, data requirements, and sensitivity issues for both IRR and PME, guiding you to articulate benchmark choice and modeling assumptions clearly in constructed‑response answers.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the principles of private equity and venture capital fund performance measurement, with a focus on the following syllabus points:

- Modeling the cash flows of private equity and venture capital investments.

- Calculating and interpreting the internal rate of return (IRR) for fund and investment performance.

- Explaining the mechanics, uses, and interpretation of the public market equivalent (PME) method.

- Evaluating the benefits and limitations of IRR and PME in benchmarking private equity returns to public markets.

- Recognizing the practical implications of timing, cash flow irregularity, and benchmark selection.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What does internal rate of return (IRR) measure in the context of private equity cash flows?

- How does the public market equivalent (PME) approach address shortcomings of IRR?

- Why are cash flow timing and benchmark selection critical when using PME?

- True or false? PME values above 1.0 imply that the private equity investment has outperformed the public benchmark, after adjusting for timing.

Introduction

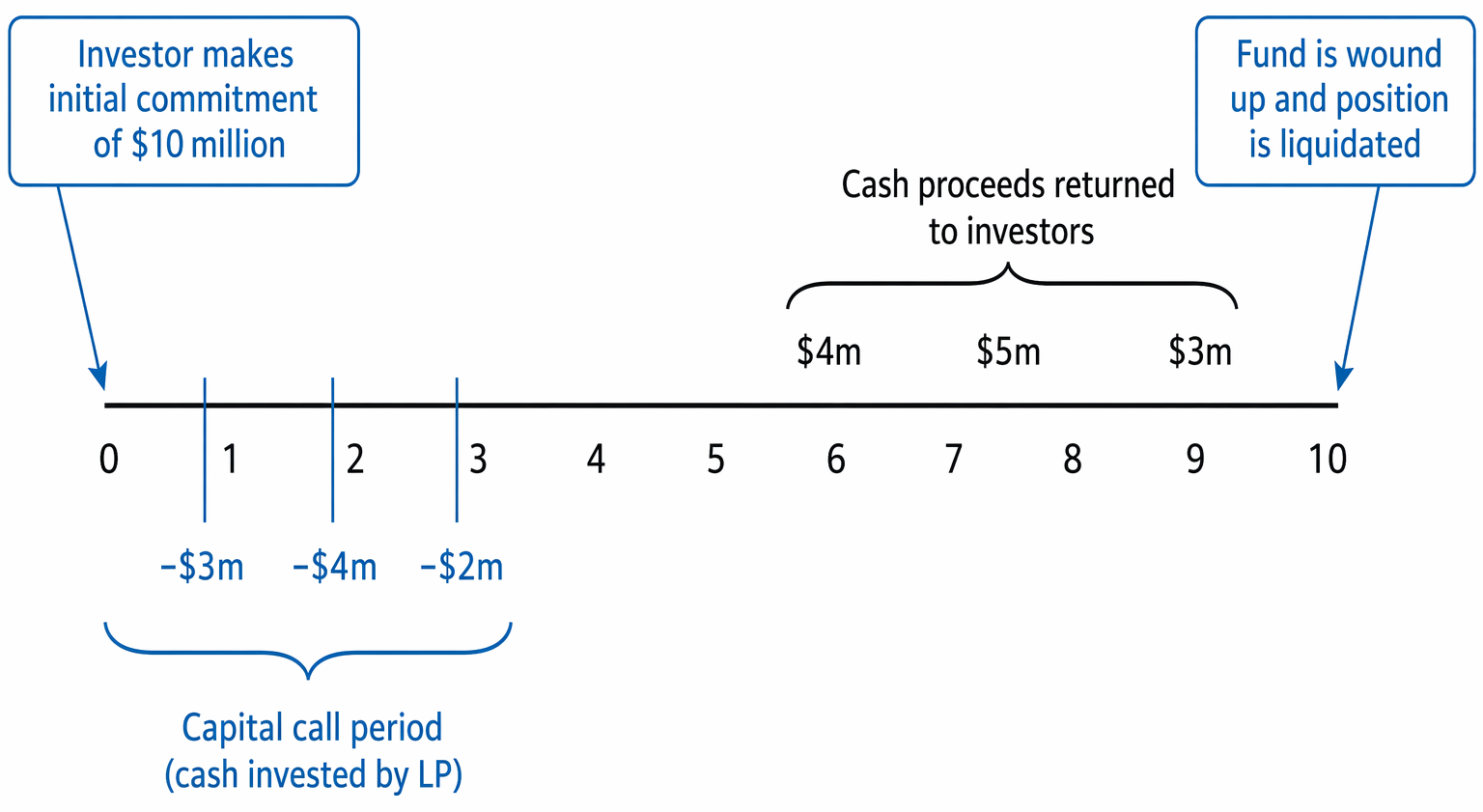

Private equity and venture capital funds differ fundamentally from traditional liquid investments. Their cash flow patterns are irregular, involving an initial outflow (called capital commitment) followed by unpredictable drawdowns, further capital calls, distributions, and a final liquidation payment. For CFA exam purposes, accurately modeling these cash flows is essential to assess returns and benchmark performance against public markets.

Private fund performance measurement maps irregular contributions and distributions into annualized IRR and PME relative to a public market benchmark.

Key Term: cash flow modeling

The process of structuring all expected outflows (capital invested) and inflows (distributions, liquidation) along a time series for an investment or fund. Used to facilitate fair measurement of returns.

Measuring Private Equity Performance: The Role of IRR

Modeling the performance of private equity or venture capital funds begins with constructing the exact dates and amounts of all cash flows in and out of the fund or investment. Unlike traditional assets, these cash flows occur sporadically, complicating standard return calculations.

Key Term: internal rate of return (IRR)

The discount rate that sets the net present value of all cash flows (inflows and outflows) of an investment to zero. Widely used to report private equity or venture capital performance.

The IRR of a private equity fund communicates the annualized return on committed capital, adjusting for the size and the specific timing of each capital call and distribution.

Mathematically, IRR is the rate, r, that satisfies:

Where CFₜ are net cash flows (negative for commitments/calls, positive for distributions/returns).

Worked Example 1.1

A fund requires an initial capital call of $1,000,000 at time 0. Three years later, it distributes $450,000 (year 3), $400,000 (year 4), and at year 7 returns $800,000. What is the IRR?

Answer:

The IRR is the discount rate r such that:

Solving (via spreadsheet or calculator), IRR ≈ 10.9%.

Limitations of IRR in Private Equity

Despite its widespread use, IRR has several known drawbacks when applied to private equity or venture funds:

- IRR is highly sensitive to the timing of cash flows. Early distributions disproportionately inflate IRR.

- It cannot be meaningfully compared across different funds or asset classes unless the pattern and timing of cash flows are similar.

- It does not provide a clear indication of absolute wealth creation or value added beyond the alternative options available to the investor.

Exam Warning: On the CFA exam, do not assume that a higher IRR always means better investment performance. Timing of cash flows and reinvestment rates can distort IRR. It is essential to benchmark IRR appropriately before interpreting results.

Public Market Equivalent (PME): Benchmarking Relative Performance

To address the shortcomings of IRR, the public market equivalent (PME) method compares the performance of a private investment directly to a public market index over the same period, aligning the timing of cash flows precisely. PME is particularly useful to assess whether a private equity or venture capital strategy has yielded returns above or below what could have been achieved by investing in a public market benchmark.

Key Term: public market equivalent (PME)

A performance measure that compares the value created by a private equity or venture investment to the simulated value if identical cash flows had been invested in a chosen public benchmark over the same time periods.

The logic is as follows:

- Each capital call and distribution is treated as if invested or withdrawn from a public index (e.g., an equity ETF or total return index) on the same actual day.

- For each cash flow, calculate how its value would have grown, or shrunk, had it experienced the market return over the holding period.

- The PME ratio is calculated as: PME = Σ[actual distributions' future values at exit] / Σ[capital calls' future values at exit]

Interpretation:

- PME > 1.0: The private investment outperformed the benchmark.

- PME < 1.0: The private investment underperformed the benchmark.

Worked Example 1.2

A VC fund calls $2.5 million on 1 Jan 2015, $1.5 million on 1 Jun 2015. It returns $1 million on 1 Jul 2017 and $4 million on 1 Dec 2019. Assume the benchmark is an equity index ETF starting at 100 and ending at 165.

Answer:

Step 1: For each cash flow, grow the called amount by the index's total return to exit date.

- $2.5m × (165/100) = $4.125m

- $1.5m × (approximate growth, say 120 to 165) = $1.5m × (165/120) ≈ $2.06m

Step 2: For each distribution, also bring its present value forward to exit.

- $1m × (165/140) ≈ $1.18m

- $4m × (165/165) = $4.0m

Step 3: PME = sum of distributions brought to exit / capital calls brought to exit = ($1.18m + $4.0m) / ($4.125m + $2.06m) ≈ $5.18m / $6.19m ≈ 0.84 PME < 1.0: The VC investment did not outperform the public market over this period.

Interpreting PME and Important Benchmarks

PME's power is in adjusting for the actual timing of invested capital—a major limitation of IRR. However, PME is only as useful as the choice of benchmark index and the accuracy of index data for all relevant dates. Benchmark selection should match the risk and liquidity profile of the private fund.

Key Term: performance benchmarking

The act of comparing investment returns, such as IRR, to an appropriately selected public market index or alternative performance metric to contextualize and interpret results.

Worked Example 1.3

An institutional investor receives PME = 1.15 using a broad equity index as a benchmark for a buyout fund. What does this indicate?

Answer:

The buyout fund generated 15% more value than would have been created by investing the same cash flows into the public index at the same times.

Sensitivities and Limitations of Cash Flow Modeling

- Both IRR and PME are affected by the accuracy and granularity of the cash flow records.

- PME requires high-frequency (typically monthly or daily) benchmark price data for interpolation.

- For venture and late-stage private equity funds, lumpy distributions and capital calls make performance volatile and may not capture risk differences.

- Benchmark indices may not be investable or may not reflect fund-specific risks (e.g., size, liquidity, sector, or geography).

Revision Tip: For CFA exam scenarios, explicitly state your benchmark, the timing of all cash flows, and your PME calculation method. If asked to assess performance, mention sensitivity to benchmark choice and cash flow modeling precision.

Summary

Effective modeling of private equity and venture capital cash flows is essential for proper performance evaluation. Both IRR and PME are standard metrics, but only PME adjusts cleanly for invested capital timing and provides a relative benchmark. Always scrutinize your benchmark selection and recognize IRR/PME sensitivities for CFA exam questions.

Key Point Checklist

This article has covered the following key knowledge points:

- Modeling irregular private equity and venture cash flows for performance analysis

- Calculating IRR and recognizing its timing and reinvestment assumptions

- Using PME to benchmark private investment returns against public markets considering exact timing

- Interpreting PME values for over/underperformance

- Critically assessing the limitations and sensitivities of IRR and PME measures in the context of fund performance

Key Terms and Concepts

- cash flow modeling

- internal rate of return (IRR)

- public market equivalent (PME)

- performance benchmarking