Learning Outcomes

This article explains private equity (PE) and venture capital (VC) deal structures, fee arrangements, and governance features that are commonly tested at CFA Level 3. It focuses on the legal and economic structure of limited partnership funds, the mechanics of capital commitments, drawdowns, and distribution waterfalls, and the distinction between European and American carry structures. It explains management fees, carried interest, hurdle rates, catch-up and clawback provisions, and how these affect GP incentives and LP returns. The article also examines key governance mechanisms, including GP commitments, key person provisions, advisory committees, no-fault divorce clauses, and reporting requirements used to manage agency risk. Throughout, it emphasizes how to interpret fund term sheets, identify alignment tools and potential conflicts, and analyze whether PE/VC terms are investor-friendly or GP-friendly. This exam-focused coverage equips you to calculate and interpret fee amounts and profit splits, evaluate the quality of PE/VC governance frameworks, and compare alternative fund structures in item set and constructed-response questions.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the mechanics of private equity and venture capital investments, with a focus on the following syllabus points:

- Describing the common structures of PE and VC deals, including limited partnership agreements and co-investment arrangements

- Explaining management and incentive fee arrangements in PE/VC, including hurdles, catch-ups, and clawbacks

- Assessing the governance mechanisms, controls, and alignment of interests between fund managers (GPs) and investors (LPs)

- Evaluating fund term sheets and recognizing standard and non-standard terms in PE/VC fund documents

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the most common economic structures and legal forms for private equity and venture capital funds?

- Describe how management fees and carried interest are typically structured in private equity funds.

- Explain what alignment mechanisms are used to control agency risk in PE/VC fund governance.

- What is the purpose of a "hurdle rate" and a "clawback" clause in a PE/VC fund agreement?

Introduction

Private equity (PE) and venture capital (VC) investments rely on specialized legal structures, bespoke contracts, and fees designed to align incentives and manage agency risks. Understanding the key features of deal structure, fee formulas, and governance is critical for comparing funds, analyzing risks, and ensuring that investor interests are protected.

Key Term: Limited partnership (LP)

A common legal structure for private equity and venture capital funds, consisting of a general partner (GP) who manages the fund and limited partners (LPs) who contribute capital but have limited liability. Key Term: General partner (GP)

The entity (often a management firm) responsible for managing the private equity fund, making investment decisions, and representing the fund to outside parties.

Deal Structures in PE and VC

Private equity and venture capital funds are nearly always structured as limited partnerships. The typical participants are the limited partners (LPs) (usually institutional investors, pensions, or wealthy individuals) and the general partner (GP), who is responsible for the overall management and investment decisions.

The limited partnership agreement (LPA) forms the backbone of the deal and defines key terms including capital commitment, drawdowns, fund term, fees, investment limits, and distributions.

Key Term: Limited partnership agreement (LPA)

The legal contract governing the operation of a private equity or venture capital fund, detailing rights, obligations, limitations, and procedures for LPs and GPs. Key Term: Capital call (drawdown)

A request by the GP for LPs to provide capital as investment opportunities arise, usually subject to agreed timelines and notice terms in the LPA.

Most funds operate using a "commitment and drawdown" model. LPs make an overall commitment, which the GP draws down in tranches as deals are sourced. The investment period is typically 3–5 years, after which new investments may be restricted.

The fund will usually have a lifespan of 10–12 years. During the first half, capital is invested; during the second, assets are managed and eventually sold.

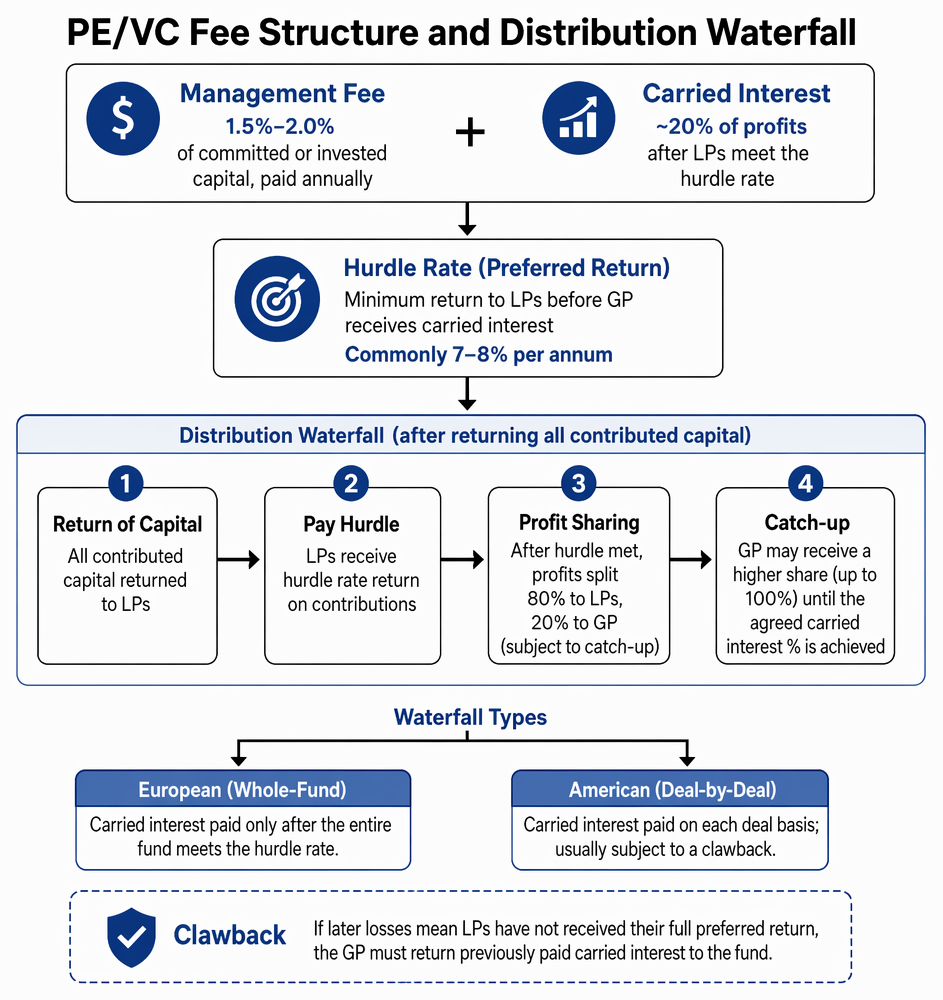

Fee Structures in PE and VC

The classic PE/VC fee model is a combination of a fixed management fee and a variable performance fee, incentivizing the GP to maximize realized returns for the LPs.

Private equity and venture capital compensation terms include management fees and GP carried interest after limited partners satisfy the hurdle return.

Management Fees

Gleaned as an annual percentage (commonly 1.5%–2.0%) of committed or invested capital, management fees are designed to cover the GP’s operating costs and are payable regardless of fund performance. As the commitment is drawn down and assets sold, the base upon which the fee is charged may shift from committed to invested capital or net asset value.

Key Term: Management fee

An ongoing fee, usually a percentage of committed or invested capital, paid by LPs to the GP for managing the fund, generally charged annually.

Carried Interest (Performance Fees)

The carried interest is the GP's share (often 20%) of fund profits, paid only after the LPs achieve a threshold return, commonly called the hurdle rate.

Key Term: Carried interest

The share of investment profits (usually 20%) retained by the GP as a performance incentive, paid after achieving minimum return targets for LPs. Key Term: Hurdle rate

The minimum return that must be delivered to LPs before the GP is entitled to carried interest, often set at 7–8% per annum.

Carried interest is typically subject to a "European" or "American" (deal-by-deal) distribution waterfall.

- European-style waterfall: Carried interest is paid only after all contributed capital and the hurdle rate have been returned for the entire fund.

- American-style waterfall: Carried interest is paid on a deal-by-deal basis, potentially allowing earlier GP payments but usually subject to a fund-level "clawback" to prevent overpayment.

Key Term: Clawback

A contractual provision requiring GPs to return previously paid carried interest to the fund if subsequent losses mean LPs have not ultimately received their full agreed preferred return. Key Term: Catch-up

A mechanism in PE/VC profit-sharing where, after the hurdle is met, the GP receives a higher split of profits (sometimes all profits) until the agreed carried interest % is achieved, then subsequent distributions revert to the standard share. Key Term: Preferred return

Another term for the hurdle rate: the minimum rate of return promised to LPs before GPs share in profits.

Worked Example 1.1

A VC fund charges a 2% management fee on committed capital and a 20% carried interest with an 8% hurdle. An LP commits $10 million. What is the maximum management fee in year one, and how is carried interest calculated if, after 7 years, the fund generates gross profits of $6 million (after returning all $10 million to LPs)?

Answer:

- Management fee: $10 million × 2% = $200,000 (year one).

- First, LPs must be paid back their $10 million plus 8% annual compound return before any carried interest accrues to the GP. Any profits remaining after the hurdle is met are split 80% to LPs, 20% to GP (subject to catch-up).

- If the fund returns enough such that, after paying the $10 million and the hurdle, $1 million remains, the GP receives 20% × $1 million = $200,000 in carried interest.

Exam Warning: In the CFA exam, be careful to check whether carried interest is paid on a deal-by-deal (American) or whole fund (European) basis, and whether a clawback applies. Failing to identify the waterfall type may lead to an incorrect answer about GP incentives and agency risks.

Governance and Alignment Mechanisms

Deal structure and fees alone are insufficient to protect LP interests. Strong governance arrangements balance the power between GPs (who control information and tactics) and LPs (who provide the capital but are exposed to agency risk).

Alignment Tools

- GP commitment: GPs usually invest their own capital—usually 1–5% of the fund—to demonstrate alignment.

- Key person provisions: If critical individuals leave the GP, new investments may be paused.

- Investment restrictions: The LPA often specifies sector, geography, borrowing limits, and diversification rules.

- Advisory committees: LP representatives may sit on advisory boards that review and approve conflicts, valuations, fund extensions, and other major decisions.

- No-fault divorce: LPs can remove the GP by vote if performance or conduct is unsatisfactory.

- Transparency: Fund reporting, including audited financial statements and regular portfolio updates, is typically contractually required.

Key Term: Key person provision

A clause in the LPA requiring suspension of investment activity if designated GP team members depart, protecting LPs' interests. Key Term: Advisory committee

A group of LP representatives that monitors major activities, approves conflicts, and reviews key decisions to improve fund governance. Key Term: No-fault divorce

A provision allowing LPs, by supermajority vote, to remove the GP and/or dissolve the fund without cause. Key Term: GP commitment

The amount of a fund's capital contributed by the GP, used to align incentives and demonstrate risk sharing with LPs.

Worked Example 1.2

A PE fund LPA has a key person provision triggered if the lead GP departs. What happens if she resigns three years into the investment period?

Answer:

Fund commitments may be suspended, with no new deals until either a replacement is approved by the LP advisory committee or the original key person returns. This provision prevents GPs from raising capital based on key individuals and then changing the team.Revision Tip: Review the detailed terms of a typical limited partnership agreement (LPA), focusing closely on fee waterfall examples, clawback provisions, and advisory committee powers. Understanding how these function to align incentives can quickly earn marks on application questions.

Summary

Efficient private equity and venture capital deals are based on clear legal structures, transparent fee arrangements, and strong governance. Key alignment tools include hurdle rates, clawbacks, catch-ups, key person provisions, and advisory committees; these mechanisms address principal–agent problems common in these funds. A high-quality LPA and robust governance reduce agency risk, increase expected returns for LPs, and are heavily tested on the CFA exam.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the legal and economic structure of private equity and venture capital funds, focusing on the limited partnership model

- Calculate and interpret management fees, carried interest, hurdle rates, catch-up, and clawback provisions

- Distinguish between European (fund-as-a-whole) and American (deal-by-deal) waterfalls and their agency implications

- Appraise the primary governance and alignment mechanisms in LPA documents, including the role of advisory committees and key person clauses

- Evaluate how fund terms protect LP interests and minimize agency risk

Key Terms and Concepts

- Limited partnership (LP)

- General partner (GP)

- Limited partnership agreement (LPA)

- Capital call (drawdown)

- Management fee

- Carried interest

- Hurdle rate

- Clawback

- Catch-up

- Preferred return

- Key person provision

- Advisory committee

- No-fault divorce

- GP commitment