Learning Outcomes

This article explains the role of private equity and venture capital in diversified portfolios, including:

- understanding how PE/VC allocations can increase expected returns, provide exposure to unique value-creation opportunities, and alter the overall risk profile of multi‑asset portfolios;

- distinguishing the main drivers of PE/VC performance—operational value creation, financial leverage, entry and exit valuations, and the illiquidity premium—and relating these to portfolio-level risk and return;

- identifying key risk factors such as illiquidity, capital call and commitment risk, J‑curve effects, manager dispersion, and vintage‑year cyclicality, and assessing how these interact with investor objectives and constraints;

- evaluating the diversification benefits and limitations of PE/VC relative to public equities, with particular emphasis on correlations in normal markets versus stress periods;

- analyzing practical allocation issues, including appropriate sizing of PE/VC commitments, liquidity planning, pacing across vintage years, and the consequences of concentrated sector or geographic exposure;

- comparing private and public equity on dimensions of transparency, governance, costs, performance measurement, and implementation complexity within the CFA Level 3 exam framework;

- integrating PE/VC within strategic asset allocation, factor-based allocation, and goals-based or liability-relative frameworks, and evaluating their impact on long‑term spending and funding objectives.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand how private equity and venture capital function within a portfolio and wealth management context, with a focus on the following syllabus points:

- The strategic and tactical roles private equity and venture capital can play in institutional and individual portfolios

- Core drivers of return and risk for PE/VC and how they differ from public markets

- The impact of illiquidity, investment horizon, and selection/diversification challenges

- Diversification, correlation, and incorporation of PE/VC into multi-asset allocation frameworks, including factor-based approaches

- Key risk considerations such as manager dispersion, capital calls, vintage year effects, performance persistence, and the J‑curve

- Practical implementation issues: sizing commitments, pacing across vintages, liquidity stress testing, and governance/monitoring requirements

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

For a long-horizon defined benefit plan seeking to improve its return relative to liabilities, what is the most defensible primary motivation for adding a 15% allocation to private equity buyout funds?

- a) To reduce portfolio volatility through stable reported quarterly valuations

- b) To lock in a guaranteed illiquidity premium above public equity returns

- c) To access manager-driven value creation and an illiquidity premium in exchange for bearing additional risk

- d) To perfectly hedge the plan’s interest rate and inflation sensitivity

-

Which combination best represents risks that are distinctively important for PE/VC compared with listed equities?

- a) Duration risk and reinvestment risk

- b) Capital call risk and commitment risk

- c) Currency risk and counterparty risk

- d) Basis risk and inflation risk

-

How does vintage year most directly influence a private equity portfolio’s realized performance?

- a) It determines the legal structure and fee terms of the fund

- b) It fixes the minimum IRR that the general partner must achieve

- c) It determines the macro environment and pricing level at which capital is invested and exited

- d) It indicates the number of portfolio companies in each fund

-

Why can illiquidity in PE/VC be both a risk and a potential source of return at the total-portfolio level?

- a) Illiquidity reduces volatility and therefore eliminates risk, increasing returns

- b) Illiquidity forces investors to hold cash, which earns the risk-free rate

- c) Illiquidity creates valuation opacity, which mechanically boosts reported IRRs

- d) Illiquidity restricts trading flexibility and raises liquidity risk, but can justify a higher required return (illiquidity premium) for investors who can bear it

Introduction

Private equity (PE) and venture capital (VC) represent alternative asset classes where investors provide capital to private companies, ranging from established mid-sized businesses (PE) to early-stage, high-growth startups (VC). These investments are typically executed through closed-end fund structures with lengthy holding periods, capital calls, and limited liquidity. In multi-asset portfolios, PE/VC allocations are designed to increase expected return, diversify public equity risk, and access unique value-creation opportunities unavailable in traditional markets.

Most Level 3 questions involving PE/VC are not about memorizing structures but about judging whether a specific allocation, commitment plan, or manager selection decision is suitable given an investor’s objectives, constraints, and the broader economic environment.

Key Term: private equity (PE)

Investments made directly in non-public companies, typically through buyouts or growth capital, seeking value creation via operational or financial restructuring. Key Term: venture capital (VC)

Equity capital provided to startups or early-stage companies with high growth potential, usually in exchange for a minority stake. Key Term: illiquidity premium

Additional expected return demanded by investors for holding assets that cannot be easily traded or converted to cash without substantial loss in value.

PE buyout funds often target established, cash-generative companies where value can be created through improving operations, changing capital structure, or repositioning strategy. VC funds focus on innovation and disruptive technologies, accepting higher failure rates at the company level in exchange for a small number of very large winners.

Because PE/VC investing is inherently long term, business cycle conditions at the time of investment (and exit) matter. Funds starting near the peak of a credit-fueled boom often face high entry valuations and tighter financing later, while vintages raised in or after recessions may benefit from lower entry prices and less competition for deals. These macro effects are central to understanding vintage-year cyclicality, one of the major risk drivers discussed below.

The Role of Private Equity and Venture Capital in Portfolios

Private equity and venture capital are included in diversified portfolios to improve long-term returns, tap into specialized sources of value creation, and diversify exposures away from public equities. These asset classes have historically delivered higher average annual returns than public stocks, though with greater return dispersion, higher volatility (on an economic basis), and significant liquidity constraints.

Strategic Roles

- Return enhancement: The illiquidity premium and the active involvement of managers in value creation (for example, operational improvements, strategic repositioning, or market expansion) can produce superior realized returns over long horizons. In addition, private equity returns can be decomposed into:

- fundamental revenue growth and margin improvement;

- the effect of leverage on equity returns; and

- changes in valuation multiples between entry and exit.

Key Term: multiple expansion

Increase in the valuation multiple (such as EV/EBITDA or P/E) applied to a company’s earnings or cash flows between entry and exit, contributing to private equity returns beyond fundamental business growth.

Skilled managers exploit all three channels. At the portfolio level, this means PE/VC allocations can shift the efficient frontier outward—higher expected return for a similar level of long-run total risk—provided the investor can bear illiquidity and manager-selection risk.

-

Diversification: PE/VC returns are only moderately correlated with public equity—providing diversification, especially when specific strategies or sectors differ from listed markets. However, correlations tend to rise in deep downturns, because fundamental business values and default risk move with the same economic drivers. Also, reported correlations can look artificially low because PE/VC valuations are updated infrequently and based on appraisals rather than market prices, which smooths short-term volatility.

-

Access to unique opportunities: VC provides access to disruptive innovation and early-stage growth that may never be fully captured in public markets. PE buyout funds open doors to operational restructurings, control transactions, and niche sectors otherwise unavailable through public markets, such as family-owned businesses or carve-outs from large corporates.

-

Potential inflation protection: Many private companies have pricing power or real‑asset backing (for example, infrastructure or asset-heavy businesses). PE/VC can therefore provide some sensitivity to growth and inflation, complementing listed equities and real assets.

Strategic versus Tactical Uses

Strategically, institutional investors set a long-run target allocation to PE/VC within the overall policy portfolio. This target is based on risk tolerance, liquidity needs, and beliefs about active manager skill and illiquidity premia.

Tactically, investors may adjust commitment pacing by vintage year—raising commitments when expected opportunities are strong (for example, post-recession, with lower entry valuations) and scaling back when competition and pricing appear excessive. However, large tactical swings are difficult: capital is drawn over several years, exits are uncertain, and timing the private markets “cycle” is much harder than timing listed markets.

Typical Allocations

Institutional portfolios, such as those of endowments and pension funds, may allocate 5–20% to PE/VC, depending on investment horizon, risk tolerance, and liquidity needs. Some large endowments and sovereign wealth funds with very long horizons and stable inflows allocate even more across the broader “private markets” bucket (including private credit and real assets).

Importantly, target allocations are usually expressed as a percentage of portfolio net asset value (NAV), whereas commitments must be higher to allow for uncalled capital and the gradual drawdown of funds. A 10% target NAV allocation to PE might require, for example, 15–20% of capital commitments once the program is fully built out.

Private clients with long-term horizons and adequate risk capacity may target lower allocations—often in the 5–10% range—reflecting smaller portfolios, less diversification across managers, and more binding liquidity constraints.

Key Considerations in Allocation

When deciding whether and how much to allocate to PE/VC, portfolio managers should consider:

-

Investment horizon: PE/VC funds typically have legal lives of 10–12 years, with the main investment period in the first 3–5 years and realizations later. Investors should have an economic horizon long enough to tolerate delayed liquidity and the J‑curve.

-

Illiquidity and lock-up periods: Interests in PE/VC funds cannot usually be redeemed on demand. Secondary markets for fund interests exist but can involve meaningful discounts, especially during downturns when liquidity is scarce.

-

Capital commitment and call profile: Investors commit capital upfront, but the general partner (GP) calls capital as deals are found. Managing this schedule is a major treasury task: too little committed capital leads to under-allocation; too much creates the risk of liquidity shortfalls when multiple funds call capital simultaneously.

Key Term: commitment risk

The risk that an investor’s aggregate commitments to PE/VC funds are mis-calibrated, leading either to underinvestment (unused commitments and lower exposure than intended) or overcommitment (liquidity stress when many funds call capital at once).

- Capital call mechanics and funding sources: Capital calls often occur when markets are stressed or when opportunities are attractive (for example, during recessions). Investors must plan funding sources—cash, bond holdings, or lines of credit—and monitor the interaction with other liquidity needs.

Key Term: capital call risk

The risk that PE/VC funds call committed capital at a time when the investor’s liquid asset values are depressed or constrained, potentially forcing asset sales at unfavorable prices.

-

Manager selection and governance capacity: Performance dispersion is large, and due diligence is resource-intensive. Investors need sufficient internal or outsourced skill to evaluate GPs, monitor funds, and manage legal and operational risks.

-

Integration with the broader risk budget: PE/VC allocations increase exposure to equity risk, leverage, and illiquidity. They must be considered alongside public equities, credit, real estate, and human or pension capital when assessing total risk and capacity for loss.

From a risk-factor-based asset allocation standpoint, PE largely adds exposure to equity, value, size, and leverage factors plus an illiquidity factor. For example, in the CFA curriculum’s factor optimization illustration, allowing a portfolio to include 15% private equity increases expected return for essentially the same volatility as a portfolio limited to public assets.

Risk Drivers and Key Return Factors

Returns from PE/VC are driven by a combination of business performance (for example, company growth or efficiency gains), financial engineering (use of debt, recapitalizations), and the valuation at which investments are acquired and exited. However, these asset classes also introduce unique sources of risk that portfolio managers must assess and integrate into portfolio-level decisions.

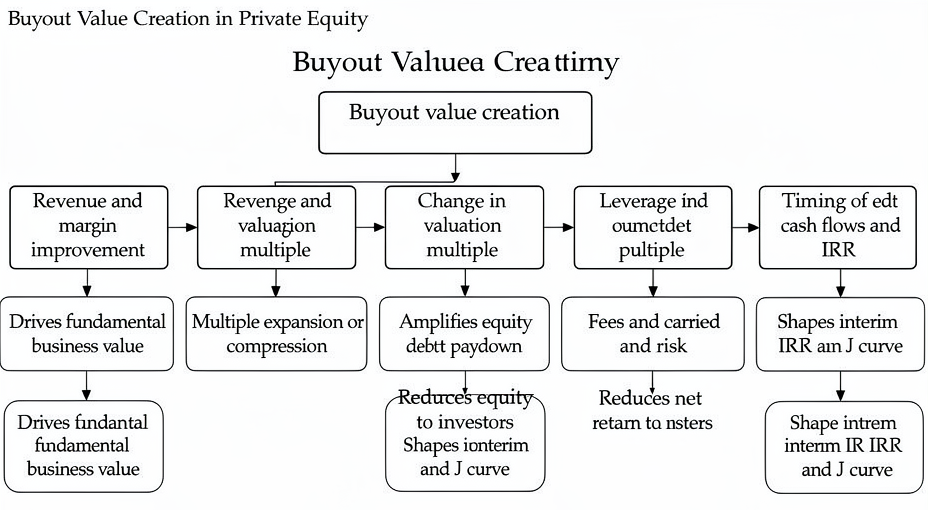

At the fund level, a simplified decomposition of value creation in a buyout might be:

- Revenue growth and margin improvement in the core business

- Change in valuation multiple (multiple expansion or compression)

- Effect of leverage and debt paydown on equity value

- Fees and carried interest paid to the GP

- Timing of cash flows (which affects IRR)

Venture capital returns are more driven by:

- Extreme dispersion between winners and losers

- Access to proprietary deal flow and follow-on capital

- Exit opportunities (IPOs, strategic sales) and market sentiment for growth stocks

Major Risk Drivers

-

Illiquidity risk: PE/VC stakes cannot be traded quickly or at fair value, especially during downturns. Investors must be compensated by an illiquidity premium, but the inability to rebalance can increase downside risk in severe drawdowns or when other parts of the portfolio face stress.

-

Manager selection risk: The spread between top- and bottom-quartile managers is wide; selecting skilled managers is critical. Because the opportunity set and GP skill vary by strategy and geography, relying on median performance is often inappropriate. Manager selection risk is particularly important where performance persistence is moderate and where access to top-tier managers is capacity constrained.

Key Term: manager dispersion

The wide variability in returns between top- and bottom-performing PE/VC managers, typically greater than in public markets.

High dispersion increases the cost of both Type I errors (backing poor managers) and Type II errors (failing to access skilled managers). This is why Level 3 questions often link PE/VC allocation to governance quality and due diligence capability.

-

Capital call/commitment risk: As noted above, investors must fund capital when called, sometimes at times of market or portfolio stress. Overcommitting relative to liquid resources can create forced selling of public assets—the “liquidity gap” risk illustrated in Worked Example 1.2.

-

Diversification risk (concentration): Even diversified funds hold a limited number of deals, and a typical investor may commit to only a handful of funds in each vintage. Concentration by vintage year, sector, or geography can magnify idiosyncratic and macro risk. For example, a portfolio heavily tilted to VC vintages raised in a late-stage tech bubble will be highly sensitive to a subsequent correction.

-

J‑curve risk: Early fund years often show negative returns (as investments are made and fees paid) before maturing and potentially generating gains alongside successful exits.

Key Term: J-curve

The characteristic pattern of private equity fund performance where net cash flows and reported returns are negative in early years due to capital calls and fees, then turn positive later as investments mature and distributions are made, producing a “J-shaped” cumulative return profile.

From a total-portfolio standpoint, funding the negative part of the J‑curve requires careful liquidity planning and realistic expectations about early underperformance.

-

Valuation and reporting risk: Interim valuations are often based on GP assumptions rather than market prices, resulting in increased uncertainty about real portfolio performance. Appraisal-based valuations smooth short-term volatility and can understate true economic risk. This makes standard risk measures such as volatility, beta, or VaR less informative for PE/VC than for listed assets and complicates style analysis and performance attribution.

-

Leverage and financial risk: Buyout funds use substantial debt at the portfolio-company level. This increases equity return sensitivity to changes in earnings and to credit conditions. In adverse macro environments (for example, recession or tightening credit spreads), highly levered deals can suffer permanent loss of capital.

-

Vintage-year cyclicality: PE/VC returns are cyclical. Vintages investing during periods of high valuations and abundant cheap credit often exhibit weaker subsequent returns; vintages deploying capital after recessions may benefit from lower entry multiples and favorable exit conditions later. Investors should therefore diversify commitments across multiple vintages to reduce macro-timing risk.

Key Term: vintage year

The year a PE/VC fund makes its initial investment, affecting the macro environment, investment opportunity set, and subsequent performance.

- Denominator effect: Because PE/VC valuations lag and adjust slowly, sharp declines in public market valuations can mechanically increase the percentage weight of illiquid holdings in the total portfolio.

Key Term: denominator effect

The mechanical increase in the portfolio weight of illiquid assets such as PE/VC when the market value of liquid assets falls, potentially breaching allocation or regulatory limits and constraining new commitments.

Worked Example 1.1

A global pension fund allocates 10% of its assets to buyout funds. If public equities return 7% per year and the buyout funds deliver a 12% gross IRR (before fees and illiquidity costs), but investments are locked up for 10 years, how could this impact the pension's overall portfolio risk/return?

Answer:

Buyout allocations may increase expected long-run return, since 12% exceeds 7%, but they also increase portfolio risk through higher economic volatility, leverage, and illiquidity. The pension must tolerate:

- inability to rebalance this 10% during crises;

- possible underperformance if the selected managers or vintages are weak; and

- a more pronounced drawdown if capital calls occur when public markets are already falling. From an ALM standpoint, the fund should run scenario analyses (for example, a 2008-type shock) to test whether it can still meet near-term benefit payments and contribution policies while honoring capital calls.

Worked Example 1.2

An endowment committed to a VC fund faces a sharp downturn in listed equities at the same time as a $10 million capital call is issued. The liquid assets have fallen, but the capital call must be met. What risk does this scenario illustrate?

Answer:

This is capital call (or liquidity gap) risk: the need to fund private investment commitments when public markets are stressed. The endowment may be forced to sell public assets at depressed prices or draw on credit lines to meet obligations, magnifying portfolio drawdowns and potentially violating policy limits on leverage or illiquid allocations.

Worked Example 1.3

A buyout fund purchases a company for an enterprise value equal to 8× current EBITDA of $50 million, using 60% debt and 40% equity. Five years later, EBITDA has grown to $70 million. The company is sold at a 9× EBITDA multiple, and all debt has been repaid. Ignoring fees, what are the main components of value creation?

Answer:

Initial equity value is 40% of $400 million (8× $50 million) = $160 million. Exit equity value is $630 million (9× $70 million, assuming no debt). Value creation can be decomposed into:

- Operating growth: If the exit multiple stayed at 8×, equity would be worth $560 million (8× $70 million), up from $160 million due to EBITDA growth and deleveraging.

- Multiple expansion: The move from 8× to 9× applied to $70 million adds $70 million (1× $70 million) of extra value. Both components are magnified by leverage, because equity holders capture all value above debt. In portfolio discussions, candidates should be able to link these components to drivers of excess return and to risks—multiple expansion is far less reliable than operational improvements.

Key Risk and Diversification Considerations

Risk of Illiquidity

PE/VC funds are structured as closed-end, limited partnerships with typical lifespans of 10 years or more. Investors do not control the timing of capital deployment or distributions, and stakes are not freely tradable. The illiquidity premium is essential to justify these constraints.

From a portfolio-construction standpoint:

- Investors with high and stable human capital or defined benefit pension wealth can more easily tolerate illiquidity, whereas retirees relying heavily on liquid financial assets for consumption should generally keep PE/VC allocations modest.

- Illiquidity interacts with other constraints. For example, regulatory rules for insurance companies or banks may cap illiquid holdings; spending rules for endowments create ongoing cash outflows that must be supported by liquid assets.

Liquidity planning should therefore include:

- forward projections of capital calls and distributions across vintage years;

- stress tests combining equity market drawdowns with higher-than-expected capital calls; and

- contingency plans (for example, standing credit facilities or capacity to sell on the secondary market).

Key Term: secondary market (private equity)

Market where existing investors sell interests in PE/VC funds to other investors prior to fund liquidation, often at a discount to reported NAV, especially during stressed periods.

Concentration, Diversification, and Manager Dispersion

-

Vintage year effects: Returns can vary widely depending on the fund's investment period relative to market cycles. An investor committing only to 2006–2007 buyout vintages, for example, would have suffered from high entry prices and the subsequent global financial crisis.

-

High dispersion: The return gap between top and bottom quartile managers is substantial; performance persistence is higher in PE/VC than in public equity. This means:

- broad diversification across many average managers does not guarantee attractive performance; and

- access to top-quartile managers can be more valuable than simply increasing the asset-class allocation.

-

Sector and geographic concentration: Inadequate diversification across deals, industries, or locations can concentrate risk and increase sensitivity to specific shocks (for example, energy prices, regional recessions, or regulatory regimes).

-

Portfolio-level trade-offs: Diversifying across more funds and managers smooths idiosyncratic risk but can dilute access to the very best GPs, increase governance burden, and complicate pacing. A well-designed PE/VC program typically:

- spans multiple vintage years;

- includes a mix of strategies (buyout, growth equity, VC) and geographies; and

- concentrates commitments in carefully selected managers rather than indexing the opportunity set.

J-Curve and Return Realization

Early years typically show negative net returns: fees, initial write-downs, and slow realizations outweigh gains. As maturing investments are exited at a profit, returns improve—often sharply in late stages or after public listings, acquisitions, or recapitalizations.

For portfolio managers, the J‑curve has several implications:

- New programs show initially weak or negative performance metrics (IRR and multiple), even if long-term prospects are good.

- Aggregated, multi-vintage programs partially smooth the J‑curve as older, cash‑flow-positive funds offset younger funds in their investment phase.

- Liquidity planning must account for several years of net cash outflows before distributions become material.

Key Term: dry powder

Committed but uncalled capital that PE/VC funds can deploy in future investments.

Dry powder benefits GPs (flexibility) but represents an additional layer of illiquidity for LPs: the capital is encumbered but not yet earning a PE/VC return.

Comparing Private Equity to Public Equity

PE/VC and public equities both provide equity exposure, but they differ on several important dimensions relevant for Level 3 portfolio management.

Private equity buyout returns are decomposed into operational performance, valuation multiples, capital structure effects, investor fees, and cash-flow timing.

Risk, Return, and Factor Exposures

-

Risk and expected return: PE/VC are less liquid, more opaque, and typically riskier on an economic basis, but they target higher expected returns. From a factor standpoint, much of PE’s risk is equity beta plus leverage, value, and size factors, with an additional illiquidity factor layered on top.

-

Leverage and downside risk: Buyout funds use substantial debt, which increases sensitivity to earnings downturns and credit markets. Public equity portfolios can also use leverage, but it is usually lower and more transparent.

-

Correlation with public equities: Correlation with public equity returns is imperfect: lower in normal markets, higher in crises. Apparent correlations using reported NAVs are biased downward by appraisal smoothing; economic exposures are closer to global equity risk factors than observed correlations suggest.

Transparency, Governance, and Control

-

Transparency and pricing: Public equities offer daily pricing, high transparency, and continuous disclosure. PE/VC fund valuations are quarterly and based on manager judgement, with limited transparency for portfolio holdings.

-

Governance and control: PE buyout investors often have control or strong influence over portfolio companies, enabling aggressive operational and financial restructuring. Public equity investors have less direct control, though they may engage through stewardship and activism.

-

Agency issues: Complex fee structures and information asymmetry increase agency risk in PE/VC. Strong limited partner (LP) governance, alignment of interests, and legal protections are essential.

Key Term: carried interest

The performance-based share of profits (often 20%) allocated to the PE/VC general partner if returns exceed a specified hurdle rate, after returning contributed capital and sometimes a preferred return to limited partners.

Costs and Performance Measurement

-

Fees and costs: PE/VC funds typically charge management fees (for example, 1.5–2% per year on committed or invested capital) plus carried interest. Trading and transaction costs at the deal level further reduce net returns. Public equity funds, particularly passive products, have much lower explicit fee levels.

-

Performance measures: PE/VC performance is often evaluated using internal rate of return (IRR) and multiples of invested capital (for example, total value to paid-in capital, TVPI). These metrics are sensitive to cash-flow timing and can be difficult to compare directly with time-weighted public market returns.

-

Benchmarking: Comparing PE/VC to public markets requires care. Public market equivalent (PME) approaches attempt to adjust for cash-flow timing by comparing actual PE cash flows to hypothetical investments in a public index. For exam purposes, you should understand that naive comparisons of PE IRRs to public equity returns can be misleading.

-

Risk measurement challenges: As highlighted in the curriculum’s discussion of style analysis, illiquid or non-traded securities create stale pricing and understate risk over shorter horizons. Returns-based analysis may misrepresent current exposures, and standard deviation or beta may be unreliable. This is a key reason why liquidity and qualitative risk assessment play a larger role in PE/VC risk management.

Implementation Complexity

-

Operational complexity: PE/VC investing involves legal negotiation of limited partnership agreements, complex cash-flow management, and ongoing monitoring. It requires more internal infrastructure than investing in public equities or mutual funds.

-

Access: Many top managers are closed to new investors or limit allocations, making access itself a key value driver. Smaller investors may lack the scale to diversify adequately or to negotiate favorable terms.

-

Regulatory and fiduciary aspects: For fiduciary investors (pension funds, insurers), PE/VC allocations must comply with regulatory constraints on illiquidity, concentration, and leverage. IPS documents must be explicit about permissible ranges, governance processes, and reporting standards.

Worked Example 1.4

An investment committee is comparing two policy portfolios with similar volatility:

- Portfolio A (public only): 60% global public equities, 30% bonds, 10% liquid alternatives

- Portfolio B (public and private): 45% global public equities, 25% bonds, 15% private equity, 15% real estate and other alternatives

The committee believes its governance and liquidity management are strong. What arguments support choosing Portfolio B?

Answer:

Portfolio B replaces part of the public equity exposure with private equity and real assets. This:

- increases expected return by adding an illiquidity premium and access to GP-driven value creation;

- provides additional diversification across economic sectors and ownership forms; and

- maintains similar overall volatility when viewed through risk-factor exposure (equity, duration, inflation). If the institution has a long horizon, low near-term spending needs, and robust risk management, the higher expected return with similar factor risk justifies accepting higher illiquidity and implementation complexity. The committee should still confirm that capital call scenarios and the denominator effect do not jeopardize funding or regulatory limits.

Revision Tip: PE/VC allocations require rigorous liquidity planning. Model cash flows, capital calls, and stress scenarios (for example, a repeat of 2008–2009) to avoid becoming a forced seller of liquid assets or breaching allocation limits during market downturns.

Exam Warning: Many candidates misstate the diversification benefit of PE/VC. While correlation with public equities can appear low based on reported returns, during crises it rises and appraisal smoothing masks true risk. In essay questions, differentiate between reported correlation and actual economic exposure, and relate diversification benefits to strategy mix, sector exposure, and vintage diversification—not merely the “private” label.

Summary

Private equity and venture capital offer portfolios potential for higher returns, access to private markets, and some diversification from public equities. They carry unique risks: illiquidity, staggered capital drawdowns, high manager return dispersion, and diversification challenges across vintages, sectors, and geographies.

Key return drivers include operational value creation, use of leverage, and changes in entry and exit valuation multiples, all layered on top of an illiquidity premium. Key risk drivers include capital call and commitment risk, J‑curve effects, valuation uncertainty, leverage, and vintage-year cyclicality. These risks interact strongly with investor-specific characteristics—horizon, liquidity needs, governance capacity, and regulatory constraints.

From a portfolio standpoint, PE/VC should be analyzed in terms of their contributions to factor exposures (equity, value, size, leverage, illiquidity) and their impact on the total risk budget. Robust implementation requires:

- well-calibrated commitments and pacing across vintage years;

- careful manager selection and monitoring; and

- liquidity and scenario analysis that recognises the denominator effect and potential stress correlations.

On the CFA Level 3 exam, most PE/VC questions ask you to evaluate suitability, size, and structure of allocations—not to value individual deals. Clear reasoning about risk, return, liquidity, and investor objectives is essential.

Key Point Checklist

This article has covered the following key knowledge points:

- Strategic roles of private equity and venture capital in institutional and individual portfolios, including return enhancement, diversification, and access to unique opportunities

- Main return and risk drivers: operational value creation, leverage, multiple expansion, illiquidity premium, and deal/vintage effects

- Effects of illiquidity, capital calls, commitment risk, and the J‑curve on multi-asset portfolios and liquidity management

- Diversification, correlation, and manager selection considerations, including manager dispersion and vintage-year cyclicality

- Comparisons between private and public equity in terms of transparency, governance, costs, performance measurement, and implementation complexity

- Use of factor-based and goals-based approaches to integrate PE/VC into strategic asset allocation and to assess their impact on long-term funding and spending objectives

- Risk mitigation methods and liquidity planning for PE/VC allocations, including pacing, secondary sales, and scenario analysis

Key Terms and Concepts

- private equity (PE)

- venture capital (VC)

- illiquidity premium

- secondary market (private equity)

- dry powder

- carried interest