Learning Outcomes

This article explains the inflation-hedging, gearing, and vehicle-selection features of real estate and infrastructure for CFA Level 3 candidates, including:

- the key economic characteristics that allow real estate and infrastructure cash flows and valuations to respond to changes in inflation, and why the inflation linkage is often imperfect;

- how to evaluate the strength of inflation protection using lease terms, regulatory structures, tariff indexation, market power, and demand sensitivity;

- the sources of explicit and embedded gearing in real estate and infrastructure investments, and how gearing magnifies returns, volatility, interest-rate sensitivity, and refinancing risk;

- how gearing at project, company, and vehicle level interacts to shape overall portfolio risk, especially during stressed market conditions;

- the main investment vehicles used to access these assets—direct holdings, listed securities, private pooled funds, and hybrid or club structures—and their respective implications for liquidity, control, transparency, and fees;

- how vehicle structure influences the transmission of asset-level risks to investors, including pricing dislocations, governance conflicts, and gating or redemption restrictions;

- practical considerations for aligning inflation-hedging objectives, risk tolerance, and liquidity needs when selecting real estate and infrastructure vehicles in an exam vignette.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand how real estate and infrastructure function within multi-asset portfolios, particularly regarding inflation protection, gearing effects, and vehicle-related issues, with a focus on the following syllabus points:

- The rationale for using real estate and infrastructure as inflation hedges in portfolios

- The influence of gearing (explicit and embedded) on risk and return in these asset classes

- The selection and trade-offs of investment vehicles (private, public, direct, listed, pooled) for gaining exposure

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What key economic characteristics allow real estate and infrastructure to serve as inflation hedges?

- State the main risks associated with gearing in a private real estate investment trust (REIT).

- Which vehicle is most suitable for gaining diversified, liquid exposure to infrastructure if daily liquidity is a priority—direct private ownership, listed shares, or unlisted closed-end funds? Explain briefly.

Introduction

Real estate and infrastructure play a central role as real assets in diversified portfolios. Their unique characteristics—physical asset backing, tangible utility, and income-generating property—make them prominent candidates for investors seeking inflation protection. These assets also provide sources of gearing, both through direct use of debt and embedded gearing at project or company level. Understanding the choice of vehicle used to access these assets is essential, as it governs liquidity, risk, return, and operational oversight.

Key Term: inflation hedging

The use of assets whose income and/or capital values tend to rise with general price levels, helping preserve purchasing power. Key Term: gearing

The use of borrowed funds or financial structure to control larger asset exposure, amplifying both investment gains and losses. Key Term: investment vehicle

The legal and operational structure through which investors gain exposure to an asset class, including private funds, listed entities, direct holdings, and pooled funds.Test Tip: When revising Inflation hedging leverage and vehicles, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

REAL ESTATE AND INFRASTRUCTURE—INFLATION HEDGING ROLES

Both real estate and infrastructure are valued for their potential to protect a portfolio against unexpected inflation. Their revenues are often directly or indirectly linked to inflation:

- Real estate: Leases may contain rent escalation clauses indexed to inflation or allow periodic rent re-setting to market levels. Rising replacement costs for buildings also tend to support capital values.

- Infrastructure: Many projects have regulated or contracted revenue streams that link tariffs or user charges to inflation indexes, especially essential services (e.g., utilities, transport, energy).

However, the correlation is not perfect. The inflation-hedging effectiveness depends on contract structure, market power, and local inflation patterns. Both assets can underperform in severe downturns or if revenues are capped.

Key Term: real asset

A physical or tangible asset with economic value—such as property, infrastructure, commodities, or land—often used for its inflation protection and diversification qualities.

GEARING IN REAL ESTATE AND INFRASTRUCTURE

Gearing is common in both real estate and infrastructure, increasing the expected return while also heightening risk. Investors must distinguish:

- Explicit gearing: Borrowed capital at the company, project, or fund level (e.g., mortgages in direct property investment; project finance debt in infrastructure).

- Embedded gearing: Indirect exposure arising from ownership of equity in layered structures (e.g., in listed vehicles that themselves hold geared projects).

Gearing amplifies both returns and losses, making vehicle and structure key to risk control. High gearing increases interest rate sensitivity, refinancing risk, and illiquidity exposure.

Key Term: explicit gearing

The direct use of borrowed capital at the investment level, such as mortgages or project finance. Key Term: embedded gearing

Indirect gearing arising from equity interest in highly geared portfolio investments or subsidiaries.

Worked Example 1.1

A closed-end private equity fund buys a commercial property for $20 million, using $5 million investor capital and $15 million debt at 4% interest. After five years, operating income nets to $1.2 million annually, and the property sells for $25 million. Ignoring tax, what is the annualized return to equity?

Answer:

Debt service = $15m × 4% = $0.6m per year. Annual cash flow to equity: $1.2m − $0.6m = $0.6m. Over five years, cash flows total $3m, and sale proceeds after repaying debt = $25m − $15m = $10m (to equity). Total cash to equity over five years: $3m + $10m = $13m. IRR on $5m invested is approx. 21.7% annually. Gearing increased both the return and the risk of loss had values declined.Exam Warning: A common exam error is to assume real estate and infrastructure will always provide perfect inflation protection. In reality, inflation-hedging efficacy depends on lease terms, revenue indexation, regulatory settings, and market conditions. Always verify the link between asset cash flows and inflation before making portfolio assignments.

INFRASTRUCTURE—SPECIAL FEATURES

Infrastructure assets include transport (roads, airports), utilities (water, electricity, gas), communications, and social projects (schools, hospitals). Many are monopoly or quasi-monopoly providers, with high barriers to entry.

- Revenue model: Income streams can be regulated, contracted, or user-fee based. Degree of inflation linkage varies.

- Gearing: High project finance gearing is standard, but risk of default and refinancing remains—especially when base rates rise.

- Economic exposure: Infrastructure can be defensive if contracts protect cash flows; however, economic downturns can reduce demand for user-pay assets (e.g., toll roads).

Key Term: infrastructure

Real assets providing essential public services, often with long-term, stable cash flows and inflation-linked revenues.

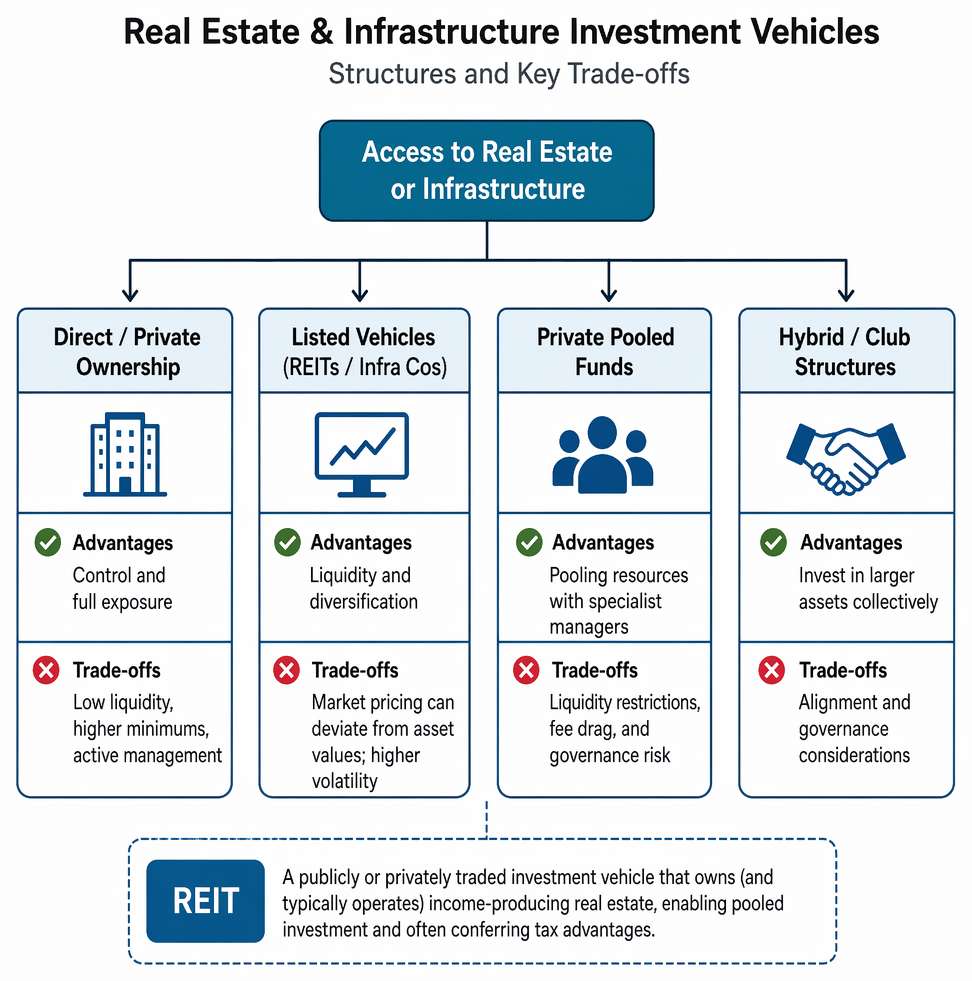

INVESTMENT VEHICLES—STRUCTURES AND SELECTION

Access to real estate or infrastructure can be through various vehicles, each with trade-offs:

Real estate and infrastructure gearing is classified by source and entity level, with effects on volatility, interest-rate sensitivity, and liquidity risk.

- Direct/private: Ownership of the asset itself (building or project SPV). Offers control and full exposure but low liquidity, higher minimums, and active management.

- Listed vehicles: Equities of REITs or infrastructure companies traded on markets. Offer liquidity and diversification, but market pricing can deviate from asset values and increase volatility.

- Private pooled funds: Unlisted open- or closed-end funds, commonly with specialist managers. Enable pooling resources, but come with liquidity restrictions, fee drag, and governance risk.

- Hybrid/club structures: Institutional investors may form consortia or club deals to invest in larger assets collectively.

Key Term: REIT (real estate investment trust)

A publicly or privately traded investment vehicle that owns (and typically operates) income-producing real estate, enabling pooled investment and often conferring tax advantages.

Worked Example 1.2

An institutional investor requires quarterly liquidity and daily valuation for its real estate allocation. Which vehicle is most suitable—private direct ownership, an open-ended core real estate fund, or a listed REIT?

Answer:

A listed REIT is most suitable due to public market liquidity and frequent pricing. However, the REIT’s returns may be more correlated with equity markets and can diverge from physical property values, especially in periods of market stress.

VEHICLE RISK AND DUE DILIGENCE

Vehicle selection affects:

- Liquidity: Listed vehicles enable easier trading but can see price disconnects from asset values. Private vehicles offer stability but restrict redemptions, sometimes locking investor capital for years.

- Control and governance: Direct investment provides oversight, but requires in-house capabilities. Funds and REITs outsource these functions to managers, creating principal-agent risks.

- Transparency and alignment: Open-ended funds may impose redemption gates or valuations based on appraisal estimates, impacting both reported volatility and risk.

Key Term: gating

Temporary restriction or suspension on investor withdrawals from a fund, typically used in periods of stressed liquidity.

Worked Example 1.3

A private open-ended real estate fund faces a surge in redemption requests during a downturn. It exercises gating provisions, delaying withdrawals for 12 months. What risk are investors experiencing?

Answer:

Investors face liquidity risk—they cannot exit their investment as planned, and may be exposed to additional property revaluations or forced asset sales, potentially impacting capital values.

Key Point Checklist

This article has covered the following key knowledge points:

- Real estate and infrastructure can serve as partial inflation hedges if revenues are sufficiently linked to price levels

- Gearing is standard and materially alters the risk/return profile of both asset classes

- Vehicle choice (direct, listed, pooled private, or hybrid) determines access, liquidity, transparency, control, and risk to capital

- Private vehicles offer less liquidity but more asset value stability; listed vehicles offer better liquidity but subject investors to equity-market volatility

- Detailed vehicle due diligence and structure assessment is essential to CFA exam answers

Key Terms and Concepts

- inflation hedging

- gearing

- investment vehicle

- real asset

- explicit gearing

- embedded gearing

- infrastructure

- REIT (real estate investment trust)

- gating