Learning Outcomes

This article explains real estate and infrastructure valuation for CFA Level 3 exam candidates, including:

- distinguishing income-based and appraisal-based approaches for commercial property and infrastructure, with emphasis on direct capitalization and DCF models

- calculating property values from NOI and cap rates, and interpreting capitalization and discount rates as risk-adjusted required returns

- assessing how appraisal frequency, subjectivity, and data limitations create smoothing, serial correlation, and understated volatility and correlations in return series

- evaluating the impact of smoothed real estate and infrastructure returns on portfolio risk, diversification assessment, and efficient frontier construction

- analyzing infrastructure-specific valuation issues, such as regulated or contracted cash flows, long asset lives, terminal value assumptions, and country or regulatory risk premiums

- identifying practical challenges in estimating inputs for private-market valuations, including illiquidity, sparse transaction evidence, and heterogeneous asset characteristics

- applying exam-style reasoning to evaluate reported performance statistics and adjust or reinterpret appraisal-based data in a multi-asset CFA context

- comparing listed (transaction-priced) and direct (appraisal-priced) real asset exposure when building or evaluating portfolios

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand the principles and practical issues involved in valuing real estate and infrastructure investments, with a focus on the following syllabus points:

- assessing and comparing income-based and appraisal-based valuation methods for real estate and infrastructure

- discussing how appraisal data may bias risk and volatility estimates and distort correlations with other asset classes

- calculating and interpreting capitalization rates, discount rates, and net operating income (NOI)

- understanding the impact of appraisal smoothing, illiquidity, and serial correlation on estimated returns and portfolio risk

- evaluating infrastructure assets’ valuation, considering regulatory or contractual elements and limited observable prices

- interpreting real estate and infrastructure statistics within an asset allocation and risk management framework

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A consultant builds an efficient frontier using a private real estate index whose returns are based on annual appraisals. Volatility appears far lower than equities and correlations are close to zero. Which conclusion is most appropriate?

- a) Real estate clearly offers superior diversification and should be maximized in the portfolio.

- b) The efficient frontier likely overstates diversification benefits because real estate returns are smoothed.

- c) The frontier is reliable because appraisals reduce unsystematic risk.

- d) The frontier understates diversification because appraisals ignore income returns.

-

A stabilized office building has current NOI of $2.5m, expected to grow at 2% per year. Investors require an 8% total return. Using a Gordon growth framework, the implied going‑in capitalization rate and value are closest to:

- a) Cap rate 8%; value $31.25m

- b) Cap rate 6%; value $41.67m

- c) Cap rate 10%; value $25.00m

- d) Cap rate 5%; value $50.00m

-

An unlisted toll road has cash flows governed by a 30‑year concession with government‑approved toll escalation. Which factor most increases the appropriate discount rate for valuing its cash flows?

- a) Strong inflation linkage of tolls

- b) Highly rated government counterparty

- c) History of unpredictable regulatory intervention in toll setting

- d) Low traffic volume volatility

-

An institutional investor wants to “unsmooth” a quarterly appraisal‑based real estate return series before estimating correlations. Which approach is most consistent with the curriculum?

- a) Replace the series with listed REIT returns from the same region.

- b) Apply a statistical adjustment that reverses the effect of serial correlation in the appraisal series.

- c) Multiply all appraisal returns by a constant to match equity volatility.

- d) Exclude real estate from the portfolio because valuation is subjective.

Introduction

Real estate and infrastructure asset valuations are distinctive in their use of income-based approaches, reliance on periodic appraisals, and the influence of illiquidity and smoothing on reported data. For CFA Level 3, competence in applying these techniques and recognizing data limitations is frequently tested where appraisal smoothing can misrepresent volatility and correlation, leading to faulty multi-asset portfolio conclusions.

In contrast to listed equities and bonds, many real estate and infrastructure assets trade infrequently and are often held in closed-end funds or separate accounts. Reported returns therefore come from periodic appraisals rather than continuous market pricing.

Key Term: Appraisal-based returns

Appraisal-based returns are return series for illiquid assets, such as commercial property or infrastructure, constructed from periodic third-party valuations or appraisals, rather than frequent market transactions. Key Term: Smoothing

Smoothing is an effect in which appraisal or estimated returns display artificially dampened volatility and correlation as compared to transaction-based returns, often due to infrequent or staggered valuation updates of individual assets.

From a portfolio management standpoint, the danger is straightforward: if you treat smoothed return series as if they were based on market transactions, you will typically understate risk, understate correlations, and overstate diversification benefits and Sharpe ratios. Level 3 questions often ask you to diagnose and correct this error qualitatively.

Test Tip: When revising Valuation income and appraisal issues, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Real Estate Valuation Approaches

Commercial real estate can be valued using three broad approaches:

- income approach

- sales comparison (market) approach

- cost approach

For investment-grade commercial property and income-producing infrastructure, the income approach dominates. Sales comparison is useful when there are many recent transactions in similar properties, and the cost approach is more relevant for special-purpose assets or as a ceiling on value (replacement cost), but exam questions focus primarily on income-based valuation and its implementation in appraisals.

Income-based Valuation

The dominant method for commercial property and income-producing infrastructure is the income approach, where value is derived from an asset’s capacity to generate net operating income (NOI) and, more broadly, cash flows.

Key Term: Net Operating Income (NOI)

NOI is the annual income expected from a property after deducting vacancy losses and operating expenses but before interest, taxes, depreciation, or amortization.

Care is needed in computing NOI:

- Use market rent, not necessarily current contract rent, for leases that will reset soon.

- Deduct a realistic vacancy and collection loss allowance.

- Deduct non-recoverable operating expenses and a reserve for recurring capital items (e.g., roof replacement).

- Exclude financing costs and income taxes (NOI is an unlevered property-level figure).

The most common income-based techniques are:

- Direct capitalization: Value is estimated by dividing NOI (typically one year of stabilized NOI) by a capitalization rate (cap rate).

- Discounted cash flow (DCF): Value is the present value of forecast future cash flows (multi-year), discounted at a risk-appropriate rate, plus a terminal value.

Key Term: Capitalization Rate (cap rate)

The capitalization rate reflects the required rate of return or yield on a property, incorporating the risk-free rate plus risk and illiquidity premiums, adjusted for expected income growth. Key Term: Direct capitalization

Direct capitalization is an income-based valuation method that converts a single period of stabilized NOI into value by dividing by a market-derived cap rate. Key Term: Discounted cash flow (DCF) valuation

Discounted cash flow valuation estimates asset value as the present value of a multi-period forecast of cash flows and a terminal value, discounted at a rate reflecting the asset’s risk.

Under direct capitalization:

where is next period’s stabilized NOI. The cap rate can also be interpreted using a Gordon growth relationship:

where is the required total return on the property and is the long‑run expected growth rate of NOI. This linkage helps you interpret changes in cap rates: a higher cap rate implies a higher required return, lower growth, or both.

Worked Example 1.1

A multi-tenant office building produces NOI of $1,200,000 and regional cap rates are 5.5%. What is the property’s indicative value under direct capitalization?

Answer:

Using direct capitalization,

This is an indication of value assuming the NOI is stabilized and the cap rate appropriately reflects property risk and growth expectations.

Worked Example 1.2

A property is expected to generate NOI of $3,000,000 next year, with NOI growing at 2% per year thereafter. Investors require an 8% total return on similar properties. Estimate the value using a Gordon growth framework.

Answer:

The implied cap rate is:> \text{Cap rate} = r - g = 0.08 - 0.02 = 0.06 \text{ (6%)}.

Value is:

This example illustrates how small changes in required return or growth assumptions can materially affect value.

When to Use DCF Instead of Direct Capitalization

Direct capitalization is most appropriate for stabilized properties with:

- predictable occupancy and expense ratios

- leases that are broadly in line with current market terms

- limited near-term capital expenditure requirements

DCF is more appropriate when:

- lease-up, redevelopment, or major capital expenditures will significantly change NOI over time

- there are material lease rollover risks (e.g., a single key tenant)

- the asset has a finite economic or contractual life

In a DCF, you project annual NOI or free cash flows to equity or to the firm, then add a terminal value at the end of the explicit forecast period.

Key Term: Terminal value

Terminal value is the estimated value of an asset at the end of an explicit forecast horizon, often calculated using a terminal cap rate applied to stabilized NOI in the final year, or using a perpetual growth model.

A common form for income-producing real estate is:

where are annual cash flows and is the terminal value.

Other Real Estate Valuation Approaches (for context)

Although the exam emphasizes income-based methods, you should be able to recognize:

- Sales comparison (market) approach: Value is inferred from prices of similar recently transacted properties, adjusted for differences in location, quality, lease terms, and other characteristics. Useful when comparable sales data are plentiful.

- Cost approach: Value is approximated as land value plus current replacement cost of the building, minus depreciation. Often provides a ceiling on value and is relevant for special-purpose assets that rarely trade.

In practice, appraisers often triangulate among these methods, but for investment analysis and exam questions, NOI/cap rate and DCF dominate.

Appraisal and Its Impact on Return Measurement

Required return components and expected NOI growth determine the capitalization rate, which is then applied to next-year NOI to estimate value.

Appraisal-based Valuation

Appraisals are typically performed quarterly or annually by independent valuers, especially for illiquid assets with infrequent trading. Appraisers usually apply income-based methods, supported by sales comparison data and professional judgment.

For portfolios of direct real estate or unlisted infrastructure, reported index values are therefore based on these appraisals. Because appraisals respond gradually to market information and are not updated continuously for every asset, published returns of direct real estate or unlisted infrastructure exhibit:

- lower reported volatility than transaction-based indices

- positive serial correlation (current returns are correlated with past returns)

- delayed recognition of market turning points

Key Term: Serial correlation

Serial correlation is the correlation of a time series with its own past values; in appraisal-based return series it reflects gradual, lagged adjustments of valuations rather than abrupt market moves. Key Term: Transaction-based index

A transaction-based index is a return series constructed solely from actual market transaction prices, rather than appraisals, and therefore reflects contemporaneous market volatility more accurately.

Worked Example 1.3

A pension fund holds retail malls appraised annually. Portfolio return volatility is 5%, while public REITs in the same region show 15% volatility. What is a likely explanation for the difference?

Answer:

The lower volatility is mainly due to appraisal smoothing, not genuine lower economic risk. Because properties are appraised infrequently and appraisers often rely on prior values with incremental adjustments, valuation changes are dampened relative to market prices of comparable listed securities. Key Term: Appraisal smoothing

Appraisal smoothing occurs when return variation is dampened by infrequent or subjective revaluations, causing understated risk and correlation estimates and positive serial correlation in reported returns.

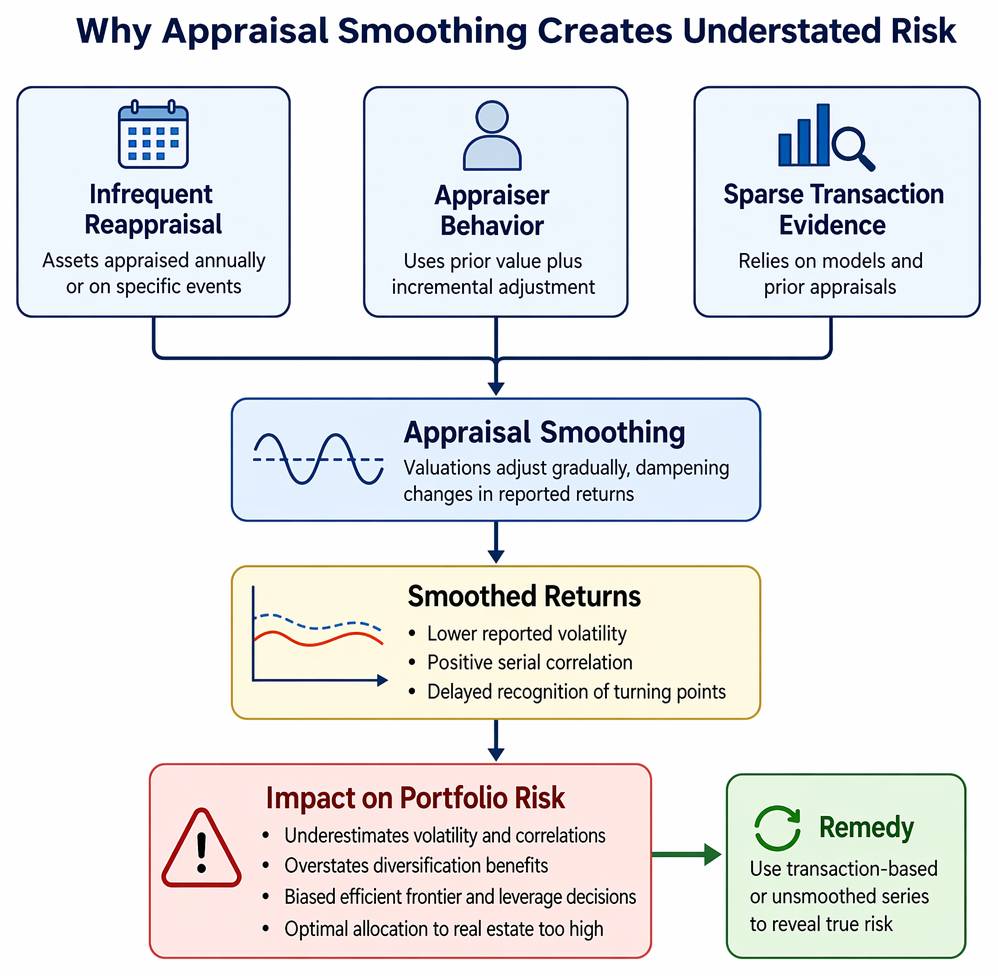

Why Appraisals Create Smoothing

Several mechanisms drive smoothing:

- Infrequent reappraisal: Individual assets may be appraised only annually or when specific events occur (e.g., refinancing), so not all assets in an index reflect current conditions at any given time.

- Appraiser behavior: Appraisers often use a “previous value plus adjustment” process rather than fully re-marking to the latest comparable transaction, partly to avoid appearing volatile or speculative.

- Sparse transaction evidence: When very few comparable trades exist, appraisers may rely heavily on models and prior appraisals, which slows adjustment.

The result is that appraisal-based indices look bond-like—smooth and low volatility—even though the actual assets may be equity-like in risk.

Key Term: Unsmoothing

Unsmoothing is the process of statistically adjusting appraisal-based return series to reverse the effects of smoothing and serial correlation, producing a better estimate of the true economic volatility and correlations.

Practitioners sometimes model appraisal returns as a lagged, smoothed version of true economic returns and mathematically “unsmooth” the series. For the exam, you do not need to apply formulas, but you should understand the objective: increase estimated volatility and correlations to better approximate true market risk.

Appraisal Smoothing: CFA Portfolio Risk Implications

Smoothing can distort asset allocation decisions by:

- underestimating the contribution of real estate or infrastructure to total portfolio volatility

- underestimating correlations with other asset classes and overestimating diversification benefits

- biasing risk–return efficient frontiers, making real estate or infrastructure appear to offer unusually attractive risk-adjusted returns

- overstating the attractiveness of leverage or allocations based on naïve mean–variance optimization using smoothed data

From a Level 3 exam standpoint, when you see a portfolio optimization that uses appraisal-based return series, you are expected to:

- question whether volatilities and correlations are realistic

- discuss the impact on recommended allocations (e.g., “allocation to private real estate is likely too high”)

- propose remedies (e.g., use transaction-based proxies, unsmoothed series, or scenario analysis)

Worked Example 1.4

An optimizer is run using a private real estate index with 4% volatility and 0.1 correlation with equities. A candidate suggests replacing that with an unsmoothed series showing 10% volatility and 0.5 correlation with equities. How is the optimal allocation to real estate likely to change?

Answer:

With higher estimated volatility and higher correlation to equities, the optimizer will view real estate as less powerful for diversification. All else equal, the optimal allocation to real estate will fall, and the efficient frontier will shift to reflect higher portfolio risk for a given return. This is a classic exam-style question linking data quality to asset allocation outcomes.Exam Warning: Many candidates overstate the diversification benefit of direct real estate because they ignore appraisal smoothing. Remember, use unsmoothed or transaction-based series for realistic multi-asset risk analysis; at minimum, comment qualitatively that smoothing likely understates risk and correlations.

Infrastructure Asset Valuation: Special Considerations

Infrastructure assets (such as toll roads, airports, ports, pipelines, or utility networks) are long-lived, often monopolistic, and may be regulated. Their valuation requires careful attention to:

- the nature of the cash flows (regulated, contracted, or demand-based)

- the asset life (economic life vs concession life)

- the regulatory or contractual framework

- country, political, and regulatory risks

- illiquidity and limited comparable transactions

Key Term: Infrastructure asset

An infrastructure asset is a physical, typically long-lived and essential real asset that generates cash flows under long-term contractual, regulatory, or monopoly regimes, such as toll roads, utilities, and regulated pipelines.

Key distinctions include:

-

Core vs opportunistic infrastructure:

- Core infrastructure (e.g., regulated utilities, mature toll roads) tends to have stable, inflation-linked cash flows and lower required returns.

- Opportunistic infrastructure (e.g., greenfield projects, merchant power plants) carries significant construction, volume, or price risk and demands higher discount rates.

-

Regulated vs user-pay:

- Regulated utilities often earn a rate of return on a regulated asset base (RAB), set by the regulator. Valuation commonly uses the allowed weighted average cost of capital (WACC) as the discount rate.

- User-pay assets (e.g., toll roads, airports) depend on demand volumes and pricing flexibility; cash flows are more uncertain.

Infrastructure valuations are usually DCF-based because of long horizons and explicit contractual structures. Income may be modeled net of operating expenditures, maintenance capex, and taxes, often with explicit inflation indexation.

Worked Example 1.5

A regulated water utility expects after-tax operating cash flows of $20m/year for 15 years, with a regulatory WACC discount rate of 6%. What is the current asset value (ignore terminal value)?

Answer:

The present value of an annuity of $20m for 15 years at 6% is:

Evaluating the factor:

So:

Using the regulatory WACC as the discount rate is consistent with valuing a regulated asset whose cash flows are determined by that allowed return.

Terminal Value and Concession Risk

Terminal value assumptions are particularly important for infrastructure:

- Some assets (e.g., perpetual utilities) may be treated as going-concern with a terminal value based on a perpetual growth model or a terminal cap rate.

- Concession-based assets (e.g., a 30‑year toll road concession) may have no residual value to the private owner at concession end, or a reversionary value determined by contract.

- Technological or policy changes can erode terminal value (e.g., reduced demand for fossil-fuel pipelines).

Terminal value often accounts for a large share of total DCF value. Level 3 questions may ask you to question excessive reliance on aggressive growth or cap rate assumptions in the terminal value.

Country, Regulatory, and Illiquidity Risk

Discount rates for infrastructure should reflect:

- Country risk premiums: Higher in emerging markets, reflecting political and macroeconomic risk (e.g., expropriation, currency controls).

- Regulatory risk: Unpredictable tariff resets or rule changes increase risk and required return.

- Illiquidity: Unlisted infrastructure is typically less liquid than listed securities; investors require a premium.

Exam tasks may include comparing two valuations where one analyst fails to reflect regulatory or country risk in the discount rate. You should be able to identify underestimation of risk and overvaluation.

Worked Example 1.6

Two analysts value the same toll road:

- Analyst A discounts expected cash flows at 7%, based on developed market government yields plus a modest risk premium.

- Analyst B uses 10%, adding a country risk premium and an allowance for regulatory uncertainty.

Which analyst’s valuation is more conservative, and why?

Answer:

Analyst B’s valuation is more conservative. The higher discount rate reflects additional risks: country and regulatory uncertainty and illiquidity. All else equal, the 10% rate will produce a lower present value, reducing the risk of overpaying for an asset whose cash flows may be impaired by adverse policy changes or macro shocks.

Appraisal Issues in Private Real Estate and Infrastructure

Appraisal-based valuations for private real estate and infrastructure face several practical challenges that are highly relevant in exam questions:

- Difficult input estimation: NOI, cap rates, and discount rates may be hard to estimate reliably because of tenant quality, lease covenants, co-tenancy provisions, and market uncertainty.

- Heterogeneity of assets: No two properties or infrastructure assets are identical. Differences in location, design, age, and contract structures limit the usefulness of comparables and increase reliance on judgment.

- Illiquidity and sparse transactions: Long periods may pass without arm’s-length transactions in a given submarket or asset type, making it hard for appraisers to calibrate values.

- Appraisal lag: Direct property appraisals often lag actual market prices, especially during rapid market moves—both up and down.

- Valuation frequency and methodology differences: Different appraisers may use different models or assumptions, leading to cross-sectional inconsistencies in reported values.

These issues are conceptually similar for private infrastructure, but infrastructure often has additional layers:

- Complex project finance structures and leverage

- Detailed concession or regulatory contracts

- Non-linear cash flow sensitivities (e.g., volume thresholds in toll roads)

From a portfolio and performance measurement standpoint:

- Illiquidity further biases risk and correlation estimates, complicating performance measurement, benchmarking, and peer comparisons.

- Reported Sharpe ratios may be overstated because volatility is understated while average returns (income yield plus smooth capital appreciation) are unaffected by smoothing.

Worked Example 1.7

A consultant compares two funds over 10 years:

- Fund X: Listed infrastructure equities, annualized return 9%, volatility 18%.

- Fund Y: Unlisted, appraisal-based infrastructure, annualized return 8%, volatility 6%.

The consultant argues that Fund Y is clearly superior on a risk-adjusted basis and recommends shifting capital from Fund X to Fund Y. Assess this recommendation.

Answer:

The comparison is flawed. Fund Y’s lower reported volatility is partly due to appraisal smoothing and illiquidity, not necessarily lower economic risk. Its true volatility and correlation with equities are likely higher than reported. Without unsmoothing or using transaction-based proxies, the apparent Sharpe ratio advantage may be illusory. A better approach is to adjust Fund Y’s risk estimates or analyze scenario outcomes before reallocating.

Summary

Income-based and appraisal-based valuations dominate real estate and infrastructure analysis. For commercial property, direct capitalization and DCF models translate NOI and growth assumptions into values; cap rates and discount rates embed risk-free rates, risk premiums, growth expectations, and illiquidity premia. Infrastructure valuation builds on the same principles but must incorporate regulatory frameworks, concession structures, contract terms, and country risk.

Because many real assets are valued by periodic appraisals rather than continuous market trading, their reported return series are smoothed: volatility and correlations are understated, and serial correlation is introduced. Using these smoothed series directly in portfolio optimization leads to over-allocation to real estate or infrastructure and overstatement of diversification benefits.

For CFA Level 3, you must both execute the mechanics of income-based valuation (NOI, cap rates, DCF) and critically evaluate reported performance statistics. When you see low volatility and low correlations for appraisal-based assets, you should immediately consider smoothing, illiquidity, and estimation error, and adjust your portfolio conclusions accordingly.

Key Point Checklist

This article has covered the following key knowledge points:

- differentiate income-based (NOI/cap rate, DCF) and appraisal-based real asset valuations

- calculate property value using NOI and cap rate; understand how discount rates and cap rates reflect required return, growth, and risk premiums

- recognize when to prefer direct capitalization versus multi-period DCF for real estate and infrastructure

- identify and explain appraisal-based returns, smoothing, and positive serial correlation in private real asset indices

- recognize the pitfalls of using unadjusted appraisal data for portfolio risk analysis (volatility, correlation, Sharpe ratios, efficient frontier)

- describe the role of unsmoothing and transaction-based indices in obtaining more realistic risk estimates

- list practical challenges in valuing infrastructure (illiquidity, contractual cash flows, regulatory discount rates, terminal value, and country/regulatory risk)

- analyze infrastructure valuations, distinguishing core/regulated assets from opportunistic/merchant assets and adjusting discount rates accordingly

- apply exam-style reasoning to evaluate reported real estate and infrastructure performance statistics in multi-asset portfolio contexts

Key Terms and Concepts

- Appraisal-based returns

- Smoothing

- Net Operating Income (NOI)

- Capitalization Rate (cap rate)

- Direct capitalization

- Discounted cash flow (DCF) valuation

- Terminal value

- Serial correlation

- Transaction-based index

- Appraisal smoothing

- Unsmoothing

- Infrastructure asset