Learning Outcomes

This article explains calendar-based and threshold-based rebalancing techniques in institutional portfolios and clarifies how overlays are used to adjust exposures efficiently within CFA Level 3–relevant contexts. It defines the mechanics of each rebalancing approach, contrasts their triggers, monitoring requirements, and sensitivity to market volatility, and highlights their impact on risk control, turnover, and transaction costs. It discusses how to select appropriate rebalancing policies given liquidity constraints, implementation capacity, and governance considerations, including when hybrid calendar–threshold frameworks are appropriate. It examines how derivative-based overlays can be structured to implement synthetic rebalancing, manage temporary cash positions, and coordinate exposures across multiple managers or sub-portfolios. It reviews common implementation pitfalls, such as excessive trading, inadequate monitoring, and basis risk, and links these issues to typical CFA Level 3 vignette questions. It reinforces exam-oriented skills such as comparing methods in a scenario, identifying the preferable policy given portfolio objectives and constraints, and interpreting how rebalancing choices affect tracking error relative to a strategic asset allocation.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand portfolio rebalancing techniques and overlays, with a focus on the following syllabus points:

- Explain and compare calendar-based and threshold-based (range) rebalancing approaches

- Articulate how overlays (e.g., derivatives) can be used to adjust exposures and facilitate rebalancing

- Assess trade-offs between different rebalancing policies with regard to risk, cost, and diversification benefits

- Describe key implementation issues and best practices for institutional portfolios

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which type of rebalancing—calendar or threshold—is more responsive to changing market volatility and why?

- State one main advantage and one key disadvantage of using threshold-based rebalancing in an illiquid portfolio.

- Explain the term "overlay" in portfolio management and outline one practical use.

- What is a typical operational challenge when implementing overlay rebalancing using derivatives?

Introduction

Rebalancing brings portfolios back to target weights as asset prices change or cash flows occur, maintaining alignment with investment policy and risk budgets. Two common approaches are calendar rebalancing (rebalance at set intervals regardless of drift) and threshold (range) rebalancing (rebalance only if weights move beyond set bands). Portfolio overlays—often using derivatives—can also adjust exposures or implement rebalancing efficiently. CFA candidates must understand the operation, benefits, and limitations of each approach and their application across institutional portfolios.

Key Term: rebalancing

The process of adjusting a portfolio’s asset class or factor exposures back to target allocations as market values change.Test Tip: When revising Calendar vs threshold rebalancing, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

CALENDAR-BASED REBALANCING

Calendar-based (periodic) rebalancing means returning a portfolio to its target weights on a fixed schedule, such as monthly, quarterly, or annually. No regard is given to the extent of drift between scheduled dates; only the passage of time triggers trades.

Key Term: calendar rebalancing

Rebalancing executed at regular, predefined intervals, regardless of the amount of drift from target allocations.

Strengths

- Simple, requiring minimal monitoring

- Predictable—facilitates operational planning and reporting

- Lower ongoing monitoring/resource needs

Weaknesses

- May allow risk exposures to drift far from target between rebalance dates

- Can result in unnecessary turnover/costs if the portfolio remains within desired range

- Less responsive to increased volatility or major market shocks

Worked Example 1.1

Question: A pension fund uses annual rebalancing. In a year of market turmoil, equities appreciate dramatically and reach 75% of portfolio value (vs. a 60% target) just two months after the last rebalance. What is the risk consequence?

Answer:

The portfolio will remain over-exposed to equities and under-allocated to other assets for 10 months, increasing tracking error relative to policy, exposing the fund to unintended risk, and potentially departing from policy objectives.

THRESHOLD-BASED REBALANCING

Threshold (range or tolerance band) rebalancing monitors actual asset weights and triggers trades only when an asset class moves outside pre-set allowable bounds (e.g., +/- 5% around target). The portfolio is rebalanced only when a limit is breached, rather than on a routine schedule.

Key Term: threshold rebalancing

Rebalancing triggered when an asset class or factor allocation moves outside a specified range, relative to its target allocation.

Strengths (Threshold-Based)

- More risk-controlled: addresses dangerous deviations faster, especially during high volatility

- May lower trading costs and turnover when assets remain within bands

- Efficient for portfolios subject to large or random cash flows

Weaknesses (Threshold-Based)

- Requires frequent monitoring and greater operational complexity

- Rebalance timing is less predictable

- Potentially many small trades if volatility is high

Setting Tolerance Bands

Typical ranges are fixed (e.g., ±5%) or proportional (e.g., ±20% of target). Often, riskier or less liquid assets are assigned wider bands to minimize transaction costs.

Worked Example 1.2

An endowment's policy allocates 40% to bonds (range: 36–44%). After a market rally, bonds fall to 35.8% of portfolio. What happens?

Answer:

The breach of the lower tolerance triggers a rebalancing trade, which will restore bonds to target, selling outperforming assets and buying bonds. If no breach occurred, no trade would be made.Exam Warning: If asked to compare rebalancing approaches, do not confuse frequency (calendar) with sensitivity (threshold)—the methods serve different control purposes.

REBALANCING WITH OVERLAYS

Rebalancing overlays typically use derivatives (e.g., futures, swaps) to synthetically adjust asset exposures without direct trading in the physical securities. Overlays are common when physical trading is costly, impractical, or would disrupt implementation across sub-portfolios or complex structures.

Key Term: overlay

A position—often using derivatives—added to a portfolio to efficiently alter asset, currency, or risk factor exposures, especially for rebalancing. Key Term: synthetic rebalancing

Changing the effective portfolio exposures using derivatives, not direct trading in the physical assets.

Typical Uses

- Temporary adjustment to exposures pending physical rebalancing

- Handling large cash inflows/outflows prior to full investment (“equitization”)

- Efficiently rebalancing illiquid portfolios or across multiple managers

Worked Example 1.3

Question: A large sovereign wealth fund wishes to rebalance from domestic equities into global equities. Trading the physical stocks would take weeks. What overlay approach is used?

Answer:

The fund can sell domestic equity futures and buy global equity index futures in desired proportions, quickly matching exposure to policy targets. Later, physical trades can be completed if necessary.

Implementation Considerations

- Margin and collateral requirements for derivatives

- Overlays may introduce basis risk if derivatives do not perfectly match asset exposures

- The timing and cost of rolling contracts must be planned

- Policies should define when overlays are permitted and the risk limits applied

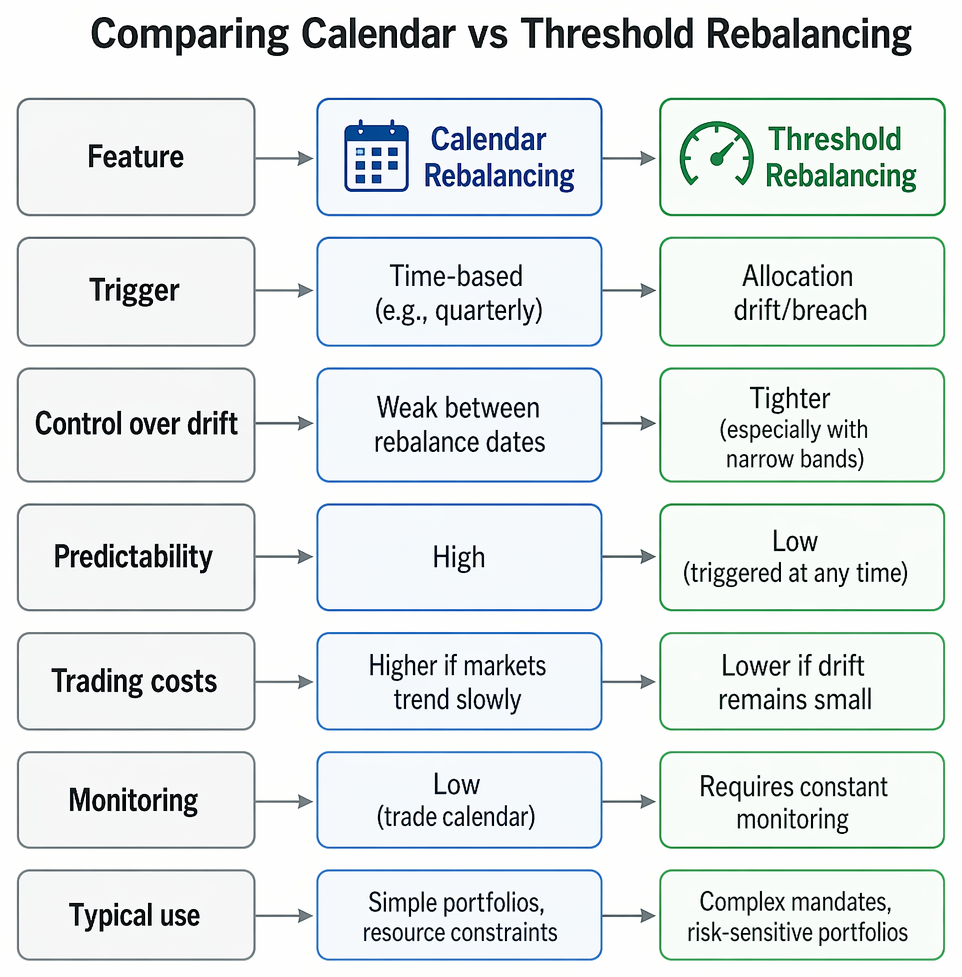

COMPARING CALENDAR VS THRESHOLD REBALANCING

Calendar rebalancing restores strategic asset weights at predetermined dates while tolerating interim allocation drift caused by market price changes.

| Feature | Calendar Rebalancing | Threshold Rebalancing |

|---|---|---|

| Trigger | Time-based (e.g., quarterly) | Allocation drift/breach |

| Control over drift | Weak between rebalance dates | Tighter (especially with narrow bands) |

| Predictability | High | Low (triggered at any time) |

| Trading costs | Higher if markets trend slowly | Lower if drift remains small |

| Monitoring | Low (trade calendar) | Requires constant monitoring |

| Typical use | Simple portfolios, resource constraints | Complex mandates, risk-sensitive portfolios |

Key Point Checklist

This article has covered the following key knowledge points:

- Recognize that calendar and threshold rebalancing are the main techniques to bring portfolios back to target weights

- Identify that calendar rebalancing is simple and predictable but can allow exposures to drift significantly between scheduled dates

- Explain that threshold (range-based) rebalancing ensures risk is controlled more tightly but needs ongoing monitoring and adds complexity

- Describe overlays as a synthetic tool—using derivatives—to facilitate efficient exposure adjustments and rebalancing

- Appreciate that overlay rebalancing is efficient in illiquid, multi-manager, and large portfolios, but requires robust derivative management and risk policies

Key Terms and Concepts

- rebalancing

- calendar rebalancing

- threshold rebalancing

- overlay

- synthetic rebalancing