Learning Outcomes

This article explores cash equitization and futures overlays in institutional portfolios, including:

- understanding why temporary cash balances create performance drag and tracking error versus fully invested benchmarks

- defining cash equitization and futures overlay strategies and distinguishing their roles in institutional rebalancing

- calculating the number of futures contracts required to equitize cash or adjust asset-class exposures using notional and beta-based formulas

- assessing how futures overlays can minimize tracking error during rebalancing, transitions between managers, or staged trading

- evaluating implementation steps, such as contract selection, trade timing, and sizing, in realistic CFA Level 3-style scenarios

- identifying key risks and limitations of overlay strategies, including basis risk, roll risk, liquidity constraints, and operational errors

- interpreting exam-style case facts to determine when a cash equitization or futures overlay solution is appropriate and how it should be structured

- linking overlay decisions to broader portfolio management objectives, such as maintaining strategic asset allocation and meeting policy benchmark requirements

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand the application of rebalancing and overlay techniques for managing portfolio exposures, with a focus on the following syllabus points:

- Define and explain the purpose of cash equitization and futures overlays in portfolio management

- Calculate and implement overlay positions using futures for institutional portfolios

- Evaluate overlay effectiveness in minimizing tracking error during rebalancing or transition

- Identify implementation considerations and risks for overlays in institutional settings

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

What is the primary objective of a cash equitization overlay for an index-tracking equity fund?

- a) To increase leverage and outperform the benchmark over the long term

- b) To maintain benchmark-like equity exposure when cash holdings are temporarily elevated

- c) To hedge currency risk associated with foreign equity holdings

- d) To avoid the need to rebalance the physical equity portfolio

-

A pension fund holds $25 million in temporary cash but wants immediate exposure to the S&P 500. S&P 500 futures trade at 5,000 with a contract multiplier of 250, and the futures beta is 1.0. The target beta is 1.0. How many contracts should be bought to equitize the cash (ignoring rounding guidance nuances)?

- a) 20

- b) 25

- c) 50

- d) 200

-

During a transition from one active equity manager to another, a fund sells equities on Day 1 and receives cash proceeds, but the new manager will only be funded over the next 10 trading days. Which action best minimizes tracking error relative to the fully invested equity benchmark during the transition?

- a) Leave the portfolio in cash until the new manager is fully funded

- b) Invest the cash in short-term government bills and accept temporary underperformance

- c) Use an equity index futures overlay to maintain equity exposure until the new manager is fully funded

- d) Use interest rate swaps to convert the cash return into an equity-like return

-

Which pair of risks is most directly associated with ongoing futures overlay programs?

- a) Style drift and benchmark misclassification

- b) Basis risk and roll risk

- c) Credit risk of held equities and inflation risk

- d) Reinvestment risk and duration risk

Introduction

Cash balances often arise in managed portfolios due to contributions, redemptions, asset reallocation, or manager transitions. If left uninvested, these balances temporarily reduce the portfolio's market exposure, causing performance drag and potentially creating unwanted tracking error versus a benchmark that is assumed to be fully invested.

Overlay strategies such as cash equitization using futures or rebalancing overlays are used to efficiently maintain intended exposures and minimize deviations from target allocations. In Level 3 case vignettes, these tools often appear when the portfolio’s policy allocation is clear, but implementation is constrained by timing, liquidity, or operational factors.

Key Term: cash equitization

The process of using derivatives (typically futures) to convert a temporary cash position into exposure that mimics a benchmark or intended asset class until the cash can be physically invested. Key Term: overlay (futures overlay)

A derivative position, usually in futures, implemented on top of an existing portfolio to adjust a portfolio's risk exposure independently of the existing assets.

These strategies are especially important for institutional investors—pension funds, endowments, insurance companies—whose mandates are framed relative to policy benchmarks. For such investors, even short periods of under- or over-exposure can generate material tracking error and governance issues, even if long-run performance is unaffected.

CASH EQUITIZATION: PURPOSE AND MECHANICS

Temporary cash balances can arise from portfolio cash inflows, asset sales, or pending contributions. Examples include:

- a large pension contribution received mid-month

- proceeds from liquidating an equity manager that will be redeployed later

- staged implementation of a new asset class where trading must be spread over days or weeks

If these balances are left in cash while the benchmark remains fully invested in equities or bonds, the portfolio is effectively underweight risk assets versus its benchmark. The consequences:

- expected underperformance if the benchmark asset rises

- lower portfolio volatility than the benchmark

- positive or negative tracking error, depending on how markets move during the under-invested period

Cash equitization overlays address this by providing synthetic risk exposure using futures contracts until physical investment is possible. Instead of trying to rush potentially costly or illiquid trades, the manager can:

- hold the cash safely in money market instruments, while

- using futures to overlay the desired equity (or bond) exposure

The combined position (cash + futures) aims to replicate the benchmark’s return on the portion of the portfolio that is temporarily in cash.

Key Term: tracking error

The standard deviation of the difference between a portfolio's returns and its benchmark, often caused by unintended under- or over-exposures.

Basic notional exposure approach

In the simplest case—equitizing domestic cash to a broad, well-matched equity index—the number of futures contracts is based purely on notional exposure:

- Determine the dollar exposure you want: typically the cash amount to equitize, .

- Compute exposure per contract: futures price × contract multiplier, .

- Compute the number of contracts: Positive implies a long futures position (equity exposure). Because you cannot trade fractional contracts, you must round up or down. In practice, the direction of rounding depends on whether the investor prefers a slight under- or over-exposure relative to target.

Beta-adjusted formulation

When the futures contract does not have a beta of 1.0 relative to the desired benchmark, or when the cash equitization is part of a broader equity exposure adjustment, a more general formula is used:

where:

- = number of futures contracts (positive for long, negative for short)

- = target beta for the equitized position (often 1.0 to match the index)

- = beta of the futures contract relative to the desired benchmark (often ≈1.0 for major index futures)

- = dollar value of the cash position to equitize

- = futures contract value (futures price × contract multiplier)

For pure cash equitization, the current beta of the cash position is zero, so the formula simplifies to the above.

Worked Example 1.1

A pension fund receives a $20 million cash contribution and wants immediate S&P 500 exposure via futures. The S&P 500 future is trading at $4,400, and the contract multiplier is 250. How many contracts should be purchased?

Answer:

Exposure per contract = $1,100,000. Required contracts:

If partial contracts are not allowed, the manager must choose 18 or 19 contracts.

- 18 contracts → $19.8 million exposure (slight under-equitization)

- 19 contracts → $20.9 million exposure (slight over-equitization) In practice, many institutional investors accept a small underweight and buy 18 contracts, but the decision should be consistent with the fund’s risk tolerance and tracking error objectives.

Worked Example 1.2

Cash equitization using the beta-adjusted formula

A Japanese equity index fund benchmarked to the Nikkei 225 has JPY 140 million of excess cash. Nikkei 225 futures trade at JPY 23,000 with a contract multiplier of JPY 1,000, so each contract has a value of JPY 23 million. The target beta is 1.0 and the futures beta is 1.0. How many contracts should be bought to equitize the cash?

Answer:

Using the beta-based formula with:

The fund would buy 6 contracts, providing approximately JPY 138 million of synthetic equity exposure. The small residual cash remains in money market instruments.

This example mirrors the structure of many exam questions: you will be given cash amount, futures price and multiplier, and possibly betas, and be asked to compute and explain why the overlay reduces tracking error.

REBALANCING AND FUTURES OVERLAYS

Rebalancing is the adjustment of portfolio holdings to align with target asset allocation. In practice, achieving the target allocation precisely and immediately is often impossible due to:

- market impact and trading costs

- limited liquidity in certain securities

- operational constraints (e.g., the need to liquidate one manager before funding another)

- governance processes that delay physical trades

These realities can create short-term deviations between actual and desired exposures—e.g., during a transition between managers, when implementing a new asset class, or if trading is staged over several days. A futures overlay can temporarily neutralize any mismatch, reducing unwanted risk or tracking error.

Key Term: rebalancing overlay

A derivative overlay used to maintain intended portfolio exposures during transitions or asset class allocation adjustments until physical trades settle.

Using futures to adjust equity exposure (general formula)

When the current portfolio already has equity exposure (beta ) and you want to change that exposure to a target beta , the required number of equity index futures contracts is:

where:

-

= current beta of the equity portfolio

-

= desired (target) beta after overlay

-

= beta of the futures contract

-

= current market value of the equity portfolio being adjusted

-

= value per futures contract

-

If , buy futures to add equity market exposure.

-

If , sell futures to reduce equity market exposure.

For rebalancing between asset classes, this formula is applied to the portion of the portfolio whose equity exposure you wish to change.

Worked Example 1.3

Overlay to increase equity exposure temporarily

An institutional portfolio has $100 million in global equities with beta to the MSCI World Index. The investment committee approves a temporary tactical overweight to beta 1.0 for the next three months using MSCI World futures. Futures trade at 2,500 with a multiplier of 50, so each contract value is $125,000. The futures beta is 1.0. How many contracts should be traded, and in which direction?

Answer:

= \left(\frac{1.0 - 0.8}{1.0}\right)\left(\frac{100{,}000{,}000}{125{,}000}\right) = 0.2 \times 800 = 160$$ The computed result is positive: $$> N_f = 160 > 0$$ Therefore, the manager **buys** 160 futures contracts, increasing overall equity market sensitivity from beta 0.8 to approximately 1.0 without changing the current holdings.

Apply the beta-adjustment formula:

Rebalancing overlays during staged trading

In many Level 3 scenarios, an institution wants to shift allocation between asset classes, but trading must be staged over time to manage costs or liquidity.

Worked Example 1.4

An endowment wishes to shift 10% of its $200 million portfolio from bonds to equities over five days; trades will be staged $4 million per day. To remain fully exposed to equities during those five days, how might a futures overlay be used?

Answer:

On Day 1, the target shift is $20 million (10% of $200 million) from bonds to equities, but only $4 million of equities will be physically purchased that day. The portfolio is underweight equities by $16 million on Day 1, $12 million on Day 2, and so on. To neutralize this temporary underweight:

- At the start of Day 1, the manager buys equity index futures with $20 million notional exposure.

- At the end of each day, as an additional $4 million of equities are purchased, the manager reduces the overlay by $4 million notional (selling the corresponding number of futures contracts).

- By Day 5, the full $20 million has been moved into physical equities and the overlay is reduced to zero.

Throughout the period, the combination of physical equities plus futures closely approximates the target equity exposure, minimizing tracking error versus the fully implemented strategic allocation.

This logic extends directly to more complex transitions (e.g., changing managers or implementing new mandates): futures are used to maintain asset-class exposure while the actual, security-level portfolio is being reconfigured.

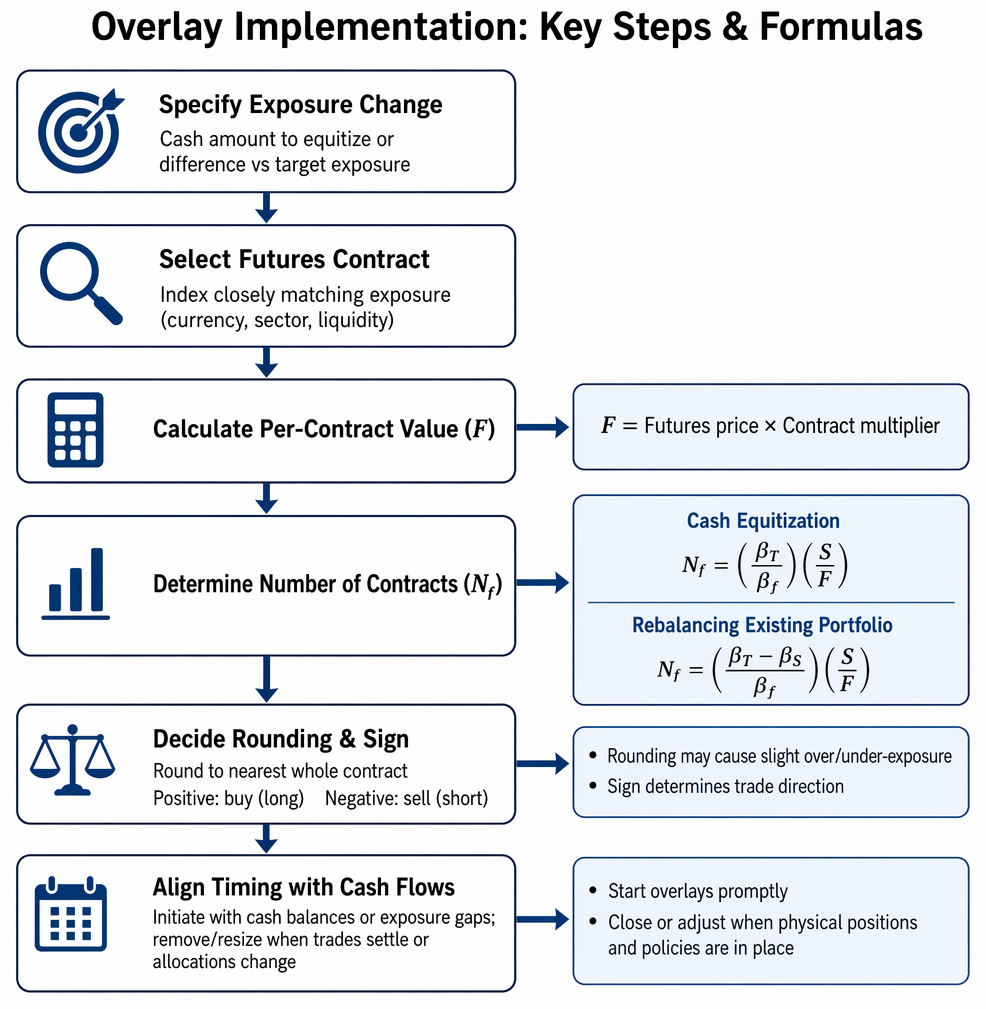

OVERLAY IMPLEMENTATION: KEY STEPS AND FORMULAS

Implementing a cash equitization or futures overlay is conceptually simple but operationally sensitive. At Level 3, you must be able not only to compute the number of contracts but also to reason through implementation details and risks.

Futures overlay contract calculation begins with the cash position and contract notional, then applies either a simple or beta-adjusted sizing formula.

Key Term: notional exposure

The dollar value of economic exposure obtained via derivatives, distinct from the cash invested or posted as margin.

Core implementation steps

For both cash equitization and rebalancing overlays, the main steps are:

-

Specify the desired exposure change.

- For cash equitization: usually the temporary cash amount that should behave like the benchmark.

- For rebalancing: the difference between current and target exposure in a given asset class (e.g., add $50 million to equities, reduce $50 million in bonds).

-

Select the appropriate futures contract.

- Choose an index whose return behavior closely matches the intended exposure (e.g., domestic large-cap index for a domestic large-cap mandate).

- Consider currency, sector composition, and liquidity.

-

Calculate per-contract value .

-

Determine the number of contracts .

- For pure cash equitization:

- For rebalancing an existing equity portfolio:

-

Decide on rounding and sign.

- Round to the nearest whole contract, with awareness of whether the result leads to slight over- or under-exposure.

- Positive : buy (long futures). Negative : sell (short futures).

-

Align overlay timing with cash flows and trades.

- Initiate overlays as soon as cash balances arise or when exposure gaps appear.

- Remove or resize overlays when physical trades settle or when policy allocations change.

Worked Example 1.5

Equitizing cash during a manager transition

A US pension fund terminates a $300 million active US equity manager benchmarked to the S&P 500. The replacement manager cannot be funded for six trading days. The investment policy requires staying close to the S&P 500 benchmark. S&P 500 futures trade at 4,800 with a multiplier of 250, and the futures beta is 1.0. What overlay should the fund implement?

Answer:

The fund will receive $300 million in cash upon liquidation of the old manager. To avoid a six-day underweight in US equities, the fund implements a cash equitization overlay: Contract value:

Number of futures:

= \frac{1.0}{1.0}\frac{300{,}000{,}000}{1{,}200{,}000} = 250$$ The fund **buys 250 S&P 500 futures** for the six-day transition period. When the new manager is funded and physical equities are in place, the futures are closed out. This minimizes tracking error versus the S&P 500 policy benchmark during the transition.

Practical implementation considerations

Beyond the arithmetic, implementation in institutional settings involves:

-

Contract choice and basis risk

- Global or style-diversified portfolios may not match any single index perfectly. You must judge whether a broad index (e.g., MSCI World) is adequate, or whether multiple overlays are needed (e.g., separate US and non-US equity futures).

-

Tenor selection and roll management

- For very temporary exposures (days/weeks), front-month contracts are usually preferred for liquidity.

- For longer overlays, you must plan for contract expiry and the need to roll positions, introducing roll risk and additional transaction costs.

-

Margin and liquidity management

- Futures require initial and variation margin. Cash equitization overlays typically leave most cash invested in short-term instruments, but sufficient liquid collateral must be available to meet margin calls if markets move.

-

Governance and documentation

- Many institutions delegate overlay execution to a specialist overlay manager. The IPS or overlay mandate must specify allowed instruments, leverage limits, tracking error constraints, and policy for rounding and rebalancing overlays.

At Level 3, expect case questions that integrate these implementation details with policy constraints and risk objectives. You may be asked not just “how many contracts?” but also “should the manager equitize the cash, given the client’s liquidity needs and risk tolerance?”

COMMON RISKS AND LIMITATIONS

Overlays quickly align risk exposures, but they introduce unique risks and operational requirements that must be recognized and managed.

Key Term: basis risk

Risk that the futures overlay does not perfectly track the performance of the intended physical exposure, due to differences in composition, currency, or other factors. Key Term: roll risk

The risk of adverse price changes or unexpected costs when rolling expiring futures into new contracts to maintain exposure.

Key risk dimensions include:

-

Basis risk

- If the overlay index is not a perfect match for the actual or intended exposure (e.g., using a domestic index future to equitize a global portfolio), the overlay return will diverge from the benchmark or actual holdings.

- For cash equitization, basis risk is often small when using major index futures that closely track the benchmark, but it can still arise from dividend yield differences, tax effects, or small composition mismatches.

-

Roll risk and term structure effects

- Maintaining an overlay beyond the nearest expiry requires rolling futures positions.

- In contango, longer-dated futures trade at a premium to spot, and rolling a long futures position can generate negative carry. In backwardation, the opposite occurs.

- For short-lived overlays (days to weeks), roll risk is usually negligible; for persistent overlay programs, it becomes important.

-

Liquidity and execution risk

- Although major index futures are highly liquid, large orders can still move markets, especially during stressed conditions or near the close.

- Slippage between decision time and execution can cause unintended exposures or implementation shortfall.

-

Margin and leverage risk

- Futures overlays allow large notional exposures with relatively small margin. This is efficient but can magnify operational errors or lead to forced liquidations if margin calls are not met.

- For institutions that must avoid leverage, overlay usage must be framed carefully at the policy level (often by defining leverage in terms of net, not notional, exposure).

-

Operational and timing risk

- Failure to implement or remove overlays in sync with cash movements leads to over- or under-exposure, causing unwanted tracking error.

- Errors in contract selection (wrong expiry, wrong index, wrong side) can have immediate and material performance impact.

Exam Warning: Futures overlay effectiveness depends on liquidity, contract selection, and precise timing relative to cash and trade flows. In exam cases, carefully line up:

- when cash arrives or is paid out

- when physical trades occur and settle

- when overlays are initiated, resized, or closed

Any mismatch is a likely source of tracking error and a common point of examiner focus.

Revision Tip: In CFA exam scenarios, always check for signs of “temporary cash,” “pending asset reallocation,” or “transition between managers.” Ask yourself:

- Is there a period when the benchmark is fully invested but the portfolio is not?

- Would a futures overlay (cash equitization or rebalancing overlay) maintain benchmark-like exposure more efficiently than rushing physical trades?

Explicitly recommending an overlay, and showing how you would size it, is often required for full credit.

Summary

Cash equitization and futures overlays are key tools for institutional rebalancing and managing temporary deviations from allocation targets. By using futures on top of existing portfolios, managers can:

- maintain equity or bond exposure when cash balances are temporarily high

- adjust beta or asset-class weights quickly and cost-effectively

- minimize tracking error during rebalancing, manager transitions, or staged implementations

At the same time, overlays introduce basis risk, roll risk, margin and liquidity considerations, and operational complexity. Effective use of overlays at Level 3 requires:

- understanding the economic objective (what exposure is being added or removed)

- correctly applying notional and beta-based contract sizing formulas

- aligning overlay timing with cash and trades

- evaluating whether the overlay is consistent with the client’s risk tolerance, liquidity needs, and policy constraints

In the exam, demonstrating this synthesis—linking calculations to policy objectives and implementation realities—is what distinguishes a strong answer from a purely mechanical one.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain cash equitization and futures overlays and their purpose in maintaining benchmark-consistent exposure

- Calculate required futures contracts for cash equitization using both simple notional and beta-adjusted formulas

- Apply overlays to manage tracking error in rebalancing, manager transition, and tactical allocation situations

- Interpret case facts (timing, liquidity, policy benchmark) to determine when an overlay is appropriate or inappropriate

- Identify operational and risk considerations: implementation timing, basis risk, roll risk, margin and liquidity management

- Recognize overlay applications in exam scenarios involving temporary cash, staged rebalancing, or manager transitions

Key Terms and Concepts

- cash equitization

- overlay (futures overlay)

- tracking error

- rebalancing overlay

- notional exposure

- basis risk

- roll risk