Learning Outcomes

This article explains the role of transaction cost models and corridor-based techniques in designing efficient rebalancing policies for multi-asset portfolios. It clarifies how to describe and compare alternative rebalancing rules, articulate the economic intuition behind cost-versus-risk trade-offs, and identify the model inputs that most strongly influence optimal rebalancing triggers. The discussion covers how explicit and implicit trading costs, asset volatility, correlations, liquidity, tax considerations, and review frequency interact when setting tolerance bands, as well as how these parameters shape the width and symmetry of corridors across different asset classes. The article also explains how to interpret model outputs such as optimal no-trade ranges, tracking-error budgets, and rebalancing thresholds, and how to connect these quantitatively to portfolio objectives and constraints that are typical in the CFA Level III curriculum. Finally, it examines when overlays and derivatives provide a superior implementation route versus physical rebalancing, enabling precise evaluation of their advantages, limitations, risks, and suitability, and supporting well-reasoned recommendations on rebalancing policy in qualitative discussion and calculation-based exam questions.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the practical and theoretical frameworks that underpin portfolio rebalancing and overlays, with a focus on the following syllabus points:

- The construction and key assumptions of transaction cost models applied to rebalancing

- The use of corridors (or tolerance bands) to minimize costs in systematic rebalancing

- Factors influencing corridor width selection and optimal rebalancing points

- The application of overlays—especially derivatives overlay management—when adjusting exposures cost-effectively

- Differences between calendar-based and tolerance band (corridor) rebalancing strategies

- The effect of illiquidity and tax constraints on rebalancing policy

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the primary trade-off that a transaction cost model attempts to balance in portfolio rebalancing decisions?

- Describe the main inputs into a corridor (tolerance band) rebalancing strategy.

- Explain how overlays can mitigate transaction costs and manage exposures in rebalancing.

- Why might an investor opt for a wider corridor in a portfolio that includes illiquid assets?

Introduction

A critical element of portfolio management is determining when and how to rebalance the portfolio to its target asset allocation. Since asset values fluctuate and capital flows occur, weights will drift from strategic targets. Rebalancing restores these weights, but each trade carries costs. Transaction cost models and corridor (tolerance band) rebalancing help managers identify cost-effective strategies, especially for complex, multi-asset portfolios. Overlays (such as derivatives) provide flexible tools for implementing rebalancing efficiently.

Key Term: rebalancing

The process of restoring a portfolio’s asset or factor weights to their strategic targets by trading portfolio holdings.

TRANSACTION COST MODELS IN REBALANCING

Transaction cost models quantify the expected costs and potential benefits of rebalancing activity. These costs include explicit costs (e.g., commissions, bid-ask spreads, taxes) and implicit costs (such as market impact and delay). Models balance these against the benefit obtained by reducing tracking error risk when the portfolio drifts from its target.

Key Term: transaction cost model

A framework for estimating and minimizing the total expected costs (explicit and implicit) incurred when executing rebalancing trades.

Transaction cost models typically include:

- Estimates of trading costs for each asset or asset class (can include liquidity, volatility assumptions)

- Measures of expected tracking error as weights deviate from target

- Constraints such as minimum trade sizes or blackout periods (for tax reasons or liquidity events)

- Sometimes tax effects and other implementation friction are modeled explicitly

The model identifies the threshold deviation (from target) where the marginal expected benefit of trading equals the marginal cost. This is the optimal rebalancing trigger.

Worked Example 1.1

Question: A manager observes that large trades in an emerging market equity position incur a 50 bps bid-ask spread, while deviation from target increases tracking error with an expected cost of 30 bps per annum. When should the manager rebalance the position?

Answer:

The cost of trading (50 bps) is greater than the estimated risk penalty (30 bps), so the manager should delay rebalancing until the tracking error cost accumulates to equal or exceed the transaction cost. Alternatively, the model can identify the asset weight deviation for which expected cumulative tracking error equals expected trading cost; this deviation determines the "no-trade" zone.

THE CORRIDOR (TOLERANCE BAND) REBALANCING APPROACH

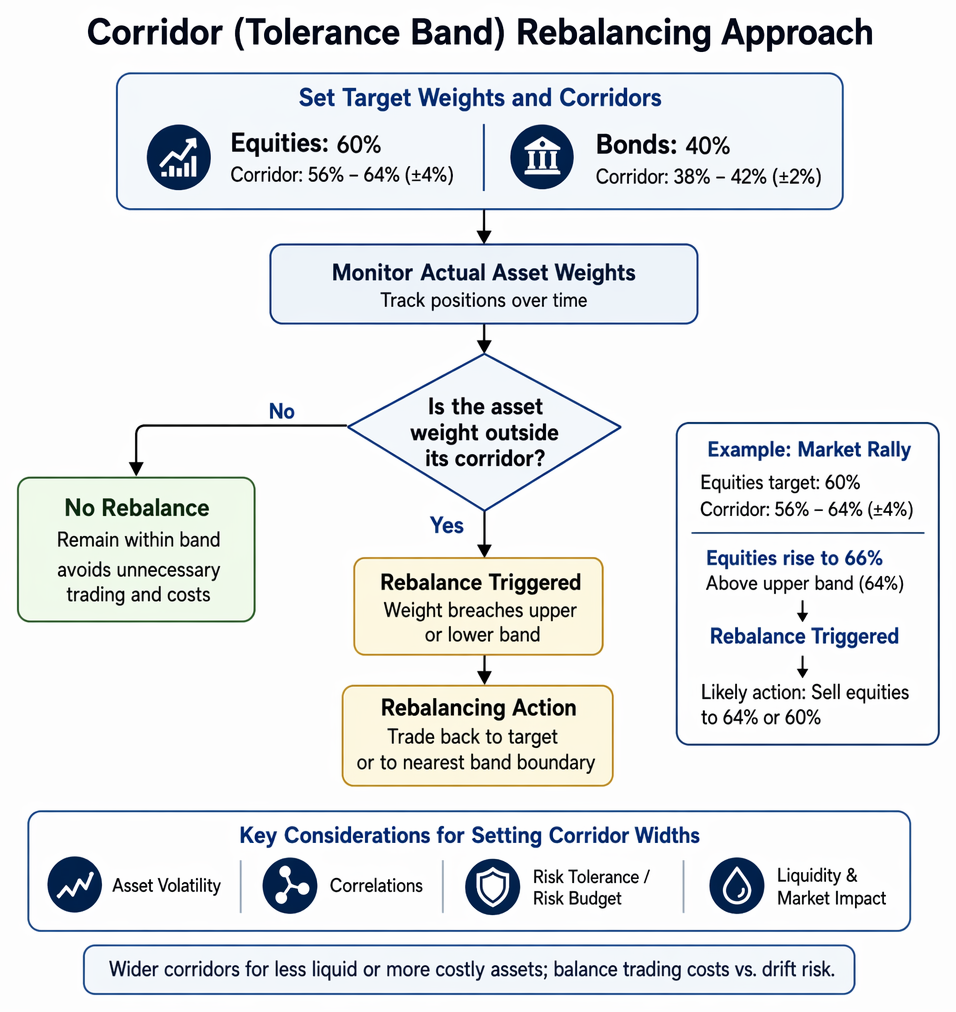

Corridor rebalancing uses specified asset weight deviation bands (corridors) around each target allocation. The manager only rebalances an asset when its weight moves outside its band—reducing unnecessary trading and associated costs. Transaction cost models can be used to optimize corridor widths, taking account of:

Corridor-based portfolio rebalancing sets target allocations and tolerance bands, monitors weight drift, and executes trades only after band breaches.

- Asset volatility

- Correlations with other assets

- Investor risk tolerance (or risk budget)

- Expected trading liquidity and market impact

When an asset's weight breaches the upper or lower band, rebalancing is triggered—typically either back to the target or to the nearest band boundary.

Key Term: corridor rebalancing

A systematic rebalancing method where trades occur only when asset weights exceed pre-determined deviation bands around the target allocation.

Different assets may have different corridor widths depending on their trading costs, volatility, or liquidity. Liquidity and transaction cost considerations often lead to wider bands on less liquid (or less expensive to trade) assets.

Worked Example 1.2

Question: A 60/40 equity/bond portfolio establishes a corridor of ±4% for equities and ±2% for bonds. During a market rally, equities appreciate to 66% of portfolio value. Should the manager rebalance, and if so, what is the likely rebalancing action?

Answer:

The equity corridor is 56%—64% (60% ± 4%). At 66%, equities exceed the corridor, so a rebalance is triggered. The manager can trade equities down—either to the 60% target or to the upper corridor boundary (64%), depending on the rebalancing protocol and cost minimization model.Exam Warning: Do not assume tight corridors are always optimal. Overly narrow bands may incur excessive trading costs, while overly loose corridors can lead to excessive drift from target, raising tracking error and risk. Corridors should reflect portfolio characteristics and implementation costs.

Revision Tip: When asset classes have asymmetric trading frictions, set corridor widths accordingly—wider corridors for less liquid or more costly asset classes.

FACTORS INFLUENCING CORRIDOR WIDTH

Corridor widths are set with reference to several parameters, including:

- Asset volatility: More volatile assets need narrower corridors to prevent large portfolio drift

- Trading costs: Assets with higher costs should have wider corridors

- Correlation with other assets: Less correlated assets may tolerate wider corridors

- Investor risk tolerance: Lower risk tolerance warrants narrower corridors to control total risk

- Frequency of portfolio review: More frequent reviews permit narrower corridors; less frequent reviews demand wider corridors

Corridor rebalancing also reduces the number of small, potentially immaterial trades, concentrating activity only when there is a significant deviation warranting the cost.

OVERLAYS AND DERIVATIVES IN REBALANCING

Using overlays, especially derivatives, enables the manager to change portfolio exposures rapidly and with lower friction than transacting in the physical assets. Overlays are particularly useful for:

- Managing asset class exposures without disturbing existing managers or long-term positions

- Implementing tactical asset allocation shifts

- Efficiently rebalancing illiquid or expensive-to-trade exposures

Key Term: overlay

A portfolio management tool (often implemented with derivatives) designed to adjust exposures, such as asset allocation or risk factors, without trading physical positions.

An overlay may be implemented using futures, swaps, or options. Overlay strategies can help achieve desired exposures during rebalancing with reduced market impact, often maintaining the economic benefits of rebalancing while deferring physical trading until more advantageous conditions arise.

Worked Example 1.3

Question: A fund manager must rebalance from domestic to international equity after strong home market performance, but global equity markets are closed. What overlay might the manager use?

Answer:

The manager can use equity index futures to sell exposure to the domestic market and buy international index futures for immediate synthetic exposure, then execute the actual cash trades over time as market liquidity improves.

ADVANTAGES AND LIMITATIONS OF CORRIDOR AND OVERLAY REBALANCING

Corridor-based rebalancing minimizes unnecessary trading and thus reduces costs, particularly for large or illiquid portfolios. It is mechanistic, avoids behavioural biases, and ensures systematic risk control. However, trading is only triggered at the extremes—which may delay action during volatile markets.

Overlay approaches offer flexibility, rapid execution, and the ability to manage exposures without untimely forced sales of illiquid assets. However, they introduce derivative counterparty and margin risks, and may not perfectly replicate the cash exposure in the very short term.

Exam Warning (Taxes)

Taxable investors should incorporate potential tax liabilities or loss of tax deferral in their transaction cost models for rebalancing. Neglecting tax impact can make rebalancing uneconomic even where tracking error appears high.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the use of transaction cost models in portfolio rebalancing decisions

- Describe the corridor (tolerance band) rebalancing approach, including optimal band width considerations

- Identify factors affecting corridor width: transaction costs, asset volatility, liquidity, correlations, risk tolerance, review frequency

- Recognize when overlays can be used to manage exposures and rebalance efficiently

- Understand the trade-offs between minimizing tracking error and avoiding unnecessary costs

- Recall that wider corridors are suitable for assets with higher trading costs or lower liquidity

Key Terms and Concepts

- rebalancing

- transaction cost model

- corridor rebalancing

- overlay