Learning Outcomes

This article explains return enhancement and overlay strategies using shorting and collateral, including:

- how short positions are created physically and synthetically, and why overlays rely on negative exposures for both hedging and alpha generation

- the role of collateral and margin in securing overlay positions, and how initial versus variation margin flows affect portfolio liquidity

- practical steps for implementing currency, duration, and factor overlays while keeping core portfolio holdings and benchmark exposures broadly unchanged

- methods for sizing overlay notional exposures relative to portfolio value, risk budgets, and regulatory or mandate constraints

- key operational, legal, and documentation requirements for securities lending, derivatives trading, collateral agreements, and counterparty selection

- principal risk sources in overlay programs—basis risk, leverage, liquidity, collateral concentration, and counterparty risk—and techniques used to monitor and mitigate them

- ongoing processes for margining, exposure monitoring, and rebalancing, including triggers for adjusting or unwinding overlays when markets move sharply

- application of these concepts to typical CFA Level 3 exam scenarios, evaluating proposed overlay trades, identifying implementation pitfalls, and formulating robust risk-control recommendations

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the mechanics and practical application of return enhancement and overlay strategies, with a focus on the following syllabus points:

- Implementation of return enhancement overlays using shorting and collateral

- The operational, legal, and risk controls for collateralised derivative and short overlay positions

- Differences between directional and non-directional overlays (e.g., currency, duration, factor overlays)

- The process for integrating overlays within portfolio constraints (liquidity, margin, regulatory)

- Limitations and best practices in execution, monitoring, and rebalancing for overlay strategies

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the main operational risk unique to implementing synthetic short exposure via derivatives rather than physical short-selling?

- Give an example of how collateral requirements can create liquidity risk in portfolio overlay strategies.

- True or false? A return overlay can use both short futures and cash collateral without increasing the aggregate portfolio risk above the reference benchmark.

- What is the purpose of margining in collateralized overlay transactions?

Introduction

Overlay strategies are widely used to modify a portfolio’s risk or return profile without extensive changes to core holdings. Common for managing currency, duration, factor, and risk exposures, overlays often use derivatives and short positions, supported by posted collateral, to implement tactical or strategic policy decisions. Understanding how collateral and shorting interact is essential for CFA Level 3 candidates, as is knowing risks and regulatory implications.

Key Term: overlay strategy

An investment approach where exposures—such as currency, duration, factor, or market—are adjusted using shorting or derivatives without altering the portfolio's core asset allocation.Test Tip: When revising Implementation shorting and collateral, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

SHORTING IN OVERLAY STRATEGIES

Shorting, or taking a negative exposure to a security or factor, is fundamental to most overlay techniques for return enhancement or risk management. Short exposure can be achieved by borrowing securities and selling them (physical shorting), or synthetically through derivatives (e.g., selling futures or entering into swap contracts).

Key Term: shorting

Combining positions to profit from or hedge against asset price declines, implemented either physically (selling borrowed assets) or synthetically via derivatives. Key Term: collateral

Assets posted to secure obligations in derivative or short positions, ensuring performance and reducing counterparty credit risk. Can consist of cash, liquid securities, or margin deposits.

Shorting in overlays enables investors to:

- Reduce portfolio risk exposures (e.g., hedging equity beta, currency, or interest rate risk)

- Generate return enhancements (e.g., harvesting risk premia by selling futures, arbitrage, or carry trades)

- Maintain or rebalance asset class weights efficiently

Physical shorting demands strict operational controls (securities lending agreements, settlement procedures), while synthetic shorting exposes the portfolio to margin and collateral requirements with counterparties or clearinghouses.

COLLATERAL MANAGEMENT IN OVERLAY IMPLEMENTATION

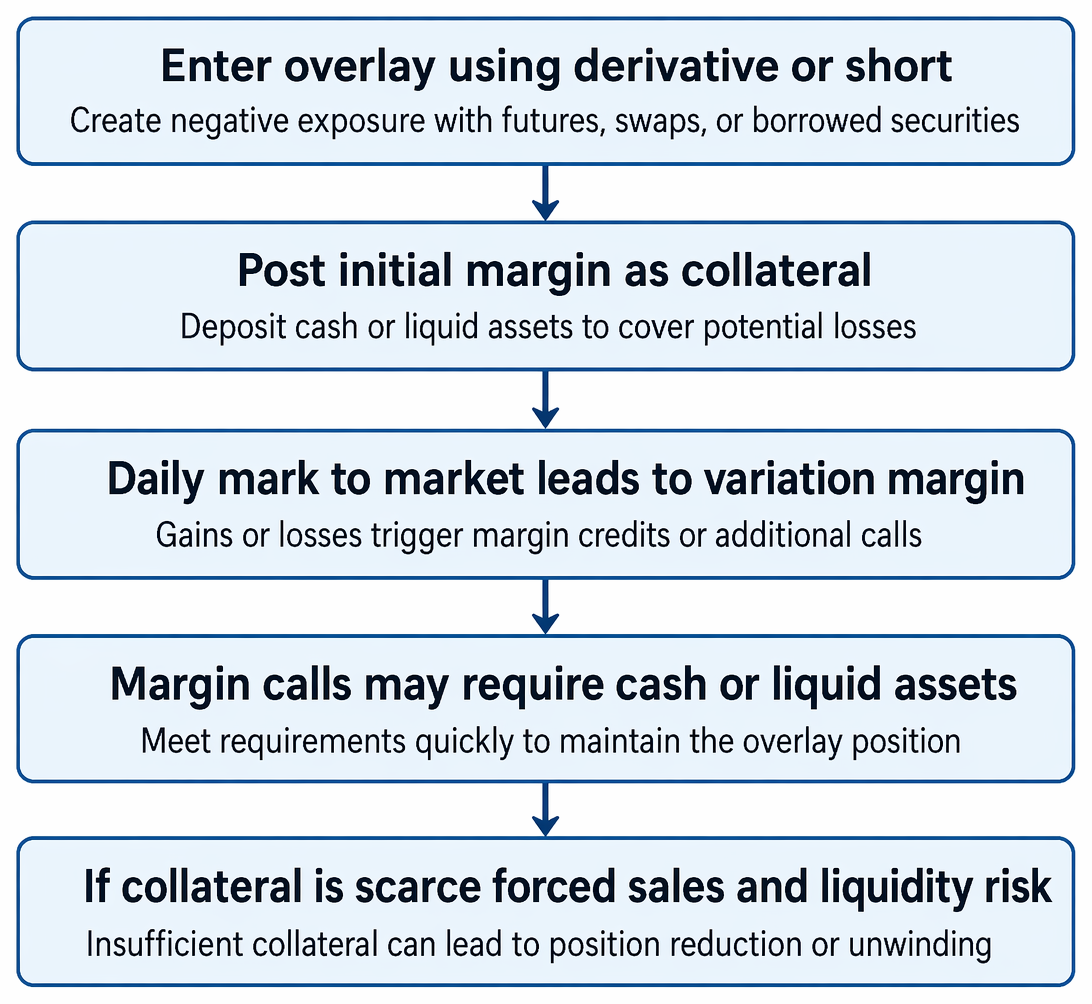

Collateral is required to secure both physical and synthetic short exposure. Margin posted to exchanges or OTC counterparties protects against non-performance, reducing credit risk. Collateral also acts as the primary source for:

Collateralized overlay positions progress from trade initiation and initial margin posting to mark-to-market variation margin and potential forced asset sales.

- Mark-to-market margin variation (reflecting daily P&L on open positions)

- Initial margin (ensuring coverage for potential losses)

- Legal recourse in case of default

Collateral needs are determined by notional exposure, market volatility, instrument liquidity, and regulatory margin models. Held assets must be highly liquid to meet margin calls and maintain overlay exposures, so large overlays can increase portfolio liquidity risk if cash outflows rise unexpectedly.

Key Term: margin

Initial or variation deposit required when entering into derivative or short positions, reflecting collateral needed to cover potential losses as market values change.

Liquidity risk emerges if posted collateral cannot be withdrawn promptly or must be sold at disadvantageous prices, especially during market drawdowns.

OVERLAY STRATEGY DESIGN AND RISK CONTROL

Overlay construction targets a specific exposure (or neutralization) by combining short positions and collateralized contracts:

- Currency overlays: Use short forward/futures positions against cash, requiring margin in each currency

- Duration overlays: Sell fixed income futures or swaps, posting cash or government securities as collateral

- Factor overlays: Take short positions in factors or baskets (e.g., value, momentum) using swaps or ETFs

- Portfolio completion: Add overlays to align portfolio exposures with policy benchmarks

Control systems must monitor:

- Aggregate notional and cash exposures

- Sensitivities (duration, beta, FX rate, factor exposures)

- Collateral sufficiency and concentration

- Legal limits (net short, gross gearing, regulatory margin)

Key Term: overlay margin policy

Rules specifying minimum required collateral to assure overlay performance, defining processes for margin calls, substitutions, and liquidation protocol, bespoke for legal and operational compliance. Key Term: counterparty risk

The risk that the overlay counterparty will fail to honor its obligations, mitigated through CCPs, bilateral collateral agreements, and regular margining.

EXECUTION, MONITORING, AND REBALANCING OVERLAYS

Execution requires:

- Liquidity assessment—ensuring overlay instruments (futures, swaps, options) can be traded in required size at acceptable transaction cost

- Collateral pre-positioning and forecast cash flow analysis

- Real-time margin call response procedures

Ongoing monitoring includes:

- Daily reconciliation of overlay exposures and margin balances

- Early warning for liquidity risk (large margin calls, falls in collateral value)

- Assessment of divergence between target and realized exposures, rebalancing as policy/tactics dictate

If margin requirements spike or collateral assets lose value, overlays may need to be rapidly reduced, increasing tracking error and potential loss.

Worked Example 1.1

A global balanced fund has a $100m equity allocation denominated in euros, but ECB policy changes increase EUR volatility. To manage risk, the CIO implements a currency overlay, shorting €50m through EUR/USD futures. Margin requirement = 10%; cash collateral must be maintained at $5m.

Answer:

By shorting €50m in futures, the fund reduces FX exposure risk by half. The $5m margin reduces available liquid assets but secures derivative performance and assures counterparty protection. If markets move sharply, margin calls may require rapid portfolio adjustment or liquidation of other holdings.

Worked Example 1.2

A pension scheme targeting passive beta exposure wants to outperform benchmark returns via a tactical overlay. It sells equity index futures (notionally $20m short) while posting $2m government bonds as collateral and reallocating cash to higher-yield credit.

Answer:

The short futures and collateral posting allow reallocation to higher-return assets, potentially increasing overall returns. The overlay must be monitored to ensure margin is maintained and policy constraints (on gearing or liquidity) are not breached.Exam Warning: Overlay implementation errors are often exam tested. A common mistake is to ignore the indirect portfolio risk created by margin calls. Always assess the impact of collateralized overlays on overall liquidity and risk budget—stress-test portfolio liquidity against plausible scenarios.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain shorting and collateral use within overlays as tools for return enhancement and risk management

- Identify main operational, legal, margin, and liquidity risks when executing overlays

- Describe monitoring and rebalancing controls for effective implementation

- Recognize regulatory constraints and documentation required for shorting/collateral overlays

Key Terms and Concepts

- overlay strategy

- shorting

- collateral

- margin

- overlay margin policy

- counterparty risk