Learning Outcomes

This article explains how portable alpha and overlay strategies are designed and implemented within institutional and multi-asset portfolios. It clarifies the distinction between alpha and beta, showing how alpha can be isolated, financed, and transported independently of market exposure using derivatives and market-neutral structures. The article explains the mechanics of beta overlays, cash equitisation, and completion trades, highlighting how managers use futures, swaps, and ETFs to close benchmark gaps, maintain policy weights, and manage residual allocations efficiently. It examines the role of overlay strategies in multi‑manager arrangements, including policy implementation, tactical tilts, and risk factor targeting across equity, fixed income, and currency exposures. The article also analyzes key implementation risks—such as basis, counterparty, liquidity, and operational risk—and emphasizes how leverage and notional exposure must be monitored against risk limits. Finally, it provides an integrated framework for evaluating when portable alpha, beta completion, and other overlay structures improve tracking, risk control, and return enhancement in the CFA Level 3 portfolio management context.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the use of return enhancement and overlay strategies in portfolio management, including key revision points for overlays, their role in alpha transfer, and completion strategies, with a focus on the following syllabus points:

- Distinguishing between alpha and beta sources of return

- Explaining portable alpha strategy mechanics and objectives

- Constructing overlays for portfolio completion (beta overlays, synthetic exposures)

- Evaluating completion trades and overlay implementation efficiencies

- Understanding the risks and operational considerations of overlays

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the primary purpose of portable alpha, and how can it be implemented in a multi-asset portfolio?

- Which risk must be managed carefully when using derivatives overlays for beta completion?

- In what situation would a portfolio manager use a completion overlay?

- Explain how overlay structures can help maintain exposures when portfolio liquidity or constraints prevent direct holdings.

Introduction

Return enhancement strategies aim to maximise performance without breaching risk or asset allocation guidelines. Portable alpha and overlay strategies allow investment managers to separate and transport alpha across portfolios, while using overlays and beta completion to fill asset class or risk factor gaps efficiently. Understanding these concepts is critical for multi-asset and total portfolio management at Level 3.

Key Term: overlay strategy

The use of derivatives or systematic exposures to adjust, complete, or substitute for physical holdings in a portfolio, commonly for return, risk, or asset allocation purposes. Key Term: portable alpha

A strategy that seeks to isolate alpha from beta, allowing the manager to retain or "port" alpha from a skill-based source while maintaining desired factor or market exposures. Key Term: beta completion

The process of supplementing a portfolio with exposures (commonly through derivatives or ETFs) to achieve a target benchmark or asset class weighting.Test Tip: When revising Portable alpha beta overlays and completion, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Portable Alpha: Structure and Purpose

Portable alpha aims to extract manager skill (alpha) from one market or strategy and transfer it—typically without its original beta—to a chosen beta exposure elsewhere. This approach allows for independent management of systematic and active sources of risk and return.

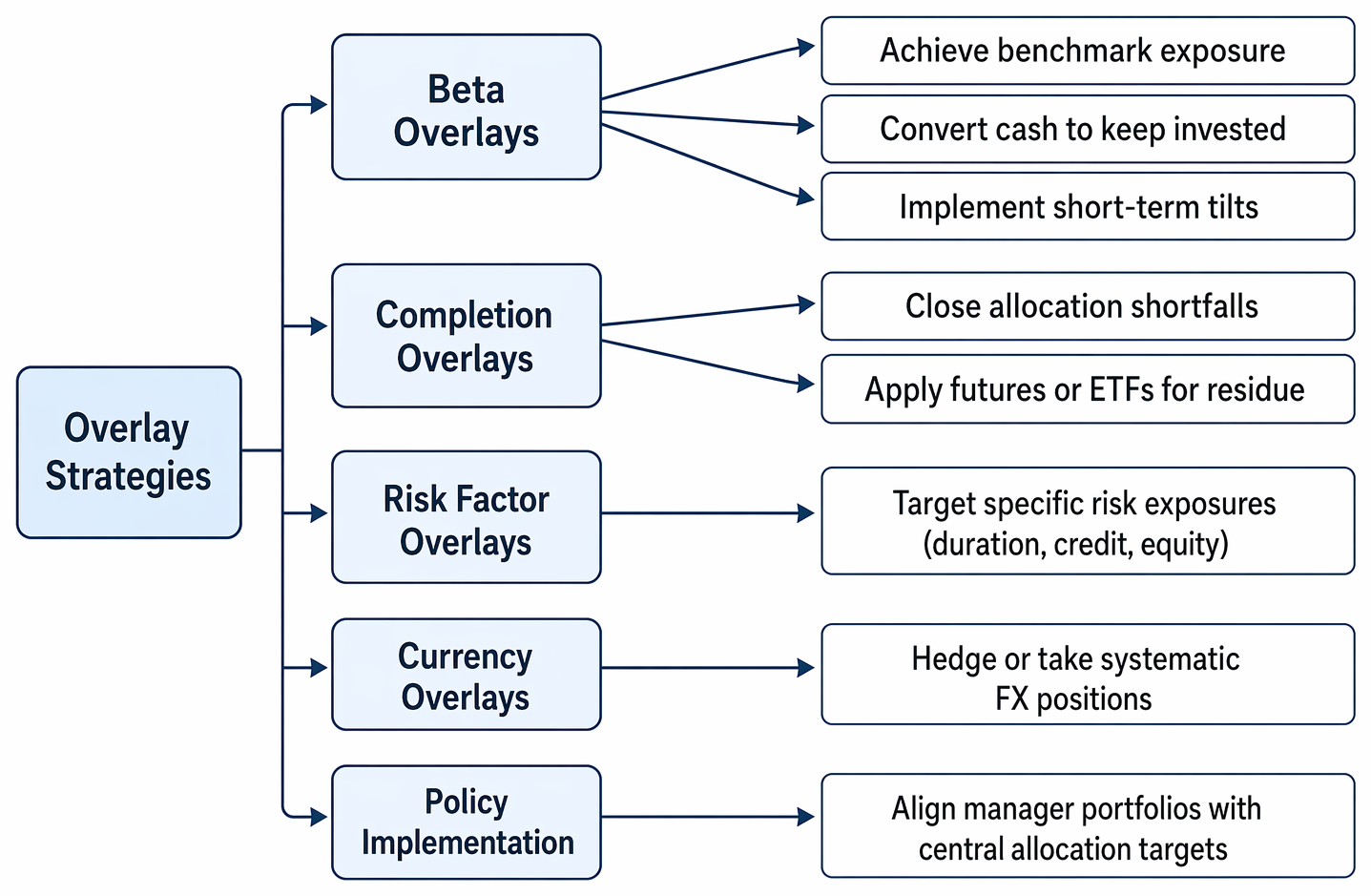

Overlay categories include beta overlays, completion trades, factor and currency exposure management, and multi-manager policy implementation.

The strategy is often used by:

- Multi-manager funds wishing to secure alpha from skilled managers where direct investment is impractical

- Institutional investors aiming for diversification and risk control

- Investors constrained by asset allocation or liquidity needs

With portable alpha, alpha is generated (for example, by a long/short manager or a hedge fund) while the portfolio's required beta (such as equity market exposure) is provided separately, usually via derivatives.

Key Term: alpha transfer

The process of separating and delivering excess return (alpha), often by neutralising market exposure and pairing it with a required beta elsewhere.

Worked Example 1.1

Question: A US pension fund wants S&P 500 index exposure but believes a global macro fund can provide additional alpha. How can the fund construct a portable alpha portfolio?

Answer:

The fund invests most assets in S&P 500 futures (for beta exposure) and allocates a proportion of capital to the global macro manager (who runs a market-neutral, absolute-return strategy). The macro fund's trades are designed to target alpha, not S&P 500 returns. The S&P 500 exposure is achieved synthetically, so all portfolio beta is S&P 500, while the macro manager's alpha is "ported" onto the equity beta portfolio.

Overlay and Completion Trades

Overlay strategies use derivatives (for example, index futures, swaps, or forwards) to efficiently adjust, add, or substitute exposures in a portfolio. Beta overlays are often used to reach a target index weighting, manage tactical exposures, or equitize cash.

Beta completion refers to using overlays or cost-effective products to fill exposure gaps remaining after active or passive mandates are funded. For instance, if residual assets are left after primary allocations, the manager can use futures or ETFs to provide efficient market exposure to complete the target allocation.

Key Term: completion overlay

A targeted trade using derivatives or pooled vehicles to achieve benchmark or risk factor weights not covered by core or satellite mandates.

Worked Example 1.2

Question: A portfolio is 90% invested in active global equity mandates, leaving a 10% residual cash allocation. What overlay trade can the manager use to complete benchmark exposure?

Answer:

The manager can purchase index futures or an ETF representing the benchmark for the remaining 10%. This completion overlay provides the required beta exposure, minimising tracking error and ensuring overall portfolio weights match the target.

Key Implementation Risks

Overlay portfolios and completion trades create efficiency but bring specific risks:

- Basis risk between overlay returns and physical holdings

- Counterparty risk with OTC derivatives

- Operational risk if exposures are not monitored or adjusted for liquidity, cash flows, or asset allocation drift

Overlay usage can also introduce gearing, liquidity mismatches, and unintended exposures if not managed carefully.

Exam Warning: Overlay trades may expose a portfolio to large notional risk with small margin requirements. Failing to monitor exposures, especially after market moves, can result in gearing exceeding risk limits and unexpected portfolio outcomes.

Overlay Completion in Practice

In multi-manager portfolios or where asset allocation is determined centrally, overlays are used to fill the gap between manager holdings and policy weights, or to adjust exposures rapidly in response to tactical views or changes in mandates.

Typical uses:

- Cash equitisation (using futures or swaps to maintain equity exposure when managers are not fully invested)

- Rebalancing or tactical shifts (temporarily adjusting exposure until physical trades can be made)

- Risk factor overlays (for example, targeting duration, credit, equity, or currency exposures to match or hedge portfolio benchmarks)

- Currency overlays to neutralise or express systematic FX exposure efficiently

Overlays allow for efficient, low-cost portfolio adjustments while minimising disruption, particularly important for large or complex mandates.

Worked Example 1.3

Question: A global balanced fund underweights emerging market equities by 4% relative to policy benchmark. Transactions in physical stocks would be illiquid and expensive. What is an alternative?

Answer:

The manager can use MSCI EM index futures or swaps to achieve the required 4% exposure, completing the allocation efficiently while managing liquidity and trading costs.

Summary

Portable alpha and overlay strategies give portfolio managers flexible tools to control beta and alpha delivery separately, enabling efficient completion of asset or risk factor exposures. Proper implementation of overlays allows for cash equitisation, filling benchmark gaps, tactical reallocations, and efficient scaling within policy or risk constraints. Associated risks include gearing, basis, and operational exposures, which must be rigorously managed.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the rationale, advantages, and construction of portable alpha strategies

- Define overlay and completion trades using derivatives and pooled vehicles

- Outline how completion overlays supplement standard mandates to meet policy weights

- List practical risks and operational considerations when implementing overlays

- Identify situations where portable alpha and overlays improve efficiency in multi-asset or multi-manager portfolios

Key Terms and Concepts

- overlay strategy

- portable alpha

- beta completion

- alpha transfer

- completion overlay