Learning Outcomes

This article explains tail-risk hedging and crisis alpha strategies as derivative-based overlays used to reshape institutional and multi-asset portfolio return distributions, including:

- Defining overlay strategies and distinguishing them from changes to the strategic asset allocation in an institutional portfolio context.

- Describing the mechanics, payoff profiles, and intended crisis protection of tail-risk hedges using OTM put options and volatility instruments.

- Outlining how crisis alpha overlays such as volatility, trend-following, and option-based programs can generate positive returns in stressed markets.

- Comparing the cost, convexity, and path-dependency of different overlay structures, and evaluating trade-offs between protection strength and ongoing performance drag.

- Assessing implementation considerations such as sizing, funding, roll management, liquidity, and governance requirements for long-term institutional investors.

- Identifying key risks and pitfalls, including timing errors, model and behavioral risks, and scenarios in which overlays may fail to deliver protection.

- Linking these concepts to CFA Level 3 exam expectations by emphasizing qualitative judgment, scenario analysis, and communication of overlay rationales to stakeholders.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the application of risk overlays and return-seeking overlays for institutional and multi-asset portfolios, with a focus on the following syllabus points:

- The rationale for and mechanics of tail-risk hedging strategies as an overlay on diversified portfolios

- The main types of overlay strategies for achieving crisis alpha, including volatility, put-option, and trend-following approaches

- Practical considerations for integrating overlays, including cost, timing, convexity, and scenario effectiveness

- Assessing the benefits, limitations, and risks of overlay approaches, and understanding implementation pitfalls for institutional portfolios

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is meant by "crisis alpha" in the context of portfolio overlays?

- Which type of derivative is most commonly used as an overlay to hedge against sudden market drawdowns?

- Briefly outline the potential drawbacks of continuous tail-risk overlays on long-term portfolio performance.

- What practical risks should an institution consider before relying solely on option-based overlays?

Introduction

Return enhancement and risk overlay strategies seek to improve the distribution of returns in institutional and multi-asset portfolios, especially during extreme market environments. These overlays do not require altering the existing asset allocation; instead, they add additional risk or return characteristics by implementing derivatives or dynamic hedging strategies “on top” of the core portfolio. Common aims are to manage the downside from tail events ("tail-risk hedging") and to generate positive returns during stressed markets ("crisis alpha"). Understanding how these overlays work is key for the CFA exam and for portfolio managers facing risk/reward trade-offs.

Key Term: overlay strategy

A derivative-based or rules-driven approach used to adjust portfolio risks or returns without modifying the physical portfolio holdings. Key Term: tail-risk hedging

Adding portfolio overlays (often options or volatility derivatives) designed to provide large positive returns during severe market declines. Key Term: crisis alpha

Return generated by strategies that profit from sudden, turbulent, or trending market conditions, typically during risk-off episodes.

TAIL-RISK HEDGING OVERLAYS

Tail-risk hedges are overlay solutions designed to cushion portfolios during rare but severe downturns. Typically, these overlays use out-of-the-money (OTM) put options, option spreads, or volatility contracts that gain value rapidly as equities or other risk assets fall sharply. The aim is not to protect against modest drawdowns but to provide meaningful compensation only if markets experience large, abrupt declines.

Key Term: OTM (out-of-the-money) put option

A put option with a strike price below the current market price, providing leveraged protection against large downside moves.

Tail-risk overlays are attractive because they offer convex protection—costing little in ordinary markets, but providing asymmetric payoff if the tail scenario is realized. However, the ongoing cost from option premiums or negative carry erodes long-term returns if tail events do not occur, making calibration, timing, and selection critical.

Worked Example 1.1

A portfolio manager buys 3-month 10% OTM S&P 500 put options as a tail hedge for a $100 million global fund, rolling the hedge every quarter. In a typical flat or rising market, the overlay cost is roughly 1.2% of AUM annually, with zero payoff. In a sudden 30% equity drawdown, the put gains approximately $7 million, partially offsetting portfolio losses.

Answer:

The put overlay delivers strong crisis protection but imposes a significant expected drag during “normal” periods, highlighting the cost/benefit dilemma.Exam Warning: For the exam, do not confuse basic put protection ("protective puts") with dedicated tail overlays. The latter are specifically designed to only hedge catastrophic events, not mild to moderate declines.

CRISIS ALPHA STRATEGIES

Crisis alpha refers to strategies that are expected to reliably deliver positive returns during deep market crises. These overlays are added alongside the main asset allocation; common examples include:

- Volatility overlays (e.g. long VIX futures or options)

- Put-spread collars and option-based programmatic hedges

- Systematic trend-following overlays (managed futures/CTAs)

- Dynamic “crisis regime” strategies that allocate to short equities, long bonds, or long volatility when certain triggers are breached

The rationale is that while standard diversification often fails in a system-wide crisis, overlays that adjust or react to volatility spikes or momentum changes can capture positive returns when traditional assets are falling.

Key Term: volatility overlay

An overlay using derivatives (such as VIX futures/options) to add long volatility exposure, which typically rises during market turmoil.

Worked Example 1.2

An institutional investor overlays a 10% allocation to a volatility index (VIX) ETF and enters dynamic short S&P 500 futures when a drawdown threshold is breached. During a sharp sell-off, both overlays contribute positive returns. In calm markets, the overlays experience negative carry and tracking error.

Answer:

The combination of volatility and dynamic crisis overlays can provide robust drawdown protection but is rarely costless; careful sizing and monitoring are required.

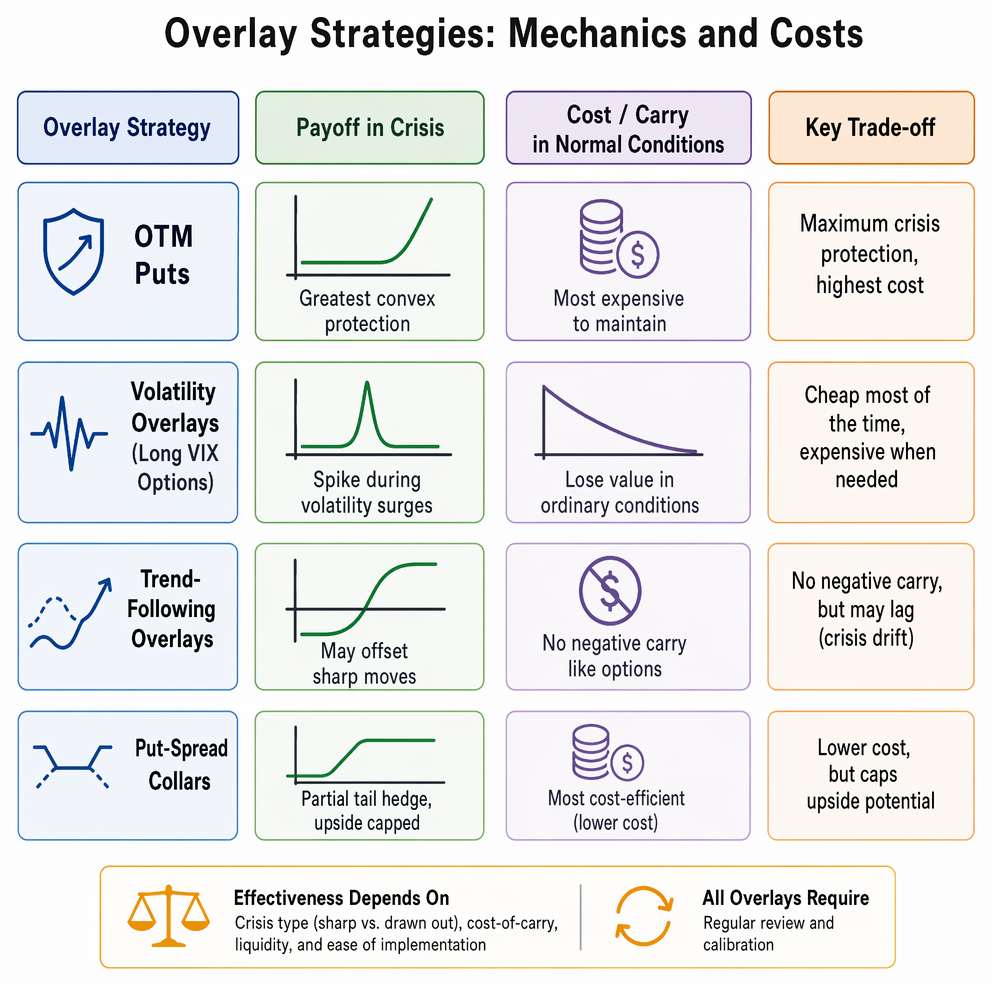

COMPARING OVERLAY MECHANICS AND COSTS

Overlay strategies vary dramatically in cost, payoff structure, and implementation complexity:

OTM put overlay on risky assets produces negative carry in normal conditions and convex protection when markets decline sharply.

- OTM puts deliver the greatest convex protection during crises but are the most expensive to maintain.

- Volatility overlays (e.g., long VIX options) lose value in ordinary conditions but spike during volatility surges.

- Trend-following overlays may offset sharp moves and do not suffer the same negative carry as options, but they may lag the onset of a rapid drawdown ("crisis drift").

- Put-spread collars are cost-efficient but only partially hedge tail risks and often cap upside.

The effectiveness of overlays depends on the crisis type (sharp vs. drawn out), cost-of-carry, liquidity, and ease of implementation. All overlay strategies require regular review and calibration.

Worked Example 1.3

A pension fund uses an option-collar overlay: long put, short call, both OTM, to limit downside risk at lower cost than puts alone. The call premium partially finances the put. In a non-crisis, the collar generates a small drag but limits large losses in a tail-event. If the market rallies strongly, upside is foregone.

Answer:

Option collars can reduce hedge cost, but they also limit potential gains—suitable only when capping upside is acceptable.Revision Tip: Overlay benefits are highly path-dependent. For the CFA exam, be able to explain overlay risk/cost trade-offs, not just the theoretical crisis payoffs.

IMPLEMENTATION RISKS AND PITFALLS

Overlay strategies may fail to protect as intended due to:

- Timing errors: crisis onset is unpredictable.

- Funding cost/negative carry: persistent drag can meaningfully reduce portfolio returns.

- Liquidity risk: options or volatility contracts may dry up in stressed conditions.

- Model risk: systematic overlays may lag sudden sharp crises or may "false trigger" in whipsaw markets.

- Behavioral risk: stakeholders may discontinue overlays after a period of poor performance, before the next tail-event.

Exam Warning (Implementation)

Simply purchasing long puts is not a free lunch—understand the drag on returns and the need for proper sizing, rebalancing, and board buy-in for institutional adoption.

Summary

Tail-risk and crisis alpha overlays are derivative or rules-based strategies added on top of an existing asset allocation to manage severe downside risk and provide return potential during crises. This includes OTM put overlays, volatility overlays, and trend-following systems. All overlays carry trade-offs: overlays protect in rare tail events but typically impose cost in calm periods. For the CFA exam, focus on assessing when, how, and why an overlay is justifiable—and how to implement, monitor, and communicate the strategy given institution- or portfolio-specific constraints.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish overlay strategies from direct asset allocation changes

- Recognize tail-risk hedging overlays and their main derivative structures

- Explain what crisis alpha overlays aim to accomplish in a multi-asset context

- Compare implementation, cost, and risk of option, volatility, and trend overlays

- Identify institutional and CFA exam-relevant trade-offs for each overlay approach

- Apply overlay principles to typical exam scenarios for institutional and multi-asset investors

Key Terms and Concepts

- overlay strategy

- tail-risk hedging

- crisis alpha

- OTM (out-of-the-money) put option

- volatility overlay