Learning Outcomes

This article explains how risk budgeting fits into portfolio construction for CFA Level 3 candidates, emphasizing the distinction between allocating capital and allocating risk. It describes techniques for setting absolute, relative, and factor-based risk budgets and interpreting marginal and total risk contributions for asset classes, factors, and managers. It examines how practical, regulatory, and client constraints interact with mean-variance optimization, leading to concentrated or unstable portfolios, and how robust optimization methods explicitly incorporate estimation error, scenario ranges, and feasibility limits to generate more resilient allocations. It presents the logic, steps, and advantages of the Black-Litterman model, including reverse-optimizing market-implied returns, integrating investor views with confidence levels, and producing diversified weights suitable for constrained mandates. It discusses risk-factor-based strategic allocation and asset-class mapping, highlighting how factor budgets can reduce hidden exposures and improve stress-test performance. It also analyzes the role of scenario analysis and ongoing monitoring in assessing portfolio robustness, enabling precise explanation, comparison, and evaluation of alternative allocation frameworks in line with CFA Level 3 learning outcome statements.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand advanced asset allocation methodologies and their practical application, with a focus on the following syllabus points:

- Describing and applying risk budgeting in portfolio construction

- Explaining the effect of constraints (including regulatory and practical) on optimization and portfolio robustness

- Comparing traditional mean-variance optimization with robust, resampled, and risk-factor approaches

- Outlining the Black-Litterman model’s process and advantages versus standard mean-variance

- Analyzing risk factor-based allocation and asset class mapping

- Evaluating portfolio outcomes and optimization results under different scenarios

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the primary purpose of risk budgeting in a portfolio context?

- Explain how portfolio constraints can affect the efficiency of mean-variance optimization.

- Briefly describe the Black-Litterman model and how it differs from standard mean-variance optimization.

- What is the advantage of using a robust or risk-factor-based approach for strategic asset allocation?

Introduction

Many investment policy statements require not just optimizing for high risk-adjusted return, but also ensuring realistic portfolio outcomes under uncertainty and constraints. Risk budgeting, robust optimization methods, and models like Black-Litterman are essential techniques for CFA candidates, as exam standards now test your ability to apply and compare these to more basic frameworks under practical and regulatory constraints.

Key Term: risk budgeting

The process of allocating a portfolio's total risk across asset classes, factors, or managers to meet defined objectives while controlling exposures. Key Term: robust optimization

A methodology that explicitly accounts for estimation error, uncertainty, and real-world constraints in portfolio optimization, aiming to produce allocations that remain effective across a wide range of possible outcomes. Key Term: Black-Litterman model

An asset allocation model that combines equilibrium (market-cap) implied returns with investor views to generate more stable, diversified expected returns for portfolio optimization.

Portfolio Risk Budgeting: Concept and Application

Portfolio risk budgeting means deciding how much total risk to accept, then deliberately allocating that risk among investments, factors, or strategies. The risk can be measured by volatility, active risk, value-at-risk (VaR), or another method depending on mandate.

Risk budgeting helps avoid unintended concentrations by linking each allocation, position, or manager to its marginal contribution to overall portfolio risk, not just capital.

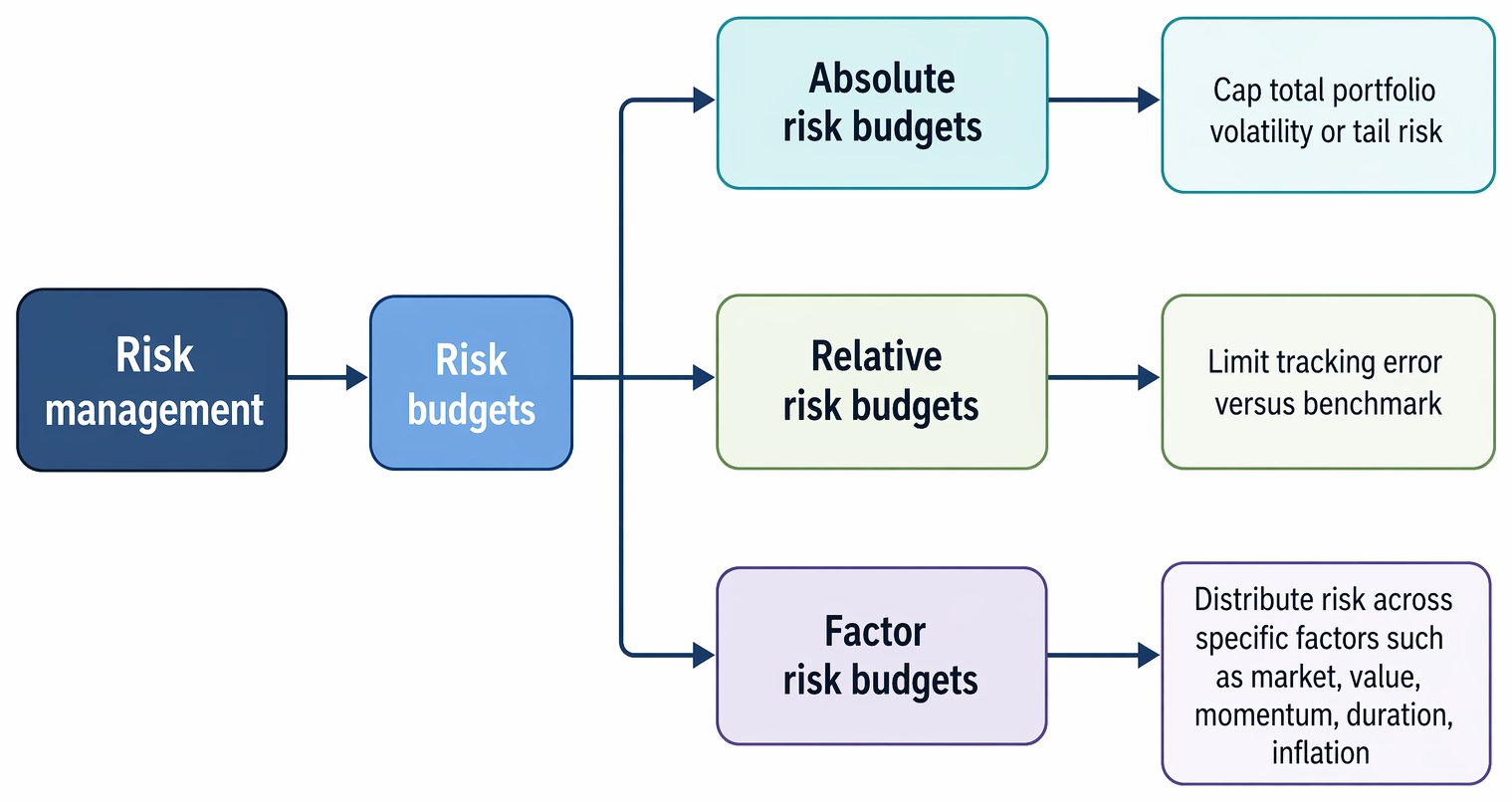

Types of Risk Budgets

- Absolute risk budgets: Place an upper limit on total volatility (e.g., 10% annualized) or tail risk (e.g., limit 1-year 99% VaR).

- Relative risk budgets: Place an upper bound on active risk (tracking error) versus benchmark or policy portfolio.

- Factor risk budgets: Allocate risk exposures among specified risk factors (e.g., market, value, momentum, duration, inflation).

Key Term: tracking error

The standard deviation of portfolio returns relative to a stated benchmark, measuring active risk in implementation.

Impact of Constraints and Robust Optimization

Mean-variance optimization (MVO) identifies capital allocations maximizing expected return for a target risk (or vice versa). However, MVO is notoriously sensitive to small input changes. In practice, investors and advisers face many constraints:

Risk management classifies risk budgets into absolute, relative, and factor-based approaches using volatility, benchmark tracking error, and factor exposure limits.

- Regulatory: e.g., caps on equity or illiquid asset weights

- Liquidity: e.g., need to maintain cash minimums

- Tax: e.g., location limits or short-selling restrictions

- Client: e.g., ESG exclusion lists, sector preference, or max drawdown tolerance

Adding constraints often causes the optimizer to produce portfolios with concentrated, corner solutions or high sensitivity to changing inputs. This can lead to portfolios that may not be stable, diversified, or plausible if conditions change.

Robust optimization methods attempt to address these issues by:

- Directly incorporating parameter uncertainty and estimation error (e.g., using input “uncertainty sets” or scenario analysis)

- Focusing on portfolio allocations that perform satisfactorily across a range of input assumptions instead of a single expected value

- Explicitly reflecting constraints and uncertainty in the mathematical programming process

Key Term: parameter uncertainty

The practical difficulty in precisely estimating inputs (returns, risks, correlations) needed for optimization, increasing the risk of poorly diversified or extreme allocations.

Worked Example 1.1

Question: A sponsor wants the optimizer to produce a portfolio with no asset class weight exceeding 40% and target expected volatility below 9%. Input estimates have considerable uncertainty. How should the optimization process change to accommodate these needs?

Answer:

The situation calls for robust optimization. Rather than a single “point” forecast of return and risk, the model should test allocations across plausible scenarios and require that the solution meets risk/weight constraints under all (or most) conditions. By specifying an “uncertainty set” for asset returns (e.g., ±1% from point estimate) and running a robust or min-max optimizer, the process will typically result in more diversified weights and less input sensitivity compared to classic mean-variance. The additional constraint (max 40% per asset) will further force diversification.Exam Warning: Most portfolio optimizers will ignore estimation risk unless you build it into the process. MVO output should not be trusted blindly—be able to explain how robust methods improve practical viability, and always refer to actual risk exposures, not just nominal weights.

The Black-Litterman Model: Overview and Benefits

Optimizing based on subjective return estimates or trailing averages often leads to corner portfolios, especially when constraints are applied. The Black-Litterman model is widely used for producing more stable, diversified portfolio weights. The methodology:

- Starts with the market portfolio (typically by market capitalization) to derive equilibrium returns using reverse optimization.

- Adjusts the implied returns based on explicit investor views (quantitative forecasts, qualitative opinions) and confidence levels.

- Combines the equilibrium and adjusted views mathematically, producing a new set of expected returns for portfolio optimization.

Key Term: reverse optimization

A process that infers implied equilibrium expected returns from observed market weights and the covariance matrix, assuming investors are risk-neutral to unexplained risk.

Equilibrium-based starting points make the model less sensitive to arbitrary assumptions or parameter errors. Black-Litterman portfolios are typically more diversified and robust, especially under constraints.

Worked Example 1.2

Question: An investor has strong confidence that bond returns will outperform equilibrium by 0.75% and weak confidence in a 0.5% overweight to emerging market equities. How does the Black-Litterman model combine these with the market starting point?

Answer:

The Black-Litterman model mathematically blends equilibrium returns with user “views,” weighted by confidence. A strong view on bonds shifts the blended expected return more towards the forecasted outperformance. For emerging markets, weak confidence in the view means the final return will be closer to the market-implied value. The resulting return vector is then used in portfolio optimization, yielding more balanced weights than classic mean-variance inputting all views as point estimates.

Risk Factor Allocation and Asset Class Mapping

Traditional approaches optimize allocations to asset classes directly. However, many asset classes share exposures to common risk factors, meaning that apparently diversified allocations may in reality concentrate exposure in specific risks (e.g., growth, inflation, credit). Instead, several institutional investors now start by allocating risk budgets** directly to fundamental risk factors and constrain each factor exposure. Asset classes are then selected to implement (as closely as possible) the desired factor exposure.

Key Term: risk factor allocation

The portfolio construction approach where risk-budgeting and allocation decisions are made for each core risk factor (e.g., equity beta, value, liquidity), and assets are then selected according to those exposures.

This approach can reduce both estimation risk and hidden concentrations, and it can produce more robust, scenario-resilient portfolios.

Worked Example 1.3

Question: A pension fund gives equity market, duration, inflation, and liquidity risk factors each a 25% risk budget. How should the asset allocation be set?

Answer:

The pension’s optimizer first assigns portfolio risk (measured by tracking error, standard deviation, or another metric) to each risk factor according to the budget. The resulting exposures may suggest allocations to public equities, private equity, TIPS, infrastructure, or cash as “proxy” asset classes for the risk factors. Some asset classes will span more than one risk factor. The final asset allocation is chosen to best replicate the target factor exposures without violating liquidity or other real-world constraints.

Scenario Analysis and Monitoring Robustness

No allocation method is perfect. Once an asset allocation has been set, it must be tested for performance and risk under a range of scenarios:

- Shortfall/loss analysis (e.g., probability of failing to meet pension obligations or a maximum allowable funding deficit)

- Market stress (e.g., 2008-style equity drawdown, interest rate spike)

- Parameter stress (e.g., what if expected returns fall 1%, correlations rise 50%)

Robust portfolios are less likely to fail under these stress tests than portfolios based on unconstrained or naïve mean-variance optimization. The process should be ongoing: scenario analysis and monitoring are part of maintaining robust risk budgeting and allocation.

Revision Tip: In the exam, when comparing allocation methods, always mention scenario analysis and robustness testing. CFA examiners expect you to demonstrate the practical impact of constraints and estimation uncertainty on portfolio outcomes.

Summary

Risk budgeting, robust optimization techniques, and the Black-Litterman model are essential for developing practical, scenario-resilient asset allocations—especially under constraints. Robust and risk-factor-based approaches go beyond standard mean-variance optimization by recognizing constraints, parameter risk, and the need for stability. The Black-Litterman model helps generate more diversified, practical portfolios by adjusting market-implied returns for human views with measured confidence, then re-optimizing. These approaches better capture regulatory, liquidity, and operational constraints, and are tested on the CFA Level 3 exam.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and apply risk budgeting processes for portfolios

- Recognize the weaknesses of constrained mean-variance optimization, including sensitivity to parameter error and instability

- Understand robust optimization and how it addresses estimation risk and scenario uncertainty

- Describe the Black-Litterman model and its advantage for practical asset allocation

- Explain risk-factor allocation as an alternative to asset-class-based optimization, and the methods to map assets to fundamental risks

- Apply scenario analysis to test portfolio robustness under adverse conditions and changing parameters

Key Terms and Concepts

- risk budgeting

- robust optimization

- Black-Litterman model

- tracking error

- parameter uncertainty

- reverse optimization

- risk factor allocation