Learning Outcomes

This article explains the structure and practical application of risk governance and risk appetite frameworks in a CFA Level 3 context, including:

- How risk governance allocates authority, decision rights, and accountability across the board, senior management, and control functions

- How the three lines of defense model separates risk ownership, risk oversight, and independent assurance, and why this segregation matters for exam scenarios

- How formal risk appetite, risk capacity, and risk tolerance are articulated and translated into concrete limits, policies, and risk reports

- How risk culture, incentive structures, and escalation practices support or undermine adherence to the stated risk appetite in investment organizations

- How to evaluate whether governance structures (e.g., CRO reporting lines, committee mandates, internal audit reporting) are appropriate, independent, and aligned with best practice

- How to identify common exam traps such as blurred responsibilities between lines of defense, weak escalation procedures, or compromised internal audit independence

- How to apply these concepts to CFA-style vignettes by diagnosing weaknesses, prioritizing governance issues, and recommending specific, exam-appropriate improvements

- How risk governance, appetite, and culture link back to fiduciary duties, client objectives, and regulatory expectations that frequently appear across Level 3 readings

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand risk governance and appetite with a focus on the following syllabus points:

- The components of a robust risk governance framework and the role of board oversight

- The three lines of defense model and distinctions between each line

- How risk appetite, risk capacity, and risk tolerance are defined, communicated, and embedded in governance

- Oversight roles for risk committees, audit functions, CROs, and senior management

- The influence of organizational risk culture and incentives on risk-taking behavior

- How governance, controls, and compliance support fiduciary duties in asset management

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Within an investment firm, which body has ultimate responsibility for approving the enterprise-wide risk appetite statement?

- a) Chief risk officer (CRO)

- b) Chief investment officer (CIO)

- c) Board of directors (or board risk committee)

- d) Internal audit function

-

Under the three lines of defense model, which pairing best describes first- and second-line responsibilities?

- a) First line: sets risk appetite; second line: executes trades

- b) First line: owns and manages risks; second line: provides oversight, policies, and challenge

- c) First line: performs internal audits; second line: approves financial statements

- d) First line: monitors compliance; second line: approves product launches

-

In the context of risk governance, what is the primary distinction between risk ownership and risk oversight?

- a) Risk owners design strategic objectives; risk oversight sets compensation

- b) Risk owners trade only for proprietary books; risk oversight trades only for clients

- c) Risk owners make and manage risk-taking decisions; risk oversight monitors and challenges those decisions

- d) Risk owners report to the board; risk oversight reports only to regulators

-

Which statement about internal audit is most consistent with the three lines of defense model?

- a) Internal audit may design day-to-day risk controls if it improves efficiency

- b) Internal audit provides independent assurance and should not be involved in routine risk management decisions

- c) Internal audit must report directly to the CRO to ensure independence

- d) Internal audit is responsible for setting trading limits for the front office

Introduction

Effective risk governance is essential for managing and controlling risk within financial and investment organizations. CFA Level 3 candidates must be able to assess whether an institution’s governance structure, risk appetite, and culture are robust, and to diagnose weaknesses in exam case scenarios.

Key Term: risk governance

Risk governance is the system of structures, authorities, and processes by which risk oversight and risk management are directed and controlled across the organization.

At Level 3, this topic is not just definitional. You are expected to link governance, risk appetite, and culture, and to evaluate whether risk-taking is aligned with fiduciary duties, client objectives, and regulatory expectations.

Test Tip: When revising Three lines of defense and oversight, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

The Risk Governance Framework

Robust risk governance creates clear accountability for identifying, assessing, monitoring, and reporting risks across the institution. It ensures that risk-taking is aligned with the institution’s strategic goals and risk appetite set by the board of directors. The framework formally outlines who owns risks, who oversees risk management, and who provides independent assurance of risk controls.

Risk governance responsibilities are allocated across business units, risk and compliance functions, and internal audit under the three-lines-of-defense model.

A well-designed framework typically addresses:

- Governance structure (board, committees, reporting lines)

- Risk management framework (policies, methodologies, risk taxonomy)

- Risk appetite and limit structure

- Risk data, reporting, and escalation processes

- Independent assurance and internal audit coverage

- Culture, incentives, and accountability mechanisms

Oversight Structures

The board of directors holds ultimate accountability for risk oversight, setting the risk appetite and culture. Senior management implements the risk framework, delegates risk-taking responsibilities, and ensures embedded risk controls. Risk committees, audit committees, and chief risk officers (CROs) are essential to effective oversight.

Key Term: board of directors

The board of directors is the highest governing body responsible for approving strategy, risk appetite, and major policies, and for overseeing management’s risk-taking on behalf of shareholders or beneficiaries. Key Term: senior management

Senior management consists of executives responsible for implementing the board-approved strategy and risk framework, ensuring that business activities operate within the defined risk appetite. Key Term: chief risk officer (CRO)

The chief risk officer is a senior executive who leads the risk management function, provides independent risk oversight, and reports on risk exposures and adherence to risk appetite.

In many institutions, the board delegates detailed risk oversight to a board risk committee and financial reporting and control oversight to an audit committee. Key exam-relevant features include:

- The CRO should have a direct reporting line to the board risk committee (or full board) to preserve independence from business pressures.

- The risk function should be structurally separate from revenue-generating units.

- The audit committee oversees financial reporting, internal controls, and the internal audit function, which provides independent assurance on both first- and second-line activities.

Regulators and best-practice codes (including the Asset Manager Code) expect asset managers to maintain documented compliance and risk management policies and to appoint a competent compliance or risk officer with authority to enforce them. This maps directly into the second line of defense discussed below.

Key Term: risk appetite

Risk appetite is the level and type of risk an organization is willing to accept in pursuit of its strategic objectives, defined and approved by the board.

A complete risk governance framework links this risk appetite to:

- Strategic planning and capital allocation

- Product design and approval

- Portfolio construction and risk budgeting

- Compensation and performance measurement

Weak governance in exam questions often shows up as:

- A CRO reporting only to the CFO, who is also lobbying for higher risk-taking

- No formal board-approved risk appetite statement

- Risk and compliance subordinated to front-office heads

- Internal audit reporting operationally to the CFO rather than to the audit committee

You should be prepared to identify such weaknesses and recommend changes that strengthen independence and accountability.

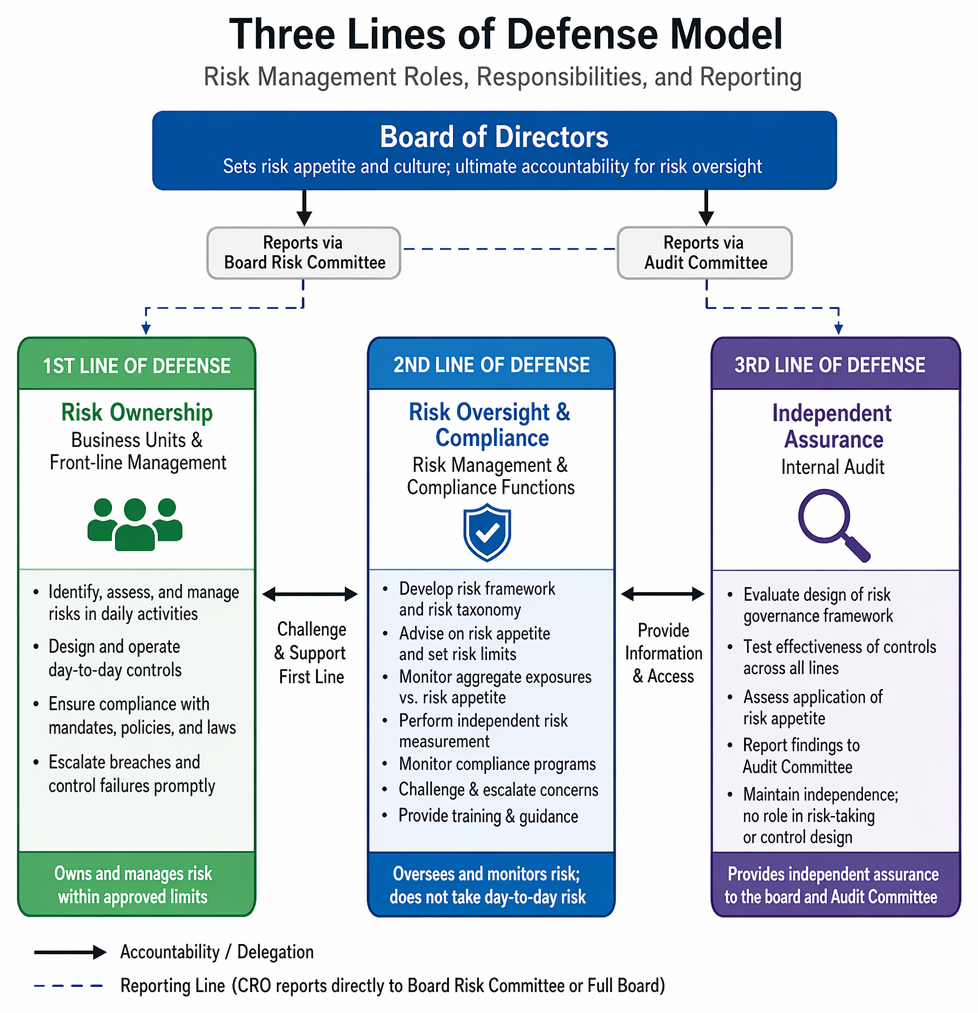

The Three Lines of Defense Model

The three lines of defense structure clarifies how risk management is distributed across the organization. It is especially relevant in asset management firms, banks, and insurers.

Key Term: three lines of defense

The three lines of defense model divides risk-related responsibilities among: (1) front line business risk owners, (2) risk oversight and compliance functions, and (3) internal audit providing independent assurance.

First Line of Defense – Risk Ownership

- First Line: Business units and front-line management. They own and manage risks in daily activities. They are responsible for identifying, assessing, and mitigating risks within their area using established controls.

Key Term: risk owner

A risk owner is the person, role, or business unit directly responsible for managing a specific risk within approved policies and procedures.

Examples in an investment firm:

- Portfolio managers managing market, liquidity, and counterparty risks in their portfolios within approved mandates

- Traders managing intraday exposures within pre-set limits

- Relationship managers managing conduct and suitability risks in client interactions

First-line responsibilities include:

- Designing and operating day-to-day controls (pre-trade checks, reconciliations, sign-offs)

- Ensuring activities conform to mandates, policies, and laws

- Promptly escalating actual or potential limit breaches or control failures

Failure of the first line often appears in exam vignettes as traders ignoring limits, portfolio managers “drifting” from mandates, or sales staff mis-selling products.

Second Line of Defense – Risk Oversight and Compliance

- Second Line: Risk management and compliance functions. These functions provide oversight, set risk policies, monitor limits, and support front lines. They do not manage risks day to day but assist with frameworks, training, and risk monitoring.

Key Term: risk oversight

Risk oversight is the monitoring, review, and challenge of the organization’s risk management practices to ensure that risks are managed within the approved risk appetite and policies. Key Term: compliance function

The compliance function is the independent function that monitors adherence to legal, regulatory, and internal policy requirements and advises the business on compliance risks.

Key second-line activities include:

- Developing and maintaining the enterprise risk management framework and risk taxonomy

- Advising the board and senior management on risk appetite and risk limits

- Monitoring aggregate risk exposures versus risk appetite

- Performing independent risk measurement (e.g., VaR, stress tests)

- Designing and monitoring regulatory compliance programs

- Providing training and guidance on risk and compliance requirements

- Challenging first-line risk decisions and escalating concerns when needed

From the Asset Manager Code standpoint, managers must maintain policies and procedures to comply with laws and ethical standards and must appoint a compliance officer empowered to investigate issues. This is classic second-line responsibility.

Third Line of Defense – Independent Assurance

- Third Line: Independent assurance, typically internal audit. This function evaluates the design and effectiveness of controls and risk frameworks put in place by the first and second lines. It is entirely independent of operations and risk oversight.

Key Term: internal audit

Internal audit is an independent function that provides assurance to the board and senior management on the effectiveness of governance, risk management, and internal controls.

Third-line responsibilities include:

- Assessing whether the risk governance framework is designed appropriately

- Testing whether controls are operating effectively across the first and second lines

- Evaluating whether the risk appetite framework is being applied in practice

- Reporting findings directly to the audit committee, with unrestricted access to records and personnel

A key exam point: internal audit should not design day-to-day controls or participate in risk-taking decisions, as that compromises its independence.

Segregation and Independence

The three lines model is essentially about segregation of duties:

- The same individuals should not both take risk and oversee that risk.

- The function assessing the effectiveness of controls should be independent from those designing or operating them.

Common exam traps:

- The CRO also heads the trading desk (combining first and second line).

- Internal audit helps write trading desk procedures (third line partially becoming first line).

- Compliance staff are compensated primarily on business growth, reducing independence.

You should be able to explain why such arrangements weaken governance and recommend alternatives.

Worked Example 1.1

A CFA candidate is reviewing a scenario where an investment firm’s risk committee notices that the front-office trading desk regularly exceeds daily VaR limits but argues that it is “within the spirit” of risk policy. Who is responsible for reporting and escalating this breach under the three lines model, and what should the second line do?

Answer:

The trading desk (first line) is responsible for risk ownership, including reporting limit breaches as soon as they occur. The risk management function (second line) must independently monitor and verify limit usage, identify the breaches, and formally escalate them to senior management and the board risk committee. The second line should challenge the trading desk’s “within the spirit” argument, require remediation (e.g., tightening limits, reducing positions), and confirm that risk-taking is brought back within the formally approved risk appetite.

Worked Example 1.2

A global asset manager states in its risk appetite that it will accept liquidity risk up to $10m of daily net outflows but is “zero tolerant” for non-compliance risk. During a quarterly review, compliance finds evidence that an order was executed in breach of regulatory requirements but the financial loss was minimal. What is the responsibility of the risk oversight function, and what should happen to the breach?

Answer:

The risk oversight function (second line), primarily compliance, must escalate non-compliance breaches regardless of financial loss, because the risk appetite is zero tolerance for this risk type. The breach should be reported to senior management and, where material, to the board or regulators as required. Root causes should be identified and corrective actions implemented (e.g., training, process changes), irrespective of financial materiality.

Worked Example 1.3

A portfolio manager exceeds a concentration limit by 5% in a client portfolio due to market movements. The manager believes the breach is temporary and plans to correct it over the next month. The risk report showing the breach is generated daily but sent to senior management only at month-end. Evaluate this situation in terms of the three lines of defense and escalation practices.

Answer:

The portfolio manager (first line) is responsible for monitoring concentration risk and must act promptly once a breach occurs, not wait a month. Deliberately delaying correction conflicts with the duty to manage risks within limits. The risk function (second line) should design reporting and escalation processes so that limit breaches are flagged and escalated in near real time to senior management, not only via monthly reports. A robust framework would require immediate notification of material breaches and pre-defined timelines for remediation.

Risk Appetite, Capacity, and Culture

The board of directors sets the risk appetite statement, outlining acceptable types and levels of risk.

Key Term: risk appetite statement

A risk appetite statement is a formal, board-approved document that articulates the types and levels of risk the organization is willing to accept and how these support strategic objectives. Key Term: risk capacity

Risk capacity is the maximum level of risk the organization can absorb without breaching constraints such as regulatory capital, solvency, or its continued viability. Key Term: risk tolerance

Risk tolerance is the degree of variability in outcomes that the organization is willing to withstand in pursuing its objectives, usually expressed as more granular limits within the broader risk appetite and capacity.

Risk appetite must be:

- Consistent with risk capacity: A firm with limited capital or strict regulatory requirements cannot credibly have a high risk appetite.

- Aligned with strategy: An asset manager pursuing low-volatility, income-oriented mandates cannot have a high appetite for illiquid, highly leveraged strategies at the enterprise level.

- Operationalized: The risk appetite statement needs to be translated into quantitative risk limits and qualitative guidelines.

Key Term: risk limits

Risk limits are quantitative boundaries (e.g., exposures, loss thresholds, leverage ratios) derived from the risk appetite that constrain risk-taking at various organizational levels.

Examples of risk appetite components:

- Maximum acceptable probability of breaching regulatory capital ratios

- Maximum permissible tracking error versus benchmark for portfolio strategies

- Limits on leverage, liquidity mismatches, or counterparty exposure

- Zero tolerance for fraud, regulatory breaches, or misappropriation of client assets

Translating Risk Appetite into Practice

To embed risk appetite:

- The board approves an enterprise-wide risk appetite statement.

- Senior management decomposes this into risk limits by business line, portfolio, or desk.

- Risk budgets (e.g., tracking error or VaR allocations) are assigned to portfolios.

- Policies specify escalation thresholds (e.g., soft limits triggering discussion, hard limits requiring immediate action).

Exam questions often test whether limits are designed and implemented coherently. For example:

- If the board has low appetite for liquidity risk, but portfolios are heavily invested in illiquid private assets with no aggregate liquidity limit, there is a misalignment.

- If tracking error limits are set but there is no monitoring of factor exposures, the firm may inadvertently take unintended risks.

A healthy risk culture is critical—individuals are expected to act ethically, challenge risk decisions, and escalate issues without fear.

Key Term: risk culture

Risk culture is the set of shared values, beliefs, and behaviors that shape how individuals in an organization perceive and manage risk.

Risk culture is reflected in:

- How seriously limit breaches are treated

- Whether staff feel safe to speak up about concerns

- How management responds to bad outcomes (learning vs blame)

- How incentives balance returns with risk and compliance behavior

Poor culture shows up in exam cases as:

- Repeated “technical” breaches with no consequences

- Management ignoring or pressuring risk and compliance staff

- Compensation plans based solely on revenue or returns, with no adjustment for risk, compliance, or long-term client outcomes

Worked Example 1.4

An asset management firm’s board approves a risk appetite that targets “top-quartile investment performance relative to peers” and states “low appetite for operational and conduct risk.” Portfolio managers’ bonuses, however, are based solely on one-year pre-fee performance relative to benchmark, with no adjustment for operational losses or compliance breaches. Evaluate the consistency of incentives with the stated risk appetite.

Answer:

The risk appetite expresses a low appetite for operational and conduct risk, but the bonus structure rewards short-term investment performance only. This misalignment encourages first-line staff to ignore operational controls or push compliance boundaries to improve returns. To support the stated appetite, performance evaluation should incorporate risk-adjusted performance, operational and compliance metrics, and longer horizons, thereby reinforcing the desired risk culture.

Risk Governance Roles and Oversight

The following governance roles appear frequently in Level 3 case studies. You should be able to describe and evaluate each.

Key Term: risk committee

A risk committee is a board or management-level committee that oversees the organization’s risk profile, risk appetite, and effectiveness of the risk management framework. Key Term: escalation procedures

Escalation procedures are formal protocols specifying when and how risk issues, breaches, or emerging threats must be reported to higher levels of management or the board.

-

Board of Directors: Establishes risk governance, approves the risk appetite statement, reviews major risk policies and material risk exposures, and oversees management. The board ensures that risk and audit functions are independent, adequately resourced, and have direct access to the board.

-

Senior Management: Implements the board-approved risk framework, delegates authority, monitors limits, and sets the tone for risk culture. Management must ensure that risk and compliance functions are independent of the business units they oversee and that escalation procedures are effective.

-

Risk Committees:

- Board-level risk committee: Oversees enterprise risk, approves risk appetite, and reviews risk reports.

- Management-level risk committee: Coordinates risk across businesses, reviews limit allocations, and considers new products from a risk standpoint.

-

CRO/Risk Function: Reports independently to the board or its risk committee (often with a secondary line to the CEO). The risk function ensures risks are measured, monitored, and escalated and that risk appetite is embedded in policies and limits.

-

Compliance Function: Focuses on regulatory and policy compliance, including conduct risk and fiduciary obligations. Plays a key role in zero-tolerance areas such as fraud and regulatory breaches.

-

Internal Audit: Provides independent assurance that controls work as intended and that the governance framework is effective. Internal audit reports to the audit committee, not management, and uses a risk-based audit plan targeting the most significant risks.

Exam Warning: Internal audit should not participate in designing day-to-day controls or risk decisions. Its role is independent assessment only. For the exam, mixing assurance with operational risk management is a frequent error. Similarly, a CRO fully embedded in the front office, reporting to a trading head, indicates weak independence.

Worked Example 1.5

In an exam vignette, an investment firm’s CRO reports to the CFO, who also chairs the internal risk committee. The CRO’s bonus is based primarily on firm profitability. Internal audit reports to the CRO. Identify and evaluate the main governance weaknesses.

Answer:

Several weaknesses are evident:

- The CRO reports to the CFO, whose primary responsibility is financial performance, creating potential pressure to downplay risks. Best practice is for the CRO to have direct access to the board risk committee or full board.

- Tying the CRO’s bonus mainly to profitability undermines independence; risk oversight should be incentivized based on risk management quality and adherence to appetite, not just earnings.

- Internal audit reporting to the CRO compromises third-line independence. Internal audit should report to the audit committee or board, not to management functions it audits. Overall, this structure weakens both the second and third lines of defense and should be flagged as inappropriate in a Level 3 answer.

Summary

Strong risk governance relies on clear distinction between risk ownership (first line), risk oversight (second line), and independent assurance (third line). Board-approved risk appetite and risk capacity steer risk-taking and are embedded through policy, limits, and culture. Oversight functions must challenge, support, and monitor management actions to enforce risk discipline and prevent the escalation of uncontrolled risks. At Level 3, you are expected not only to recall these structures but to evaluate whether a given governance arrangement is adequate and to justify recommended improvements.

Key Point Checklist

This article has covered the following key knowledge points:

- The purpose and structure of risk governance in financial organizations

- How the board, risk committees, and senior management share responsibilities for risk oversight

- The three lines of defense model: responsibilities and separation of roles

- How risk appetite, risk capacity, and risk tolerance are articulated and cascaded into limits

- How risk appetite is communicated and enforced through policies, limits, and escalation practices

- The role of risk culture and incentives in supporting or undermining risk appetite

- How internal audit provides independent assurance and why its independence must be preserved

- Typical governance weaknesses and exam traps involving blurred responsibilities and compromised oversight

Key Terms and Concepts

- risk governance

- board of directors

- senior management

- chief risk officer (CRO)

- risk appetite

- three lines of defense

- risk owner

- risk oversight

- compliance function

- internal audit

- risk appetite statement

- risk capacity

- risk tolerance

- risk limits

- risk culture

- risk committee

- escalation procedures