Learning Outcomes

This article explains how to classify, measure, and monitor liquidity risk, gearing, and counterparty risk in an investment portfolio setting, with specific focus on CFA Level 3 exam requirements. It clarifies key terminology, distinguishes between asset, funding, and system-wide liquidity risk, and links these concepts to common quantitative metrics, stress tests, and scenario analysis. It describes how gearing is defined in balance-sheet, economic, and regulatory terms, how it amplifies volatility and drawdowns, and how it should be monitored using risk measures such as VaR, stress VaR, and capital ratios. It also details how counterparty exposure arises in derivatives, repos, and OTC trades, how collateral, netting, and CSAs reduce exposure, and how wrong-way risk is identified. The article further outlines legal and regulatory duties for risk disclosure, documentation, and reporting, emphasizing how managers should evidence independent risk oversight. Throughout, the focus is on interpreting data, drawing exam-ready conclusions, and proposing practical monitoring actions for different risk scenarios.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the classification, measurement, and monitoring of key investment risks, with a focus on the following syllabus points:

- Evaluating liquidity risk, gearing, and counterparty risk in portfolio contexts

- Describing methods to measure and monitor these risks across instruments and portfolios

- Explaining regulatory, operational, and legal requirements involving risk disclosures and reporting

- Assessing the impact of gearing on overall risk and return

- Analysing how counterparty exposures are monitored and managed

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which metric is most appropriate for measuring a portfolio’s sensitivity to funding stress?

- What is the main legal requirement for reporting material counterparty exposures?

- When using gearing, what additional risk must be disclosed to investors compared to an unlevered portfolio?

- True or false: Counterparty risk is only relevant for derivatives held on-exchange.

Introduction

Effective risk measurement and monitoring are critical for safeguarding investor capital and for meeting regulatory standards. Three areas require close attention: liquidity risk, gearing, and counterparty risk. Investment professionals must regularly assess their portfolio’s ability to withstand market shocks, cover obligations, and recover from default events. This article outlines key risk types, measurement techniques, disclosure obligations, and CFA-relevant best practices.

Liquidity Risk

A portfolio must be able to meet payment demands, withstand market stress, and rebalance on short notice. Inadequate liquidity can cause forced sales, price discounts, or breaches of contractual and regulatory covenants.

Key Term: liquidity risk

The risk that a position cannot be sold, converted to cash, or financed without unacceptable loss, cost, or delay.

Sources of Liquidity Risk

- Asset liquidity risk: Difficulty quickly selling holdings at or near fair value.

- Funding liquidity risk: Inability to obtain or roll over external funding when required.

- System-wide liquidity risk: The threat that market-wide liquidity evaporates in times of crisis.

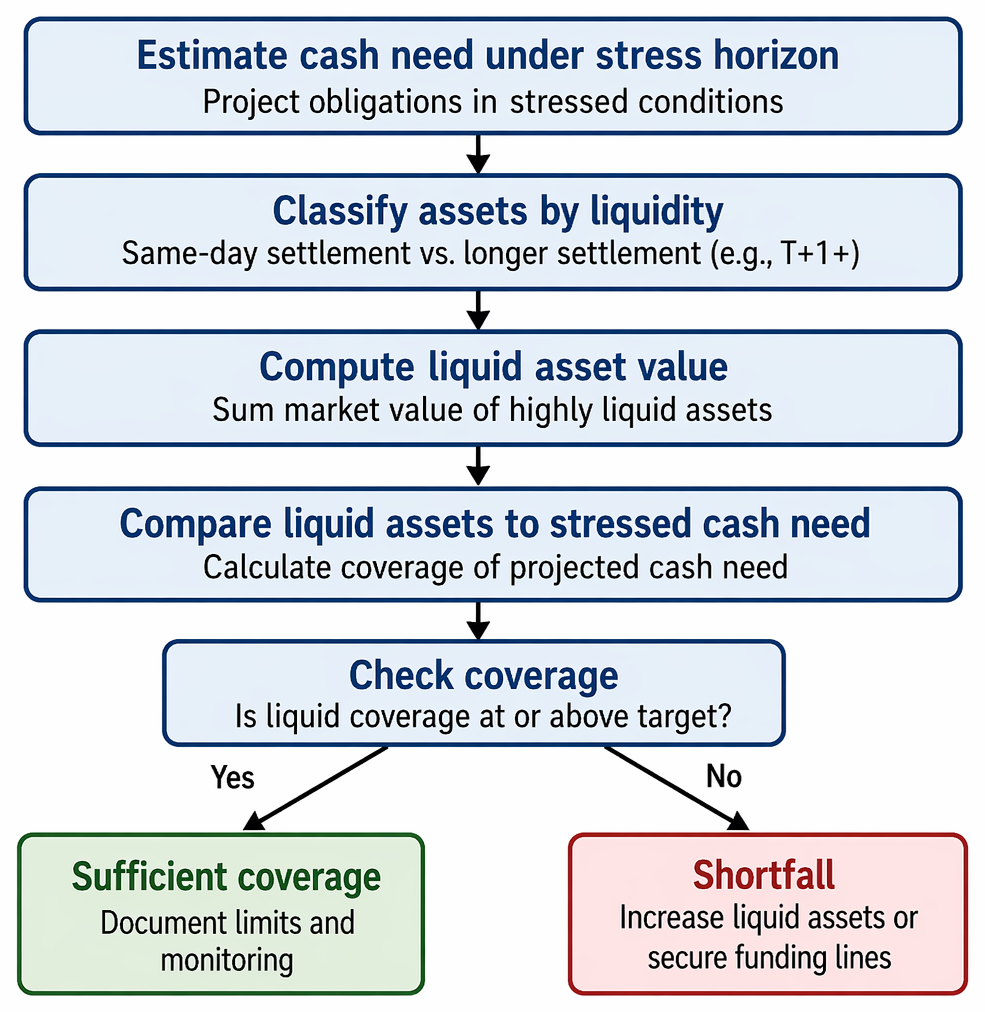

Measurement Techniques

- Bid–ask spread analysis and average daily trading volume for asset liquidity

- Cash flow projections and stress scenario testing for funding liquidity

- Liquid asset ratios (e.g., percentage of portfolio in same-day and T+1 settlement assets)

- Metrics such as Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR)

- Scenario testing: Model portfolio cash requirements under normal and stressed conditions

Worked Example 1.1

A UK pension fund holds £80m in government bonds, £20m in private equity, and £15m in emerging market debt. It estimates that, in a moderate market stress, it would need to free up 12% of its assets for liability payments within one week.

Answer:

The government bonds are highly liquid, while the private equity and some emerging market debt may be illiquid. The fund should check if the value of liquid assets covers at least £13.5m (12% of total assets). If not, liquidity risk is material and monitoring procedures must be updated.Exam Warning: Many exam candidates only consider asset liquidity. Always include funding risk and stress scenarios in your answer to receive full marks.

Gearing Risk

Gearing magnifies gains and losses. Regulatory and legal requirements demand clear disclosures on how gearing is calculated, used, and monitored.

Key Term: gearing

The use of borrowed money (or derivatives with embedded financing) to increase portfolio exposure relative to capital.

Types and Measurement

- Balance sheet gearing: Ratio of assets to equity capital.

- Economic gearing: Sensitivity of the portfolio’s value to changes in market factors (e.g., duration for bonds, delta for options).

- Regulatory gearing: As defined by legal rules (e.g., UCITS, AIFMD, and SEC rules).

Monitor gearing using:

- Value at Risk (VaR) and Stress VaR

- Maximum drawdown analysis

- Regulatory capital ratios

- Scenario analysis: Examine the impact of market shocks under current gearing

Worked Example 1.2

A hedge fund with £10m in capital borrows £40m and invests £50m in high-yield corporate bonds. The annualized volatility of the bonds is 10%. Calculate the volatility of fund equity.

Answer:

Portfolio volatility is £50m × 10% = £5m. Fund volatility as a percentage of capital is £5m / £10m = 50%. Gearing increases the risk of the portfolio fivefold.Revision Tip: Always relate gearing risk to stress-test outcomes and capital adequacy when responding to exam scenarios.

Counterparty Risk

Counterparty risk can crystallize instantly—especially in derivatives, repo, and OTC markets. CFA examiners expect you to distinguish between on-exchange and bilateral risks and to describe documentation and monitoring techniques.

Stress-horizon cash requirements are matched against liquid-asset values by settlement bucket to confirm target coverage or identify funding actions.

Key Term: counterparty risk

The risk that the other party to a financial contract defaults before settlement or fulfilment of their obligations. Key Term: credit support annex (CSA)

An agreement within derivative documentation specifying the terms for collateral posting to cover current and potential credit exposure. Key Term: netting agreement

A contract between counterparties to offset mutual obligations, reducing exposure if one party defaults.

Measurement and Monitoring

- Credit exposure metrics: Peak and expected exposure, potential future exposure (PFE).

- Aggregated notional and market values by counterparty.

- Exposure to wrong-way risk (when counterparty default likelihood increases as exposures rise).

Regulators (such as the FCA, SEC, and ESMA) often require at least daily monitoring and prompt reporting of material changes.

Worked Example 1.3

A fund manager enters a long-term interest rate swap with a bank, collateralized by a CSA requiring daily margin. After a sudden downgrade in the bank’s credit rating, how should the fund react?

Answer:

The fund should check margin calls are adequate, consider demanding increased collateral or reducing notional exposure, and promptly disclose the increased counterparty risk according to legal requirements.

Exam Warning

It's a frequent exam error to assume that clearing via a Central Counterparty (CCP) removes all counterparty risk. In practice, CCPs still pose risk if margining and default waterfall procedures are misunderstood.

Risk Disclosures, Legal Duties, and Documentation

Investment managers have legal obligations to:

- Prepare clear risk disclosures on liquidity, gearing, and counterparty exposures for investors and relevant authorities.

- Review and update risk policies and process documentation annually (or when material changes occur).

- Maintain evidence of independent risk assessment for regulatory inspection (e.g., policies signed by a responsible person, documented stress tests).

Key Term: risk disclosure statement

A document provided to clients or regulators summarizing material risks, assumptions, metrics, and stress test results for portfolio risk factors.

Regulatory Filing Requirements

- Report large exposures, breaches of concentration or gearing limits, and serious liquidity or funding concerns according to notice periods required by law or local regulatory rules.

- Use standardized templates or regulatory portals for reporting (e.g., Form PF, AIFMD Annex IV, EMIR reports).

Revision Tip

In exams, always highlight the duty to escalate and document any risk regime change—unexpected illiquidity, gearing increase, or major counterparty deterioration.

Summary

Measurement and monitoring of liquidity risk, gearing, and counterparty risk are central to investment risk control and legal compliance. Liquidity risk analysis involves asset and funding stress scenarios. Gearing increases both expected returns and risk; the effects must be carefully modelled and disclosed. Counterparty risk requires aggregate measurement, collateral and netting agreements, and clear reporting. Legal duties mandate that risk metrics, scenario tests, and exposures be documented and disclosed for both regulatory review and client reporting.

Key Point Checklist

This article has covered the following key knowledge points:

- Define liquidity risk, gearing, and counterparty risk and their respective legal disclosure requirements

- Identify and apply quantitative and qualitative risk measurement tools—including scenario analysis and stress testing

- Monitor and document portfolio risks using clear, investor-friendly language and legal documentation

- Recognize regulatory notification and on-going risk monitoring obligations for all three risk areas

- Use worked examples to apply core measurement and disclosure methods

Key Terms and Concepts

- liquidity risk

- gearing

- counterparty risk

- credit support annex (CSA)

- netting agreement

- risk disclosure statement