Learning Outcomes

This article explains stress testing, scenario analysis, and sensitivity analysis for risk measurement and monitoring in the CFA Level 3 curriculum, including:

- understanding the objectives of stress testing and how it complements traditional risk measures such as VaR in capturing tail risk and concentration risk;

- distinguishing between historical, hypothetical, and reverse stress scenarios, and recognizing when each approach is most appropriate for institutional portfolios;

- identifying and selecting relevant risk factors, building coherent scenarios, and specifying assumptions that reflect an institution’s actual exposures and risk appetite;

- applying stepwise stress testing and sensitivity analysis techniques to evaluate interest-rate, equity, credit-spread, and multi-factor shocks on portfolio value;

- interpreting loss distributions, key drivers of risk, and scenario results to assess risk capacity, test risk limits, and support capital and liquidity planning;

- translating numerical stress-testing outputs into clear management reports, recommendations, and exam-quality justifications for hedging, rebalancing, or adjusting exposures;

- recognizing practical limitations of models, data, and scenario design, and explaining why stress-testing results should complement, rather than replace, other quantitative risk metrics in exam answers.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the application of stress testing and sensitivity analysis in risk measurement and monitoring, with a focus on the following syllabus points:

- Explain the objectives and tools of scenario and sensitivity analysis in institutional risk monitoring

- Apply scenario stress testing to identify potential adverse risk exposures

- Evaluate portfolio risk exposures using sensitivity analysis

- Interpret and communicate stress testing results to inform risk management decisions

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the main objective of scenario stress testing in a risk management framework?

- How does sensitivity analysis differ from scenario analysis in risk monitoring?

- Why are both moderate and extreme events considered in stress tests?

- True or False? Stress testing results should be used as the sole basis for all risk management decisions.

Introduction

Stress testing and sensitivity analysis are critical risk measurement and monitoring tools used by institutional investors and risk managers. These techniques are designed to identify how portfolio values respond to adverse or extreme events and to reveal risks that standard measures might overlook. For the CFA exam, you must understand the design, implementation, and interpretation of stress tests and how these assessments support sound risk management.

Key Term: stress testing

The process of assessing the impact of extreme but plausible events on a portfolio’s value or on an institution’s financial condition. Key Term: scenario analysis

A risk management tool where the outcomes for a portfolio are evaluated under defined market or economic conditions, sometimes hypothetical or based on historical events. Key Term: sensitivity analysis

The technique of measuring changes in a portfolio’s value or a position’s risk measure due to small shifts in one or more input variables (e.g., market factors).

Why Stress Test and Use Scenario Analysis

Traditional risk measures (such as value at risk, VaR) often underestimate tail risks and do not capture risks of extreme market movements, illiquid assets, or non-linear products. Stress testing and scenario analysis address these limitations by exposing a portfolio to a range of justified “what-if” conditions, including severe market shocks or simultaneous adverse moves in multiple variables. They are essential for identifying vulnerabilities, testing risk capacity, and validating the robustness of investment strategies.

Key Term: risk factor

An explanatory variable (e.g., interest rate, currency, credit spread) that affects the value of the portfolio or its components.

Types of Stress Testing

Stress testing and scenario analysis can be classified into two main approaches:

- Historical scenarios: Testing portfolio behavior using actual historical events (e.g., 2008 financial crisis, dot-com crash).

- Hypothetical scenarios: Constructing plausible but not yet observed situations based on expert judgment, regulatory guidance, or “reverse stress testing” (finding the scenario that would lead to a critical breach).

Stress testing generally involves more extreme conditions than regular scenario analysis and is designed to explore portfolio robustness beyond typical market environments.

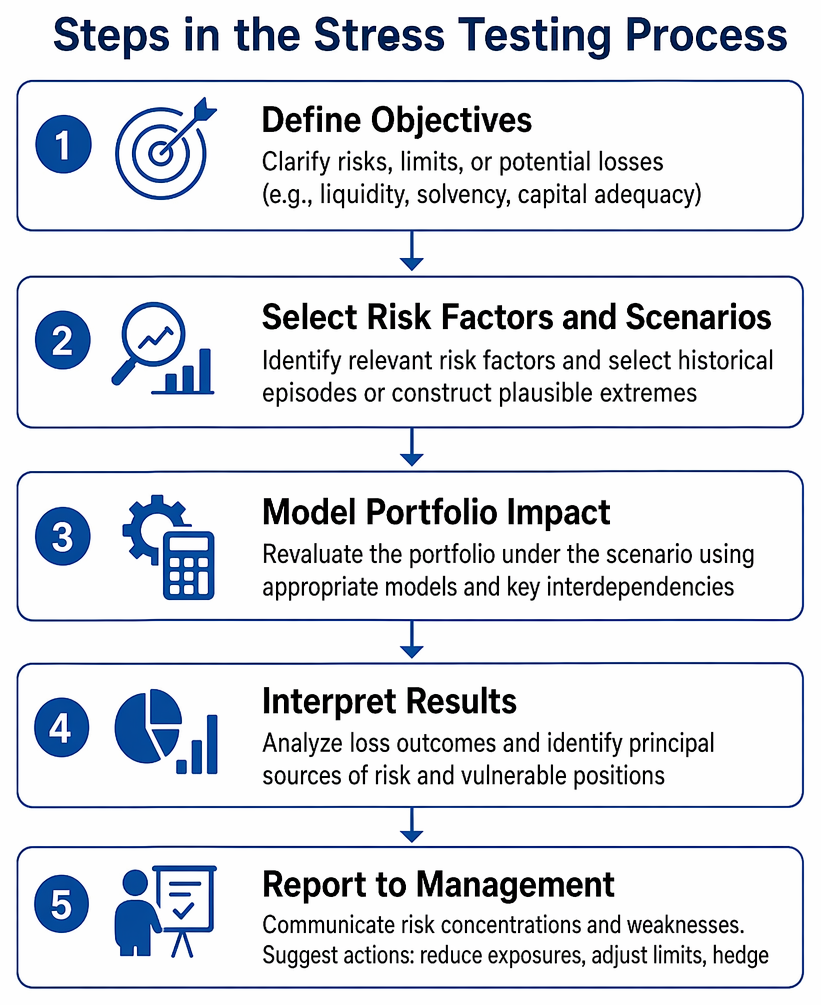

Steps in the Stress Testing Process

A robust stress testing framework follows a systematic process:

Stress-testing workflow linking risk objectives, scenario design, portfolio revaluation, loss analysis, and management reporting with recommended actions.

- Define Objectives: Clarify what risks, limits, or potential losses are to be explored (e.g., liquidity, solvency, capital adequacy).

- Select Risk Factors and Scenarios: Identify relevant risk factors and either select historical episodes or construct plausible extreme movements. Scenarios should be consistent with the institution’s exposures.

- Model Portfolio Impact: Revaluate the portfolio under the scenario using appropriate pricing models, considering all relevant non-linearities, correlations, and interdependencies.

- Interpret Results: Analyze the loss outcomes, identify principal sources of risk, exposures to specific factors, or positions prone to large drawdowns.

- Report to Management: Communicate risk concentrations and weaknesses to decision-makers. Suggest actions such as reducing exposures, adjusting limits, or hedging.

Key Term: risk appetite

The amount and type of risk an investor or institution is willing to accept in pursuit of objectives.

Sensitivity Analysis

Sensitivity analysis quantifies the effect of small changes in single or multiple risk factors (e.g., a 50bp rise in rates, a 5% drop in equity markets) on portfolio value. It highlights which exposures are most influential and can be used for both linear and non-linear positions.

Common examples:

- Interest rate risk (“DV01” or “PV01”): change in value per basis point change.

- Equity delta: change in value for a 1% change in equity index.

- Credit spread risk: shift in credit spreads.

Key Term: DV01

Dollar value change of a portfolio or position for a 1 basis point change in yield.

Practical Application and Limitations

Stress tests are most useful when they are targeted to a portfolio’s actual risk exposures and consider plausible but severe events—including both direct and indirect risk channels. However, results are highly scenario-dependent and sensitive to modeling assumptions. They should be interpreted as complements to statistical risk measures, not substitutes.

Worked Example 1.1

Question: A global bond portfolio manager wants to assess risk to a sudden 100bp rise in US Treasury yields along with a 25bp increase in investment-grade credit spreads. The portfolio market value is $200 million with effective duration of 8 years, and 50% is allocated to US Treasuries, 50% to investment-grade corporate bonds (spread duration of 5 years). What is the estimated portfolio loss under this stress scenario?

Answer:

- US Treasury portion: Loss = $100 million × 8 × 1% = $8 million.

- Corporate bond portion: Rate loss = $100 million × 8 × 1% = $8 million; Spread loss = $100 million × 5 × 0.25% = $1.25 million.

- Total loss: $8m (Treasury) + $8m (Corp rate) + $1.25m (Corp spread) = $17.25 million, or 8.6% of portfolio value.

Using Stress Tests in Decision-Making

Risk monitoring must be timely and actionable. Stress test results are used to:

- Review potential portfolio losses.

- Identify primary drivers of loss or risk concentrations.

- Inform setting or revision of risk limits.

- Support capital and liquidity planning.

- Guide hedging or rebalancing decisions.

Exam Warning: Stress testing is only as robust as the scenarios and inputs considered. Unrealistically mild or excessively remote events may provide false security or excessive conservatism. Base scenarios on relevant, plausible (but severe) market events.

Revision Tip: Explain the logic behind your scenario selection in the exam. Relate the scenario to actual exposures in your case study or calculation.

Summary

Stress testing and scenario analysis are core risk measurement and monitoring methods for institutional investors. Carefully designed tests support identification of vulnerabilities, assessment of risk limits, and capital planning under stressed conditions. Sensitivity analysis is a necessary complement for understanding direct exposure to individual risk factors. For the CFA exam, be able to explain the purpose, design steps, and appropriate interpretation of these methods, alongside their practical limitations.

Key Point Checklist

This article has covered the following key knowledge points:

- Define the objectives and methodology of stress testing/scenario analysis in risk measurement.

- Distinguish between historical and hypothetical (reverse) scenario and stress tests.

- Outline the stepwise process for performing stress tests and sensitivity analysis.

- Apply scenario and sensitivity analysis to a sample institutional portfolio.

- Interpret stress testing results for risk limits, capital planning, and management action.

- Recognize key limitations and correct interpretation of scenario and sensitivity analysis.

Key Terms and Concepts

- stress testing

- scenario analysis

- sensitivity analysis

- risk factor

- risk appetite

- DV01