Learning Outcomes

This article explains the principal tools for measuring and monitoring portfolio risk in a CFA Level 3 context, with particular emphasis on value at risk (VaR), conditional value at risk (CVaR, or expected shortfall), and drawdown. It describes how each measure is defined, calculated, and expressed, and how the choice of confidence level and time horizon affects the numerical results. The article discusses the assumptions behind historical, parametric, and Monte Carlo VaR methods and highlights how departures from normality, such as skewness, kurtosis, and option positions, influence both VaR and CVaR estimates. It examines why CVaR is considered a more coherent risk measure, how it captures tail losses beyond the VaR threshold, and when exam questions are likely to prefer CVaR-based analysis. The article also analyses drawdown as a path-dependent risk metric, linking maximum drawdown to capital preservation, liquidity needs, and investor tolerance for losses. Finally, it compares the strengths and weaknesses of VaR, CVaR, and drawdown for portfolio risk reporting, stress testing, and performance evaluation, emphasising typical CFA examination traps, such as misinterpreting VaR statements or assuming that VaR and CVaR will be similar for portfolios with non-normal return distributions.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand how risk is measured and monitored across various portfolio contexts, with a focus on the following syllabus points:

- Calculating and interpreting value at risk (VaR) and conditional value at risk (CVaR, or expected shortfall)

- Explaining the differences and appropriate uses of VaR, CVaR/expected shortfall, and drawdown

- Describing the limitations and assumptions of common risk measures

- Using these risk metrics for portfolio performance and risk management

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the main difference between VaR and expected shortfall (CVaR)?

- Describe a practical scenario where drawdown risk is more informative than standard deviation.

- Name one major limitation of using VaR as a risk measure.

- True or false? CVaR is always less than or equal to VaR for the same confidence level.

Introduction

Effective investment risk management depends on reliable risk measurement and monitoring. CFA candidates must be familiar with three principal tools: value at risk (VaR), conditional value at risk (CVaR, also called expected shortfall), and drawdown. This article explains how each risk measure works, how they can be compared, and which practical applications and limitations you may encounter in the exam.

MEASURING RISK: OVERVIEW

Portfolio managers need to quantify the potential for losses. The most widely used risk measures—VaR, CVaR, and drawdown—help compare risk exposure across portfolios, communicate risk to stakeholders, and monitor for excessive risk taking.

The choice of risk measure affects risk reporting, investment decisions, and regulatory compliance. Each metric provides a different view and suits different investment contexts and asset classes.

Key Term: value at risk (VaR)

The estimated maximum expected loss on a portfolio over a specified time period at a given confidence level. Key Term: conditional value at risk (CVaR, expected shortfall)

The average portfolio loss in the tail beyond the VaR threshold at a given confidence level. Key Term: drawdown

The decline of a portfolio from a peak value to a subsequent low, typically measured as the maximum observed loss from a historical high.

VALUE AT RISK (VaR)

VaR is a standard risk metric that estimates the worst expected loss over a time frame for a given confidence level (e.g., 95%, 99%). The measure is expressed as a currency amount or a percentage of portfolio value. VaR provides a single number answer to the question: "How much could the portfolio lose in the worst X% of cases over Y period?"

Example: "The 1-day, 99% VaR for this portfolio is $1.2 million" means there is a 1% chance of losing more than $1.2 million in one day.

VaR can be calculated using different methods:

- Historical simulation: using empirical returns

- Variance-covariance (parametric): assuming normal or other distributions

- Monte Carlo simulation: generating many possible scenarios

Worked Example 1.1

Suppose a portfolio’s daily 99% VaR is $2 million. What does this number tell the investment committee?

Answer:

The committee should expect that, on average, losses greater than $2 million in one day will occur only 1% of the time (about 2 to 3 times per year if 250 trading days are assumed).Exam Warning: VaR does not indicate the size of losses greater than the VaR figure—it only identifies the minimum loss exceeded at a specific probability. Extreme tail losses can be much larger, so risk managers should not assume that VaR alone captures total risk.

CONDITIONAL VALUE AT RISK (CVaR/EXPECTED SHORTFALL)

CVaR (expected shortfall) provides additional information by estimating the average loss experienced if the loss is already beyond the VaR threshold. Essentially, it answers: "If we experience a loss worse than VaR, how bad could it be on average?"

CVaR is particularly useful for non-normal or fat-tailed return distributions, and is more coherent as a risk measure (meeting properties such as subadditivity).

CVaR is always equal to or greater than VaR at the same confidence level, except when returns are normally distributed, where they may be close.

Worked Example 1.2

A portfolio has a daily 99% VaR of $2 million and a CVaR of $3 million. What does this difference indicate?

Answer:

While the VaR shows that 1% of daily losses will exceed $2 million, those losses, on average, will be $3 million in those worst-case days. This highlights tail risk not captured by VaR alone.Revision Tip: When comparing portfolios, use CVaR rather than VaR if the return distributions are skewed, fat-tailed, or if the focus is on extreme losses.

DRAWDOWN AS A RISK MEASURE

Drawdown measures the reduction of portfolio value from its historical peak. Maximum drawdown over a sample period is especially relevant for assessing liquidity needs, regulatory compliance, and real-world loss experience. Investing stakeholders, including trustees, often care about largest historical losses rather than volatility alone.

Drawdown is typically expressed as a percentage. For example, a 30% drawdown means the portfolio value declined by 30% from its peak before recovering.

Drawdown is path-dependent and especially important for portfolios requiring capital preservation or regular withdrawals. Fund managers and committees often use drawdown limits to control risk.

Worked Example 1.3

If a fund peaked at $100 million, then fell to $68 million before recovering, what was the maximum drawdown?

Answer:

The maximum drawdown was 32%: ($100m - $68m)/$100m = 32%.

COMPARING RISK MEASURES AND LIMITATIONS

VaR estimation is classified into historical, parametric, and Monte Carlo approaches, distinguished by empirical-return, distributional, and simulation-based loss modeling.

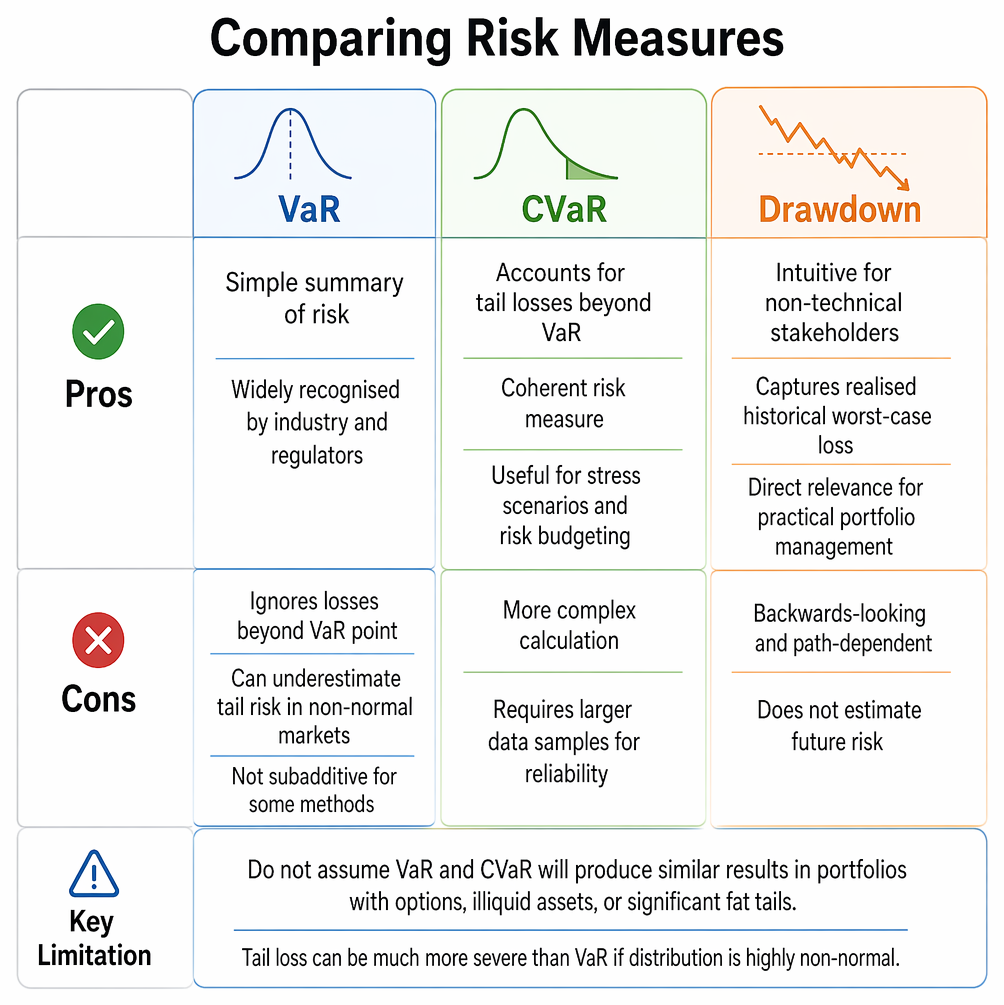

VaR

- Pros: Simple summary of risk; widely recognised by industry and regulators.

- Cons: Ignores losses beyond the VaR point; can underestimate tail risk in non-normal markets; not subadditive for some methods.

CVaR

- Pros: Accounts for tail losses beyond VaR; coherent risk measure; useful for stress scenarios and risk budgeting.

- Cons: More complex calculation; requires larger data samples for reliability.

Drawdown

- Pros: Intuitive for non-technical stakeholders; captures realised historical worst-case loss; direct relevance for practical portfolio management.

- Cons: Backwards-looking and path-dependent; does not estimate future risk.

Exam Warning

For CFA questions, do not assume VaR and CVaR will produce similar results in portfolios with options, illiquid assets, or significant fat tails. Tail loss can be much more severe than VaR if distribution is highly non-normal.

Summary

VaR, CVaR (expected shortfall) and drawdown are essential for measuring and monitoring investment risk. VaR focuses on the threshold loss at a given confidence level but ignores the severity of tail events. CVaR improves upon VaR by considering average losses in the tail, making it more informative for extreme risk analysis and risk capital planning. Drawdown connects directly to real, observed loss experience and is often used to set practical risk limits. Combine these tools for comprehensive risk assessment, and always interpret results with an understanding of their limitations.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and interpret value at risk (VaR), conditional value at risk (CVaR/expected shortfall), and drawdown

- Explain the differences and uses of VaR, CVaR, and drawdown measures

- Identify the practical limitations and assumptions behind each risk metric

- Calculate VaR, CVaR, and drawdown in simple portfolio contexts

- Recognise when each measure is most appropriate for exam questions and practical monitoring

Key Terms and Concepts

- value at risk (VaR)

- conditional value at risk (CVaR, expected shortfall)

- drawdown