Learning Outcomes

This article explains how liquidity needs and transaction costs shape both strategic and tactical asset allocation decisions for institutional and private investors. It clarifies the main sources of liquidity demand across different investor types, distinguishing predictable outflows such as spending policies and benefit payments from irregular or contingent cash requirements. The article evaluates how portfolio composition, market conditions, and investor-specific features translate these cash-flow demands into explicit liquidity constraints that limit allocations to illiquid assets and influence acceptable rebalancing policies. It analyzes explicit and implicit transaction costs, showing how commissions, taxes, bid–ask spreads, and market impact affect realised returns, optimal trading frequency, and the design of rebalancing bands. The discussion links these constraints directly to investment policy statement (IPS) construction, emphasizing how to set realistic allocation ranges, choose suitable investment vehicles, and preserve tactical flexibility under stress scenarios. Worked examples illustrate how to size liquidity buffers, judge when transaction costs may overwhelm expected alpha, and articulate these considerations clearly in a CFA Level 3 constructed-response answer.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand how liquidity and transaction cost constraints affect asset allocation decisions, with a focus on the following syllabus points:

- Evaluating the sources and drivers of portfolio liquidity needs in institutional and private wealth contexts

- Assessing the influence of transaction costs on long-term (strategic) and short-term (tactical) allocation choices

- Integrating constraints into the investment policy statement (IPS) and selecting appropriate investment vehicles

- Comparing portfolio solutions under varying liquidity and transaction cost environments

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What institutional factors cause liquidity to be a primary constraint in a strategic asset allocation?

- Why might increasing allocation to illiquid assets impair tactical asset allocation flexibility?

- How do explicit and implicit transaction costs differ, and why are both relevant for portfolio construction?

- What are the main ways an institutional investor can meet sudden large cash-flow demands?

Introduction

Liquidity requirements and transaction costs are key constraints shaping the construction and management of investment portfolios. For strategic (long-term, policy-driven) asset allocation, they influence asset class selection and permissible weight ranges. For tactical (short-term, opportunistic) allocation, they determine how quickly and efficiently a manager can respond to evolving market conditions. Optimal allocation strategy must balance the return potential of less-liquid instruments against the need for timely, cost-effective cash generation and portfolio adjustments.

Key Term: liquidity constraint

A limitation on portfolio composition or trading imposed by the need to generate cash efficiently, without incurring excessive loss or delay. Key Term: transaction cost

A measurable or implicit expense incurred when buying or selling portfolio assets, including commissions, market impact, bid-ask spreads, taxes, and opportunity costs.

LIQUIDITY AS A PORTFOLIO CONSTRAINT

Liquidity needs arise whenever a portfolio must provide cash for spending, rebalancing, liability payments, or opportunistic investments. The magnitude and predictability of these outflows determine the appropriate allocation to liquid assets and the risk that must be managed when adding illiquid investments.

Sources of Liquidity Need

- Defined Benefit (DB) Pension Plans: Benefit payments to retirees, possible lump-sum cash-outs, or regulatory requirements. Mature plans (with larger retiree populations) require higher regular cash distributions.

- Defined Contribution (DC) Plans: Participant transfers, in-service withdrawals, and rollovers require the portfolio to maintain a buffer of liquid assets.

- Endowments/Philanthropic Funds: Annual spending targets to support institutional goals; unexpected funding demands.

- Private Wealth Clients: Lifestyle spending, opportunistic purchases, or responses to unplanned events such as emergencies, major bills, or taxes.

- Sovereign Wealth Funds & Reserve Funds: Budget support or intervention after large macro shocks.

Factors Affecting Liquidity Constraints

- Portfolio Composition: Illiquid assets (private equity, real estate, infrastructure, direct lending) offer return and diversification, but cannot be readily sold at fair value in all market conditions.

- Allowance for Early Redemption: DC plans, mutual funds, and certain endowments may experience unpredictable participant redemptions.

- Concentration of Flows: Single large cash events (e.g., a pension buyout program or an institutional grant) may dwarf typical annual spending flows.

- Market Environment: Liquidity "dries up" in crisis periods, making even broadly traded assets hard to sell without deep discounts.

Worked Example 1.1

A university endowment targets a 5% annual spending rate but also faces a potential $20 million building expense within three years. Its current asset mix includes 45% equities, 35% bonds, and 20% private market alternatives. What is a suitable approach to structuring liquidity?

Answer:

The endowment should maintain sufficient short- and intermediate-duration fixed income and public equities to easily fund the annual spending and the potential building expense, even under unfavorable market scenarios. Limiting the illiquid allocation at or below 20% supports flexibility. Scenario analysis stress-testing can gauge how quickly assets could be liquidated in extreme conditions.

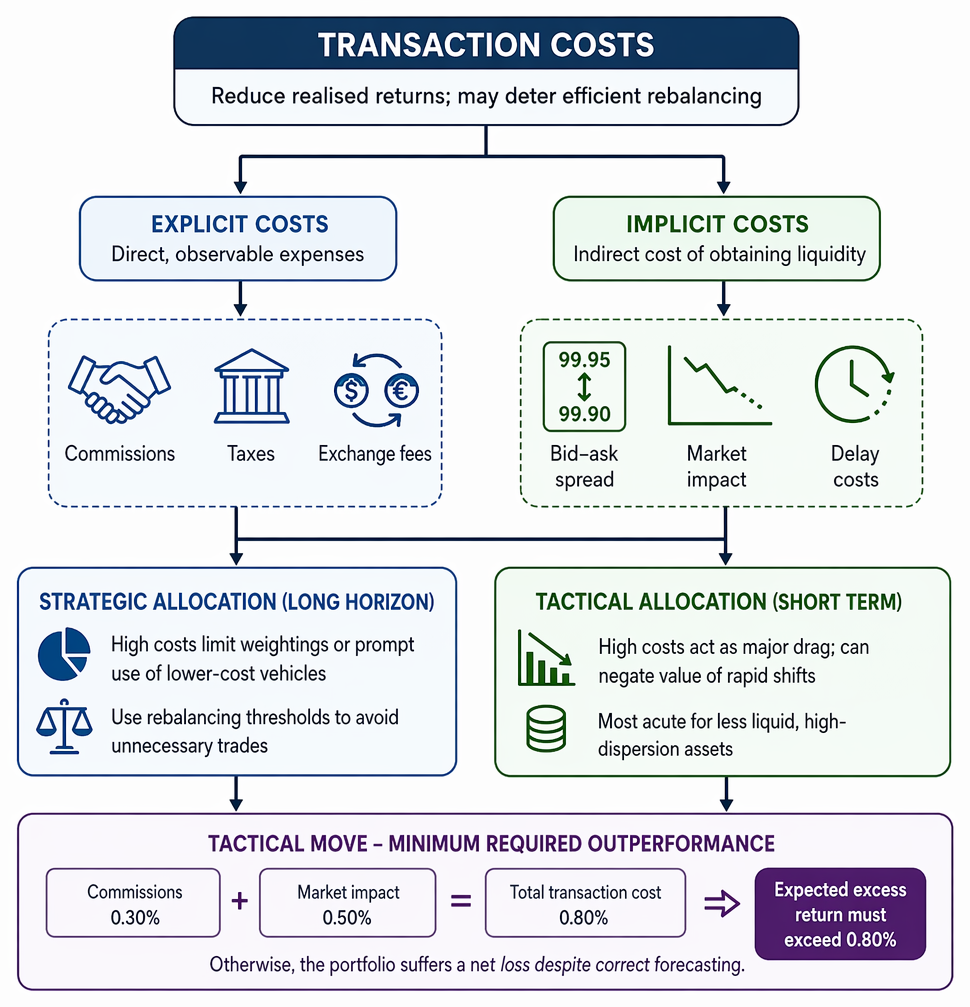

TRANSACTION COSTS IN STRATEGIC & TACTICAL ALLOCATION

Transaction costs reduce realised returns and may deter efficient rebalancing. These costs have two main forms:

Liquidity management framework links cash-flow analysis, portfolio liquidity, buffer sizing, funding and rebalancing policies, and strategic allocation flexibility.

- Explicit costs: Readily measured expenses such as commissions, taxes, and exchange fees.

- Implicit costs: Price slippage, bid-ask spreads, and market impact—the degree to which large trades move the asset price.

Key Term: explicit transaction cost

A direct, observable cost paid to a broker, exchange, or government when executing a trade. Key Term: implicit transaction cost

An indirect or non-observable cost associated with obtaining liquidity—primarily bid-ask spread, price impact, and delay costs.

Strategic Allocation and Transaction Costs

In strategic (long horizon) allocations, high transaction costs in a particular asset class (e.g., emerging market equities, private market assets) may limit its weighting or prompt use of lower-cost vehicles (e.g., index funds or ETFs, futures overlays for rebalancing). When designing rebalancing rules, transaction costs often motivate the use of thresholds (e.g., only rebalance when weights deviate by a set percentage) rather than automatic periodic rebalancing, to avoid unnecessary trades.

Tactical Allocation and Trading Costs

In tactical (short-term) allocation, high transaction costs act as a major drag, often negating the value of rapid strategy shifts. This is especially acute for less liquid, high-dispersion assets (such as small- or micro-cap stocks or some alternatives), where trading volume is less than the size of the intended trade.

Worked Example 1.2

A pension fund seeks to shift 5% of its $2bn portfolio from government bonds to emerging market equities, which incur 0.30% in commissions plus 0.50% market impact for this trade size. What is the minimum required outperformance to justify this tactical move?

Answer:

The trade incurs approximately 0.80% in total transaction costs (0.30% + 0.50%). For a tactical shift to add value, the expected excess return must exceed this hurdle, otherwise the portfolio suffers a net loss despite correct forecasting.Exam Warning: Transaction costs can be asymmetric—rebalancing into illiquid or stress-affected assets may have sharply higher implicit costs during market downturns. For Level 3 questions, always discuss both explicit and implicit cost implications, and reflect stress test scenarios where relevant.

PRACTICAL APPROACHES TO MANAGING CONSTRAINTS

Institutional investors and wealth managers use several techniques to address liquidity and transaction cost constraints:

- Liquidity Bucketing: Group assets by time-to-liquidation (e.g., daily, monthly, annual); ensure cash flow demands can be met from the most liquid buckets under stress.

- Limit on Illiquid Allocation: Set a percentage cap on private equity, property, infrastructure, or similar investments. Review alignment with projected outflow peaks.

- Contingency Planning: For expected but unpredictable events (e.g., early retirement programs, buyout offers, capital calls), maintain cash and lines of credit, or use public market overlays to rapidly raise cash.

- Rebalancing Policy: Combine periodic reviews with threshold triggers and explicit transaction cost modeling to determine optimal bands.

Worked Example 1.3

A philanthropic fund has an annual spending policy set at 6% of NAV and holds 25% in alternatives. During a financial crisis, the public market values halve, but the alternatives revalue slowly. What are two practical risks if the philanthropic fund must meet its entire spending requirement from public assets?

Answer:

First, selling only public assets in a downturn can force the sale of equities or bonds at depressed prices, locking in large losses. Second, apparent illiquidity in alternatives may mask real shortfall risk, and a forced sale on secondary markets would result in steep discounts and impair long-term capital.

IMPACT ON ASSET ALLOCATION POLICY AND IMPLEMENTATION

Liquidity and transaction cost constraints directly influence the investment policy statement (IPS) and practical implementation:

- Asset Allocation Limits: Specify permissible ranges for illiquid investments based on liability forecasts, spending policy, and stress-test results.

- Investment Vehicle Choice: Prefer vehicles with lower transaction costs where feasible (e.g., index funds rather than traditional mutual funds, or using derivatives overlays for short-term exposure shifts).

- Tactical Leeway: For mandates allowing frequent tactical shifts, limit illiquids accordingly and ensure transaction cost modeling factors into both policy design and performance attribution.

Revision Tip: Use simple cash-flow projections and transaction cost estimates to illustrate your answers—CFA Level 3 will often test awareness of how these numerical factors drive policy.

Summary

Liquidity and transaction cost constraints play a fundamental role in both strategic and tactical asset allocation. Efficient portfolios require not just careful modeling of expected return and volatility, but explicit recognition of the real-world hurdles posed by cash-flow demands and trading costs. Strong portfolio policies align the asset mix, rebalancing approach, and vehicle selection with forecasted liquidity needs and expected trading costs, maintaining sufficient flexibility for both normal and stress market scenarios.

Key Point Checklist

This article has covered the following key knowledge points:

- The definition and importance of liquidity and transaction cost constraints in allocation

- Main drivers of portfolio liquidity needs across institutional and private settings

- The difference between explicit and implicit transaction costs, and their practical impact

- How strategic and tactical asset allocation integrate liquidity and cost considerations

- Portfolio tools and policies for efficiently managing these constraints

Key Terms and Concepts

- liquidity constraint

- transaction cost

- explicit transaction cost

- implicit transaction cost