Learning Outcomes

This article explains strategic and tactical asset allocation, including:

- distinguishing clearly between strategic (policy) and tactical asset allocation in terms of horizon, decision drivers, and governance expectations.

- describing how long-term policy portfolios are constructed from IPS objectives, risk tolerance, constraints, and capital market assumptions for different mandate types.

- linking each asset class selection, benchmark, and target weight back to explicit IPS statements for institutional and private client cases.

- designing policy ranges around strategic weights and articulating when breaches, market moves, or client changes require formal portfolio review.

- explaining the objectives, mechanics, and trade-offs of systematic rebalancing strategies versus discretionary, tolerance-band, or calendar-based rebalancing rules.

- evaluating the role and limits of tactical asset allocation as an active risk decision relative to the policy benchmark and risk budget.

- assessing when changes in funded status, risk capacity, market conditions, or investment beliefs justify revising the strategic policy portfolio.

- applying these concepts to exam-style scenarios that require recommending, justifying, or critiquing asset allocation and rebalancing decisions under a given IPS.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand policy portfolio design and its alignment with IPS objectives and constraints, with a focus on the following syllabus points:

- Define strategic and tactical asset allocation and distinguish between them for exam scenarios

- Illustrate how long-term policy portfolios (strategic allocation) are constructed and their linkage to investment policy statements

- Explain the rationale for fixed allocation ranges and rebalancing around the policy weights

- Evaluate how tactical asset allocation operates as a short-term deviation from policy

- Outline best-practice alignment of asset allocation process within the IPS framework

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the primary difference between a policy portfolio (strategic allocation) and a tactical asset allocation?

- List three essential elements that must be aligned between the IPS and the long-term policy portfolio for a DB pension plan.

- In which scenarios should an institutional investor update its policy portfolio weights?

- Why is rebalancing around policy weights important for risk management?

Introduction

Strategic asset allocation (policy portfolio selection) sets the long-term direction for portfolio construction, aiming to meet client objectives within stated IPS constraints. The policy portfolio represents an investor’s or institution’s optimal allocation based on expected returns, risk preferences, constraints, and beliefs. Tactical asset allocation (TAA) allows the manager to take short-term deviations from policy weights to exploit perceived opportunities or manage risks, but the IPS framework and strategic allocation remain the central reference point for discipline and accountability.

Key Term: strategic asset allocation

The long-term allocation to eligible asset classes that is expected to achieve desired objectives subject to the investor's constraints, as stated in the IPS. Key Term: tactical asset allocation (TAA)

Short-term, intentional deviations from the strategic asset allocation, made to capitalize on perceived market opportunities or to manage risks outside strategic assumptions. Key Term: policy portfolio

The explicitly defined set of long-term target weights assigned to eligible asset classes, established to provide optimal asset mix given client goals, risk tolerance, and constraints. Key Term: Investment Policy Statement (IPS)

A formal written document describing an investor’s objectives, risk tolerance, and constraints, which serves as the basis for developing, monitoring, and reviewing the portfolio and allocation process.

STRATEGIC AND TACTICAL ASSET ALLOCATION: FUNDAMENTALS

What Is the Strategic Asset Allocation (Policy Portfolio)

The policy portfolio embodies strategic asset allocation, setting fixed long-term weights for each eligible asset class. These targets are determined using the investor’s objectives, risk tolerance, constraints, capital market assumptions, and correlations between asset classes.

Strategic allocation is designed to be stable and is only revisited after material changes to the investor’s profile, market environment, or investment beliefs. The main justification for setting target weights is to maintain alignment between risk/return expectations and goals over time, and to avoid behavioural mistakes that may arise during market volatility.

The Linkage between Policy Portfolio and the IPS

The IPS and the policy portfolio are intrinsically linked. The IPS articulates the overarching mission, required return, risk appetite, liquidity needs, time horizon, and constraints. Strategic asset allocation is the quantitative translation of these requirements into actionable portfolio design. Asset class inclusion, eligible ranges, and targets are all justified by direct reference to the IPS.

Key Term: rebalancing

The process of realigning portfolio allocations with target policy weights to maintain intended exposures and risk characteristics in line with the policy portfolio.

Why Is Strategic Asset Allocation (Policy Portfolio) So Important

Evidence shows that long-term asset allocation decisions explain the majority of portfolio return risk and overall performance. The policy portfolio is designed:

- To achieve portfolio return within an acceptable risk envelope

- To control exposure to systematic risk factors over time

- To enable accountability, by allowing for assessment of management decisions versus a clear benchmark

HOW POLICY PORTFOLIOS ARE DESIGNED

Strategic asset allocation process translating IPS objectives, eligible asset classes, and capital market assumptions into approved long-term target weights and ranges.

Core Steps in Policy Portfolio Construction

- Translate the long-term required return, risk appetite, and constraints from the IPS into a quantitative target.

- Define the eligible asset classes (based on liquidity, investability, and unique needs from the IPS).

- Estimate expected risk, return, and correlations for asset classes (drawing from capital market assumptions).

- Use optimisation methods (mean–variance, Black-Litterman, or risk-factor-based approaches) to derive long-run efficient allocations.

- Review for qualitative consistency with investor beliefs or unique objectives, then confirm with governing board or ultimate client.

- Document policy weights and permissible ranges in the IPS appendix or investment guidelines.

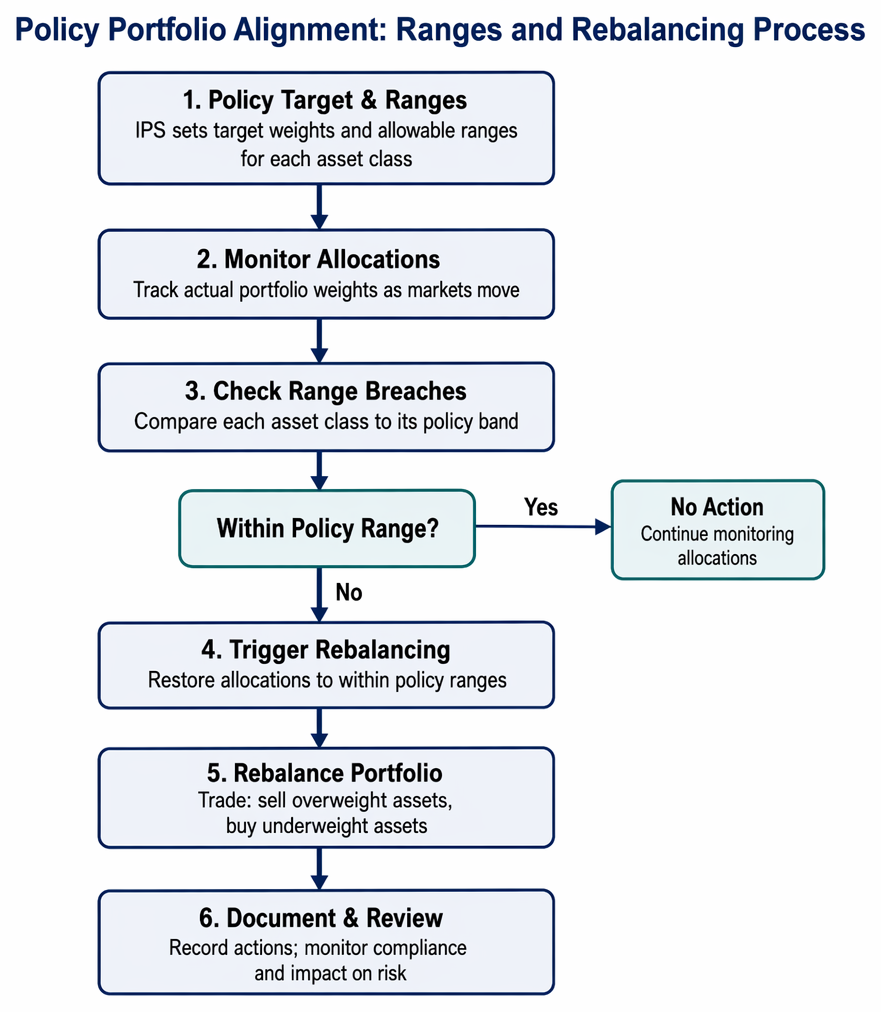

Maintaining Policy Portfolio Alignment: Ranges and Rebalancing

Because asset returns fluctuate, portfolio allocations will drift over time. The IPS or supporting guidelines should set explicit ranges for each asset class. If an allocation breaches its range, rebalancing is triggered to restore weights to within policy bands. This process is central to disciplined risk control and performance attribution.

Tactical Asset Allocation (TAA): Role and Limits

TAA is permitted for some mandates, allowing short-horizon deviations in weights to reflect current market opportunities or manage short-term risks. The IPS or investment guidelines must specify:

- Permitted deviation bands (e.g., ±5% from policy weight)

- Risk or allocation limits on the cumulative effects of TAA

- The process for review and restoration to policy weights after the TAA period ends

TAA is a value-added and risk control tool, but excessive TAA can undermine consistency with the stated long-term strategy and should always be monitored.

Worked Example 1.1

A university endowment has a policy portfolio of 50% global equities, 40% fixed income, 10% private assets, with ±5% allocation ranges. After a sharp equity rally, equities now constitute 58% of assets, fixed income 34%, private assets 8%. What must the investment committee do?

Answer:

The equity allocation now exceeds the maximum permitted range (55%). The investment committee should trigger a rebalancing process, selling equities and redeploying to fixed income and private assets, to restore allocations within policy limits. This preserves intended risk exposures and adherence to long-term objectives as set out in the IPS.

Worked Example 1.2

A corporate DB plan’s strategic policy allocates 60% to equities (with domestic and international splits), 30% core bonds, 10% alternatives. The IPS mandates a review if the funded status falls below 90% or if plan contributions become unsustainable. During a market downturn, funding drops to 85%. What action is required?

Answer:

The investment committee must consider revising the policy portfolio weights and asset class risk exposures. The IPS requires action if funding falls below threshold, so de-risking (e.g., reducing equity and raising fixed income/LDI allocation) or a special review of capital market assumptions might be necessary.

Alignment with Governance and Review

For institutional investors, board or investment committee oversight ensures the policy portfolio remains consistent with the mission. The IPS mandates periodic (usually annual) review of policy benchmarks and allocation logic, but changes are only made after thorough analysis showing a shift in goals, constraints, or asset class expectations.

Exam Warning: Deviating from the policy portfolio or IPS constraints without proper approval or process is a common exam error and may result in breaches of fiduciary duty in CFA exam scenarios.

Revision Tip: Always link each recommended policy portfolio design or revision back to the specific investor objective, risk, and constraint statements in the IPS.

Summary

The policy portfolio is the anchor of portfolio management, operationalising the IPS by specifying long-term asset class weights aligned with investor goals, risk, and constraints. Tactical asset allocation is permitted within specified ranges, but major portfolio design changes are triggered only by material shifts in the investor IPS or in market assumptions. Periodic rebalancing enforces discipline and risk management.

Key Point Checklist

This article has covered the following key knowledge points:

- Define strategic and tactical asset allocation, and distinguish between them for CFA exam context.

- Describe policy portfolio construction process and its alignment with the IPS (objectives, constraints, ranges).

- Recognise the key role of rebalancing in restoring strategic allocations and managing risk.

- Identify requirements for linking TAA decisions to the IPS and limiting their scope.

- Explain policy portfolio review triggers and the importance of ongoing alignment to client mission/constraints.

Key Terms and Concepts

- strategic asset allocation

- tactical asset allocation (TAA)

- policy portfolio

- Investment Policy Statement (IPS)

- rebalancing