Learning Outcomes

This article explains tactical asset allocation and tactical tilt implementation and governance, including:

- distinguishing strategic from tactical asset allocation in terms of objectives, time horizon, decision frequency, and sources of value added;

- describing alternative approaches for implementing tactical tilts, such as discretionary macro views versus systematic model-driven processes, and the use of cash securities and derivatives;

- outlining key governance structures, including investment policy statements, permitted ranges, risk budgets, delegation of authority, and documentation requirements;

- evaluating risk controls for tactical activity, covering tracking error limits, drawdown tolerances, leverage and liquidity management, counterparty exposure, and scenario or stress testing;

- interpreting performance and risk attribution for tactical tilts relative to the strategic asset allocation, and explaining how monitoring reports support oversight and escalation;

- identifying common pitfalls of poorly governed tactical asset allocation, such as style drift, persistent range breaches, excessive turnover, and inadequate reporting, and explaining appropriate remedial actions;

- applying these concepts to typical CFA Level 3 exam vignettes by diagnosing governance weaknesses, recommending process improvements, and justifying or criticising specific tactical decisions using appropriate terminology.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand how tactical asset allocation decisions are made, implemented, and controlled in the context of overall portfolio management, with a focus on the following syllabus points:

Tactical tilt process links signal generation, risk-budget approval, instrument selection, trade execution, and tracking-error monitoring to the policy portfolio.

- Differentiating between strategic and tactical asset allocation, including their objectives and typical horizons

- Describing methodologies for implementing tactical tilts, such as discretionary and systematic approaches

- Outlining the governance framework required for monitoring, controlling, and documenting tactical allocation activities

- Recognising the main governance roles: oversight, delegation, risk management, and reporting of tactical asset allocation

- Evaluating risk and performance attribution for tactical tilts relative to a strategic policy portfolio

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which statement best distinguishes strategic asset allocation (SAA) from tactical asset allocation (TAA)?

- a) SAA is based on short-term forecasts; TAA is based only on long-term expected returns.

- b) SAA sets the long-term policy mix; TAA makes temporary deviations from that mix to add active return.

- c) SAA focuses on security selection; TAA focuses on manager selection.

- d) SAA is implemented only with derivatives; TAA uses only cash securities.

-

Why should an investment governance policy explicitly define risk budgets and range limits for tactical tilts?

- a) To maximise turnover and ensure all tactical views are implemented.

- b) To allow the CIO to ignore the strategic allocation when strong views arise.

- c) To constrain active risk, align tactical activity with risk tolerance, and support monitoring and escalation.

- d) To ensure tactical positions are always fully hedged and market neutral.

Introduction

Asset allocation remains the central driver of long-term portfolio outcomes. While strategic asset allocation defines the target weights for each asset class based on long-term objectives and constraints, tactical asset allocation seeks to adjust exposures opportunistically, aiming to exploit shorter-term inefficiencies, macro trends, or valuation misalignments. Effective implementation of tactical tilts demands robust governance to ensure accountability, transparency, and alignment with the portfolio’s overall mandate.

Key Term: strategic asset allocation

The process of setting long-term target weights for portfolio asset classes, creating the policy portfolio against which any tactical deviations are measured. Key Term: tactical asset allocation

The active management process of making shorter-term adjustments (tilts) to asset class or factor weights around the strategic allocation, aiming to benefit from perceived market opportunities or manage near-term risks. Key Term: policy portfolio

A benchmark asset mix derived from the strategic asset allocation that represents the investor’s long-term risk–return position and is used to evaluate all active decisions, including tactical tilts. Key Term: tactical tilt governance

The structures, controls, and policies that guide, monitor, and limit tactical allocation activity so that it remains consistent with fiduciary duties, the investment policy statement, and the client’s risk tolerance.

In institutional practice, tactical asset allocation can be material. A few percentage points of overweight or underweight in equities, duration, or credit risk can dominate the active return of a diversified portfolio. The Level 3 curriculum emphasises not only what tilts to take, but how they are sized, implemented, monitored, and governed.

Distinguishing Strategic and Tactical Asset Allocation

Strategic asset allocation (SAA) defines the long-term policy mix, based on the investor’s objectives, liabilities, and constraints. It:

- targets long-run risk and return over multi-year horizons, often decades for pensions or endowments;

- is reviewed infrequently (e.g., annually or when circumstances change materially);

- is usually based on long-horizon capital market expectations and liability characteristics;

- is implemented with tight rebalancing rules to keep the portfolio close to target weights.

Tactical asset allocation (TAA), by contrast, represents deliberate, temporary moves away from the SAA to exploit perceived shorter-term market opportunities. TAA:

- seeks incremental active return (alpha) or risk reduction over horizons typically up to 12–36 months;

- is based on nearer-term signals (macro, valuation, sentiment, technicals);

- changes more frequently as those signals change;

- increases active risk relative to the policy portfolio and therefore must be bounded by explicit risk budgets.

The business-cycle material in the curriculum reinforces that short- to medium-horizon forecasts are noisy. Identifying the precise timing of turning points between expansion, slowdown, and contraction is difficult. This reinforces why tactical tilts should be modest, risk-controlled, and evaluated over multiple decisions rather than judged on a single call.

Exam Warning: Avoid confusing the time horizon and objectives of SAA and TAA:

- SAA sets structural risk/reward over multiple years and is typically linked to required return objectives or funding ratios.

- TAA targets temporary alpha or risk management over horizons typically not exceeding 12–36 months.

In an essay question, if you justify a multi-year, liability-driven change (e.g., moving from 60/40 to 40/60 because of ageing demographics) using “tactical” language, you are likely to lose credit. Label changes correctly as strategic or tactical and link them to the appropriate horizon.

Tactical Tilts: Approaches and Implementation

Tactical tilts can be implemented through different decision-making approaches and across various levels of granularity.

-

Discretionary tactical asset allocation: Relies on qualitative judgement, such as committee forecasts or macroeconomic views, to alter allocations. Inputs may include business-cycle phase, central bank policy, valuation spreads, and geopolitical risk. Discretionary processes offer flexibility but are vulnerable to behavioural biases (overconfidence, herding, loss aversion).

-

Systematic tactical asset allocation: Uses quantitative models, often factor- or signal-based, to generate and size tactical tilts. Signals can include valuation (e.g., equity risk premium), momentum, carry, or macro indicators. Systematic processes can reduce behavioural bias and enforce discipline, but they embed model risk and may fail when regimes change.

In practice, many institutions use a hybrid approach: models generate baseline signals and recommended tilts; an investment committee applies judgement to accept, resize, or override them within defined governance constraints.

TAA decisions typically target broad asset classes (equities vs bonds, credit vs government, nominal vs inflation-linked bonds), but may also focus on:

- regions (e.g., overweight emerging markets vs developed markets);

- styles (e.g., tilt to value vs growth, small vs large cap);

- sectors or industries (e.g., overweight defensives late in the cycle);

- risk premia (e.g., equity beta, duration, credit spread, volatility).

When TAA is implemented centrally (e.g., by a CIO or overlay manager), it should be coordinated with mandate managers to avoid unintended bets (such as simultaneously overweighting and underweighting the same region across different mandates).

Tactical Tilts: Sizing, Horizon, and Risk Budgeting

Key Term: risk budget

The amount of active risk, often defined as tracking error or drawdown tolerance, that an investor is willing to allocate to active decisions such as tactical tilts. Key Term: active risk (tracking error)

The standard deviation of portfolio returns relative to the policy portfolio or benchmark over time, used to measure and constrain the risk introduced by tactical and other active decisions.

Sound tactical processes start from a risk budget, not a return target. A board or investment committee may, for example, permit:

- an overall ex ante tracking error of 3% relative to the policy portfolio;

- of which up to 1% may be consumed by TAA, with the rest allocated to security selection or active managers.

Tactical tilt sizing then becomes a risk-allocation problem:

- A 5% equity overweight in a volatile environment might consume most of a 1% TAA risk budget.

- Several smaller tilts (e.g., 2% equity overweight, 1% credit spread increase, 0.5 years duration underweight) may together use the budget.

The planning horizon for a tilt should be explicitly linked to the driving signal. Business-cycle-based tilts are often held for 1–3 years, whereas shorter-term technical signals may justify tilts of only a few months. Governance should require a review date and exit criteria for each tilt (e.g., when valuation gap closes, signal reverses, or time limit is reached).

Worked Example 1.1

Suppose a balanced fund's SAA is 60% equity and 40% bonds. The investment team forecasts a short-term equity rally and shifts to 65% equity, 35% bonds for 9 months. Identify the strategic and tactical allocations.

Answer:

The SAA remains 60/40; that policy mix has not changed. The temporary 5% overweight to equities (65/35 actual vs 60/40 policy) is a tactical tilt designed to capture anticipated equity outperformance over the 9‑month horizon. Once the view expires or risk limits are hit, the portfolio should be rebalanced back toward the 60/40 SAA.

Implementation Controls and Practical Considerations

All tactical tilts must be transacted with reference to clear, pre-defined ranges. For example, an IPS may allow plus/minus 5% tactical tilts on equities relative to SAA. Tilts can be executed using:

-

Cash securities: Buying or selling the cash instruments (e.g., equities, bonds). This is simple and transparent but may entail higher transaction costs, capital charges (for institutions), and slower implementation.

-

Derivatives: Futures, total return swaps, options, or ETFs can adjust exposures quickly with limited capital outlay, making them well-suited to short-horizon tilts and overlays.

When using derivatives, governance must address additional dimensions:

Key Term: leverage

The use of borrowed funds or derivatives to increase exposure beyond the portfolio’s net asset value, magnifying both gains and losses. Key Term: liquidity risk

The risk that positions cannot be transacted quickly, in the required size, and at reasonable prices, which becomes critical when tactical tilts need to be unwound. Key Term: counterparty risk

The risk that the other party to a derivatives or securities-lending transaction fails to meet contractual obligations, causing losses or delays.

Key controls when tilts are implemented via derivatives include:

- monitoring gearing (effective exposure) versus net asset value;

- managing margin and collateral to avoid forced deleveraging;

- diversifying and monitoring counterparties, with limits per dealer;

- understanding basis risk (e.g., equity futures on an index vs a portfolio that only partially overlaps that index).

Tactical tilts should also be sized within agreed risk budgets. Typical controls include:

- daily or weekly reporting against allocation ranges and risk budgets;

- monitoring ex ante and ex post tracking error attributable to TAA;

- monthly or quarterly committee review of all active tilts and their rationales.

Tactical changes must be distinct from rebalancing. Rebalancing is the rule-based discipline of returning portfolio weights toward SAA when market moves alone cause drift.

Key Term: rebalancing policy

Pre-defined rules for returning portfolio weights to strategic targets or tolerance bands, often time-based or threshold-based, helping distinguish systematic maintenance of SAA from discretionary tactical tilts.

An IPS might specify:

- threshold-based rebalancing (e.g., rebalance when any asset class deviates more than ±3% from target), and

- additional discretionary TAA ranges (e.g., CIO can tilt equities ±5% within board-approved risk budgets).

Worked Example 1.2

A pension fund is allowed TAA tilts of ±4% around its 55/35/10 (equity/bonds/alternatives) SAA. The CIO wants to add a 3% overweight to global equities after a market correction. What is the permitted range and is this tactical tilt permissible?

Answer:

The equity allocation can range from 51% to 59% under policy (55% ± 4%). Moving from 55% to 58% equities is a 3% overweight, which lies within the permitted tactical band. Assuming risk budgets and other constraints (e.g., tracking error limits) are respected, the tilt is permissible under the IPS.

Risk Controls for Tactical Activity

Tactical activity introduces additional risks relative to a pure SAA portfolio and therefore requires explicit risk controls.

Key Term: drawdown

The peak-to-trough decline in portfolio value over a specified period, often expressed as a percentage, used as a risk measure and to trigger review or de‑risking. Key Term: stress testing

Scenario analysis that evaluates portfolio performance under extreme but plausible market conditions, used to assess the robustness of tactical tilts. Key Term: information ratio

A measure of risk-adjusted active performance, defined as average active return divided by active risk (tracking error), commonly used to evaluate tactical allocation skill.

Key tactical risk controls typically include:

-

Tracking error limits: Define how much active risk TAA may contribute (e.g., TAA TE ≤ 1% within a total TE limit of 3%). Both ex ante (model-based) and ex post (realised) TE should be monitored.

-

Drawdown and stop-loss rules: For example, close or reduce a tilt if it loses more than 1% relative to the SAA over a given horizon, or if portfolio drawdown exceeds a threshold (e.g., 10%).

-

Leverage limits: Caps on gross and net exposures (e.g., gross exposure ≤ 120% of NAV) and on notional derivative exposures by asset class.

-

Liquidity and concentration limits: Minimum proportion of the portfolio in readily marketable instruments and caps on exposures to illiquid assets, especially for short-horizon tactical positions.

-

Counterparty limits: Maximum exposure to any single derivatives counterparty, with periodic review of creditworthiness.

-

Stress testing and scenario analysis: Assess how current tactical tilts would perform under adverse scenarios (e.g., rapid rate hikes, equity crashes, credit spread blowouts). For banks and insurers, regulators explicitly require such tests; asset owners increasingly expect the same standard.

Worked Example 1.3

A university endowment committee delegates tactical tilts to its internal CIO with a 2% tracking error budget around the SAA in equities and fixed income, plus full documentation. The CIO decides to tactically overweight fixed income by 3% using a derivatives overlay that, according to the risk system, increases expected TE by 1.8%. What governance control is most at risk?

Answer:

The CIO has effectively used 1.8% of the 2% TE budget with a single tilt. While the 3% overweight may be within allocation ranges, it nearly exhausts the delegated risk budget. The primary governance issue is the potential breach of the tracking error (risk) budget and the lack of diversification across multiple tilts. The CIO should either seek committee approval to expand the risk budget or resize the tilt to keep expected TE comfortably within 2%.Revision Tip: In exam answers, reference practical governance measures such as:

- IPS-mandated tactical ranges and tracking error budgets;

- the frequency of tilt review and stress testing;

- requirements for written rationales, expected horizon, and exit conditions for each tilt.

Simply stating “governance is weak” is not sufficient; specify which control is missing or breached and how to improve it.

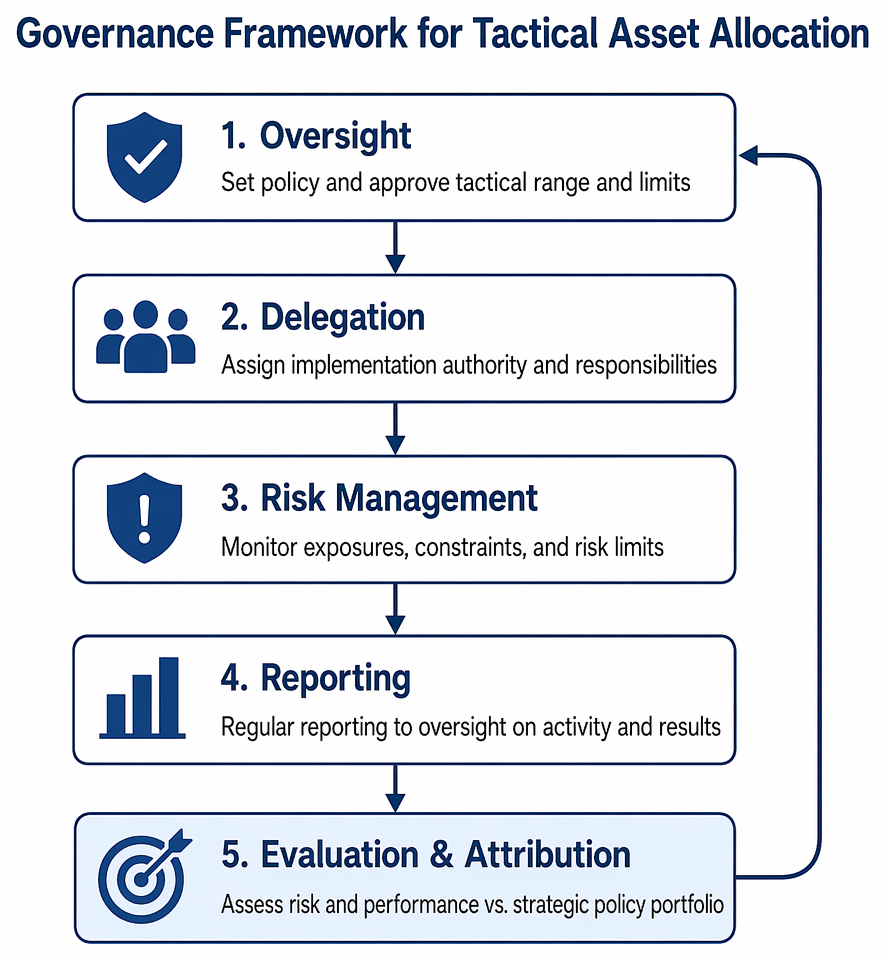

Governance of Tactical Tilts: Oversight and Process

Sound tactical tilt governance encompasses several layers, from policy design to day-to-day execution.

At the policy level, the IPS or governance manual should:

- explicitly state whether TAA is permitted and its role (return-seeking vs risk management);

- set permitted allocation ranges around the SAA and, where used, explicit risk budgets for TAA (e.g., TE limits);

- define the expected holding horizon for tilts and under what conditions they may be renewed or extended;

- describe the rebalancing policy and how it interacts with tactical decisions.

The Level 3 private wealth readings illustrate similar concepts: an IPS often has sections on Discretionary Authority, Rebalancing, Tactical Changes, and Implementation. Those same headings can structure governance for institutional TAA.

At the delegation and oversight level, governance should clarify:

- which body sets strategic allocation and approves the overall TAA framework (e.g., board, investment committee);

- who has authority to implement tilts (CIO, internal team, external overlay manager) and up to what limits;

- when committee approval is required (e.g., tilts that exceed a specified size, risk, or move outside standard ranges);

- the role of independent risk management and compliance in pre‑trade checks and post‑trade monitoring.

Banks and insurers provide a useful analogy: they use asset–liability management committees (ALM committees) to set risk appetites, approve strategies, and monitor compliance. For TAA, an analogous investment or risk committee should:

- review reports on active tilts, performance attribution, risk metrics, and breaches;

- ensure consistency with regulatory constraints, funding requirements, and rating agency expectations where relevant.

At the process and documentation level, good practice requires:

- an investment note for each material tilt summarising thesis, sizing, instruments, horizon, risk impact, and exit plan;

- a log of decisions, including who approved and when, supporting after-action review;

- records sufficient to comply with the CFA Institute Standards on diligence, reasonable basis, and record retention.

Clear governance not only protects clients but also protects investment professionals: decisions that are properly authorised, documented, and monitored are easier to defend when outcomes are unfavourable but within the agreed risk framework.

Worked Example 1.4

A family office IPS permits the CIO to implement equity tilts of up to ±5% around the SAA, provided that ex ante TAA tracking error does not exceed 1.5%. The CIO believes equities are attractive and proposes a +4% equity overweight and a +2% high-yield bond overweight, which together raise expected TE by 2.0%. What should the oversight committee require?

Answer:

The proposed tilts stay within the ±5% allocation range but breach the 1.5% tracking error limit. The committee should insist on adherence to the risk budget and require one or more of the following:

- reduce the size of one or both tilts so expected TE ≤ 1.5%;

- replace one tilt with a lower-volatility expression (e.g., equity sector rotation rather than broad beta); or

- explicitly revise the IPS to increase the TAA risk budget, if justified by the client’s risk tolerance. Implementing the full proposal without addressing the TE breach would represent weak governance and poor risk control.

Common Risks and Mistakes

Tactical asset allocation exposes the portfolio to risks not captured solely by long-run SAA. Common pitfalls of poorly governed tactical activity include:

-

Overconfidence and mis-forecasting: Strong views about business-cycle timing or market direction that prove incorrect, producing negative alpha.

-

Excessive tilts relative to risk tolerance: Violating risk budgets or permitted ranges, leading to unintended volatility or large drawdowns.

-

Style drift: Tactical decisions that systematically change the portfolio’s risk profile (e.g., a “balanced” mandate behaving like an aggressive equity portfolio) without explicit approval.

-

Persistent range breaches and slow remediation: Positions remain outside IPS bands for extended periods without timely rebalance or formal exception approval.

-

Excessive turnover and transaction costs: Frequent small tilts that do not clear a minimum implementation hurdle after costs and taxes.

-

Weak documentation and incomplete audit trail: Rationales not recorded, making it difficult to review decisions, demonstrate diligence, or satisfy regulators and auditors.

-

Policy drift: Failure to rebalance back to SAA at the end of the tactical view horizon, gradually transforming tactical tilts into de facto strategic changes.

Regular review by the governing body can guard against these risks by enforcing policy discipline, requesting explanations for underperformance or breaches, and commissioning periodic audits of adherence to the TAA framework.

Exam Warning 2

Delegation of tactical tilt authority without precise range limits, risk metrics, or periodic review increases the risk of style drift, excessive risk, breaches of client mandate, and potential regulatory or fiduciary violations. In a vignette, you should flag such gaps explicitly and recommend concrete remedies (e.g., add a TE limit, formalise drawdown triggers, require quarterly TAA review).

Assessing Success and Monitoring Performance

Tactical tilts must be assessed on both performance and risk dimensions:

-

Performance relative to the policy portfolio: Evaluate whether TAA has delivered positive active return versus the SAA over appropriate horizons (multiple years and multiple decisions). Use contribution analysis to isolate the allocation effect from security selection.

-

Risk taken to achieve that performance: Examine realised tracking error, volatility, and drawdowns attributable to TAA decisions. A high active return with disproportionate risk may be inconsistent with the investor’s risk appetite.

Monitoring frameworks should include:

-

Performance attribution: Decompose total active return into components such as:

- strategic allocation changes (if any);

- tactical allocation (asset class, region, factor tilts);

- security selection and manager selection.

Asset allocation attribution (e.g., Brinson-style) is particularly suited to evaluating TAA skill: the allocation effect across asset classes indicates whether overweights and underweights added value.

-

Risk attribution: Attribute tracking error and other risk measures to sources such as equity beta, duration, credit spreads, currency exposure, and specific tilts. This ensures TAA is not inadvertently assuming undesirable factor risks.

-

Information ratio analysis: Calculate the information ratio for TAA (TAA active return divided by TAA active risk). A persistently negative or low IR may justify scaling back or discontinuing TAA efforts.

-

Scenario and stress reports: Show how current tilts would perform under adverse conditions (e.g., equity crash combined with widening credit spreads). This helps committees judge whether TAA is consistent with capital-preservation objectives.

-

Compliance and breach logs: Summaries of any tactical range, risk budget, or counterparty limit breaches, together with remedial actions and timelines.

Monitoring reports support oversight and escalation by:

- giving boards and investment committees a clear line of sight from policy (SAA and TAA framework) to implementation (actual exposures and trades);

- enabling timely interventions when risk budgets are exceeded, performance deteriorates, or processes are not followed;

- providing evidence of adherence to fiduciary and regulatory obligations, consistent with the CFA Institute Standards on loyalty, prudence, and fair performance presentation.

Worked Example 1.5

An endowment’s SAA benchmark returned 6% over the last three years with a standard deviation of 8%. The actual portfolio, including TAA decisions, returned 7% with a standard deviation of 9%. Regression-based analysis attributes 0.8% of the annual active return to TAA and the remaining 0.2% to security selection. The ex post tracking error of the portfolio versus the SAA is 2%. Evaluate the effectiveness of TAA.

Answer:

TAA contributed 0.8% of annual active return with a contribution to total tracking error estimated at around 1.5%–2%. The implied TAA information ratio is roughly 0.8 / 1.5 ≈ 0.5, which is reasonably strong for an asset allocation process. The modest increase in total volatility (from 8% to 9%) appears acceptable given the higher return. On these metrics, TAA has been an effective use of the risk budget and supports continuing the program, subject to ongoing monitoring and capacity limits.

Summary

Strategic asset allocation defines a portfolio’s long-term structure via the policy portfolio, while tactical tilts seek temporary deviations based on perceived shorter-term opportunities or risks. Because TAA introduces additional active risk, robust governance is essential to control, monitor, and document tactical allocation activity.

Key elements of effective tactical governance include:

- explicit IPS coverage of whether TAA is permitted, its role, and its permitted ranges and risk budgets;

- clear delegation of authority, with defined limits by exposure and tracking error;

- disciplined implementation via cash instruments and derivatives, with controls for leverage, liquidity, and counterparty risk;

- frequent, transparent reporting and performance/risk attribution that isolates TAA effects from other sources of active return;

- structured review and escalation processes for breaches and persistent underperformance.

For Level 3 candidates, the synthesis challenge is to connect these governance and risk-control concepts to specific case facts: diagnose weaknesses, recommend process improvements, and evaluate individual tactical decisions against both policy and risk–return objectives.

Key Point Checklist

This article has covered the following key knowledge points:

- Strategic asset allocation establishes long-term, target asset class weights (policy portfolio) based on investor objectives, constraints, and liabilities.

- Tactical asset allocation introduces temporary, active deviations (tilts) around SAA to pursue perceived market opportunities or manage near-term risks.

- TAA can be implemented via discretionary (qualitative) or systematic (quantitative) approaches, or a hybrid of both.

- Tactical tilt sizing should be driven by explicit risk budgets, commonly expressed as tracking error and drawdown limits.

- All tactical tilts must operate within transparent policy ranges and defined risk budgets, with clear delegation and approval thresholds.

- Implementation choices (cash securities vs derivatives) affect leverage, liquidity, and counterparty risk and must be addressed in governance.

- Sound governance ensures clear delegation, documentation, and periodic review of all tactical allocation activity, supported by independent risk management.

- Performance and risk attribution frameworks should isolate the contribution and risk of TAA, enabling evaluation of skill and adherence to risk appetite.

- Common pitfalls include style drift, excessive tilts, persistent range breaches, high turnover, and weak documentation; exam answers should propose specific remedies.

- Committees and boards retain ultimate responsibility for oversight, monitoring, and enforcement of tactical tilt policy and reporting, even when discretion is delegated.

Key Terms and Concepts

- strategic asset allocation

- tactical asset allocation

- policy portfolio

- tactical tilt governance

- risk budget

- active risk (tracking error)

- leverage

- liquidity risk

- counterparty risk

- rebalancing policy

- drawdown

- stress testing

- information ratio