Learning Outcomes

This article explains how algorithmic execution strategies—VWAP, TWAP, and POV—are structured and applied to institutional orders in the CFA Level 3 context. It clarifies the mechanics of each algorithm, including how orders are sliced over time or volume, how participation rates are set, and how these choices influence transaction costs and market impact. The article distinguishes the market environments and client objectives that favor VWAP, TWAP, or POV, emphasizing differences in liquidity, volatility, urgency, and volume predictability. It highlights how these algorithms interact with execution benchmarks such as VWAP and arrival price, and how their performance feeds into implementation shortfall analysis. The discussion also reviews strengths, limitations, and typical failure modes of each strategy so you can diagnose when an algorithm is mis-specified or misused in exam scenarios. Finally, the article links conceptual understanding to common CFA Level 3 question styles—item sets and short vignettes—so you can quickly infer the most appropriate algorithm, justify the choice with precise reasoning, and avoid frequent conceptual traps tested around algorithm selection and evaluation.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the key features of algorithmic execution and their role in institutional trading, with a focus on the following syllabus points:

- Explain the purpose and functionality of common algorithmic trading strategies (VWAP, TWAP, POV)

- Evaluate the factors that determine the best choice of algorithm for different trading scenarios

- Identify and discuss implementation shortfall, trade scheduling, and benchmark selection in algorithmic trading

- Recognize common pitfalls or misapplications of these algorithms and how to avoid them

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which algorithm is most suitable for executing an order over a full trading day in a thickly traded, non-volatile stock?

- How does a POV algorithm react in a market with a declining volume profile?

- True or false? A TWAP strategy always avoids market impact costs.

- What is "implementation shortfall," and why is it significant in evaluating algorithmic execution?

Introduction

Trade implementation is central to institutional portfolio management. Large orders require careful execution to minimize transaction costs and manage risks of information leakage and market impact. Algorithmic trading tools—VWAP (Volume Weighted Average Price), TWAP (Time Weighted Average Price), and POV (Percentage of Volume)—are widely used to automate and optimize the trade execution process.

Key Term: algorithmic trading

The use of computer algorithms to automate the placement, timing, and size of trade orders according to defined rules with the goal of reducing market impact and slippage. Key Term: market impact

The adverse price movement caused by the execution of a large order, making it more expensive to complete a trade. Key Term: implementation shortfall

The difference between the decision price and the final execution price, reflecting all costs and delays associated with the trading process. Key Term: benchmark

A reference price (such as VWAP or arrival price) used to measure the quality of trade execution.

Algorithmic Strategies: VWAP, TWAP, and POV

Algorithmic strategies break up large orders into smaller pieces and execute them according to preset rules, balancing cost, timeliness, signaling risk, and other constraints. The three main strategies are VWAP, TWAP, and POV.

Algorithm selection maps urgent orders to POV or VWAP, liquid low-urgency orders to classic VWAP, and thin unpredictable flow to TWAP.

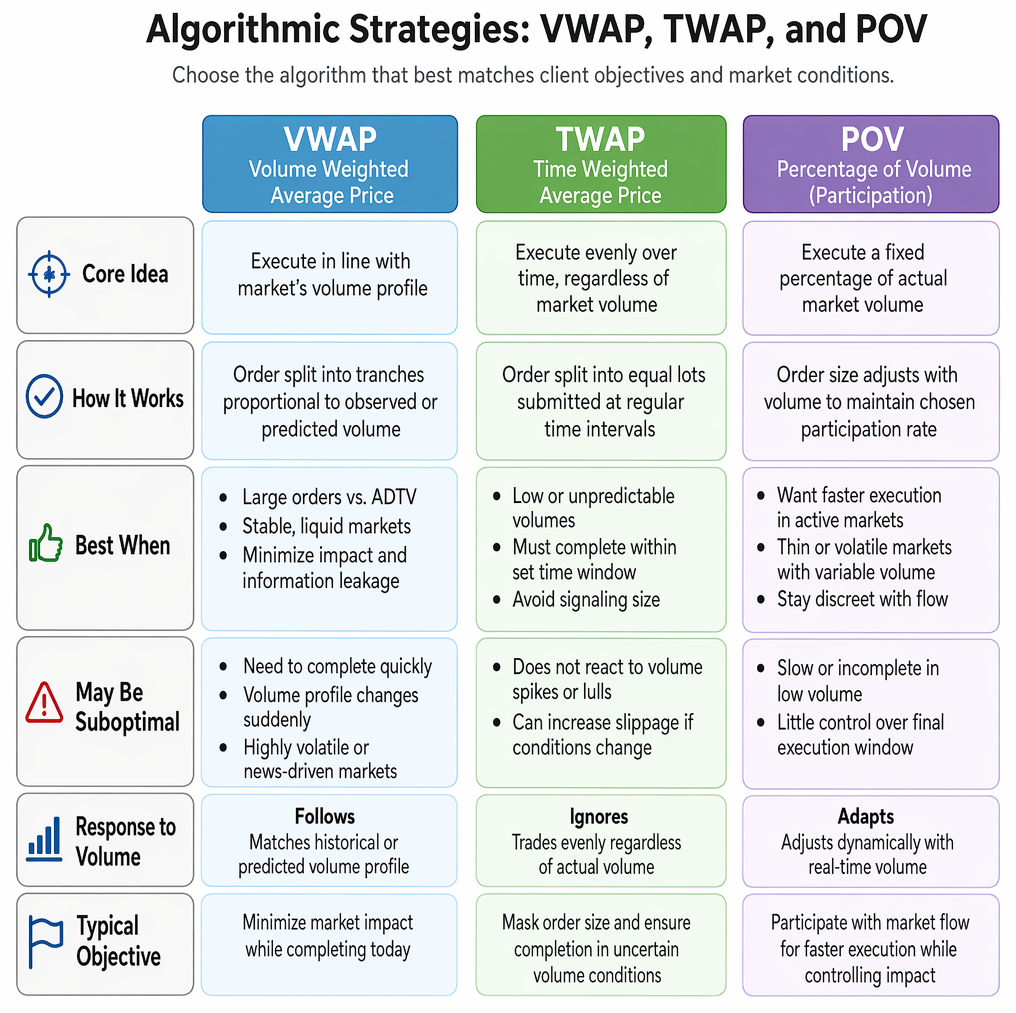

VWAP (Volume Weighted Average Price)

The VWAP algorithm aims to execute trades in-line with the market’s historical or predicted volume profile so that the average execution price is close to that day’s VWAP.

Key Term: Volume Weighted Average Price (VWAP)

The average price of a security over a given period, weighted by the volume traded at each price.

VWAP divides the total order into smaller tranches, submitting each in proportion to observed (or predicted) market volume. It is designed to mask the order and reduces the chance of significant market impact.

When to Use VWAP

VWAP is best for:

- Large orders relative to average daily volume

- Securities with stable, liquid markets

- Minimizing market impact and information leakage

When VWAP May Be Suboptimal

VWAP may perform poorly if:

- A client needs to complete an order quickly (VWAP stretches trades over the session)

- The market volume profile changes suddenly

- Market conditions are highly volatile or news-driven

TWAP (Time Weighted Average Price)

The TWAP algorithm spreads trades evenly throughout a specified period, regardless of actual market volume.

Key Term: Time Weighted Average Price (TWAP)

The average price of a security over a defined time window, giving equal weight to each time interval.

TWAP breaks an order into equal-sized lots submitted at regular intervals, e.g., every 15 minutes. This is effective when market volume is unpredictable or masking the true order size is essential.

When to Use TWAP

TWAP is preferred for:

- Securities with low or unpredictable trading volumes

- Orders that need to be fully completed in a specific time window, regardless of volume

- Cautious clients seeking to avoid signaling large volume at once

Limitations of TWAP

TWAP does not adjust to real-time volume spikes or lulls, which can increase slippage if market conditions change during execution.

POV (Percentage of Volume or Participation)

A Participation (POV) algorithm executes the order as a fixed percentage of actual market trading volume.

Key Term: Percentage of Volume (POV) algorithm

A strategy that dynamically adjusts order size so execution speed matches a preselected fraction of market volume, continuously throughout the day.

As market volume changes, the algorithm increases or decreases order submission to maintain the chosen participation rate, making this method responsive and flexible.

When to Use POV

POV is best when:

- The client wants rapid execution if the market is active but prefers minimal market impact

- Trading in thin or volatile markets where volumes are highly variable

- The trader wishes to remain discreet, avoiding detection by trading in line with the general flow

Drawbacks of POV

With low market volume, order completion may be slow or incomplete. POV provides little control over the final execution window.

Worked Example 1.1

A fund manager is instructed to sell 50,000 shares of company ABC. On average, ABC trades 200,000 shares per day. The manager seeks to avoid significant price movement but must finish the order today. Which algorithm is likely to be most appropriate?

Answer:

VWAP. The order is large but not overwhelming relative to market volume. Executing with VWAP offers discretion, reduces market impact, and assures completion within the day. TWAP may be less suitable since it does not account for intraday volume patterns. POV may be too slow if volume drops, risking order incompletion. Key Term: slippage

The difference between the theoretical execution price and the actual execution price, often due to timing delays and market volatility.

Worked Example 1.2

A trader receives an urgent, market-sensitive sell order for a thinly traded small-cap stock. The client insists the full block must be sold, but market volume is sporadic and unpredictable through the day. Which algorithm is preferable?

Answer:

TWAP. In illiquid, low-volume names, equal time-based slices avoid revealing order size and can be completed regardless of trading lulls. VWAP or POV may stall if volume vanishes. However, expect higher slippage if a sudden spike in volume gets missed.Exam Warning: It is a common mistake in the exam to assume all three algorithms provide similar execution outcomes. In fact, their suitability depends on market liquidity, volatility, urgency, and volume patterns. Be precise when matching an algorithm to the scenario.

Revision Tip: Always match the algorithm to the client's objectives: fast completion (choose POV or a high urgency VWAP), minimal impact (classic VWAP with low participation), or masking order size in unpredictable volumes (TWAP).

Summary

VWAP, TWAP, and POV are the primary algorithmic strategies used to execute institutional orders efficiently. VWAP tracks the market’s natural volume curve, while TWAP slices orders evenly over time. POV adjusts flexibly, trading as a percentage of current volume. The optimal choice depends on order size, urgency, liquidity, and trading objectives. Understanding these algorithms and their trade-offs is critical for CFA success.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish among VWAP, TWAP, and POV algorithmic strategies

- Identify scenarios that best suit each algorithm, based on market conditions and order characteristics

- Understand how benchmarks (VWAP, arrival price) relate to execution analysis

- Recognize and avoid common mistakes when selecting an execution algorithm

Key Terms and Concepts

- algorithmic trading

- market impact

- implementation shortfall

- benchmark

- Volume Weighted Average Price (VWAP)

- Time Weighted Average Price (TWAP)

- Percentage of Volume (POV) algorithm

- slippage