Learning Outcomes

This article explains the function, mechanics, and strategic use of block trading and crossing networks in institutional equity trade implementation. It clarifies how these venues operate relative to public exchanges, the roles of dealers and alternative trading systems, and how orders are priced, matched, and executed. The article highlights how block trades and dark pools help manage market impact, information leakage, and execution risk, and contrasts their effects on liquidity, price discovery, and trading costs. It analyzes key trade-offs among anonymity, execution certainty, speed, and potential price concessions, enabling you to judge when a portfolio manager should prefer a block trade, a crossing network, or traditional market execution. The discussion links these mechanisms directly to CFA Level 3 exam requirements on trading cost minimization, portfolio transitions, and manager implementation shortfall. It also develops your ability to evaluate principal versus agency execution, identify conflicts of interest, and recognize regulatory and ethical considerations when using off-exchange venues. Finally, the article strengthens your skills in interpreting case-based scenarios, performing qualitative comparisons of execution choices, and justifying a recommended trading approach in constructed-response (essay) and item-set questions.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the main mechanisms available for executing large equity trades and minimizing market impact, with a focus on the following syllabus points:

- The rationale for and process behind block trading as a means to manage large trade executions

- The function, advantages, and risks of alternative trading venues such as crossing networks and dark pools

- How block trading and crossing networks mitigate information leakage and limit price movement

- The practical trade-offs between liquidity access, anonymity, and execution certainty

- The application of these methods for institutional orders and portfolio transitions

Command of these topics is critical for portfolio management questions involving trade execution and trading cost minimization.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the primary motivation for using block trading or crossing networks for large institutional equity trades?

- Choose the correct statement: Crossing networks typically provide

- a) Immediate price discovery but little confidentiality

- b) High anonymity and reduced price impact

- c) Guaranteed execution for all submitted orders

- Name one key risk that can arise from placing a large order in a block trading facility.

- Explain the potential trade-off between execution certainty and information leakage in block trading.

Introduction

Institutional investors frequently need to buy or sell large equity positions on behalf of clients or funds. Executing such trades presents unique challenges: the risk of alerting the market to a large order, causing adverse price moves, and the possibility of higher transaction costs due to market impact. Block trading and crossing networks have developed as specialist venues and mechanisms to help manage these risks, offering institutional investors discreet and efficient execution options that minimize explicit and implicit costs. CFA candidates must be able to assess their role in portfolio management and manager performance.

Key Term: block trade

A single negotiated transaction of a large order, usually exceeding a minimum size threshold, typically executed away from the public order book to minimize market impact. Key Term: crossing network

An alternative trading system that matches large buy and sell orders anonymously at designated times or prices, often without routing these orders to the public exchange. Key Term: dark pool

A type of crossing network or alternative venue where order information is not publicly displayed before execution to reduce signaling risk and price movement.Test Tip: When revising Block trading and crossing networks, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

THE CHALLENGE OF LARGE TRADE EXECUTION

Trading a large volume of shares presents a dilemma for institutional investors. If an order is submitted to the open market, the visibility can cause other market participants to adjust prices, increasing execution costs. Alternatively, trading in small increments over time can limit market impact but increases execution risk and opportunity cost if prices move unfavorably during execution.

Block trades and crossing networks seek to address these issues by allowing institutional traders to execute large quantities with reduced price impact, increased anonymity, and more control over information leakage.

Block Trading Facilities

Block trading generally involves a broker-dealer (often called a block house or program desk) who acts as a principal or agent. The broker either matches the large order with another institution, or assumes part of the risk by committing its own capital to fill the order, quoting a “block price” based on market conditions.

Key Term: principal trade

A transaction where a broker-dealer assumes risk by buying or selling securities against its own inventory to facilitate client execution.

Advantages and Trade-Offs

The chief advantage of block trading is minimization of market impact; the order generally does not appear in the public limit order book. The primary trade-off is execution certainty versus price. Immediate execution may require a price concession to compensate the broker for adverse price movement or the risk of holding inventory.

Block trading is most appropriate for liquid securities with active institutional participation and for investors who value fast, confirmed execution over possible price improvement in the open market.

Crossing Networks and Dark Pools

Crossing networks, sometimes called “dark pools,” are venues organized to match large, typically institutional, buy and sell orders away from the exchange. Orders are not displayed to the public before matching, limiting information leakage.

Crossing networks may execute orders at pre-set times (e.g., the closing price) or at the mid-point of the bid-offer spread. This structure allows institutional traders to access liquidity without revealing their interest to the market.

Key Term: midpoint crossing

An execution in a crossing network at the mid-point price between prevailing best bid and best offer, commonly used in dark pools to achieve price improvement and reduced impact.

Comparison: Block Trading vs. Crossing Networks

- Block trading can provide faster execution certainty, particularly for urgent needs, but may require a larger price concession and involves bilateral negotiation with dealers.

- Crossing networks prioritize anonymity and price efficiency by limiting information on pending large orders and executing at neutral prices, but there is no certainty of execution unless sufficient contra-side interest exists.

- Dark pools cater to very large, professional traders and are not suitable for all investor types or stock sizes.

Worked Example 1.1

Question: An institutional fund needs to sell 500,000 shares (2% of a company’s daily volume). Should they use the open market, a block trade, or a crossing network? What are the advantages and risks?

Answer:

- Submitting to the open market risks moving the price down through information leakage and limited liquidity.

- A block trade through a principal dealer may guarantee full and quick execution, but at a discounted price due to inventory risk for the dealer.

- A crossing network or dark pool can offer an anonymous, low-impact execution at the mid price, but there is no guarantee of finding a matching buyer; execution could be partial or may fail.

- The fund must weigh urgency, desire for price improvement, and willingness to accept potential non-execution.

Exam Warning: If a block trade is matched but not fully confidential, the information can leak to the open market, causing adverse price moves even before the block is executed. Partial fills in a crossing network can delay completion and increase opportunity cost.

PRACTICAL FACTORS FOR CFA CANDIDATES

CFA candidates must know that practical implementation involves:

Large-order execution choice depends on urgency, confidentiality needs, and security liquidity when selecting dealer facilitation, dark liquidity venues, or market trading.

- Evaluating urgency and liquidity needs

- Comparing information leakage, market impact, and execution certainty for available trading mechanisms

- Understanding regulations and potential conflicts of interest in block trades (e.g., agency vs principal, fair pricing for clients)

- Justifying why an institution might use a crossing network or dark pool rather than expose a large order to a public exchange

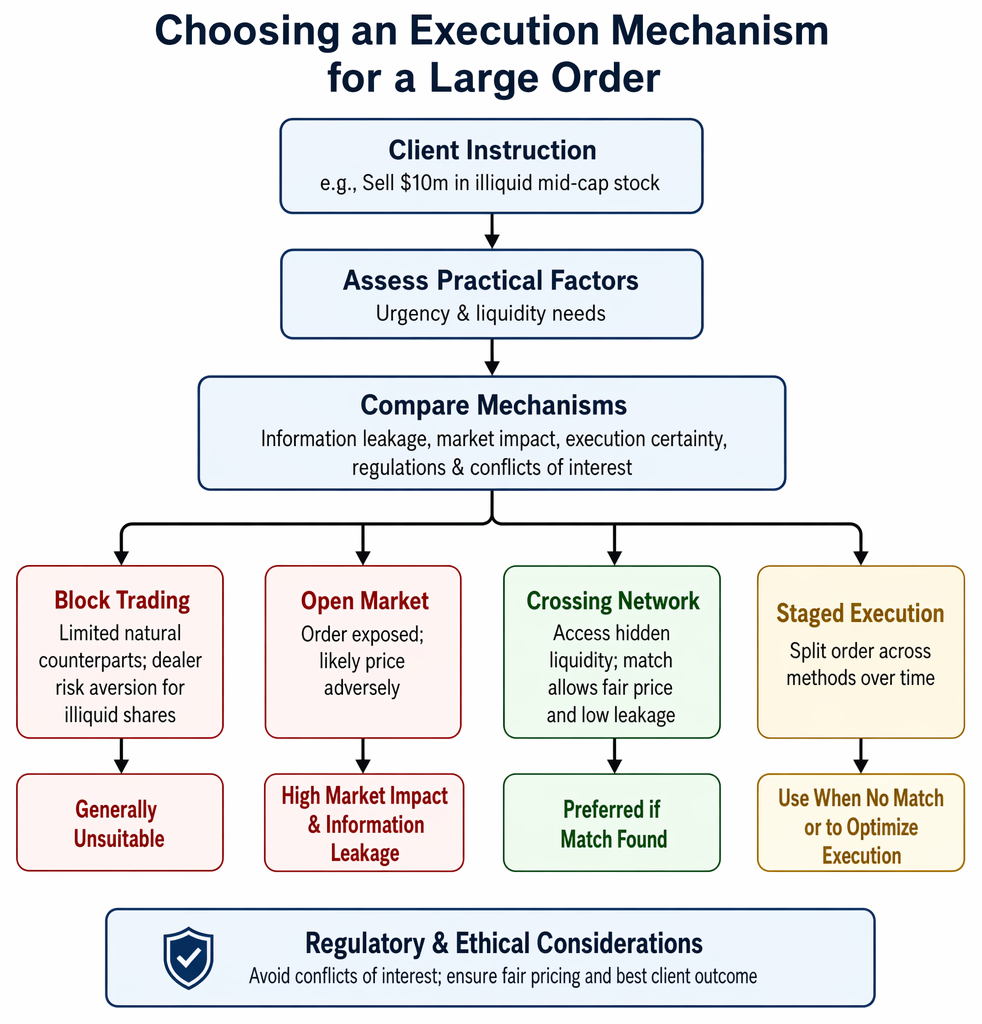

Worked Example 1.2

Question: Suppose an asset manager is given client instructions to rebalance a portfolio, selling $10 million in a relatively illiquid mid-cap stock. What execution mechanism would best minimize trading costs and why?

Answer:

- Block trading may be unsuitable due to limited natural counterparts and dealer risk aversion for illiquid shares.

- The open market would expose the order and likely move the price unfavorably.

- A crossing network could access hidden liquidity. If a matching buyer is found, the trade can execute at a fair price with low information leakage. However, if no match occurs, alternative methods may be required.

- In some cases, staged execution across several methods may be optimal.

Summary

Block trading and crossing networks are specialized tools for executing large equity transactions with minimal market impact, increased confidentiality, and flexible execution options. Block trades offer speed and certainty, but may involve price concessions; crossing networks provide anonymity and price efficiency, but with less execution certainty. CFA candidates must be able to analyze each tool’s merits and risks and select the optimal approach based on transaction objectives, market conditions, and regulatory guidelines.

Key Point Checklist

This article has covered the following key knowledge points:

- Define block trading, crossing networks, and dark pools as trade implementation venues for large orders

- Explain how block trades can minimize market impact and the potential price/risk trade-offs involved

- Assess when a block trade vs a crossing network is most appropriate for institutional execution

- Recognize the principal-agent and information leakage risks associated with block and dark-pool trading

- Apply these methods for effective execution and cost minimization of large portfolio transitions or allocations

Key Terms and Concepts

- block trade

- crossing network

- dark pool

- principal trade

- midpoint crossing