Learning Outcomes

This article explains active fixed-income term structure strategies for CFA Level 3 candidates, including:

- constructing and comparing active yield curve positions (level, slope, curvature) relative to a benchmark portfolio;

- applying duration and key rate duration to express views on specific maturity segments while controlling total interest rate risk;

- distinguishing parallel shifts, twists, and butterfly moves, and mapping each to suitable bullet, barbell, flattener, steepener, or butterfly structures;

- formulating duration-neutral trades that monetize anticipated curve changes using cash bonds, futures, and swaps;

- calculating approximate price effects of curve moves using effective duration, key rate duration vectors, and simple scenario analysis;

- evaluating trade payoffs, sources of tracking error, and scenario outcomes under alternative yield curve paths;

- diagnosing and avoiding common implementation pitfalls, such as unintended duration bets or misaligned key rate exposures;

- integrating active term structure views into a broader fixed-income mandate while honoring constraints, risk limits, and benchmark objectives;

- articulating clear exam-quality explanations that link interest rate expectations to specific term structure trades and risk metrics.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the design, implementation, and evaluation of active term structure strategies, with a focus on the following syllabus points:

- Explaining and applying duration and yield curve concepts in portfolio management

- Identifying types of yield curve shifts (parallel, twists, butterflies) and linking them to active strategies

- Designing active yield curve trades that reflect interest rate views (e.g., level, slope, curvature)

- Calculating and interpreting key rate durations for restructuring risk along the curve

- Evaluating the performance and risks of yield curve strategies within overall portfolio objectives

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are three common types of yield curve shifts, and how does each affect bond values?

- Define portfolio duration and key rate duration. Why is key rate duration important for active yield curve strategies?

- A manager expects the short end of the curve to rise while long rates fall. Which trade structure (bullet, barbell, or flattener) best reflects this view?

- Explain how an investor can implement a duration-neutral yield curve trade to profit from an expected curve steepening.

Introduction

Active yield curve and duration strategies are central tools in fixed-income portfolio management. These strategies seek to exploit anticipated changes in the level, slope, and shape of the yield curve by adjusting portfolio duration, positioning along the curve, or targeting specific maturity segments. Success requires careful analysis of interest rate expectations, understanding the mechanics of curve shifts, and precise implementation using key rate durations to control risk. This article covers core principles, examples, and common errors CFA candidates must fully understand.

Test Tip: When revising Active term structure strategies, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Exam Warning: Do not rely on keyword recognition alone; check the precise condition, exception, calculation step, or evidence the question requires.

YIELD CURVE PATTERNS AND STRATEGIC POSITIONING

Active fixed-income managers express views on future rates by structuring portfolios to benefit from expected yield curve shifts:

Key Term: yield curve shift

A movement in the term structure of interest rates, including parallel shifts, twists (change in slope), and changes in curvature, that affects bond prices differently across maturities.

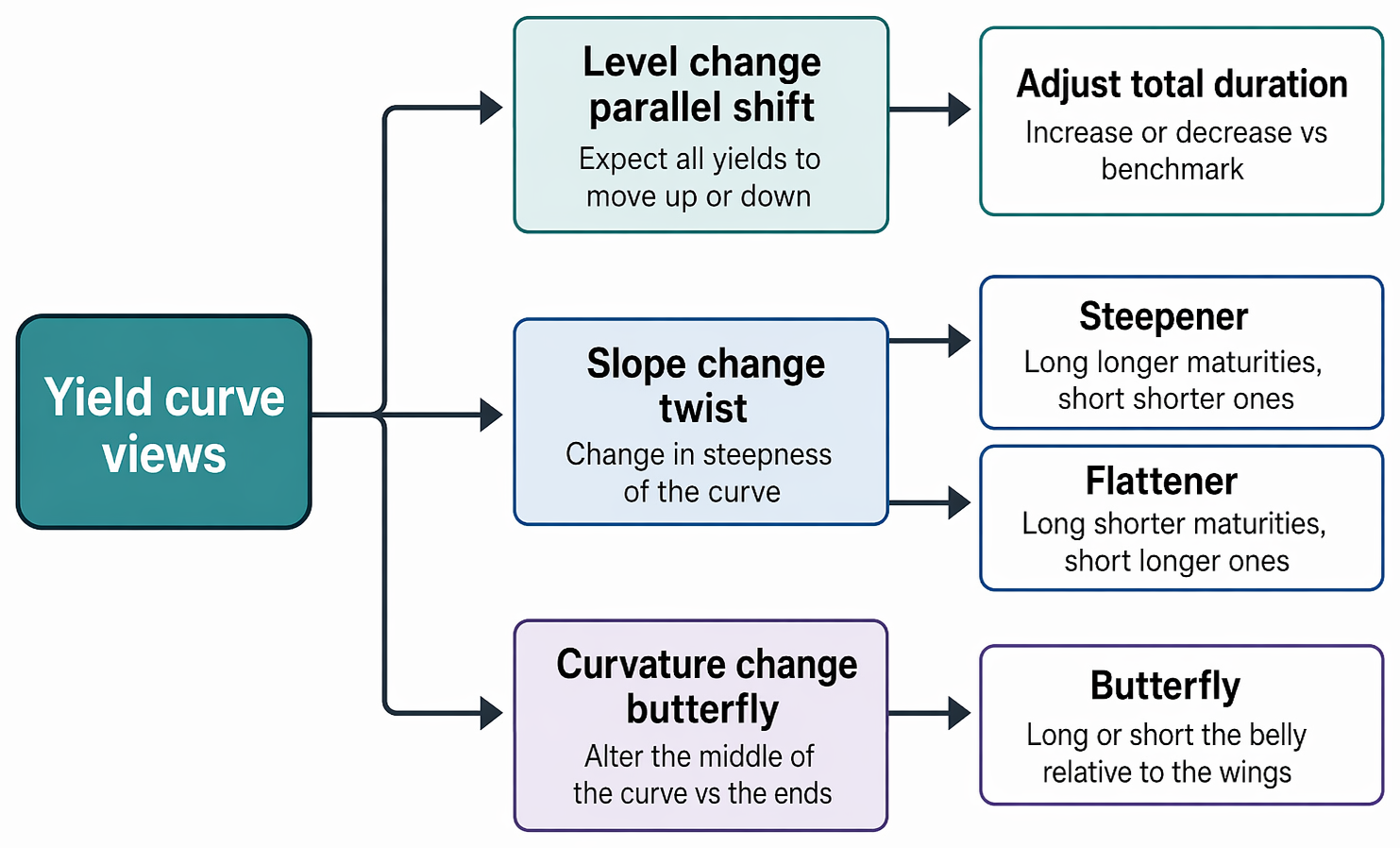

Parallel shifts involve moving all rates up or down by the same amount. Twists change the curve's steepness—steepening if the spread between long and short rates increases or flattening if it narrows. Butterfly (curvature) changes affect the middle of the curve relative to the ends.

Key Term: duration

A measure of a bond's or portfolio's price sensitivity to a parallel change in yields; typically Macaulay or modified duration. Key Term: key rate duration

The sensitivity of a bond or portfolio to a specific point (maturity) yield change, holding other yields constant; used to manage exposure to non-parallel curve shifts.

ACTIVE TERM STRUCTURE STRATEGIES

Active yield curve strategies fall into three main categories:

Term structure strategies map level, slope, and curvature expectations to benchmark-duration adjustments, steepener or flattener trades, and butterfly positions.

-

Level (parallel shift) trades: Adjust portfolio duration relative to the benchmark. Overweight duration if rates are expected to fall; underweight if rates are expected to rise.

-

Slope (steepener/flattener) trades: Use bullet or barbell structures to position for steepening or flattening of the curve. A steepener profits if the yield differential widens, typically with a duration-neutral long-short combination across maturities.

-

Curvature (butterfly) trades: Combine long and short positions in short, intermediate, and long-term bonds to profit from changes in curve curvature.

Implementing these strategies may involve cash bonds, bond futures, swaps, or options, depending on mandate and constraints.

Worked Example 1.1

Question: A manager expects the curve to flatten: short rates to rise 50 bps, long rates stable. How could they structure a trade to profit from this expectation without changing overall portfolio duration?

Answer:

The manager would enter a flattener by shorting short-duration bonds and going long an equal-duration position in long-term bonds. Duration-neutrality is maintained, so the portfolio does not add market risk; profit comes from the relative movement between segments.

KEY RATE DURATION APPLICATION

Key rate durations allow precise targeting of risk. Instead of changing total portfolio duration, managers can emphasize or reduce exposure at specific maturities to match their interest rate view.

For example, if risk at the 2-year key rate is undesired, portfolio exposure can be minimized there. If the 10-year point is expected to fall disproportionately, increased key rate duration at 10 years will add to potential outperformance. Typically, key rate durations across selected maturities sum to the effective duration.

Worked Example 1.2

Question: A portfolio has the same effective duration as its benchmark but 2x the 5-year key rate duration and less at other points. What is the manager's rate view, and what trade structure likely reflects this?

Answer:

The manager anticipates a decline in 5-year yields relative to others (a butterfly trade favoring the belly), increasing exposure at 5 years and reducing elsewhere to keep overall duration unchanged.

EXAM WARNING

A common exam mistake is assuming that flatteners or steepeners always have higher risk. In fact, they can be structured to be duration-neutral; active risk arises from deviations away from the benchmark in key rate exposures, not from absolute market risk.

PORTFOLIO IMPLEMENTATION: TRADE TYPES

- Bullets: Concentrate exposure in maturities at a single point (e.g., 5-year bonds).

- Barbells: Split exposure between short and long maturities, minimizing exposure in the middle.

- Flatteners/Steepeners: Go long one segment, short another, balanced for duration neutrality.

- Butterflies: Long/short combinations in three segments, targeting the "body" or "wings" of the curve for anticipated curvature changes.

Active trades can be implemented using government bonds, futures, swaps, or options, depending on scale and liquidity. Key point: Duration matching and key rate duration analysis allow managers to take targeted interest rate views without increasing overall market risk.

Worked Example 1.3

A fund manager expects short rates to rise and long rates to fall. What is the most effective duration-neutral portfolio structure?

Answer:

Implement a barbell strategy: short short-term bonds, long long-term bonds, adjusting position sizes so the total dollar durations offset. Gains/losses arise only if curve slope changes as expected.

Risk and Return Analysis

Assess the risk and return profile of each trade. Duration-neutral strategies have tracking error (active risk) but do not increase absolute market risk. If the view is incorrect, outperformance will be negative, but portfolio volatility need not rise.

Summary

Active yield curve and duration strategies target alpha by expressing rate, slope, or curvature views while controlling or neutralizing total duration risk. Implementation requires:

- Defining interest rate view (level, slope, curve changes)

- Structuring bullet, barbell, steepener, flattener, or butterfly trades accordingly

- Allocating key rate durations to align with views, maintaining or limiting tracking error

- Using bonds, futures, or swaps for efficient risk transfer

Constant monitoring and adjustment are essential as views or curve patterns change.

Key Point Checklist

This article has covered the following key knowledge points:

- Define active yield curve and duration strategies for fixed-income portfolios

- Distinguish parallel, slope, and curvature yield curve shifts

- Construct duration-neutral steepener, flattener, and butterfly trades

- Apply key rate duration to target specific curve risk exposures

- Implement active curve trades using bonds, futures, and swaps

- Identify and avoid common errors in curve trade interpretation

Key Terms and Concepts

- yield curve shift

- duration

- key rate duration