Learning Outcomes

This article outlines the business and organisational characteristics of Limited Liability Partnerships (LLPs) for SQE1 FLK1, including:

- How LLPs are formed and incorporated at Companies House, and how this differs from general partnerships and limited companies

- The effect of separate legal personality, the scope of limited liability, and situations where members may incur personal liability

- Roles, decision‑making powers and statutory responsibilities of members and designated members, including compliance with filing and disclosure obligations

- The structure and purpose of LLP agreements, the operation of default rules under the LLP Regulations 2001, and how these mirror or depart from Partnership Act 1890 provisions

- Principles of agency and member authority (actual and apparent), and how these determine when the LLP is bound by members’ acts

- Application to LLPs of insolvency and clawback provisions, including wrongful trading, fraudulent trading and recovery of pre‑insolvency withdrawals

- The tax‑transparent treatment of LLPs, allocation of profits and losses to members, and the consequences for income tax and corporation tax

- The practical advantages and disadvantages of LLPs compared with companies and general partnerships when advising clients on choice of business vehicle

SQE1 Syllabus

For SQE1, you are required to understand the business and organisational characteristics of Limited Liability Partnerships (LLPs), with a focus on the following syllabus points:

-

Business and organisational characteristics (Limited liability partnerships (LLPs))

-

Legal personality and limited liability

-

Procedures and documentation required to form an LLP and other steps required under companies and partnerships legislation to enable the entity to commence operating:

- Constitutional documents

- Companies House filing requirements (including PSC disclosure and annual confirmation statements)

-

Partnership decision-making and authority of partners (applied to LLPs)

- Common provisions in LLP agreements

- Default rules under the LLP Regulations 2001 (profit sharing, management, remuneration, unanimity for certain changes)

-

Authority of members and the LLP’s liability for members’ acts

-

Application to LLPs of insolvency provisions (wrongful trading, fraudulent trading and clawback of withdrawals)

-

Taxation treatment of LLPs (transparency; allocation of profits and losses)

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- True or False? An LLP requires a formal written agreement between members to be validly formed.

- What is the minimum number of designated members required for an LLP?

- Explain the concept of 'separate legal personality' in the context of an LLP.

- Are members of an LLP personally liable for the LLP's debts?

Introduction

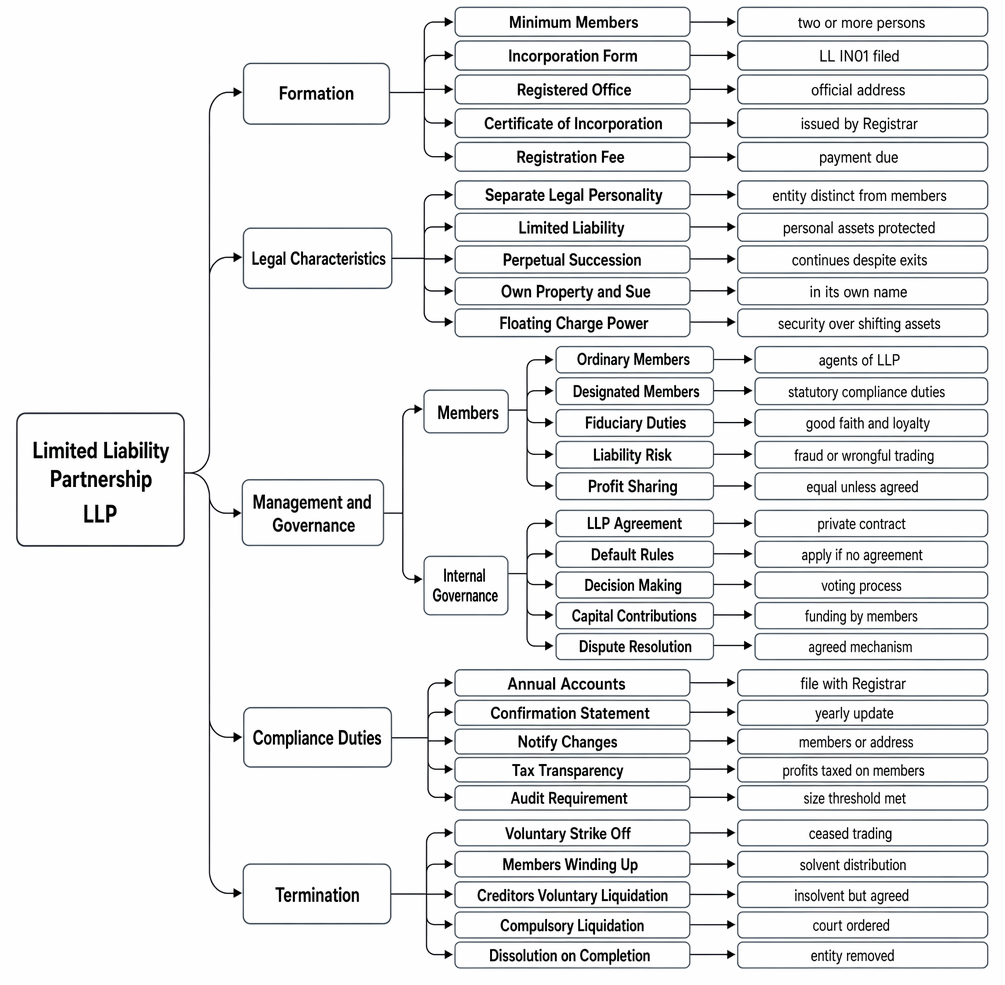

Limited Liability Partnerships (LLPs) offer a business structure combining features of both traditional partnerships and limited companies. Governed by the Limited Liability Partnerships Act 2000 (LLPA 2000) and associated regulations, LLPs provide flexibility alongside protection for members' personal assets. LLPs are bodies corporate with corporate personality and are created by incorporation, like companies, rather than arising informally like general partnerships. They are particularly popular with professional services firms, but are also used for joint ventures and other enterprises where flexibility in internal arrangements is desirable together with limited liability and the ability to grant floating charges.

LLP formation, separate legal personality, governance, compliance obligations, and dissolution.

Some regard LLPs as hybrid organisations. In practice, they share more with companies than with ordinary partnerships: they are incorporated, have separate legal personality, use the term “members” rather than “partners”, and many Companies Act 2006 (CA 2006) provisions (and virtually all relevant Insolvency Act 1986 provisions) apply to LLPs by virtue of secondary legislation. Unlike companies, LLPs do not require a board of directors or a separation between owners and managers; internal governance is largely contractual.

Formation requirements

Establishing an LLP involves a formal registration process with Companies House. This contrasts with general partnerships, which can arise informally.

Key Term: Limited Liability Partnership (LLP)

An incorporated business structure offering limited liability to its members, governed by the LLPA 2000. It possesses separate legal personality.

The key steps for incorporation include:

-

Minimum membership: At least two persons (which can include individuals or companies) intending to carry on a lawful business with a view to profit must agree to form an LLP. There is no upper limit on members.

-

Incorporation document (Form LL IN01): This must be delivered to the Registrar of Companies with the requisite fee. LL IN01 includes:

- The proposed name of the LLP (which must end with "Limited Liability Partnership" or "LLP").

- The location of the registered office (England and Wales, Wales, Scotland, or Northern Ireland).

- The registered office address.

- Details of initial members, specifying which are designated members (at least two must be designated, unless all are designated).

- Members’ service addresses, month and year of birth, usual residential addresses (not publicly displayed), and country of residence; corporate member details where relevant.

- PSC information (if applicable), or confirmation that there is or is not someone with significant control over the LLP.

- A statement of compliance confirming adherence to registration requirements.

-

Registration fee: Payment must accompany the application.

Key Term: People with Significant Control (PSC)

Individuals or legal entities who have significant control over an LLP. PSC details must be maintained and, where required, filed to Companies House. Key Term: Perpetual Succession

The feature of an incorporated entity allowing continuous existence regardless of changes in membership.

Once registered, Companies House issues a certificate of incorporation. The LLP comes into existence as a separate legal entity on the date stated. The LLP’s name must be displayed at places of business and on its stationery, together with its place of registration, registered number and registered office address.

Where the members are individuals, they normally register with HMRC as self-employed, reflecting the LLP’s tax-transparent treatment.

LLPs can change their name by notifying the Registrar; a certificate of name change will be issued. Members must notify Companies House of changes in membership within 14 days (forms LL AP01/AP02 for appointments; LL TM01/TM02 for terminations). LLPs must also file a yearly confirmation statement to keep public registry information up to date.

A point often overlooked is the single-member rule: if membership falls to one and remains so for more than six months, that sole member becomes jointly and severally liable for debts incurred during the period from six months after the reduction in membership until a second member is admitted.

Test Tip: Do not confuse formation of an LLP with a general partnership. An LLP only comes into existence on incorporation and issue of the certificate of incorporation.

Separate legal personality

Once incorporated, an LLP acquires its own legal identity, distinct from its members.

Key Term: Separate Legal Personality

The principle that an incorporated entity is legally distinct from its owners and managers. It can own property, enter contracts, sue, and be sued in its own name.

This separation means the LLP itself is responsible for its debts and obligations. It can own property, enter contracts, and continue indefinitely, irrespective of changes in membership (perpetual succession). Practically, this facilitates continuity of business operations and ownership interests, and allows the LLP to grant security, including floating charges, to lenders. The LLP can be liable in civil law (contract and tort) and, as an organisation, can be convicted of certain criminal offences, though sanctions will be fines and other non-custodial orders because an LLP cannot be imprisoned.

Limited liability

A significant advantage of the LLP structure is the limited liability afforded to its members.

Key Term: Limited Liability

A legal protection where members' personal liability for the debts and obligations of the LLP is restricted, typically to the amount of their agreed capital contribution (if any).

Members are generally not personally responsible for the LLP's debts. Liability protection is not absolute, however. Members may incur personal liability in specific situations, such as:

- Personal torts: a member remains liable for their own tortious conduct (e.g. negligent advice causing loss), though the LLP may also be liable if committed in the course of LLP business.

- Wrongful trading: personal contribution orders can be made if, before insolvent liquidation, a member knew or ought to have concluded there was no reasonable prospect of avoiding insolvent liquidation and failed to take every step to minimise potential loss to creditors.

- Fraudulent trading: personal liability arises where business is carried on with intent to defraud creditors or for any fraudulent purpose.

- Two‑year clawback: certain withdrawals by members prior to insolvent liquidation can be ordered to be repaid.

- Single-member rule: remaining as a single member for more than six months carries joint and several liability for debts incurred during the relevant period.

Moreover, members can be disqualified from acting as LLP members (and company directors) under the Company Directors Disqualification Act 1986, reflecting the application of corporate regulatory standards to LLPs.

Exam Warning: Limited liability does not mean no personal liability in all circumstances. In problem questions, check for personal torts, wrongful trading, fraudulent trading, clawback, and the single-member rule.

Designated members

Every LLP must have at least two designated members.

Key Term: Designated Member

A member of an LLP with specific statutory responsibilities for administrative and compliance tasks, such as signing accounts and filing documents with Companies House.

If an LLP fails to nominate designated members on incorporation, all members are treated as designated by default. Designated members’ duties include:

- Ensuring proper accounting records are kept; preparing, signing and filing the LLP’s annual accounts with Companies House within the statutory time limits (private LLPs usually have nine months from the end of the accounting reference period).

- Appointing, removing and remunerating the auditor, where an audit is required.

- Filing the annual confirmation statement and updating details of members and PSCs.

- Notifying Companies House of changes to the registered office address or LLP name and filing membership changes within 14 days.

- Taking steps in relation to winding up, including liaising with insolvency practitioners.

Failure to comply with filing obligations can constitute criminal offences and may expose designated members to fines. While designated members carry additional administrative responsibilities, all members owe duties to the LLP and are subject to the legal framework applicable to LLPs.

Internal governance and management

While the LLPA 2000 and related regulations provide a default framework, LLPs typically formalise their internal operations through an LLP agreement.

The LLP agreement

This private agreement between the members governs their mutual rights and duties and the internal management of the LLP.

Key Term: LLP Agreement

A contractual document outlining the internal rules, responsibilities, profit sharing, decision-making processes, and other governance matters agreed upon by the members of an LLP.

Key areas typically covered include:

- Capital contributions, including whether capital is fixed or variable, and whether interest is payable on capital.

- Profit and loss sharing arrangements, including salaries to working members, profit allocation or drawings, and treatment of capital profits.

- Management roles and decision-making authority, such as management committees, voting thresholds, and reserved matters.

- Procedures for admitting new members and handling exits, including retirement, expulsion, compulsory buyout, valuation methodology, and payment terms.

- Restrictions on competition and confidentiality, restrictive covenants, and notice periods.

- Dispute resolution mechanisms.

- Insurance, indemnities, and limitation of liability provisions.

- Policies on distributions to manage insolvency risk and potential clawback.

In the absence of an LLP agreement, default provisions from the LLP Regulations 2001 apply, which mirror many aspects of the Partnership Act 1890, such as:

- Equal sharing of capital and profits among members.

- Every member may take part in management.

- Every member may inspect the LLP’s books and records.

- No member is entitled to remuneration for acting in the business or management of the LLP.

- Ordinary matters decided by majority; unanimity is required to change the nature of the business, vary the agreement, or admit a new member.

- Indemnities for members who incur liabilities in the proper conduct of LLP business.

- Duties to render accounts, account for benefits received without consent, and refrain from competing with the LLP without consent.

- No default right to expel a member; expulsion must be expressly provided for in the LLP agreement.

- Members may leave by giving reasonable notice, subject to agreement terms.

These defaults are practical starting points but often unsuitable for modern practice; most LLPs tailor their agreement to reflect differing capital inputs, workload, and management structures, and to include expulsion and reserved matters to protect the LLP.

Test Tip: If a question states there is no LLP agreement, apply the default rules. Equal profit sharing and no remuneration for management are common exam traps.

Flexibility vs. formality

Compared to companies, LLPs offer greater internal flexibility. There is no statutory requirement for board meetings or the rigid separation between directors and shareholders found in companies. Members can tailor the LLP agreement to suit their specific business needs. However, LLPs face more administrative and filing requirements than general partnerships due to their incorporated status. Public disclosure obligations, such as accounts, confirmation statements, and certain member and PSC filings, are the trade‑off for the benefits of corporate personality and limited liability.

Worked Example 1.1

Alex, Ben, and Chloe want to set up a consultancy business. They are concerned about potential personal liability if a client sues them for negligent advice. They want a flexible management structure where all can participate equally. They anticipate needing external finance in the future. Which business structure might be most suitable?

Answer:

An LLP could be highly suitable. It offers limited liability, protecting their personal assets from business debts and negligence claims compared with a general partnership, while retaining flexible internal management through an LLP agreement. As an incorporated entity, an LLP can grant floating charges, potentially making it easier to secure finance than a general partnership. While more formal than a partnership, it avoids the stricter corporate governance of a limited company.

Liability and duties of members

Members of an LLP have specific duties and potential liabilities.

Members act as agents of the LLP and owe fiduciary duties to the LLP, similar to partners in a general partnership. These include:

- A duty of good faith.

- A duty to render accounts and provide full information on LLP matters to other members.

- A duty to account for benefits derived from the LLP's business without consent.

- A duty not to compete with the LLP without consent.

Members also owe a duty of reasonable care and skill to the LLP. Designated members have additional statutory administrative duties.

Key Term: Apparent Authority

Authority inferred from a principal’s representation that an agent has authority. If a member appears to have authority to a reasonable third party, the LLP may be bound even if the member lacked actual authority.

LLPs should clearly define the scope of members’ authority internally and manage external representations to reduce the risk of unauthorised commitments. Nonetheless, apparent authority can bind the LLP where a third party reasonably believes a member has authority and the transaction is of a type usual for the LLP’s business.

Liability of the LLP

As a separate legal entity, the LLP is liable for its own debts. It is also liable for wrongful acts or omissions committed by a member acting in the ordinary course of the LLP's business or with its authority. Contractually, the LLP is bound by acts of members within actual or apparent authority.

Worked Example 1.2

Mara, a member of an LLP accountancy firm, signs a tax advisory contract with a client. The other members had limited Mara’s actual authority to engagements under £10,000, but the contract is for £25,000 and tax advisory work is a usual part of the firm’s business. The client had no notice of the internal limit. Is the LLP bound?

Answer:

Likely yes. Mara was acting in the usual business of the LLP and appeared to have authority. The client did not know of the internal limit. The LLP would be bound on apparent authority principles and may pursue internal remedies against Mara for breaching the internal authority limit.

Clawback and insolvency provisions

In an insolvent liquidation, sums withdrawn by members, for example profit distributions, salaries, loan repayments, interest on loans, or capital repayments, within two years prior to the winding-up can potentially be clawed back if it is proved the member knew or had reasonable grounds for believing the LLP was unable to pay its debts, or would become so as a result of the withdrawal. This look‑back provision is designed to protect creditors from value being stripped out in the lead‑up to insolvency.

These provisions operate alongside wrongful and fraudulent trading personal liability and can have significant practical impact, especially in LLPs making regular drawings. Many LLP agreements incorporate distribution policies, such as retention buffers and solvency statements, to mitigate clawback risk.

Worked Example 1.3

Jae’s LLP distributed substantial profits to members over the last 18 months. The LLP has now entered insolvent liquidation. The liquidator discovers that two large withdrawals were made when creditors were unpaid and cash‑flow forecasts showed mounting arrears. Can the liquidator seek recovery from members?

Answer:

Potentially, yes. Withdrawals within two years of insolvent liquidation can be ordered to be repaid if members knew, or had reasonable grounds to believe, the LLP could not pay its debts, or would become unable to pay, as a result of the withdrawals. The liquidator will examine the timing, financial position, and members’ knowledge. If the test is met, repayment orders may be made.

Taxation

For tax purposes, LLPs are generally treated as transparent entities, similar to general partnerships.

Key Term: Tax Transparency

A principle where the business entity itself is not taxed on its profits; instead, the profits are allocated to the owners or members who are then individually taxed on their share.

This means the LLP itself does not pay corporation tax on trading profits. Profits are allocated to members who are then taxed individually: income tax and National Insurance for individual members, and corporation tax for corporate members, on their share of the profits for the relevant accounting period, irrespective of whether profits are actually drawn. If the LLP makes losses, each member chooses how to claim relief on their share of the loss, subject to applicable rules.

Individual members therefore ordinarily register with HMRC as self-employed, even though the LLP itself is a separate legal person.

For capital gains, an LLP carrying on a trade is treated like a partnership: disposals of partnership assets are treated as disposals by each member of their fractional interest, with each member assessing any chargeable gain on their share. Reliefs and allowances are considered at the member level. Where an LLP ceases to trade, certain corporate capital gains rules can apply.

LLP accounting typically includes an appropriation account showing how net profits are divided between members, including any salaries and interest on capital payable under the LLP agreement. This facilitates tax reporting and clarity between capital accounts and current accounts.

Worked Example 1.4

Sam and Dia are individual members of a trading LLP. The LLP’s net trading profit is £240,000. Their LLP agreement provides £30,000 salary to Dia, 8% interest on capital (Sam £100,000; Dia £50,000), and the remaining profit shared 60:40 (Sam:Dia). What amounts are assessed on each for income tax?

Answer:

Dia’s salary (£30,000) and interest on capital (£4,000) are appropriations of profit, not employment income. Interest on Sam’s capital is £8,000. Net profit of £240,000 is appropriated: first interest (£12,000) and salary (£30,000) leave £198,000 to share. Sam takes 60% (£118,800) and Dia 40% (£79,200). Sam’s taxable share is £118,800 + £8,000 = £126,800. Dia’s is £79,200 + £30,000 + £4,000 = £113,200. Each is taxed on their total share of LLP trading profits.

Termination

An LLP continues to exist until formally dissolved. Dissolution typically occurs through:

- Voluntary striking off: If the LLP is no longer trading, members can apply to Companies House to have it struck off the register, provided eligibility conditions are met.

- Winding up or liquidation: An LLP can be wound up either voluntarily or compulsorily, following procedures similar to those for companies under the Insolvency Act 1986. LLP members may be liable for wrongful or fraudulent trading and subject to clawback of recent withdrawals.

Members should ensure that the LLP’s public filings are brought up to date before striking off and that creditors are not prejudiced. Where trading has occurred, a formal liquidation may be the proper route.

Summary

LLPs provide a valuable structure, particularly for professional services firms, offering the benefits of limited liability and separate legal personality while retaining much of the operational flexibility of a partnership. Key considerations include the formal incorporation process, the distinction between members and designated members, the importance of an LLP agreement, and the implications of tax transparency. Lenders favour the ability of LLPs to grant floating charges. Public filing obligations are the necessary trade‑off for these benefits; members must manage distribution policies and solvency prudently to avoid wrongful trading and clawback risks.

| Feature | LLP | General Partnership | Private Limited Company |

|---|---|---|---|

| Legal Status | Incorporated (Separate Legal Personality) | Unincorporated (No Separate Personality) | Incorporated (Separate Legal Personality) |

| Liability | Limited (for members) | Unlimited (for partners) | Limited (for shareholders) |

| Formation | Formal (Registration at Companies House) | Informal (Can arise by agreement/conduct) | Formal (Registration at Companies House) |

| Internal Governance | Flexible (Governed by LLP Agreement / Default Regulations) | Flexible (Governed by Partnership Agreement / PA 1890) | More rigid (Governed by Articles / CA 2006) |

| Taxation | Transparent (Members taxed individually on profit share) | Transparent (Partners taxed individually on profit share) | Opaque (Company pays Corporation Tax; shareholders taxed on dividends) |

| Public Disclosure | Required (Accounts, Confirmation Statement) | Minimal | Required (Accounts, Confirmation Statement etc.) |

| Floating Charges | Can grant | Cannot grant | Can grant |

Note: Unlike an ordinary partnership, LLP members can be disqualified under the CDDA 1986; many company law and insolvency provisions apply to LLPs by regulation.

Key Point Checklist

This article has covered the following key knowledge points:

- LLPs are incorporated bodies formed under the LLPA 2000, requiring registration at Companies House.

- LLPs possess separate legal personality and offer limited liability protection to members.

- At least two members are required, including a minimum of two designated members; if none are specified, all members are treated as designated.

- If an LLP has only one member for more than six months, that sole member becomes jointly and severally liable for certain debts incurred during the relevant period.

- Internal governance is flexible, often detailed in a private LLP agreement; default LLP Regulations 2001 apply otherwise.

- Members act as agents of the LLP; actual and apparent authority principles can bind the LLP in dealings with third parties.

- LLPs are tax transparent: trading profits are allocated to members and taxed in their hands; corporate members pay corporation tax on their share.

- LLPs can grant fixed and floating charges, aiding access to finance.

- Many CA 2006 and IA 1986 provisions apply to LLPs; members can face personal liability for wrongful or fraudulent trading, and recent withdrawals may be clawed back in insolvency.

- Designated members are responsible for filing accounts, confirmation statements, and PSC/member updates; failure to comply may attract sanctions.

- Dissolution occurs via striking off, subject to conditions, or winding up under insolvency procedures.

Key Terms and Concepts

- Limited Liability Partnership (LLP)

- People with Significant Control (PSC)

- Perpetual Succession

- Separate Legal Personality

- Limited Liability

- Designated Member

- LLP Agreement

- Apparent Authority

- Tax Transparency