Learning Outcomes

This article examines the principal types of security a company can grant over its assets: fixed and floating charges. It outlines their characteristics, the process for their creation and registration, and their implications, particularly in insolvency scenarios. After reading this article, you should be able to distinguish between fixed and floating charges, understand the concept of crystallisation, appreciate the importance of registration under the Companies Act 2006, and identify the priority of these charges during a company's liquidation according to the Insolvency Act 1986. You should also be able to explain when a mortgage is used as the highest form of security, how book debts may be secured (and when a purported fixed charge is properly analysed as floating), the typical content of a secured lending debenture (including negative pledge and events of default), and the effect of preferential debts and the prescribed part on floating charge recoveries. This knowledge is essential for advising on secured lending transactions in business law practice.

SQE1 Syllabus

For SQE1, you are required to understand the practical implications of different types of security used in business finance, including advising on the creation, perfection, and enforcement of fixed and floating charges and their respective priorities in insolvency, with a focus on the following syllabus points:

- the distinction between fixed and floating charges and their attachment to company assets

- the legal requirements for creating and registering charges at Companies House under the Companies Act 2006

- the concept of crystallisation of floating charges and its consequences

- the order of priority for distributing assets to secured creditors upon a company's insolvency, including the effect of the prescribed part for unsecured creditors

- the purpose and effect of a negative pledge clause

- control requirements for a valid fixed charge over receivables (book debts) and the Spectrum Plus analysis distinguishing fixed from floating

- the scope of preferential debts (including HMRC’s secondary preferential status for certain taxes) and how they rank

- avoidance of certain floating charges under s 245 Insolvency Act 1986 (relevant time, connected persons, and the “new money” exception)

- the ability of a qualifying floating charge holder to appoint an administrator and the limits on administrative receivership for post‑September 2003 charges

- registration practice (MR01, 21‑day time limit, keeping instruments available for inspection) and consequences of non‑registration.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which type of charge typically allows a company more freedom to deal with the charged assets in the ordinary course of business?

- a) Fixed charge

- b) Floating charge

- c) Legal mortgage

- d) Equitable charge

-

What is the time limit for registering a charge created by a UK company at Companies House?

- a) 14 days

- b) 21 days

- c) 28 days

- d) No time limit

-

What event typically causes a floating charge to become fixed on the assets it covers?

- a) Creation of the charge

- b) Registration of the charge

- c) Crystallisation

- d) Repayment of the loan

-

In a company liquidation, which type of charge generally ranks higher in priority for repayment from the proceeds of the specific charged asset?

- a) Floating charge

- b) Fixed charge

- c) Unsecured loan

- d) Preferential debts

Introduction

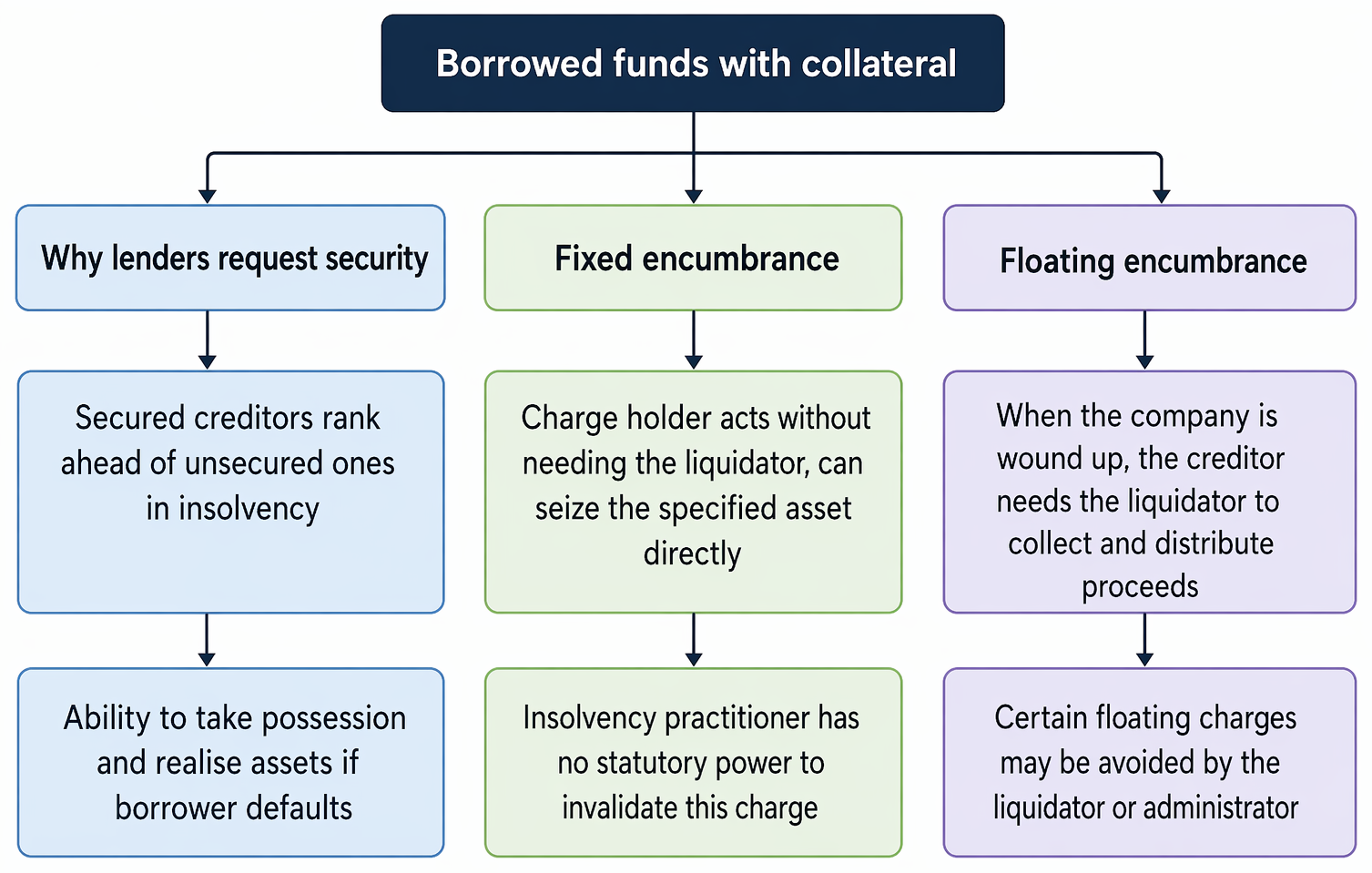

When a company borrows money, particularly substantial amounts, the lender will often require security for the loan. Security provides the lender with rights over certain company assets, reducing the lender's risk if the company defaults on repayment or becomes insolvent. The two main types of security granted by companies over their assets are fixed charges and floating charges. Understanding their characteristics, creation, registration, and priority is essential for business law practitioners advising either lenders or borrowers. These forms of security have significant implications for the company's ability to deal with its assets and for the distribution of assets upon insolvency.

Companies and LLPs have access to floating charges in a way sole proprietors and ordinary partnerships do not. As a result, incorporated bodies often find it easier to raise debt capital because a lender can take a comprehensive “all‑assets” security package in a debenture comprising both fixed charges (over assets capable of control, such as land or heavy machinery) and floating charges (over fluctuating assets, such as stock and receivables). In smaller companies, lenders may also require director or shareholder personal guarantees to supplement security, which can diminish the practical protection of limited liability for those guarantors.

Test Tip: In SQE-style questions on Types of security (fixed and floating charges), identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Exam Warning: Do not rely on a familiar phrase from Types of security (fixed and floating charges) alone; check whether the facts satisfy every condition, exception, and timing requirement.

Fixed Charges

A fixed charge attaches to specific, identifiable assets owned by the company. These assets are typically tangible and relatively permanent, such as land, buildings, heavy machinery, or specific intellectual property rights like registered trademarks or patents.

Key Term: Fixed charge

A security interest granted over specific, ascertainable assets of a company. The company cannot deal with (e.g., sell or grant further charges over) the charged asset without the charge holder's consent.

The key feature of a fixed charge is the degree of control it gives the charge holder (the lender) over the specific asset. The company (the chargor) retains ownership and possession but loses the freedom to dispose of or otherwise deal with the asset in the ordinary course of business without the lender's permission. This lack of flexibility is a disadvantage for the company but provides strong security for the lender.

If the company defaults on the loan, the fixed charge holder has the right to take possession of the charged asset and sell it, using the proceeds to satisfy the debt owed. In an insolvency situation, the holder of a registered fixed charge has a high priority claim over the proceeds of sale of that specific asset, ranking ahead of floating charge holders and unsecured creditors.

Many secured lending transactions combine fixed charges over assets that are suitable for control (for example, real estate or large items of plant) with floating charges over other parts of the undertaking. A frequent area of exam focus is charges over book debts (trade receivables). Even if the instrument labels a charge over receivables as “fixed”, the courts look to substance: if the company is free to collect receivables and pay the proceeds into its general account to use in its business without restriction, the charge is likely to be a floating charge. Conversely, a genuine fixed charge requires real control by the lender over both the receivables and their proceeds (for example, a blocked account arrangement). This control analysis is important when determining priority on insolvency.

Key Term: Legal mortgage

The highest form of security over certain assets (including land), typically created by a charge by way of legal mortgage. It gives the mortgagee an immediate right to possession and, on default, to sell, with reconveyance of title when the debt is satisfied.

Fixed charges over land are often created by a legal mortgage executed as a deed. In addition to Companies House registration, mortgages and fixed charges over registered land must be protected at HM Land Registry to be effective against third parties dealing with the land. The lender will also expect covenants requiring the company to insure, maintain, and not dispose of the asset without consent.

Floating Charges

A floating charge is granted over a class of assets, both present and future, which may fluctuate in the ordinary course of the company's business. Examples include stock-in-trade, raw materials, cash at bank, and book debts (receivables).

Key Term: Floating charge

A security interest granted over a class of present and future company assets which, in the ordinary course of business, the company is free to deal with until crystallisation.

The defining characteristic of a floating charge is the company's freedom to deal with the assets within the charged class without needing the charge holder's consent. For example, a company can sell its stock, collect its debts, and use cash from its bank account as part of its normal trading activities. This flexibility is essential for the company's operations but presents a greater risk for the lender compared to a fixed charge, as the value and composition of the asset pool can change.

The floating charge 'floats' or 'hovers' over the identified class of assets until a specific event occurs which causes it to 'fix' or attach to the assets within that class as they exist at that moment. This process is known as crystallisation.

Key Term: Crystallisation

The event upon which a floating charge ceases to 'float' and attaches ('fixes') to the specific assets within the charged class at that time, restricting the company's ability to deal with them.

Crystallisation typically occurs upon:

- The company going into liquidation or administration.

- The appointment of a receiver (where permitted).

- The company ceasing to trade.

- Any other event specified in the charge document (the debenture), such as a payment default or breach of financial covenants.

Once crystallisation occurs, the floating charge effectively becomes a fixed charge over the assets then present in the class, and the company can no longer deal with them freely. Notably, floating charges rank behind certain other claims in insolvency, and the liquidator or administrator must carve out a statutory “prescribed part” from floating charge realisations for unsecured creditors (explained below).

Key Term: Book debts

Amounts owed to a company by its customers (trade receivables). They are frequently secured, either by a genuine fixed charge (where the lender exercises real control over collection and proceeds) or—more commonly—by a floating charge when the company collects and uses proceeds in the ordinary course of business. Key Term: Qualifying Floating Charge (QFC) holder

The holder of a floating charge which, by its terms, relates to the whole or substantially the whole of the company’s property and states statutory powers to appoint an administrator or administrative receiver. For charges created after 15 September 2003, a QFC holder can appoint an administrator out of court.

Worked Example 1.1

Innovate Ltd, a manufacturing company, grants a floating charge over its stock to SecureBank plc. The charge document states crystallisation will occur if Innovate Ltd defaults on loan repayments. Innovate Ltd sells finished goods from its stock daily. It then defaults on a loan repayment. What is the effect on the stock?

Answer:

Before the default, Innovate Ltd could freely sell its stock as part of its business. The default is a crystallisation event specified in the charge document. Upon default, the floating charge crystallises and becomes a fixed charge attaching to the stock held by Innovate Ltd at that precise moment. Innovate Ltd can no longer sell that stock without SecureBank plc's consent.

Creation and Registration of Charges

Both fixed and floating charges are typically created by deed, often contained within a document called a debenture.

Key Term: Debenture

A document issued by a company evidencing a debt, which often includes provisions creating fixed and/or floating charges over the company's assets as security for that debt.

A modern secured lending debenture will usually include:

- The security grants (fixed charges over controllable assets; a floating charge over the undertaking).

- Representations and warranties about title to assets and absence of prior charges.

- Covenants (negative pledges, information undertakings, restrictions on disposals, further assurances).

- Financial covenants and events of default (triggering enforcement or crystallisation).

- Powers of enforcement (including appointing an administrator or receiver, where applicable).

Key Term: Registration of charges

The process of filing particulars of a charge created by a company, together with the charging instrument, at Companies House within a statutory time limit (usually 21 days) to ensure its validity against third parties in insolvency.

For a charge created by a UK company to be valid against liquidators, administrators, and other creditors, it must be registered at Companies House. Section 859A of the Companies Act 2006 (CA 2006) requires that particulars of the charge, along with a certified copy of the instrument creating it (if any), must be delivered to the Registrar of Companies within 21 days beginning with the day after the date the charge is created. In practice, the lender’s lawyers will file form MR01 with the certified instrument and obtain confirmation of registration from the Registrar. The company must keep the instrument and any memorandum relating to the charge available for inspection (s 859Q CA 2006).

Fixed charges over registered land must also be protected at HM Land Registry to be effective against purchasers and other chargees. Registration at Companies House is not a substitute for Land Registry protection; both are required where the charged asset is land.

Key Term: Due diligence

The process by which a lender investigates a borrower’s title to assets, existing charges, corporate capacity and authority, and insolvency position before taking security. This typically includes Companies House searches, Land Registry searches, and winding‑up searches, and reviewing the articles for any restrictions on borrowing/security.

Directors should also verify they have authority under the company’s articles to borrow and grant security. Generally, model articles give directors broad management authority, but any bespoke restrictions must be considered. Section 39 and section 40 CA 2006 protect third parties dealing in good faith by ensuring acts are not called into question for lack of capacity and by deeming directors’ powers to bind the company to be free of constitutional limitations, but directors acting outside authority may nevertheless breach duties internally.

Consequences of Non-Registration

Failure to register a charge within the 21-day period has severe consequences under s 859H CA 2006:

- The charge becomes void against any liquidator, administrator, or creditor of the company.

- The security conferred by the charge is lost, meaning the lender becomes an unsecured creditor in relation to that debt as against the insolvent estate.

- The money secured by the charge becomes immediately payable by the company.

Even if a charge is void against the insolvency officeholder, the principal debt remains. In practice, careful transaction management is required to ensure timely filing; late registration cannot be cured by a court extension under current law. Where a charge has not been registered in time, parties sometimes restructure or take new security, but in insolvency the original unregistered security will not bind the officeholder.

Worked Example 1.2

BuildCo Ltd creates a fixed charge over its main office building in favour of Lender A on 1st March. On 10th March, it creates a floating charge over its stock in favour of Lender B. Lender A registers its charge on 25th March. Lender B registers its charge on 15th March. BuildCo Ltd goes into liquidation in June. What is the status of the charges?

Answer:

Lender B registered its floating charge within the 21-day limit (15th March is within 21 days of 10th March). Lender A failed to register its fixed charge within the 21-day limit (25th March is more than 21 days after 1st March). Therefore, Lender A's fixed charge is void against the liquidator and other creditors. Lender A becomes an unsecured creditor as against the insolvent estate. Lender B's floating charge is valid (assuming it met all other requirements).

Negative Pledge Clauses

Lenders taking a floating charge often seek to protect their position against subsequent fixed charges by including a negative pledge clause in the debenture.

Key Term: Negative Pledge Clause

A contractual clause in a floating charge document prohibiting the company from creating subsequent charges (especially fixed charges or other floating charges ranking equally or ahead) over the same assets without the floating charge holder's consent.

A negative pledge clause does not prevent the company from creating a later charge in breach of the clause. However, if the holder of the later charge (e.g., a fixed charge) had actual notice of the negative pledge clause when they took their charge, their charge will rank behind the floating charge, despite the usual priority rules. Constructive notice (e.g., simply because the floating charge containing the clause was registered) is generally not sufficient; actual knowledge is required. Registration of the charge document containing the negative pledge at Companies House makes it highly likely a subsequent lender conducting proper due diligence will have actual notice.

Worked Example 1.3

RetailCo grants a floating charge to Bank X containing a negative pledge. Six months later, RetailCo grants a fixed charge over its machinery to Bank Y. Bank Y’s lawyers obtained and reviewed RetailCo’s registered debenture before completion. RetailCo later enters administration. How do the charges rank?

Answer:

Bank Y had actual notice of Bank X’s negative pledge because it reviewed the registered debenture. Although a fixed charge would usually outrank a floating charge over the same assets, the negative pledge reverses the priority where there is actual notice. Bank Y’s fixed charge will be postponed to Bank X’s earlier floating charge.

Worked Example 1.4

TechCo grants a debenture (fixed and floating charges) to Lender Z on 1 February. The MR01 is not filed within 21 days. TechCo goes into liquidation in August. What is the effect of the late registration?

Answer:

The debenture is void against the liquidator and creditors under s 859H CA 2006. Lender Z loses security as against the insolvent estate and ranks as an unsecured creditor. The debt remains immediately payable, but the security cannot be enforced in the insolvency.

Worked Example 1.5

FinanceCo takes a “fixed charge” over Receivables Ltd’s book debts, allowing collection into Receivables Ltd’s normal trading account without any restrictions on use. On liquidation, Receivables Ltd argues that the charge is fixed and should outrank preferential debts. What is the likely analysis?

Answer:

Substance prevails over label. Because Receivables Ltd could collect receivables and use the proceeds freely in its business, the lender lacked the necessary control over the debts and their proceeds. The charge will be characterised as floating, ranking behind fixed charges, insolvency expenses, and preferential debts, and subject to the prescribed part.

Priority of Charges in Insolvency

The ranking of charges is critical when a company becomes insolvent, as it dictates the order in which creditors are paid from the proceeds of realised assets.

Key Term: Preferential creditors

Categories of creditors whose debts have statutory priority over floating charge holders and unsecured creditors. These include certain employee entitlements and, since December 2020, HMRC for certain taxes (VAT, PAYE income tax, employee NICs) on a secondary preferential basis. Key Term: Pari passu

A principle that unsecured creditors rank equally and share rateably in the insolvent estate where there are insufficient assets to pay them in full.

General Order of Priority:

- Fixed Charges: Holders of validly registered fixed charges are paid first from the proceeds of the specific assets over which their charge is held.

- Expenses of Insolvency: The costs and fees of the liquidator or administrator (in the order set by the Insolvency (England and Wales) Rules 2016).

- Preferential Creditors: Certain debts have statutory priority, including some employee entitlements (wages up to a limit, holiday pay) and certain sums due to HMRC (secondary preferential status for specified taxes from December 2020).

- Prescribed Part: A portion of the assets subject to floating charges set aside for unsecured creditors (see below).

- Floating Charges: Holders of validly registered floating charges are paid from the remaining assets subject to their charge, after the prescribed part is deducted. Charges rank in order of creation date, subject to registration and any subordination agreements or negative pledge effects.

- Unsecured Creditors: Paid from any remaining funds, including the prescribed part. They rank equally amongst themselves (pari passu).

- Shareholders: Receive any surplus after all other creditors are paid in full (rare in insolvency).

Floating charge holders may have extensive enforcement rights under the debenture, but since 15 September 2003 administrative receivership is largely restricted to charges created before that date. Qualifying floating charge holders under post‑2003 charges typically appoint administrators out of court instead, with administration objectives focused on rescue or achieving a better result than liquidation.

The Prescribed Part

Section 176A of the Insolvency Act 1986 requires a liquidator or administrator to set aside a 'prescribed part' of the company's net property (assets subject to floating charges, after costs of realisation and preferential debts) for the benefit of unsecured creditors. This fund is calculated as:

- 50% of the first £10,000 of net property available to floating charge holders; plus

- 20% of the net property above £10,000.

This is subject to a maximum cap (currently £800,000 for charges created on or after 6 April 2020; £600,000 for earlier charges). The prescribed part is paid to unsecured creditors before the floating charge holder receives payment from the remaining funds covered by their charge.

Key Term: Prescribed Part

A statutory fund carved out from assets subject to a floating charge in an insolvency, set aside for the benefit of unsecured creditors before the floating charge holder is paid.

Worked Example 1.6

Construct PLC is in liquidation. After paying insolvency expenses and preferential creditors, £100,000 remains available from assets covered only by a floating charge created in 2021. How much will be set aside as the prescribed part for unsecured creditors?

Answer:

- 50% of the first £10,000 = £5,000

- 20% of the remaining £90,000 (£100,000 - £10,000) = £18,000

- Total prescribed part = £5,000 + £18,000 = £23,000. This £23,000 will be made available to unsecured creditors. The floating charge holder will receive the remaining £77,000 (£100,000 - £23,000). Because the charge was created after 6 April 2020, the applicable cap is £800,000; the calculated amount here is below the cap.

Worked Example 1.7

Two fixed charges over the same machine are granted by Engineering Ltd to Bank A (January) and Bank B (March). Both are properly registered within 21 days and notified on Companies House. There is no subordination. Engineering Ltd goes into liquidation. Which charge has priority?

Answer:

Fixed charges on the same asset rank by order of creation (assuming both were registered in time). Bank A’s January charge takes priority over Bank B’s March charge, so sale proceeds will first satisfy Bank A; any surplus will then go to Bank B.

Avoidance of Floating Charges

Under Section 245 of the Insolvency Act 1986, a floating charge created within a certain period before the onset of insolvency may be invalid, except to the extent of any new money or value provided to the company at the time of, or after, the charge's creation. This prevents companies granting floating charges to secure past debts shortly before insolvency, potentially preferring one creditor over others.

Reasons for taking security and the principal insolvency effects of fixed and floating charges over company assets are summarised.

The relevant time period ('hardening period') is:

- 2 years ending with the onset of insolvency if the charge was granted to a person connected with the company (e.g., a director or group company). No insolvency condition needs to be proved for connected persons.

- 12 months ending with the onset of insolvency if the charge was granted to an unconnected person. For unconnected persons, the company must also have been insolvent at the time the charge was created, or become insolvent as a result of the transaction creating the charge.

Only the element of indebtedness representing “new money” advanced at the time of, or after, the charge is created is protected; the floating charge is invalid to the extent it secures pre‑existing debt.

Worked Example 1.8

In September, Director D loans £250,000 to Company C (no security). In April, C borrows a further £50,000 from D and grants D a floating charge over its undertaking to secure both loans. A winding‑up petition is presented in July. Is the floating charge valid?

Answer:

D is a connected person, and the charge was created within two years ending with the onset of insolvency. Under s 245 IA 1986, the floating charge is invalid except to the extent of “new money”. The April £50,000 is new value given at the time the charge was created and is protected; the earlier £250,000 is past indebtedness and is not protected by the new charge. The floating charge will therefore be valid only up to £50,000.

Enforcement and officeholder interaction

On default, security enforcement typically follows the terms of the debenture:

- A fixed charge holder may appoint an LPA (Law of Property Act 1925) receiver over land or require sale of the specific asset, applying proceeds to the debt.

- A qualifying floating charge holder can appoint an administrator out of court (subject to procedural notice to prior QFCs and to any pending insolvency petitions).

- Administrative receivership is generally limited to floating charges created before 15 September 2003; for later charges, appointment of an administrator is the usual route.

- In administration or liquidation, officeholder duties require maximising realisations and distributing by statutory priority; secured creditors’ rights are exercised within that framework, and floating charges are subject to the prescribed part.

Understanding the interaction between security rights and officeholders’ powers is essential for advising on timing (e.g., crystallisation triggers), notifications, and likely recoveries.

Summary

Fixed vs Floating Charges

| Feature | Fixed Charge | Floating Charge |

|---|---|---|

| Attachment | Specific, identifiable assets | Class of fluctuating assets (present & future) |

| Control | Company cannot deal with asset without consent | Company free to deal with assets in ordinary course of business until crystallisation |

| Crystallisation | Not applicable (already fixed) | Attaches to specific assets upon certain events (e.g., insolvency) |

| Registration | Required (within 21 days of creation) | Required (within 21 days of creation) |

| Priority (General) | High (paid first from specific asset proceeds) | Lower (paid after fixed charges, expenses, preferential debts, prescribed part) |

| Flexibility | Low for company | High for company |

| Lender Risk | Lower | Higher |

Key Point Checklist

This article has covered the following key knowledge points:

- Fixed charges attach to specific assets, restricting the company's ability to deal with them, while floating charges cover a class of changing assets, allowing the company operational freedom until crystallisation.

- For receivables, a valid fixed charge requires genuine lender control over collection and proceeds; otherwise the charge is likely to be floating.

- Crystallisation converts a floating charge into a fixed charge, typically upon insolvency events or specified events of default.

- Both fixed and floating charges must be registered at Companies House within 21 days of creation under the Companies Act 2006 to be valid against liquidators, administrators, and other creditors; fixed charges over land must also be protected at HM Land Registry.

- Failure to register a charge within the time limit renders it void against these parties, and the secured debt becomes immediately payable; the lender will rank unsecured as against the insolvent estate.

- In insolvency, fixed charges generally have priority over floating charges regarding the specific assets charged; floating charges rank behind insolvency expenses and preferential debts and are subject to the prescribed part.

- Floating charge proceeds are subject to deductions for insolvency expenses, preferential debts, and the 'prescribed part' set aside for unsecured creditors before the floating charge holder is paid.

- A negative pledge clause in a floating charge can affect the priority of subsequent charges if the later charge holder has actual notice.

- Floating charges created shortly before insolvency for past debt may be invalidated under s 245 Insolvency Act 1986, although protection remains for “new money” introduced when the charge is granted.

- Qualifying floating charge holders can appoint administrators out of court; administrative receivership is largely restricted to pre‑15 September 2003 charges.

Key Terms and Concepts

- Fixed charge

- Floating charge

- Crystallisation

- Debenture

- Registration of charges

- Negative Pledge Clause

- Prescribed Part

- Legal mortgage

- Book debts

- Qualifying Floating Charge (QFC) holder

- Preferential creditors

- Pari passu

- Due diligence