Learning Outcomes

This article outlines the principal CGT reliefs and exemptions for individuals and business owners, including:

- the qualifying conditions for Business Asset Disposal Relief (BADR) on disposals of all or part of a business, shares in a personal company, and associated disposals of personally owned business assets, and how to identify a qualifying business disposal in exam-style scenarios

- the scope, restrictions, and main conditions of hold-over relief (including eligible assets, the requirement for a joint claim, and typical disqualifying situations) and how the deferred gain adjusts the recipient’s base cost

- how rollover relief operates in practice, including qualifying assets, the reinvestment window, partial reinvestment, and the special treatment for depreciating assets where gains are held over rather than immediately deducted from base cost

- the function of the annual exempt amount (AEA), its current level for the 2023/24 and 2024/25 tax years, when it can be set against gains, and the correct order of applying reliefs and the AEA in CGT computations

- the interaction of these reliefs with standard and residential property CGT rates, claim time limits, basic computation steps, and common pitfalls in combining BADR, hold-over relief, rollover relief, and the AEA in SQE1 multiple-choice questions

- the ability to compare when to use deferral reliefs versus claiming BADR immediately, and to spot where reliefs are not available due to non-trading or investment assets

SQE1 Syllabus

For SQE1, you are required to understand the principal CGT reliefs and exemptions available to individuals and businesses, with a focus on the following syllabus points:

- the operation and conditions of Business Asset Disposal Relief (BADR)

- the requirements and effect of hold-over relief for gifts of business assets

- the application of rollover relief for reinvestment in qualifying business assets

- the annual exempt amount and its use in CGT calculations

- the interaction and order of application of these reliefs and exemptions

- associated disposals for BADR and the two-year ownership/employment conditions

- partial reinvestment and depreciating assets rules under rollover relief

- claim time limits and practical computation steps

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the maximum lifetime gain that can qualify for Business Asset Disposal Relief, and what is the CGT rate applied?

- Which relief allows a capital gain to be deferred when a business asset is gifted, and what is the main condition for this relief?

- How does rollover relief operate when a business reinvests proceeds from a qualifying asset into a new asset?

- What is the annual exempt amount for individuals for CGT in the 2023/24 tax year, and can it be carried forward if unused?

Introduction

Capital gains tax (CGT) is charged on the profit made when certain assets are disposed of. However, several reliefs and exemptions can reduce the tax rate or defer the charge. For SQE1, you must be able to identify when these reliefs apply, calculate the effect on the taxable gain, and understand their interaction and the correct order of application. This article covers the main reliefs and exemptions: Business Asset Disposal Relief, hold-over relief, rollover relief, incorporation relief, and the annual exempt amount.

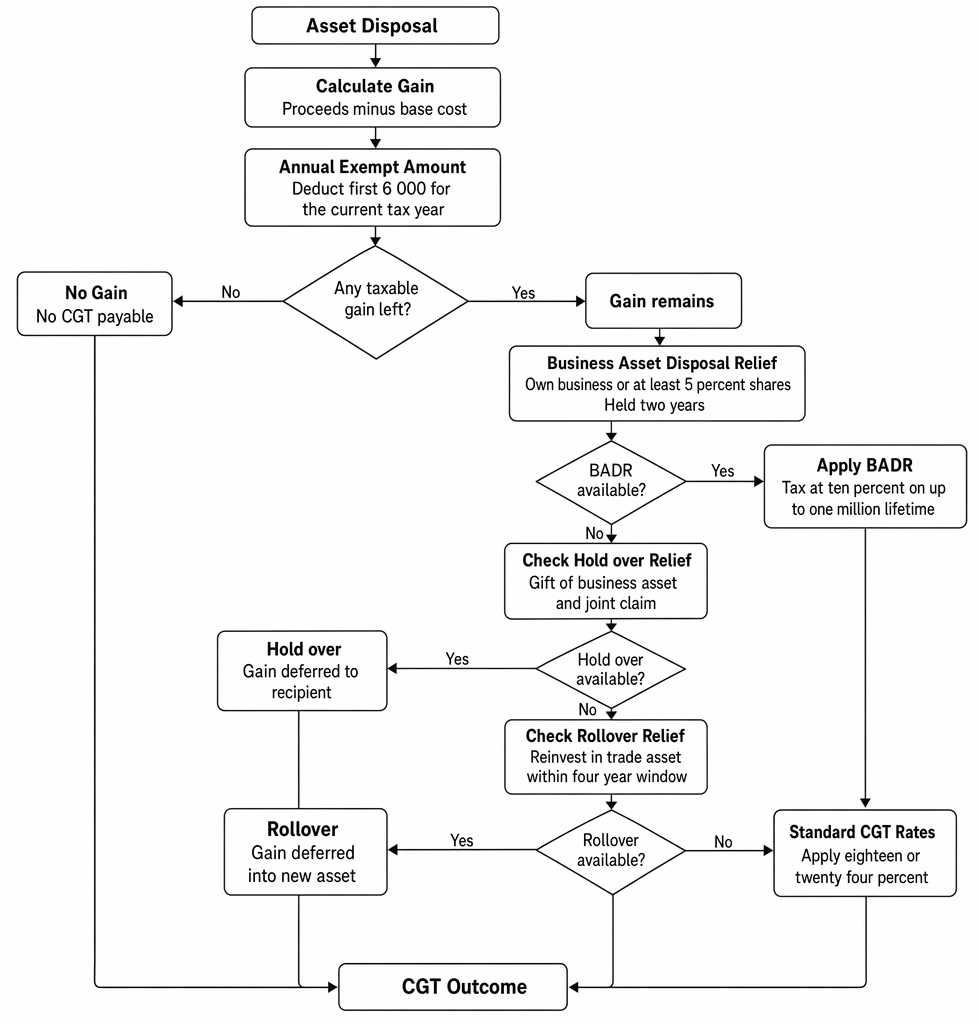

Capital gains tax outcomes after disposal are summarised by reference to annual exemption, BADR, hold-over relief, rollover relief, and standard rates.

Key Term: chargeable gain

The net gain on a disposal of a chargeable asset after deducting allowable costs and applying any reliefs and exemptions. Key Term: qualifying business disposal (QBD)

A disposal that can qualify for BADR: disposal of all or part of a business, shares/securities in a personal trading company, or certain associated disposals of assets used in that business. Key Term: personal company

For BADR, a company where the disposer holds at least 5% of the ordinary share capital with at least 5% of voting rights and an economic entitlement (generally at least 5% to profits/assets or sale proceeds) and is an employee or office holder. Key Term: depreciating asset (rollover relief)

A replacement asset expected to have a life of less than 50 years (e.g. certain plant or machinery). For such assets, gains are held over and crystallise later rather than reducing base cost immediately.

CGT rates for individuals depend on total taxable income and the asset type. Following the alignment under the Autumn Budget 2024, main rates on all assets (residential and non-residential) are 18% within any unused basic rate band and 24% above it; the legacy 10%/20% main rates applied to non-residential disposals before 30 October 2024, and the historic 28% upper residential rate fell to 24% from 6 April 2024. Gains qualifying for BADR are taxed at the BADR rate (10% before 6 April 2025, 14% in 2025/26, 18% from 6 April 2026) up to the £1 million lifetime limit. Trustees and personal representatives pay at 24%.

Test Tip: In SQE-style questions on Main reliefs and exemptions, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Business Asset Disposal Relief (BADR)

Business Asset Disposal Relief (BADR), formerly Entrepreneurs’ Relief, reduces the CGT rate on qualifying business disposals, up to a lifetime limit. The BADR rate has risen on a phased basis: 10% for disposals before 6 April 2025, 14% in 2025/26, and 18% from 6 April 2026.

Key Term: Business Asset Disposal Relief (BADR)

A relief reducing CGT on qualifying business disposals, subject to a £1 million lifetime limit and strict conditions. The applicable BADR rate is 18% from 6 April 2026 (10% before 6 April 2025; 14% in 2025/26). Key Term: associated disposal (BADR)

A disposal of an asset owned personally but used in a business by the individual’s company or partnership. It may qualify for BADR if made in association with a qualifying disposal of shares/partnership interest and certain conditions (including a reduction of at least 5% of the individual’s interest) are met.

To qualify for BADR, the disposal must be of one of the following and each has specific conditions:

-

all or part of a business carried on by the individual as a sole trader or as a partner, provided the business (or the part being disposed of) has been owned for at least two years before disposal

-

shares or securities in a personal trading company (or holding company of a trading group) where, for at least two years before disposal, the individual:

- holds at least 5% of ordinary share capital and at least 5% of voting rights, and

- meets an economic entitlement test (e.g. 5% of profits/assets on a winding-up or at least 5% of sale proceeds), and

- is an employee or office holder of the company or holding company

-

associated disposals of assets owned personally but used in the business (e.g. a building owned personally and used by the company), provided the asset has been owned for at least three years and used by the business for at least two years prior to disposal, and the associated disposal occurs when the individual reduces their share in the company/business by at least 5%

The maximum lifetime gains eligible for BADR is £1 million. Claims must be made on or before the first anniversary of 31 January following the tax year of disposal. BADR applies to gains; allowable losses and the annual exempt amount can be set against gains, but note the correct order of application is critical (see Interaction and Order of Application).

Worked Example 1.1

Question: Sarah has run a bakery as a sole trader for 10 years. She sells the business, making a gain of £600,000. She has never claimed BADR before. What CGT rate applies?

Answer:

Sarah can claim BADR, so the £600,000 gain is taxed at the BADR rate in force for the tax year of disposal (10% before 6 April 2025, 14% in 2025/26, 18% from 6 April 2026), not at the main 18%/24% rates.

Worked Example 1.2

Question: Amir, a director-employee, sells shares in his personal trading company. He meets the 5% voting and economic entitlement tests for the last two years. His total gain is £1.2 million, and he has not previously claimed BADR. How is the gain taxed?

Answer:

Amir can claim BADR on up to £1,000,000 of lifetime qualifying gains at the prevailing BADR rate (18% from 6 April 2026). The remaining £200,000 is taxed at the main rates for shares (18% in any unused basic rate band, 24% above it).

Worked Example 1.3

Question: Priya personally owns a warehouse used by her trading company. She sells 10% of her shareholding and simultaneously sells the warehouse, which has been owned for 5 years and used by the company for the last 3 years. BADR conditions for shares are met. Is the warehouse disposal eligible for BADR?

Answer:

Yes. The warehouse is an associated disposal: it has been owned and used for the required periods and Priya reduces her interest in the company by at least 5% on a qualifying disposal. Subject to other conditions, the gain on the warehouse can qualify for BADR at the prevailing BADR rate (18% from 6 April 2026).Exam Warning: BADR is only available if all conditions are met at the date of disposal and for the full qualifying period. For shares, check the 5% holding, voting and economic entitlement tests, and the employment/office holder requirement, all for at least two years before disposal. For associated disposals, do not overlook the three-year ownership/two-year use conditions and the minimum 5% reduction in the interest in the business/company.

Hold-Over Relief

Hold-over relief allows a gain on the gift of certain business assets to be deferred until the recipient disposes of the asset.

Key Term: hold-over relief

A relief deferring CGT on the gift (or sale at undervalue) of qualifying business assets. The deferred gain reduces the recipient’s base cost; CGT arises when the recipient disposes of the asset.

Hold-over relief is available when all main conditions are met:

- the asset is gifted or sold at undervalue, and is a qualifying business asset

- both donor and recipient make a joint claim to HMRC within the time limit (normally within four years from the end of the tax year of the gift)

- the asset is used in a trade, or the shares are in a trading company (typically unlisted shares in a trading company or the holding company of a trading group)

- the donor’s gain is deferred and deducted from the recipient’s base cost; CGT is paid by the recipient when they later dispose of the asset

Qualifying business assets for hold-over relief typically include:

- land and buildings used in the donor’s trade

- goodwill of an unincorporated business

- unlisted shares or securities in a trading company (or holding company of a trading group)

Relief is generally not available for gifts of non-business assets (e.g. investment properties) or for shares in investment companies (e.g. companies whose main activity is holding investments or letting property). Special rules apply to gifts to trusts (separate hold-over provisions can apply to chargeable transfers to certain trusts), but in all cases a joint claim and the trading nature of the asset/class must be satisfied.

The deferred gain can never reduce the recipient’s base cost below zero; any excess would be immediately chargeable.

Worked Example 1.4

Question: Tom gifts shares in his family trading company to his daughter. The shares have a gain of £100,000. They claim hold-over relief. What is the effect?

Answer:

Tom pays no CGT now. The £100,000 deferred gain is deducted from his daughter’s base cost. She will pay CGT on this gain when she sells the shares.

Worked Example 1.5

Question: Maria gifts shares in a company which holds residential rental properties (an investment company). The shares have a gain of £80,000. Can they claim hold-over relief?

Answer:

No. Hold-over relief requires business assets. Shares in a property investment company are not shares in a trading company, so hold-over relief is not available. Maria is liable to CGT on the £80,000 gain at the time of the gift.

Rollover Relief

Rollover relief allows a business to defer a gain when proceeds from a qualifying asset are reinvested in a new qualifying asset.

Key Term: rollover relief

A relief deferring CGT when a gain from a qualifying business asset is reinvested in a new qualifying asset within a set period, by reducing the base cost of the replacement asset (or holding over the gain for depreciating assets).

The main conditions are:

-

the old asset and the new asset must be qualifying business assets used in the trade

- for individuals/partnerships, common qualifying assets include land and buildings, fixed plant and machinery, and goodwill of a trade

- for companies, qualifying assets include land and buildings and certain other assets used in the trade; goodwill and most other intangible assets are subject to separate corporation tax rules (outside CGT)

-

the replacement asset must be acquired within one year before or three years after the disposal of the old asset (HMRC may extend by concession in limited cases)

-

a claim must be made (typically within four years of the end of the tax year in which the later of the disposal or acquisition occurs)

-

the gain is deducted from the base cost of the new asset; CGT is paid when the new asset is subsequently disposed of

Partial reinvestment:

- if only part of the proceeds is reinvested, the portion not reinvested is immediately chargeable, with only the reinvested portion eligible for deferral

Depreciating assets:

- if the replacement asset is a depreciating asset, the gain is not deducted from base cost immediately; instead, it is held over and crystallises on the first of: disposal of the replacement asset, ten years after acquisition, or when the asset ceases to be used in the trade

Worked Example 1.6

Question: A partnership sells a delivery van for a gain of £20,000 and buys a new van for the same trade within two years. What is the effect if they claim rollover relief?

Answer:

The £20,000 gain is deducted from the base cost of the new van (or held over if the van is a depreciating asset under the rules). CGT is paid when the new van is later sold or when the hold-over period ends.

Worked Example 1.7

Question: Lara sells a workshop for £200,000, realising a £60,000 gain after costs. Within three years, she reinvests £140,000 in a new qualifying workshop and keeps £60,000 of proceeds. How much gain is immediately chargeable and how much can be rolled over?

Answer:

The unreinvested £60,000 is immediately chargeable. The £60,000 reinvested gain is eligible for rollover into the new workshop’s base cost (subject to claim and conditions).

Worked Example 1.8

Question: Ben sells a warehouse (gain £50,000). Within one year, he buys fixed plant expected to last 20 years (a depreciating asset) for use in the trade. How is the £50,000 gain treated?

Answer:

As the replacement is a depreciating asset, Ben cannot reduce base cost immediately. Instead, the £50,000 gain is held over and will crystallise on the first of: disposal of the plant, ten years from acquisition, or cessation of use in the trade. Another business deferral relief worth recognising is incorporation relief. Where a sole trader or partnership transfers a business as a going concern to a company in exchange for shares, the gains on the transferred assets can be rolled into the base cost of the shares received. If any part of the consideration is taken in cash or other non-share form, relief is restricted and the non-share element may trigger an immediate charge.

Key Term: incorporation relief

Relief that defers gains arising on the transfer of a business to a company where the business is transferred as a going concern and the consideration consists wholly or partly of shares. The deferred gain reduces the base cost of the shares received.

The Annual Exempt Amount

Each individual has an annual exempt amount for CGT. Gains up to this amount are tax-free, but it cannot be carried forward if unused.

Key Term: annual exempt amount

The annual CGT allowance for individuals. Gains up to this amount are exempt from CGT in the tax year; it cannot be carried forward.

From 2024/25 onwards (including 2026/27) the annual exempt amount for individuals is £3,000, having been cut from £6,000 in 2023/24 and £12,300 in 2022/23. Trustees generally have a lower exempt amount (commonly half the individual figure, shared across same-settlor trusts). It cannot be carried forward if unused.

Important interaction rule: the annual exempt amount can only be used against gains that remain chargeable after losses and any deferral reliefs have been applied. It cannot be applied to gains that are deferred or held over/rolled over (e.g. hold-over relief, rollover relief, incorporation relief). BADR does not defer the gain; it changes the rate on qualifying gains. Accordingly, once deferred gains have been taken out of the year’s computation, the annual exempt amount is deducted from the gains that remain chargeable and the appropriate BADR or main rate is then applied to what is left.

Worked Example 1.9

Helen sells shares and makes a gain of £5,000 in 2023/24. What is her CGT liability?

Answer:

The gain (£5,000) is below the 2023/24 annual exempt amount of £6,000, so no CGT is due. Note that from 2024/25 the AEA is just £3,000, so the same gain in a later year would leave £2,000 chargeable.

Worked Example 1.10

Question: Jake, a higher rate taxpayer, sells a holiday home in 2024/25, making a chargeable gain (after allowable costs) of £185,700. The annual exempt amount is £3,000. What CGT applies (ignoring any losses)?

Answer:

Deduct the annual exempt amount (£3,000) to get a chargeable gain of £182,700. The historic 28% residential rate was reduced to 24% from 6 April 2024, so for a 2024/25 disposal Jake pays £182,700 × 24% = £43,848. (For an equivalent disposal from 30 October 2024, the same 24% upper rate applies because residential and non-residential rates are now aligned.)

Interaction and Order of Application

When more than one relief or exemption applies, the correct order of application is essential. In CGT computations:

- identify chargeable disposals and compute basic gains after allowable expenditure (including acquisition/incidental costs and enhancement expenditure), netting off allowable losses

- apply reliefs that defer gains (e.g. rollover relief, hold-over relief, incorporation relief). Deferred gains do not count towards chargeable gains for the current year

- deduct the annual exempt amount from the gains that remain chargeable for the year

- apply the BADR rate to any qualifying gains that remain within the lifetime limit, and the relevant main CGT rates to the balance

Worked Example 1.11

Mark sells qualifying business assets for a gain of £1,020,000. He has not used his annual exempt amount. What is his CGT position?

Answer:

BADR applies to qualifying gains up to the £1,000,000 lifetime limit. Because BADR already gives the lowest available rate, the sensible use of the £3,000 AEA is against the remaining £20,000 non-BADR gain. Tax the first £1,000,000 at the prevailing BADR rate (18% from 6 April 2026, so £180,000). The remaining £20,000 is a normal gain: deduct the £3,000 AEA and apply main rates of 18%/24% to the £17,000 balance, depending on where that gain falls relative to any unused basic rate band.

Worked Example 1.12

Question: Ella sells a shop (gain £70,000) and reinvests all proceeds in a new shop within two years. In the same tax year, she also sells shares in her personal company (qualifying gain £200,000 under BADR; lifetime limit unused). She has no losses and has not used her annual exempt amount. How do the reliefs interact?

Answer:

First, claim rollover relief on the £70,000 shop gain, deferring it into the new shop’s base cost (no current-year tax or AEA usage on this gain). Ella is then left with the £200,000 BADR-qualifying share gain as the only chargeable gain for the year. Deduct the £3,000 annual exempt amount from that gain, leaving £197,000 taxed at the prevailing BADR rate (18% from 6 April 2026), so the CGT is £35,460.

Key Point Checklist

This article has covered the following key knowledge points:

- Business Asset Disposal Relief reduces CGT on qualifying business disposals, subject to a £1 million lifetime limit and strict conditions (including a two-year ownership/employment requirement and 5% tests for shares); the BADR rate is 18% from 6 April 2026 (10% before 6 April 2025, 14% in 2025/26).

- Associated disposals can qualify for BADR where personally owned assets used in the business are disposed of in association with a qualifying share/interest disposal and required ownership/use and reduction tests are met.

- Hold-over relief defers CGT on gifts (and sales at undervalue) of business assets such as land/buildings used in trade and unlisted shares in a trading company; a joint claim is required. The gain reduces the recipient’s base cost.

- Rollover relief defers CGT when proceeds from a qualifying asset are reinvested in a new qualifying asset within the one-year-before/three-years-after window. Partial reinvestment creates an immediate charge on the unreinvested portion.

- For depreciating replacement assets, gains are held over and crystallise later rather than reducing base cost immediately.

- Incorporation relief can defer gains where a business is transferred as a going concern to a company in exchange for shares; any non-share consideration can create an immediate charge.

- The annual exempt amount (AEA) for individuals has been £3,000 since 2024/25 (and remains £3,000 for 2026/27); it cannot be carried forward and can only be used against gains on which tax would otherwise be paid (not deferred gains).

- Apply deferral reliefs first, then deduct the annual exempt amount from the gains that remain chargeable, and finally apply the BADR or main CGT rates to the balance.

Key Terms and Concepts

- chargeable gain

- qualifying business disposal (QBD)

- personal company

- associated disposal (BADR)

- Business Asset Disposal Relief (BADR)

- hold-over relief

- rollover relief

- depreciating asset (rollover relief)

- annual exempt amount