Learning Outcomes

This article explains the principal methods available to a judgment creditor seeking to enforce money judgments in England and Wales, including:

- the core enforcement options under the Civil Procedure Rules and related legislation, and how they fit within the wider enforcement framework;

- how to select an appropriate enforcement route by analysing the debtor’s asset profile, income stream, solvency and employment status;

- the structure, procedure and strategic use of Taking Control of Goods, Charging Orders, Third Party Debt Orders and Attachment of Earnings Orders;

- the two-stage nature of Charging Orders and Third Party Debt Orders, and the distinct functions of interim and final orders in each remedy;

- pre-enforcement information-gathering tools, particularly orders to obtain information under CPR Part 71, and how they support reasoned method choice;

- the differences between County Court and High Court enforcement, including when transfer up is available and the role of High Court Enforcement Officers;

- the treatment and calculation of interest on judgment debts, and how different enforcement routes affect interest accrual and recovery;

- practical and ethical considerations when combining enforcement methods or using insolvency procedures as enforcement leverage, with a focus on SQE1 exam-style scenarios and common pitfalls.

SQE1 Syllabus

For SQE1, you are required to understand the enforcement of money judgments in England and Wales, with a focus on the following syllabus points:

- the distinction between High Court and County Court enforcement procedures

- orders to obtain information under CPR Part 71 (formerly ‘oral examination’)

- the scope and limitations of Taking Control of Goods (including exempt goods and controlled goods agreements)

- the process for obtaining Charging Orders and their effect, including interim and final stages and registration

- how Third Party Debt Orders operate, particularly against bank accounts and issues with joint accounts and overdrafts

- the requirements and variations for Attachment of Earnings Orders, including protected earnings rate

- interest on judgment debts in the High Court and County Court, and how enforcement affects interest accrual

- the use of insolvency procedures as a means of enforcement pressure, including statutory demands and thresholds

- combining enforcement methods and when court permission is needed

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A judgment creditor wishes to enforce a £4,000 County Court judgment. Which enforcement method involving the seizure of goods is available?

- a) Writ of control

- b) Warrant of control

- c) Charging Order

- d) Third Party Debt Order.

-

Which of the following assets would typically be considered 'exempt goods' and therefore protected from seizure under Taking Control of Goods regulations?

- a) A second television set used occasionally in a spare room.

- b) A van essential for the debtor's sole trader business, valued at £1,000.

- c) Antique jewellery inherited by the debtor.

- d) A laptop primarily used for personal entertainment.

-

A creditor obtains a final Charging Order over a debtor's residential property. What does this order directly allow the creditor to do?

- a) Immediately evict the debtor and sell the property.

- b) Receive payments directly from the debtor's employer.

- c) Secure the debt against the property, affecting future sale proceeds.

- d) Freeze the debtor's main bank account.

-

A Third Party Debt Order is sought against funds held in a debtor's bank account. Who are the main parties notified when an interim order is made?

- a) The judgment creditor and the court only.

- b) The judgment debtor and the third party (the bank).

- c) The judgment creditor and the judgment debtor only.

- d) The third party (the bank) and the court only.

Introduction

Obtaining a court judgment is often only the first step for a successful claimant (judgment creditor). If the defendant (judgment debtor) fails to pay the amount awarded, the judgment creditor must take further steps to enforce the judgment. Enforcement refers to the legal processes used to compel payment or compliance with a court order. Choosing the correct method depends on the debtor’s assets, income, and solvency and often starts with gathering reliable information about those matters.

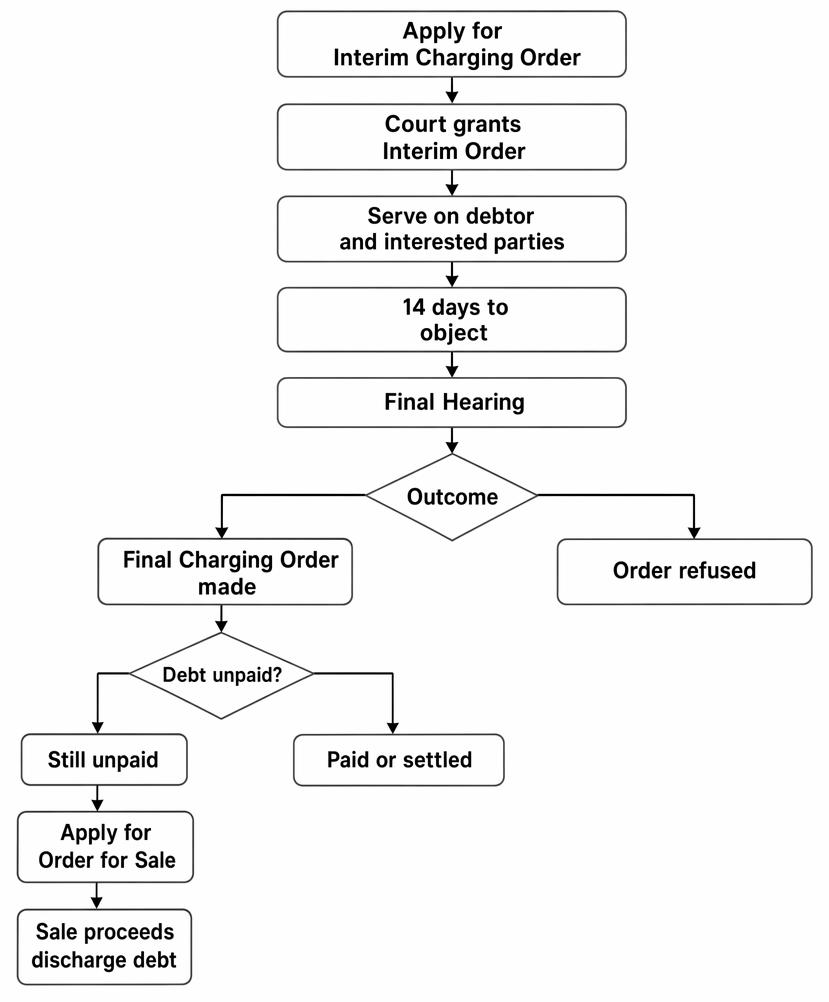

Charging order procedure from application for an interim order to final order and, if the debt remains unpaid, an order for sale.

Key Term: Judgment creditor

The party who has obtained a court judgment in their favour for a sum of money. Key Term: Judgment debtor

The party against whom a court judgment for a sum of money has been made.

The rules governing enforcement of money judgments are primarily found in the Civil Procedure Rules (CPR) Parts 70-73 (general enforcement framework; third party debt and charging orders), Part 71 (orders to obtain information), Part 83-84 (taking control of goods), and Part 89 (attachment of earnings), together with the Tribunals, Courts and Enforcement Act 2007 (TCEA 2007) and regulations made under it.

Judgments up to £5,000 are typically enforced in the County Court, while High Court judgments (or County Court judgments over £600 transferred up) can utilise High Court Enforcement Officers (HCEOs). Judgments for £5,000 or more can generally be transferred from the County Court to the High Court for enforcement without needing the court's permission (subject to exceptions). Consumer Credit Act–regulated agreements must be enforced in the County Court regardless of amount.

Key Term: Interest on judgment debts

Statutory interest payable on a judgment debt. High Court judgments carry interest at 8% per annum under s.17 Judgments Act 1838. County Court judgments may carry interest under s.74 County Courts Act 1984 and the County Courts (Interest on Judgment Debts) Order 1991 (usually at 8% for judgments of £5,000 or more or where contract/statute provides otherwise).Test Tip: In SQE-style questions on Methods of enforcement, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Obtaining information from the judgment debtor (Part 71)

Before choosing an enforcement method, creditors often need reliable information about a debtor’s assets and means. CPR Part 71 enables an order requiring the debtor (or, for corporate debtors, an officer of the company) to attend court to provide information on oath to assist enforcement.

Key Term: Order to obtain information

A court order under CPR Part 71 requiring a judgment debtor (or a company officer) to attend court and answer questions on oath about assets, income, employment, bank accounts and other matters relevant to enforcement.

Applications are made without notice using Form N316 (individual debtor) or N316A (company officer), issued in the court that made the judgment. Service must normally be personal and at least 14 days before the hearing. Failure to attend or to answer questions may result in committal proceedings. The information obtained helps the creditor assess the viability of each enforcement method.

Taking Control of Goods (TCG)

This is a common method allowing enforcement agents (HCEOs or County Court bailiffs) to seize the judgment debtor's goods and sell them to satisfy the debt. The procedure is governed by Schedule 12 to the TCEA 2007 and the Taking Control of Goods Regulations 2013.

Key Term: Taking Control of Goods (TCG)

The statutory process allowing enforcement agents to seize a debtor's goods for sale to recover a judgment debt. Replaces the older terms 'distress' and 'execution'.

The enforcement agent must give the debtor at least 7 clear days' notice of their intention to enter premises to take control of goods (the 'Notice of Enforcement'). Entry must usually be peaceful and between 6 am and 9 pm, and may be to places where the debtor lives or carries on a trade or business. Reasonable force may be permitted in limited circumstances set by the TCEA and CPR, typically for certain business premises.

Crucially, certain goods are protected from seizure.

Key Term: Exempt goods

Goods protected by law from being taken by enforcement agents. Includes items necessary for the debtor's basic domestic needs (clothing, bedding, basic furniture, cooker etc.) and tools, vehicles and equipment necessary for the debtor’s personal employment, business, or education up to an aggregate value of £1,350.

Goods owned solely by third parties cannot be taken. Co-owned goods may be seized, but the co-owner can claim a share of sale proceeds. Items subject to hire-purchase or lease are typically not the debtor’s property and are outside scope, subject to complex ownership terms. If goods are taken, they are typically sold at public auction unless the court orders an alternative sale method. Sale proceeds are applied to enforcement costs and the judgment, with any surplus returned to the debtor.

High Court enforcement uses a writ of control, whereas County Court enforcement uses a warrant of control.

Key Term: Writ of control

A High Court command directing an HCEO to take control of a judgment debtor's goods to satisfy a judgment debt. Key Term: Warrant of control

A County Court command directing a County Court bailiff to take control of a judgment debtor's goods to satisfy a judgment debt. Key Term: High Court Enforcement Officer (HCEO)

A court-appointed enforcement officer authorised to execute High Court writs, including writs of control, to enforce judgments and orders. Key Term: Controlled goods agreement

An agreement under which the enforcement agent leaves seized goods in the debtor’s custody on terms that the debtor will not dispose of them and will pay as agreed. Breach allows removal and sale.

Choice of court and instrument depends on judgment amount and nature:

- less than £600: County Court warrant of control

- £600 or more but under £5,000: County Court warrant or transfer to High Court for writ of control

- £5,000 or more: High Court writ of control (except for Consumer Credit Act–regulated debts, which must remain in County Court)

Worked Example 1.1

A judgment creditor has a High Court judgment for £10,000 against Ben, a self-employed plumber. Ben owns two vans; one worth £8,000 used daily for work, and an older one worth £1,500 used for spares. Can the HCEO take control of both vans?

Answer:

The HCEO can likely take control of the older van (£1,500). The main work van (£8,000) is likely essential for Ben's business. As its value exceeds the £1,350 limit for tools of the trade, it is not automatically exempt, but the HCEO must consider the proportionality of seizing an essential tool. However, the second van is unlikely to be considered essential and can be taken.

Additional practical points on TCG

- Notice of enforcement must be served giving 7 clear days before attendance (excluding date of service and the day of attendance).

- Entry is generally peaceful; forced entry powers are narrow and more commonly relevant to certain commercial premises without living accommodation.

- If a third party claims ownership of seized goods, the agent must be notified promptly; disputes can be resolved by the court and may stay sale pending determination.

- Enforcement can be combined with other methods (e.g., a charging order), but permission is required to enforce by taking control of goods if an attachment of earnings order is already in force.

Charging Orders

A Charging Order secures the judgment debt against the debtor's beneficial interest in assets, most commonly land or property, but also securities like shares. It operates like a mortgage, meaning if the asset is sold, the judgment creditor is paid out of the proceeds (after any prior secured creditors). The procedure is governed by CPR Part 73 and the Charging Orders Act 1979.

Key Term: Charging Order

A court order securing a judgment debt against a debtor's interest in specified property (e.g., land, shares).

The process involves two stages:

Key Term: Interim Charging Order

An initial order (often without notice) that temporarily charges the debtor’s interest in the property and prevents disposal pending a final decision. It must be served on the debtor and relevant third parties. Key Term: Final Charging Order

The order made after consideration of any objections, permanently securing the judgment debt against the debtor’s charged interest until satisfied or discharged.

Once an interim order is granted, it must be served on the debtor and on relevant third parties such as co-owners, mortgagees, or company registrars (for securities). The debtor can object within the time specified, and the court will then decide whether to make the order final. A Charging Order should be registered: against registered land at the Land Registry and, for unregistered land, in the Land Charges Department; charges over securities follow company registrar or CREST procedures.

A Charging Order does not itself force a sale. The creditor must make a separate application for an order for sale if they wish to compel the sale of the property. Courts have discretion and consider factors such as whether it is a family home, the interests of other occupiers (including children), proportionality, and the amount of equity, before deciding whether to order sale.

Key Term: Order for Sale

A separate court order, applied for after obtaining a final Charging Order, which compels the sale of the charged property to satisfy the debt.

Charging orders on jointly owned property attach to the debtor’s beneficial interest only. Upon sale, the charging creditor is paid from the debtor’s share of net proceeds after prior charges and costs. For securities, transfer or realisation mechanisms depend on the type of security and registry rules.

Worked Example 1.2

Chloe has a £25,000 judgment against David, who jointly owns his house (worth £300,000, mortgage £150,000) with his wife. Chloe obtains a final Charging Order against David's beneficial interest. Can she immediately force the sale of the house?

Answer:

No. The final Charging Order secures the debt against David's share of the equity. To force a sale, Chloe must apply for a separate Order for Sale. The court will consider all circumstances, including the fact it is jointly owned and is likely the family home, and the amount of equity available for David after the mortgage. Sale is not guaranteed.

Third Party Debt Orders (TPDO)

This method allows a judgment creditor to intercept money owed to the judgment debtor by a third party. The most common use is to obtain funds held in the debtor's bank or building society account. The procedure is under CPR Part 72.

Key Term: Third Party Debt Order (TPDO)

A court order requiring a third party who owes money to the judgment debtor (e.g., a bank) to pay that money directly to the judgment creditor instead.

Similar to Charging Orders, there is a two-stage process:

- Interim TPDO: An initial order served on the third party (e.g., the bank) freezing the amount in the debtor's account up to the judgment amount at the time of service, and notifying the debtor. Only sums standing to the debtor’s credit when the bank is served are caught. Overdraft facilities cannot be attached.

- Final TPDO: After the debtor and third party have an opportunity to respond, the court decides whether to order the third party to pay the frozen funds to the creditor. The debtor may object on grounds such as the funds belonging to someone else or being exempt (e.g., trust funds).

Banks are only required to ring-fence and pay funds actually available in the account at the time the interim order is served, up to the judgment amount. Joint accounts present complexities; TPDOs may be granted, but only the debtor’s beneficial share of the joint balance can be attached, which can be contentious and may require evidence on shares.

Worked Example 1.3

A creditor has a £1,500 judgment against Sam. They know Sam has a current account with Bank X which usually has funds. They apply for and obtain an interim TPDO which is served on Bank X when Sam's account balance is £800. What happens next?

Answer:

Bank X must freeze the £800. The interim order is served on Sam. At the final hearing, unless Sam has valid objections, the court will likely order Bank X to pay the £800 to the creditor. The creditor would need to use other methods to recover the remaining £700.

Additional practical points on TPDO

- If multiple accounts exist, details should be provided to assist service. Unknown balances can still be targeted; the bank must respond to the interim order stating the amounts frozen.

- TPDOs may be used against trade debtors (where a third party owes the judgment debtor), but the court considers whether the debt is due or contingent.

- Salary paid into a bank account becomes part of the account balance; TPDOs may catch it if present at time of service. By contrast, unpaid salary from an employer is addressed via attachment of earnings, not TPDO.

Attachment of Earnings Orders (AEO)

An Attachment of Earnings Order requires the judgment debtor's employer to make deductions from the debtor's wages or salary and pay them directly to the court, which then forwards the money to the judgment creditor. This method is only available in the County Court (CPR Part 89, Attachment of Earnings Act 1971).

Key Term: Attachment of Earnings Order (AEO)

A court order directed to a judgment debtor's employer to make regular deductions from the debtor's earnings and pay them to the court for the judgment creditor.

This method is only suitable if the judgment debtor is employed (not self-employed) and receiving earnings. The court sets a protected earnings rate to ensure the debtor retains a minimum income.

Key Term: Protected earnings rate

The minimum amount of a debtor’s net earnings that must remain after deductions under an AEO, ensuring the debtor has sufficient income for basic living needs. Deductions cannot reduce earnings below this rate.

Applications are made to the County Court. The debtor may be required to provide a statement of means. The court then fixes the deduction rate and serves the order on the employer, who is legally obliged to comply and may face sanctions if they do not. AEOs can be varied or suspended upon application if circumstances change (e.g., loss of employment, reduced hours), and multiple judgments may be consolidated into a single AEO.

AEOs cannot be made against companies or self-employed debtors. If the debtor changes employment, the order continues, but the court and creditor must be informed; there is a duty on the debtor to notify the court of new employer details.

Worked Example 1.4

Kiran has a County Court judgment for £2,800 against Alex, who is employed full-time. Alex has no assets but regular net earnings of £2,100 per month and minimal savings. What is the most suitable enforcement method?

Answer:

An Attachment of Earnings Order in the County Court is suitable. The court will set a protected earnings rate and order Alex’s employer to deduct an amount from wages each pay period until the judgment is satisfied. Taking control of goods is less appropriate where there are no seizable assets; a TPDO is only viable if Alex has sufficient funds in an account when an interim order is served.Exam Warning: Remember that AEOs are only available against employed individuals and applications are made to the County Court. They are not suitable for debtors who are self-employed, unemployed, or companies.

Insolvency Procedures

While primarily designed to deal with inability to pay debts generally, initiating insolvency proceedings can be used tactically to put pressure on a debtor to pay a specific judgment debt.

For individual debtors owing £5,000 or more, the creditor can serve a Statutory Demand. If the debt is not paid or disputed within 21 days, the creditor can petition for the debtor's bankruptcy.

Key Term: Statutory Demand

A formal written demand for payment of an undisputed debt (minimum £5,000 for individuals, £750 for companies). Failure to comply can be used as evidence of inability to pay debts in subsequent insolvency proceedings.

For company debtors owing £750 or more, a Statutory Demand can be served, followed by a winding-up petition if the company fails to pay. Insolvency is a blunt instrument and should not be used for genuinely disputed debts. If used inappropriately, the court may dismiss the petition and make adverse costs orders.

Practical considerations on interest and combining methods

Key Term: Interest on judgment debts

As above: High Court judgments accrue interest at 8% per annum until payment; County Court interest at 8% per annum may apply to judgments for £5,000 or more (or where contract/statute provides), but interest usually ceases upon commencement of County Court enforcement unless the enforcement produces no payment.

Enforcement methods can be combined to improve prospects of recovery. For example, a creditor might secure a charging order over property while simultaneously obtaining a TPDO to capture funds in an account. However, permission is needed to enforce by taking control of goods where an AEO is already in force, to avoid unfair duplication.

Worked Example 1.5

Delta Ltd has a £19,000 County Court judgment against Zeta Ltd. Zeta’s bank account has fluctuating balances; it owns a van on finance and a small warehouse jointly owned with another company. What combination of enforcement steps is most logical?

Answer:

Apply for a TPDO against Zeta’s bank account to capture available funds on the day of service, and in parallel seek an interim charging order over Zeta’s beneficial interest in the warehouse. The van is likely not suitable for TCG if title is with the finance company. Depending on the TPDO outcome, proceed to a final charging order and consider an order for sale if proportionate.

Key Point Checklist

This article has covered the following key knowledge points:

- Enforcement is necessary when a judgment debtor fails to pay voluntarily; it is not automatic.

- Orders to obtain information (CPR Part 71) can compel disclosure of a debtor’s assets and income to guide enforcement choices.

- Different methods exist under CPR Parts 70–73 and related Acts, with procedural distinctions between County Court and High Court routes.

- Taking Control of Goods (writ/warrant of control) allows seizure and sale of non-exempt goods. Exempt goods include essential domestic items and tools of the trade up to £1,350 aggregate.

- Controlled goods agreements enable goods to remain with the debtor subject to payment terms.

- Charging Orders secure debt against property or shares via interim and final stages; registration is required; a separate Order for Sale is needed to force sale.

- Third Party Debt Orders attach funds owed to the debtor by third parties (commonly bank accounts), catching only funds present at service of the interim order; overdrafts are not attachable.

- Attachment of Earnings Orders deduct from an employed debtor's wages (County Court only) and require setting a protected earnings rate; AEOs can be varied or consolidated.

- Interest on High Court judgment debts accrues at 8% per annum until payment; County Court interest regimes differ and may cease on commencement of enforcement unless enforcement yields no payment.

- Insolvency (bankruptcy/winding-up) can be used tactically via a Statutory Demand for undisputed debts, subject to threshold amounts and judicial discretion.

- Combining methods is permitted, but permission is needed to enforce by taking control of goods while an AEO is in force.

Key Terms and Concepts

- Judgment creditor

- Judgment debtor

- Order to obtain information

- Taking Control of Goods (TCG)

- Exempt goods

- Writ of control

- Warrant of control

- High Court Enforcement Officer (HCEO)

- Controlled goods agreement

- Charging Order

- Interim Charging Order

- Final Charging Order

- Order for Sale

- Third Party Debt Order (TPDO)

- Attachment of Earnings Order (AEO)

- Protected earnings rate

- Interest on judgment debts

- Statutory Demand