Learning Outcomes

This article outlines Conditional Fee Agreements (CFAs) as a funding mechanism for civil litigation in England and Wales, including:

- identifying the statutory and regulatory framework governing CFAs, success fees and QOCS, and how these interact with LASPO 2012 reforms;

- explaining the formal validity requirements for an enforceable CFA, such as writing, clear definition of “success”, and compliant success fee caps;

- distinguishing between solicitor–client costs, inter partes costs, and additional liabilities, and who ultimately bears each category in common exam scenarios;

- calculating success fees within statutory limits, applying the 100% uplift cap and the 25% personal injury damages cap to numerical problems;

- evaluating typical CFA terms, including risk assessments, allocation of disbursements, and the drafting of precise success definitions;

- applying professional conduct duties when advising on CFAs, including cost transparency, conflicts of interest, and advice on alternative funding and insurance;

- analysing how QOCS operates in personal injury litigation, with particular focus on its exceptions, set-off rules, and interaction with Part 36 offers;

- assessing practical risks and advantages of CFAs for clients and solicitors, and predicting likely exam pitfalls and trick questions based on these principles.

SQE1 Syllabus

For SQE1, you are required to understand the funding options available for legal services, specifically Conditional Fee Agreements (CFAs), with a focus on the following syllabus points:

- the statutory requirements for valid CFAs (including writing, definition of success, and success fee caps)

- the calculation and implications of success fees

- the effect of recent legislative changes (e.g., LASPO 2012) on recoverability of fees

- the professional conduct duties when advising on and entering into CFAs

- the risks and practical consequences for both clients and solicitors

- the prohibition on CFAs in criminal and family proceedings

- the 100% uplift cap and the personal injury cap of 25% of “relevant damages” (general damages and past pecuniary loss, excluding future loss)

- the scope and exceptions to QOCS, including fundamental dishonesty, strike-out and Part 36 consequences

- the role of ATE/BTE insurance and the limited recoverability of ATE premiums (e.g., clinical negligence expert reports)

- the requirement to provide transparent, written costs information under SRA rules, including how success fees and disbursements are borne

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What statutory requirements must a Conditional Fee Agreement (CFA) satisfy to be enforceable?

- What is a success fee, and how is it calculated in a CFA?

- Who is responsible for paying the success fee under a CFA if the client wins the case?

- What professional conduct duties must a solicitor observe when advising a client about a CFA?

Introduction

Conditional Fee Agreements (CFAs) are a key funding option for civil litigation in England and Wales. Under a CFA, a solicitor’s fees (or part of them) are payable only if the case is successful. This arrangement, often called "no win, no fee," allows clients to pursue claims without paying legal fees upfront, but may require payment of an additional fee (the success fee) if the claim succeeds. Understanding the legal requirements, calculation of fees, and professional conduct obligations is essential for SQE1. It is also important to understand how CFAs interact with other funding mechanisms (such as ATE insurance), the distinction between solicitor–client costs and inter partes costs, and how post-LASPO rules and QOCS shape who pays what at the end of a case.

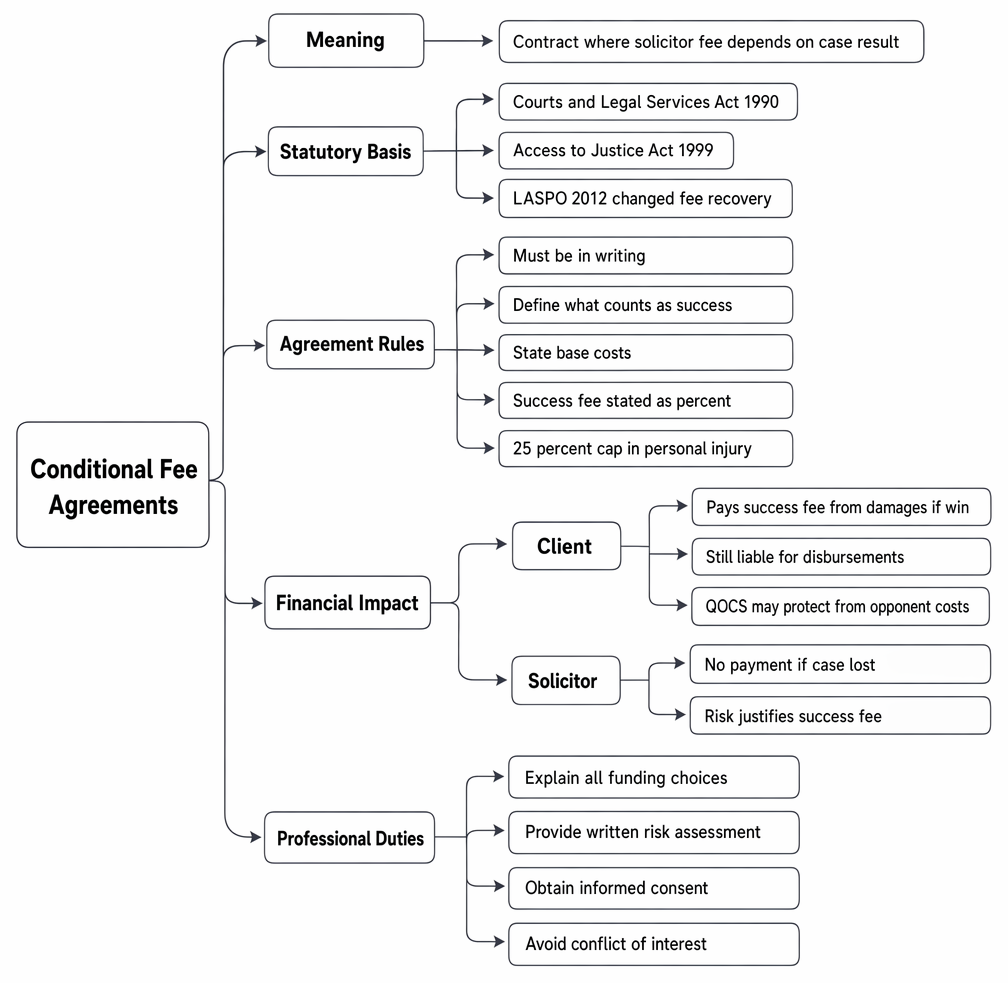

The diagram presents the meaning, statutory framework, formal requirements, costs consequences, QOCS and professional duties associated with conditional fee agreements.

Key Term: Conditional Fee Agreement (CFA)

A contract between a client and solicitor where payment of some or all legal fees is conditional on the outcome of the case.Test Tip: In SQE-style questions on Conditional fee agreements (CFAs), identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Statutory Requirements for CFAs

CFAs are governed primarily by the Courts and Legal Services Act 1990 (ss 58 and 58A), the Access to Justice Act 1999, and the Legal Aid, Sentencing and Punishment of Offenders Act 2012 (LASPO). To be enforceable, a CFA must:

- Be in writing.

- Clearly define what constitutes "success" in the case.

- State the percentage uplift for any success fee (i.e., the percentage by which base fees will be increased if the case succeeds).

- Comply with statutory caps on success fees (including the general 100% uplift cap and the personal injury damages cap).

- Not relate to criminal or family proceedings.

Under s 58, a CFA is an agreement with a person providing advocacy or litigation services which provides for their fees or any part of them to be payable only in specified circumstances. A success fee must be expressed as a percentage increase on base costs (e.g., hourly rates or fixed fees) that would be payable absent the CFA. The uplift cannot exceed 100% of base costs. In personal injury claims, there is an additional cap: the success fee payable by the client is limited to 25% of the “relevant damages” (general damages for pain, suffering and loss of amenity, plus past pecuniary losses), expressly excluding future losses.

If a CFA fails to meet statutory requirements, it is unenforceable and the solicitor cannot recover fees under it. Courts have taken a purposive approach to compliance in some contexts (e.g., substantial compliance where minor defects do not materially affect client protection or the administration of justice), but as between solicitor and client, any material non-compliance risks the agreement being void and fees irrecoverable.

Key Term: Success Fee

An additional fee payable to the solicitor under a CFA if the case is successful, expressed as a percentage uplift on base costs, and subject to statutory caps.

Structure and Operation of CFAs

A typical CFA sets out:

- The solicitor’s standard hourly or fixed fee (base costs).

- The agreed success fee, payable only if the client wins.

- The definition of "success" (e.g., obtaining damages, costs recovered, injunctive relief, settlement above a minimum threshold).

- The client’s liability for disbursements (e.g., court fees, expert reports, counsel’s fees), which are usually payable win or lose unless otherwise agreed.

- Any recommendation or requirement to consider insurance (BTE/ATE) and how premiums will be paid.

- Termination provisions (e.g., what happens if the client ends the retainer, or if the solicitor ceases to act).

The success fee reflects the risk the solicitor takes in not being paid if the case fails. The higher the assessed litigation risk, the higher the justified success fee—subject to statutory caps. The uplift must be a genuine, evidence-based reflection of risk (supported by a documented risk assessment) and must not be designed simply to inflate income.

Most CFAs exclude disbursements from the conditional element to avoid the risk that the firm is left out of pocket for third-party costs. If the case fails, the client will ordinarily remain liable for disbursements and may also face an adverse costs order (subject to QOCS in personal injury cases and any insurance in place). If the case succeeds, base costs are usually recoverable from the losing party on assessment; the success fee is not recoverable inter partes post-LASPO and must be paid by the client.

When defining “success,” precision matters. Where relief sought is non-monetary (e.g., an injunction) or where partial success is possible (e.g., mixed claims, or beating/ not beating offers), the CFA should specify what outcomes trigger the success fee and whether different uplifts apply to different types of success.

Worked Example 1.1

A solicitor agrees to act for a client in a personal injury claim under a CFA. The base costs are £4,000. The CFA specifies a success fee of 20%. The client wins and is awarded £10,000 in damages.

Answer:

The solicitor’s base costs (£4,000) are usually recoverable from the losing party. The success fee (20% of £4,000 = £800) is payable by the client and is deducted from the damages. The client receives £9,200 after paying the success fee.

Worked Example 1.2

Base costs total £12,000 in a personal injury claim. The CFA success fee is 50%. Damages awarded are £30,000, of which £20,000 are general damages and £5,000 are past loss of earnings (the remaining £5,000 are future losses).

Answer:

The success fee calculated as an uplift on base costs is £6,000 (50% of £12,000). However, in PI the success fee payable by the client is capped at 25% of “relevant damages,” i.e., general damages plus past pecuniary loss. Relevant damages here are £25,000 (£20,000 + £5,000), so the cap is £6,250. The success fee of £6,000 does not breach the damages cap, and it is below the general 100% uplift cap. The client pays £6,000 from damages (future loss is excluded from the cap calculation, but the fee is still payable from the overall award).

Professional Conduct Duties

Solicitors must comply with the SRA Code of Conduct when advising on and entering into CFAs. Key duties include:

- Explaining all funding options, not just CFAs. Where appropriate, advise on private retainers, fixed fees, damages-based agreements, third-party funding, and legal aid (if potentially eligible), and signpost to providers if the firm does not undertake certain work types.

- Ensuring the client understands the terms, including liability for success fees and disbursements, the non-recoverability of success fees from the opponent post-LASPO, and the distinction between solicitor–client costs and costs payable between the parties.

- Complying with SRA Transparency Rules by providing clear, written costs information at engagement and as the matter progresses. This must include the circumstances in which clients may have to make payments themselves, including any deduction from damages for success fees or insurance premiums.

- Advising on the availability and cost of legal expenses insurance (before-the-event or after-the-event), including limitations on recoverability of ATE premiums and any panel solicitor restrictions under BTE policies. Clients have a qualified right to choose their own solicitor; insurers may cap payable rates to panel levels provided the choice is not rendered meaningless.

- Avoiding conflicts of interest—success fees must reflect genuine risk, not be set arbitrarily high. Overcharging would breach SRA Principles (best interests and integrity) and Code provisions against taking unfair advantage of clients.

- Acting in the client’s best interests at all times, including advising on offers and settlement with a clear explanation of any costs consequences (e.g., Part 36 impacts) and how these interact with the CFA and QOCS.

- Ensuring counsel’s funding terms are explained. Barristers are not obliged to accept instructions on non-standard funding (cab rank rule does not apply to CFAs); if counsel acts under a CFA, the client should understand any separate success fee and how counsel’s costs are treated.

Key Term: After-the-Event (ATE) Insurance

Insurance taken out after a dispute arises to cover potential liability for the opponent’s costs and disbursements if the case is lost. Key Term: Qualified One-Way Costs Shifting (QOCS)

A costs rule in personal injury cases where a losing claimant is not usually liable for the defendant’s costs, subject to exceptions.

Clients must also be informed about complaint procedures and their rights to challenge bills or seek assessment where applicable. Clear written retainers and regular cost updates help ensure informed decision-making and reduce disputes.

Practical Implications and Risks

For Clients

- If the claim is successful, the client pays the success fee (from damages), plus any unrecovered disbursements. In personal injury claims, the success fee is capped at 25% of relevant damages (excluding future losses), and the uplift cannot exceed 100% of base costs.

- If the claim fails, the client usually pays no solicitor’s base fees under the CFA but remains liable for disbursements unless otherwise agreed. ATE insurance can cover adverse costs and sometimes disbursements, but premiums are typically not recoverable from opponents (with a limited exception in clinical negligence for the part of the premium relating to expert reports on liability and causation).

- QOCS protects most personal injury claimants from paying the defendant’s costs if they lose, but not from paying their own disbursements. QOCS has exceptions (e.g., fundamental dishonesty, strike-out for abuse of process, and certain Part 36 outcomes). Recent amendments allow defendants to set off their costs against claimants’ damages, interest, and certain costs awarded to the claimant.

- Settlement decisions can affect costs exposure. Failing to beat a defendant’s Part 36 offer can result in adverse costs orders enforceable up to the level permitted under QOCS (e.g., set-off against damages and interest).

For Solicitors

- If the claim fails, the solicitor may receive no payment for their work. Firms must manage the financial risk, including disbursement funding, and only take on CFA work with a realistic assessment of prospects.

- The success fee must be justified by a documented risk assessment and set as a percentage uplift on base costs; setting an arbitrary or excessive uplift risks breach of conduct rules and unenforceability.

- Failure to comply with statutory or conduct requirements can render the CFA unenforceable. If invalid, the solicitor may be unable to recover fees from the client.

- Robust costs advice is essential. Clients should receive clear explanations of the distinction between solicitor–client costs and costs between the parties, likely recoverability on assessment, and potential shortfalls.

- Counsel’s funding arrangements should be aligned. If counsel is engaged on a CFA, ensure consistency and clarity about how their base costs and any success fee will be treated and paid.

Worked Example 1.3

A client loses a CFA-funded claim. The solicitor’s base costs were £5,000, and the client had paid £500 in court fees (disbursements). The client had no ATE insurance.

Answer:

The client pays no solicitor’s base fees but remains liable for the £500 disbursement. If QOCS does not apply, the client may also be liable for the opponent’s costs. If QOCS applies and no exception is triggered, the client should not face enforcement of the defendant’s costs beyond permitted set-off limits.

Worked Example 1.4

The claimant wins £15,000 in damages but fails to beat the defendant’s Part 36 offer. The court orders the claimant to pay the defendant’s costs from the expiry of the relevant period. Base costs incurred by the claimant’s solicitor total £7,000; the success fee uplift is 30%.

Answer:

The claimant pays the success fee (30% of £7,000 = £2,100) from damages. Under QOCS, the defendant’s costs can be enforced by set-off against the claimant’s damages and interest and, following recent rules, against certain costs orders in the claimant’s favour. If defendant’s recoverable costs exceed damages and interest, enforcement may be limited by QOCS unless an exception applies (e.g., fundamental dishonesty). The net sum to the claimant will be reduced by set-off and the success fee.

Worked Example 1.5

A CFA in a judicial review-style claim defines “success” only as “obtaining a favourable order.” The court dismisses the substantive claim but orders the defendant to pay the claimant’s costs due to late disclosure.

Answer:

If “success” is not defined to cover costs-only successes, the success fee may not be triggered by a costs order alone. This illustrates why CFAs must define success precisely (e.g., by including obtaining specific relief, a settlement above a threshold, or costs recovered).

Recent Legislative Changes

LASPO 2012 made significant changes:

- Success fees under CFAs are no longer recoverable from the losing party (except in limited cases). The client pays the success fee from their damages.

- In personal injury claims, the success fee is capped at 25% of “relevant damages” (general damages and past pecuniary loss), expressly excluding future loss. The uplift must also stay within the general 100% cap relative to base costs.

- QOCS protects most personal injury claimants from paying the defendant’s costs if they lose, but there are exceptions. Amendments to the Civil Procedure Rules allow defendants to set off their costs against a claimant’s damages, interest, and certain costs awards in the claimant’s favour. Fundamental dishonesty or claims struck out for abuse can disapply QOCS protection.

- ATE insurance premiums are generally not recoverable from the losing party post-LASPO. A limited exception exists in clinical negligence for recovery of the part of the premium relating to expert reports on liability and causation. Parties should check the current CPR provisions and relevant regulations.

- Pre-LASPO CFAs (entered into before 1 April 2013) retained recoverability of success fees and certain ATE premiums under transitional rules. Backdating a CFA agreed after that date does not revive recoverability; only CFAs actually entered before commencement qualify.

Exam Warning: In SQE1, read questions carefully to determine who is responsible for paying the success fee and whether QOCS or ATE insurance applies. Remember, the success fee is now deducted from the client’s damages, not paid by the losing party.

Summary

| Feature | Pre-LASPO CFA (before April 2013) | Post-LASPO CFA (after April 2013) |

|---|---|---|

| Success fee recoverable from losing party? | Yes | No (client pays from damages) |

| Cap on success fee? | No statutory cap | 25% of damages (PI claims) |

| QOCS applies? | No | Yes (PI claims) |

| ATE insurance premium recoverable? | Yes | No (except limited cases) |

Key Point Checklist

This article has covered the following key knowledge points:

- CFAs are agreements where solicitor’s fees (or part) are payable only if the case succeeds.

- CFAs must be in writing, define success, and state the success fee as a percentage uplift on base costs.

- The success fee uplift cannot exceed 100% of base costs; in personal injury it is further capped at 25% of relevant damages (excluding future loss).

- Success fees are not recoverable from the losing party post-LASPO; the client pays from damages.

- Solicitors must comply with professional conduct duties when advising on CFAs, including transparency on costs and advising on alternative funding and insurance.

- Clients may still be liable for disbursements and, if not protected by QOCS or insurance, the opponent’s costs.

- QOCS applies in most personal injury claims but has exceptions; set-off mechanisms can reduce a claimant’s net recovery.

- ATE premiums are generally not recoverable, subject to limited exceptions (e.g., part of the premium in clinical negligence).

- Pre-LASPO CFAs retain recoverability under transitional rules; backdating does not revive recoverability.

- Careful drafting of the definition of “success” is essential to avoid disputes over when the success fee is triggered.

Key Terms and Concepts

- Conditional Fee Agreement (CFA)

- Success Fee

- After-the-Event (ATE) Insurance

- Qualified One-Way Costs Shifting (QOCS)