Learning Outcomes

This article outlines the purpose and scope of accountants’ reports under the SRA Accounts Rules and how they safeguard client money. It explains when a firm must obtain a report, including where client money is held or received, or where joint accounts or clients’ own accounts are operated as signatory, and clarifies how “cease to hold” scenarios are treated. It identifies who may prepare and sign the report, the need for an independent, qualified accountant, and the respective responsibilities of the firm, its managers and the COFA. It details the six‑month deadlines for obtaining reports and delivering qualified reports to the SRA, and how exemption thresholds are calculated using average and maximum client money balances, including Legal Aid Agency‑only funding models and use of TPMAs. It examines the SRA’s powers to require a report or grant a waiver, sets out key submission and record‑keeping procedures, and highlights retention requirements. It also analyzes the consequences of non‑compliance, including financial penalties, restrictions on handling client money, follow‑up reporting obligations, and potential referral to the Solicitors Disciplinary Tribunal, reinforcing typical SQE1 problem scenarios and exam traps.

SQE1 Syllabus

For SQE1, you are required to understand the requirements for accountants’ reports under the SRA Accounts Rules and related regulatory compliance, with a focus on the following syllabus points:

- when a firm must obtain and deliver an accountant’s report

- the deadlines for obtaining and submitting the report

- who is qualified to prepare the report

- the main content and scope of the report

- exemptions from the reporting requirement

- the SRA’s powers to require a report or waive the requirement

- the consequences of failing to comply with reporting obligations

- how to calculate the average and maximum balance thresholds for exemption

- the firm’s record‑keeping duties, the COFA’s role, and retention requirements

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which firms are exempt from obtaining an accountant’s report under the SRA Accounts Rules?

- What is the deadline for delivering a qualified accountant’s report to the SRA?

- Who is responsible for preparing and signing an accountant’s report for a law firm?

- What are the consequences if a firm fails to deliver a required accountant’s report within the deadline?

Introduction

Accountants' reports are a key part of the regulatory framework for solicitors in England and Wales. They provide independent assurance that client money is being handled in accordance with the SRA Accounts Rules. For the SQE1 exam, you must know when a report is required, who prepares it, the deadlines for submission, and what happens if a firm fails to comply.

Requirements under the SRA Accounts Rules include exemptions, six-month reporting deadlines, submission of qualified reports, retention, and non-compliance consequences.

Test Tip: In SQE-style questions on Deadlines and submission procedures, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

The Purpose of Accountants' Reports

The SRA requires most firms that hold or receive client money to obtain an independent accountant’s report after every accounting period. This report confirms whether the firm has complied with the Accounts Rules and whether client money has been put at risk. Reports focus on core risks to client money: separation from business money, prompt banking and repayment, restrictions on withdrawals, prohibition on using client accounts as banking facilities, payment of interest where due, and adequacy of accounting systems and reconciliations.

Key Term: accountant’s report

A report prepared by a qualified accountant, reviewing a law firm’s compliance with the SRA Accounts Rules, especially in relation to the handling of client money.

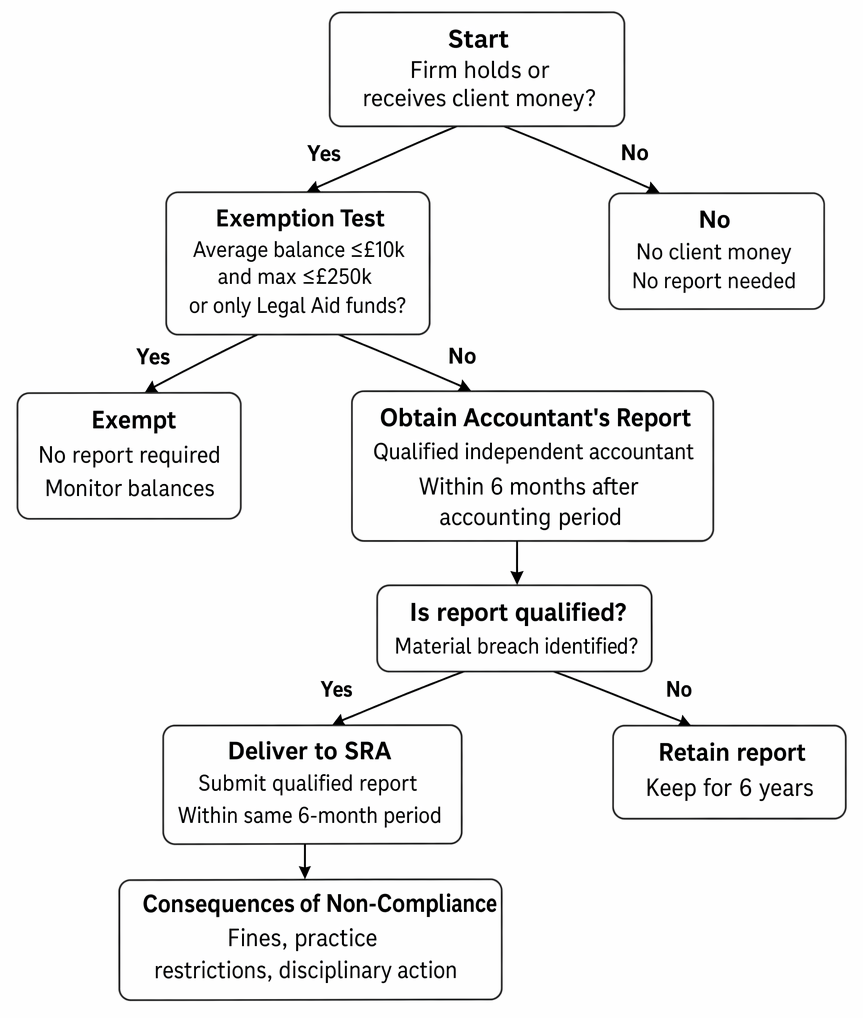

When Is an Accountant’s Report Required?

A firm must obtain an accountant’s report if, at any time during its accounting period, it has held or received client money, or operated a joint account or a client’s own account as signatory. This includes firms that ceased holding client money mid‑period. The requirement applies even if client money was held briefly or in small amounts, unless an exemption applies.

The trigger is broad. It captures:

- client money in pooled client accounts and separate designated client accounts

- client money held as stakeholder or agent in conveyancing

- mortgage advances and redemptions handled through the client account

- money held or received when acting as trustee, attorney/donee of a power, Court of Protection deputy, or trustee of an occupational pension scheme

- joint accounts and clients’ own accounts operated as signatory (with limited record‑keeping overrides)

Key Term: accounting period

The period (normally twelve months) for which a firm prepares its financial statements and must obtain an accountant’s report.

Who Can Prepare the Report?

The report must be prepared and signed by an accountant who is a member of a recognised chartered accountancy body and is, or works for, a registered auditor. The accountant must be independent of the firm’s day‑to‑day operations. Engagement terms should confirm the accountant’s right to obtain all relevant records and their duty to report material concerns to the SRA (for example, evidence of fraud, theft or serious systems weaknesses that put client money at risk). The SRA can disqualify an accountant from preparing reports where due care and skill has not been exercised.

Key Term: qualified accountant

An accountant who is a member of a recognised chartered accountancy body and is, or works for, a registered auditor, and is eligible to prepare an accountant’s report for a law firm.

What Must the Report Cover?

The accountant’s report must review the firm’s compliance with key areas of the Accounts Rules, including:

- the operation and use of client accounts

- withdrawals from client account

- the duty to correct breaches promptly

- client accounting systems and controls

- record‑keeping and reconciliations

The review typically covers whether client money is kept separate from business money; whether money is paid in promptly and returned when no longer properly held; whether client money is only withdrawn for permitted purposes and where sufficient funds are held for the specific client; whether the client account is not being used to provide banking facilities; and whether interest is accounted for fairly (or a written agreement is in place to depart from default interest). The report also assesses whether reconciliations are performed at least every five weeks, whether ledgers are properly maintained for each client/matter, and whether central records (including bills and notifications of costs) are readily accessible.

The accountant must use professional judgement to decide whether any breaches are material and whether the report should be qualified. Qualification is required where failures in compliance mean client money “is, has been, or is likely to be placed at risk,” or where significant weaknesses in systems and controls are identified.

Key Term: qualified report

An accountant’s report that identifies material breaches of the Accounts Rules or significant risks to client money, and must be delivered to the SRA.

Deadlines for Obtaining and Delivering the Report

A firm must obtain the accountant’s report within six months of the end of its accounting period. If the report is qualified, it must be delivered to the SRA within the same six‑month period. The responsibility for delivery lies with the firm, not the accountant. For multi‑office practices that adopt separate accounting periods for different offices, each office must be covered by a report obtained within six months of its respective period; there must be no gap in coverage.

The deadline is strict. Only qualified reports are delivered in the ordinary course; unqualified reports should be retained. If the firm is ceasing to hold or operate a client account (for example, on closure), the SRA may require a final report on a case‑by‑case basis and will specify the deadline.

Key Term: qualified report

An accountant’s report that identifies serious breaches or risks to client money and must be submitted to the SRA.

Exemptions from the Reporting Requirement

Some firms are exempt from obtaining an accountant’s report if they meet both of the following criteria during the accounting period:

- the average balance of client money held does not exceed £10,000; and

- the maximum balance at any time does not exceed £250,000.

These thresholds are calculated using statements or passbook balances obtained at least every five weeks across all general and separate designated client accounts, plus any joint accounts and clients’ own accounts operated by the firm as signatory in the period. The “average” is the total of these balances divided by the number of reconciliation points in the period.

Firms that only hold client money received from the Legal Aid Agency are also exempt. Where a firm uses a third‑party managed account (TPMA) instead of operating its own client account, money is held by the TPMA provider rather than by the firm, so the reporting requirement may not arise.

However, the SRA can require a report at any time if it considers it necessary in the public interest, including where a firm ceases to practise or where risk indicators suggest that client money may be at risk.

Key Term: exemption (accountants’ report)

A firm is not required to obtain an accountant’s report if it meets the SRA’s criteria for low client money balances or only holds Legal Aid Agency funds. Key Term: statement/passbook balance

The total balance across all client money accounts (including joint accounts and clients’ own accounts operated as signatory) taken from bank/building society statements at least every five weeks for reconciliation purposes.

Submission Procedures

The firm must ensure the following steps are followed:

- Appoint a qualified accountant and agree the terms of engagement, confirming independence and rights of access to records (including authority to report concerns to the SRA).

- Provide the accountant with all necessary information and access to records, including details of all accounts used during the period, bank statements, reconciliations, client and cash ledgers, and the central record of bills and notifications of costs.

- Obtain the report within six months of the end of the accounting period.

- If the report is qualified, or the SRA has required delivery of a report, deliver it within the same six‑month period via

mySRAand ensure the COFA has a copy. The AR1 form may be uploaded by the firm or the reporting accountant. - Retain a copy of the report and the engagement terms for at least six years.

The firm’s COFA should oversee the process, ensure managers see the report, and confirm that any breaches identified have been corrected promptly. If the firm changes accountant during the cycle, it should notify the SRA of the change and provide the replacement firm’s details.

Key Term: SRA (Solicitors Regulation Authority)

The regulatory body for solicitors in England and Wales, responsible for enforcing the Accounts Rules and receiving qualified accountant’s reports. Key Term: COFA (Compliance Officer for Finance and Administration)

The manager responsible for oversight of the firm’s compliance with the Accounts Rules, including keeping central records, ensuring the report is seen by managers, and overseeing prompt correction of breaches.

SRA Powers and Waivers

The SRA may require a firm to obtain and deliver an accountant’s report at any time, even if the firm is otherwise exempt. This includes where a firm has ceased holding client money during the period (“cease to hold” scenario), where the SRA has reason to believe that client money may be at risk, or where public interest considerations arise. The SRA may also grant a waiver from the requirement in exceptional circumstances. The SRA can disqualify an accountant from preparing reports for failures of due care and skill, and can require production of documents and explanations to its appointed investigator.

Consequences of Non-Compliance

Failure to obtain or deliver a required accountant’s report is a serious breach of the Accounts Rules. The SRA may impose financial penalties, restrict the firm’s ability to handle client money, require remedial action and follow‑up reports, or take disciplinary action against the firm or its managers. Persistent or serious failures may result in conditions on authorisation, intervention, or referral to the Solicitors Disciplinary Tribunal. Where a qualified report identifies client money at risk, the SRA will expect immediate remediation, including correction of breaches and strengthening of systems and controls.

Worked Example 1.1

A small firm holds client money throughout the year, but the average balance is £8,000 and the maximum at any time is £12,000. Is the firm required to obtain an accountant’s report?

Answer:

No. The firm is exempt because both the average and maximum balances are below the SRA’s thresholds.

Worked Example 1.2

A firm’s accounting period ends on 31 March. The accountant completes a qualified report on 15 July. By what date must the firm deliver the report to the SRA?

Answer:

The deadline is 30 September (six months after 31 March). The firm must deliver the qualified report to the SRA by this date.

Worked Example 1.3

A firm reconciles all client accounts every five weeks. Across eight reconciliation points in an accounting period, the total of statement/passbook balances is £72,000. The highest balance at any reconciliation point is £18,000. Does the firm qualify for exemption?

Answer:

Yes. The average balance is £9,000 (£72,000 ÷ 8), and the maximum is £18,000. Both are below the exemption thresholds (average ≤ £10,000; maximum ≤ £250,000), so the firm is exempt.

Worked Example 1.4

A criminal defence firm funds its work entirely from the Legal Aid Agency (LAA) and does not hold any other client money. It receives LAA payments into the business account. Must it obtain an accountant’s report?

Answer:

No. Firms that only hold or receive money from the LAA are exempt from the reporting requirement. The SRA can still require a report in the public interest, but the default position is exemption.

Worked Example 1.5

A conveyancing firm stops operating a client account on 30 November and transfers any remaining client balances to a TPMA. The firm’s accounting period ends 31 December. Must it obtain a report, and might the SRA require delivery?

Answer:

Yes, the firm must obtain a report covering the period in which it held or received client money. The SRA may require delivery of a final report on a case‑by‑case basis where the firm ceases to hold or operate a client account, particularly to confirm closure and proper transfer of funds.Exam Warning: If a firm fails to deliver a required accountant’s report within the deadline, the SRA may take regulatory and disciplinary action. Common traps include assuming the thresholds apply only to pooled client accounts (they also include separate designated client accounts and, for calculation purposes, relevant joint accounts and clients’ own accounts operated as signatory), or overlooking the six‑month deadline when the firm has ceased to hold client money mid‑period.

Key Point Checklist

This article has covered the following key knowledge points:

- Most firms holding or receiving client money must obtain an accountant’s report after every accounting period; this includes where joint accounts or clients’ own accounts are operated as signatory.

- The report must be prepared by a qualified accountant and obtained within six months of the end of the accounting period; only qualified reports must be delivered to the SRA within that six‑month window.

- Exemption applies only if both the average balance (calculated from regular reconciliation balances) does not exceed £10,000 and the maximum balance does not exceed £250,000, or if the firm only holds LAA funds.

- Threshold calculations use statement/passbook balances taken at least every five weeks and include all client money accounts, plus relevant joint and clients’ own accounts operated as signatory.

- The firm must provide the accountant with records and access; the COFA should oversee the process, and both the report and engagement terms should be retained for at least six years.

- The SRA can require a report at any time in the public interest, including upon cessation of holding client money, and may grant waivers in exceptional cases.

- Failure to comply can result in penalties, restrictions on handling client money, and disciplinary action; serious or persistent failures may lead to intervention or SDT referral.

Key Terms and Concepts

- accountant’s report

- accounting period

- qualified accountant

- qualified report

- exemption (accountants’ report)

- SRA (Solicitors Regulation Authority)

- COFA (Compliance Officer for Finance and Administration)

- statement/passbook balance