Learning Outcomes

This article explains how to obtain and deliver accountants’ reports under the SRA Accounts Rules, including:

- identifying when a firm must obtain an accountant’s report, when exemptions apply, and how TPMA use, joint accounts and clients’ own accounts affect the duty

- determining whether an accountant is independent, suitably qualified and permitted to prepare and sign the report for a particular firm

- mapping the chronological steps in the reporting process, from defining the accounting period to meeting the six‑month timeframe for obtaining and, where required, delivering the report to the SRA

- distinguishing between unqualified and qualified reports, recognising common qualification triggers, and predicting likely regulatory consequences

- analysing fact patterns to decide when a qualified report must be delivered, even where breaches have been remedied internally

- evaluating the COFA’s systems, controls, and oversight responsibilities that reduce the risk of qualification and support compliance

- applying rule‑based reasoning to client‑money scenarios, including breaches of Rules 2, 3, 4, 5, 6 and 8, to assess whether client money has been placed at risk

- recalling recordkeeping and retention standards for accounting records and reports, and explaining why poor records may themselves justify qualification

- integrating knowledge of these rules to answer SQE1 multiple‑choice questions efficiently and avoid common exam traps on thresholds, deadlines and exemptions

SQE1 Syllabus

For SQE1, you are required to understand the regulatory requirements for accountants’ reports under the SRA Accounts Rules, with a focus on the following syllabus points:

- when a firm must obtain an accountant’s report and when exemptions apply

- who is qualified to prepare and sign an accountant’s report

- the process and deadlines for delivering reports to the SRA

- the meaning and consequences of a qualified report

- the firm’s obligations to provide information and retain records

- the role of the Compliance Officer for Finance and Administration (COFA) in this process

- how joint accounts and clients’ own accounts trigger reporting obligations

- how use of third‑party managed accounts (TPMAs) impacts whether a report is required

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which firms are exempt from obtaining an accountant’s report under the SRA Accounts Rules?

- What is a qualified accountant’s report, and what must a firm do if it receives one?

- Who is permitted to prepare and sign an accountant’s report for a solicitor’s firm?

- What is the deadline for delivering an accountant’s report to the SRA after the end of an accounting period?

Introduction

Accountants’ reports are a key regulatory requirement for solicitors’ firms that hold or receive client money. These reports provide independent assurance to the SRA that client funds are managed in accordance with the SRA Accounts Rules. Understanding when a report is required, who can prepare it, and how and when to deliver it is essential for SQE1 and for compliance in practice. The report operates alongside the firm’s internal controls—accurate ledgers, five‑weekly bank reconciliations, and robust authorisation of withdrawals—to show the SRA that client money has not been placed at risk.

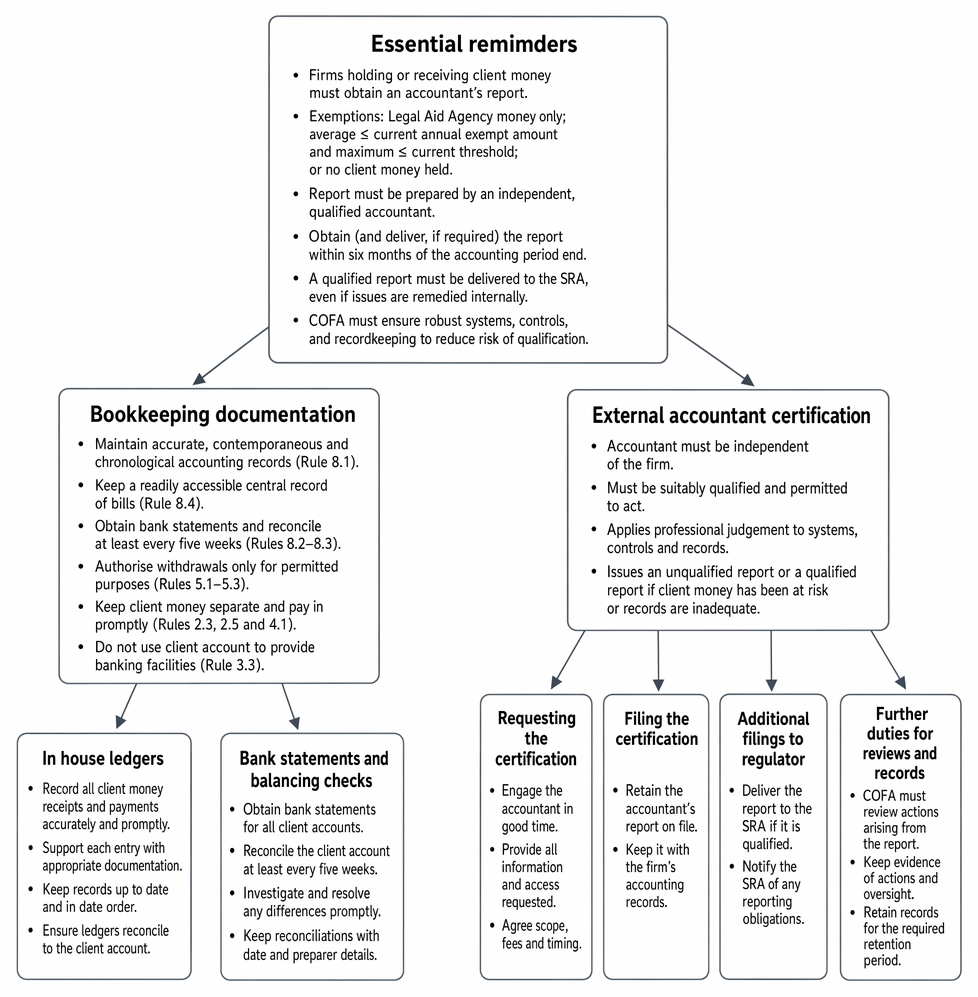

Essential reminders comprise bookkeeping documentation and external accountant certification requirements when obtaining and delivering accountants’ reports under the SRA Accounts Rules.

Key Term: accountant’s report

A formal report prepared by an independent, qualified accountant confirming a solicitor’s firm’s compliance with the SRA Accounts Rules regarding client money.Test Tip: In SQE-style questions on Obtaining and delivering accountants' reports, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

The Purpose of Accountants’ Reports

Solicitors’ firms must safeguard client money and comply with strict financial controls. The SRA requires most firms that hold or receive client money to obtain an accountant’s report each year. This report is prepared by an independent, qualified accountant and confirms whether the firm has complied with the Accounts Rules and whether client money has been at risk.

The accountant applies professional judgement to the firm’s systems and records. Typical areas reviewed include:

- whether client money has been kept separate from business money (Rule 4.1)

- whether client money was paid promptly into a client account (Rule 2.3) and returned promptly when no longer properly held (Rule 2.5)

- whether the client account has been used to provide banking facilities (Rule 3.3)

- whether withdrawals were only for permitted purposes and properly authorised (Rules 5.1–5.3)

- whether bank statements were obtained and reconciliations carried out at least every five weeks (Rules 8.2–8.3)

- whether accounting records are accurate, contemporaneous and chronological (Rule 8.1), with a readily accessible central record of bills (Rule 8.4)

Where weaknesses or breaches are identified that put client money at risk, the accountant qualifies the report, triggering a delivery obligation to the SRA.

When Must a Firm Obtain an Accountant’s Report?

A firm must obtain an accountant’s report if, at any time during its accounting period, it has held or received client money, or operated a joint account or a client’s own account as signatory. The obligation is triggered even if client money was held only briefly during the period.

However, there are important exemptions:

- If all client money held or received during the accounting period is from the Legal Aid Agency, no report is required.

- If the average client money balance during the period does not exceed £10,000 and the maximum balance at any time does not exceed £250,000, the firm is exempt. Both thresholds must be satisfied.

- If the firm does not hold or receive client money at all during the period, no report is required.

Key Term: accounting period

The period (normally 12 months) for which a firm prepares its annual accounts and obtains an accountant’s report.

The “average” for the exemption is assessed using statement or passbook balances obtained at least every five weeks across all client accounts and any joint accounts or clients’ own accounts the firm operated as signatory. Firms should retain evidence of the calculation and the five‑weekly balances to demonstrate eligibility.

If a firm uses a third‑party managed account (TPMA) and does not hold or receive any client money itself, it may fall outside the duty to obtain a report for that period. However, if the firm operated a joint account or a client’s own account as signatory at any point, the duty to obtain a report re‑applies notwithstanding the TPMA.

Key Term: Legal Aid Agency (LAA)

The public body that funds legal services for eligible clients. Client money received solely from the LAA during an accounting period can exempt a firm from obtaining a report. Key Term: joint account

A bank or building society account in the joint names of the firm and a client/third party. Operating such an account as signatory triggers the duty to obtain a report for the relevant period. Key Term: client’s own account

A bank account in the client’s name which the firm operates as signatory (e.g. under a power of attorney or Court of Protection appointment). Operating such an account as signatory triggers the duty to obtain a report. Key Term: third‑party managed account (TPMA)

An arrangement under which client money is held and managed by a FCA‑regulated third party. Money in a TPMA is not held or received by the firm; accordingly, if the firm otherwise holds no client money and operates no joint/client’s own account, the duty to obtain a report does not arise.

Who Can Prepare and Sign an Accountant’s Report?

The report must be prepared and signed by an independent accountant who is a member of a recognised chartered accountancy body and is, or works for, a registered auditor. The accountant must not be a partner, director, or employee of the firm being reported on during the accounting period. Independence is essential to ensure objective scrutiny.

The SRA can disqualify an accountant from preparing reports for firms if the accountant has been found guilty of professional misconduct by their professional body or has failed to exercise due care and skill in preparing reports. Accountants must sign their reports in the prescribed form and should retain a copy for at least six years.

Key Term: qualified accountant

An accountant who is a member of a recognised chartered accountancy body and is, or works for, a registered auditor, and is independent of the firm.

Accountants have statutory obligations when preparing reports. If they discover evidence of theft or fraud in relation to client money, or information which is materially significant in determining whether a solicitor or firm is fit and proper to hold client money, they must report the matter to the SRA immediately. This duty exists even if the firm’s report is not yet finished.

The Process and Deadlines for Obtaining and Delivering Reports

A firm must obtain the accountant’s report within six months of the end of its accounting period. If the report is qualified (see below), it must be delivered to the SRA within the same six-month period. If the report is not qualified, it does not need to be delivered unless requested by the SRA.

If a firm ceases to hold client money (for example, on closure), it should liaise with the SRA promptly. The SRA can require a final report to be obtained and delivered; it may also require reports to be obtained earlier than usual or more frequently where it is in the public interest. Good practice is to plan for a clean closure with reconciled ledgers and, where directed, obtain and deliver the final report within six months of the cessation date.

Key Term: qualified report

An accountant’s report that identifies material breaches of the SRA Accounts Rules or significant risks to client money.

Worked Example 1.1

A firm’s accountant discovers that, during the accounting period, the firm’s client account was overdrawn for several days due to a bookkeeping error. The accountant considers this a material breach and qualifies the report. What must the firm do?

Answer:

The firm must deliver the qualified report to the SRA within six months of the end of the accounting period. The SRA may investigate further and require the firm to take remedial action. In addition to the headline deadlines:

- the accountant will generally send a copy of the report to the firm’s COFA

- both the firm and the accountant should retain a copy of the report for at least six years

- the SRA may require a report earlier than six months (e.g., three months after year end) or at more frequent intervals if specific risks arise (public interest)

What Is a Qualified Report?

A report is qualified if the accountant finds material breaches of the Accounts Rules or significant weaknesses in the firm’s systems and controls that put client money at risk. Only qualified reports must be delivered to the SRA. The SRA may take regulatory action if a qualified report reveals serious concerns.

Typical findings that may lead to qualification include:

- using the client account as a banking facility (e.g., paying a client’s personal bills from the client account without connection to regulated services)

- repeated or unexplained differences between bank statements and client ledgers not resolved promptly

- client balances being used to fund another client’s matter (e.g., withdrawals made before funds are available for the specific client—Rule 5.3)

- persistent failure to obtain bank statements and conduct reconciliations at least every five weeks

- failure to correct breaches promptly upon discovery (Rule 6.1)

Worked Example 1.2

During a reconciliation, a firm finds a difference between the client account bank balance and the aggregate of client ledger balances. The discrepancy persists for several months and is not investigated. When preparing the annual report, the accountant notes the unresolved difference. Does this create a risk of qualification?

Answer:

Yes. Failure to reconcile and promptly resolve differences between bank statements and internal records can put client money at risk. An unresolved discrepancy over months is likely to lead to a qualified report.

Worked Example 1.3

A firm pays a client’s monthly credit card bill from the general client account, unrelated to any regulated services. The accountant identifies that the client account has been used as a banking facility. How should this be reflected?

Answer:

The use of a client account as a banking facility breaches Rule 3.3 and puts client money at risk. The accountant should qualify the report. The firm must cease the practice immediately, return money promptly, and strengthen controls.

Exemptions from the Requirement to Obtain a Report

A firm is exempt from obtaining an accountant’s report if:

- All client money held or received during the period is from the Legal Aid Agency.

- The average balance of client money held during the period does not exceed £10,000 and the maximum balance at any time does not exceed £250,000.

The firm must keep records to demonstrate that it meets the exemption criteria. The “average” is derived from the total balances captured at least every five weeks during the year across all relevant accounts (client accounts, joint accounts, and clients’ own accounts operated by the firm as signatory), divided by the number of balance points taken. Both the average and the maximum must be within threshold.

Note that even when exempt from obtaining a report, firms must still comply fully with the Accounts Rules in relation to client money that they hold (e.g., separation, prompt banking, permitted withdrawals, recordkeeping and reconciliation duties).

Worked Example 1.4

A small firm holds client money balances of £8,000, £9,000, and £11,000 at its monthly reconciliations during the accounting period. The maximum balance is £11,000 and the average is £9,333. Does the firm need to obtain an accountant’s report?

Answer:

Yes. Although the average balance is below £10,000, the maximum balance exceeds £10,000, so the firm does not qualify for the exemption.

Worked Example 1.5

A firm has used a TPMA for all client funds and did not operate any joint accounts or clients’ own accounts as signatory during the period. It received no client money into its own bank accounts. Must it obtain an accountant’s report?

Answer:

No. If the firm did not hold or receive client money and did not operate any joint or clients’ own accounts as signatory, it is outside the duty to obtain a report for that accounting period.

Worked Example 1.6

Over an accounting period, a firm’s five‑weekly balances across all relevant accounts were: £6,000, £4,000, £9,500, £10,200, and £7,800. The average is £7,900; the maximum is £10,200. Is the firm exempt?

Answer:

No. The average is below £10,000, but the maximum exceeds £10,000. Both limbs must be satisfied to claim the exemption.

The Role of the COFA and the Firm’s Obligations

The Compliance Officer for Finance and Administration (COFA) is responsible for ensuring compliance with the Accounts Rules, including the obligation to obtain and deliver accountant’s reports. The COFA should ensure:

- a robust reconciliation process (bank statements and reconciliations at least every five weeks), with prompt investigation and resolution of differences

- withdrawals from client account are only for permitted purposes, authorised by appropriately senior personnel and supported by evidence (Rules 5.1–5.3)

- client money is kept separate from business money and never used to prop up cash flow

- client money is returned promptly once there is no proper reason to hold it

- a central record of bills and written notifications of costs is kept and readily accessible (Rule 8.4)

- that the accountant receives complete information, including details of all bank/building society accounts used during the period and internal records required to complete the report

Key Term: Compliance Officer for Finance and Administration (COFA)

The individual in a solicitor’s firm responsible for ensuring compliance with the SRA Accounts Rules and reporting material breaches to the SRA.

Worked Example 1.7

The COFA notes that several withdrawals were made from the client account without documentary evidence of the purpose. What action is required before the accountant’s review?

Answer:

The COFA should obtain supporting evidence, check authorisations, and, if any withdrawal was not permitted under Rule 5.1 or lacked sufficient funds for the specific client (Rule 5.3), replace the money immediately from the business account and record the corrective entries. Material breaches must be reported promptly to the SRA.

Recordkeeping and Retention

Firms must retain all accounting records, including accountant’s reports and supporting documents, for at least six years. “Accounting records” broadly include client ledgers, cash sheets, reconciliation statements, bank statements, transfer journals, and the central record of bills and other written notifications of costs. Where a firm operates a client’s own account as signatory, statements must be retained and reconciliations carried out at least every five weeks; for joint accounts, at least five‑weekly statements and a central record of bills must be retained.

Robust recordkeeping underpins the accountant’s ability to verify compliance and reduces the risk of qualification. Failures in recordkeeping—missing reconciliations, incomplete ledgers, or absent bank statements—may themselves lead to qualification if they put client money at risk.

Consequences of Non-Compliance

Failure to obtain or deliver a required accountant’s report is a serious breach of the Accounts Rules and may result in disciplinary action by the SRA. The SRA may impose conditions, require remedial steps, order an early or more frequent report, or increase monitoring. Where reports or other information suggest risks to client money, the SRA may investigate the firm and, in serious cases, take enforcement action.

Immediate corrective action is expected if client money has been improperly withheld or withdrawn. Firms should replace any shortfall at once, review controls, and, where conduct amounts to a serious breach, report promptly to the SRA under the Codes of Conduct.

An accountant must report immediately to the SRA if they discover evidence of theft or fraud or information materially significant to whether a firm is fit and proper to hold client money. This reporting duty applies independently of the firm’s delivery obligations.

Exam Warning: If a firm fails to deliver a qualified accountant’s report to the SRA within the required deadline, this is a regulatory breach and may result in a financial penalty or further investigation.

Summary Table: When Is an Accountant’s Report Required?

| Situation | Report Required? |

|---|---|

| Firm holds client money during the period | Yes |

| Firm holds only Legal Aid Agency money | No |

| Average client money ≤ £10,000, max ≤ £250,000 | No |

| Firm holds no client money during the period | No |

| Report is qualified | Must deliver to SRA |

| Report is not qualified | Deliver only if SRA requests |

Key Point Checklist

This article has covered the following key knowledge points:

- Most firms holding or receiving client money must obtain an accountant’s report each accounting period.

- Exemptions apply for firms holding only Legal Aid Agency money or with low client money balances (both average and maximum thresholds must be satisfied).

- Operating a joint account or a client’s own account as signatory during the period triggers the duty to obtain a report.

- The report must be prepared and signed by an independent, qualified accountant and is obtained within six months of period end.

- Qualified reports (identifying material breaches or risks) must be delivered to the SRA within six months of the end of the accounting period; unqualified reports are retained but not delivered unless requested by the SRA.

- The SRA may require reports earlier than usual, more frequently, or at cessation of holding client money, where it is in the public interest.

- The COFA is responsible for ensuring compliance and providing information to the accountant, including ensuring five‑weekly bank reconciliations and accurate records.

- Firms must retain all accounting records, including reports, for at least six years.

- Failure to comply may result in regulatory action by the SRA, and accountants have independent duties to report fraud or significant concerns immediately.

Key Terms and Concepts

- accountant’s report

- accounting period

- qualified accountant

- qualified report

- Compliance Officer for Finance and Administration (COFA)

- Legal Aid Agency (LAA)

- joint account

- client’s own account

- third‑party managed account (TPMA)