Learning Outcomes

This article outlines the regulatory requirements governing accountants’ reports and the storage and retention of those reports for SQE1 purposes, including:

- the purpose, scope, and timing of accountants’ reports, and when they must be obtained and delivered to the SRA

- the six-year retention obligation and the range of supporting documents that must be stored, such as ledgers, bank statements, reconciliation statements, and interest records

- how to calculate and apply the low-balances exemption using five-weekly reconciled totals, and how to recognise when the thresholds are exceeded

- the distinction between LAA-only, low-balance, and no-client-money exemptions, and the continuing need to maintain accurate records even where an exemption applies

- the treatment of joint accounts, clients’ own accounts, and TPMAs, and how they affect reporting duties and retention of records

- the COFA’s responsibilities for system controls, reconciliations, central records, secure storage, and prompt production of reports and supporting documentation

- the SRA’s power to require a report in the public interest (including on firm closure) and the regulatory, disciplinary, and reputational consequences of non-compliance

- applying these rules to typical SQE1-style problem questions, enabling accurate analysis of scenarios involving exemptions, retention failures, and qualified reports.

SQE1 Syllabus

For SQE1, you are required to understand the regulatory framework and practical requirements for accountants' reports under the SRA Accounts Rules, with a focus on the following syllabus points:

- the purpose and function of accountants' reports in legal practice, including the “accounting period” and timing requirements

- the SRA's rules on the storage and retention of accountants' reports and supporting records (six-year retention)

- the duty to obtain accountants’ reports within six months of the end of the accounting period; delivery to the SRA when the report is qualified

- exemptions from obtaining/delivering accountants' reports (LAA-only and low balances), and how to calculate the average and maximum thresholds

- impacts of joint accounts, clients' own accounts, and TPMAs on reporting and record-keeping

- COFA responsibilities for system controls, five-weekly bank statements and reconciliation, and maintaining accessible records

- the consequences of failing to retain, obtain, deliver, or produce reports and records when required, and the SRA’s power to require a report in the public interest

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- How long must a firm retain accountants' reports and supporting documentation under the SRA Accounts Rules?

- Which of the following firms is exempt from obtaining an accountant's report?

- a) A firm that only holds Legal Aid Agency money

- b) A firm that never holds client money

- c) A firm whose average client account balance is £8,000 and maximum is £200,000 during the accounting period

- d) All of the above

- What is the main compliance risk if a firm cannot produce an accountant's report from four years ago during an SRA investigation?

- True or false? If a firm qualifies for an exemption from obtaining an accountant's report, it no longer needs to keep any financial records for that period.

Introduction

Accountants' reports are a key part of the regulatory framework for solicitors in England and Wales. These reports provide independent assurance that firms are complying with the SRA Accounts Rules, especially in relation to the handling of client money. The SRA imposes strict requirements on the storage and retention of these reports and related documents. Understanding these rules—and the exemptions that may apply—is essential for SQE1.

Accountants’ report obligations, exemption criteria, six-year record retention, and production to the SRA are set out for firms handling client money.

The Purpose of Accountants' Reports

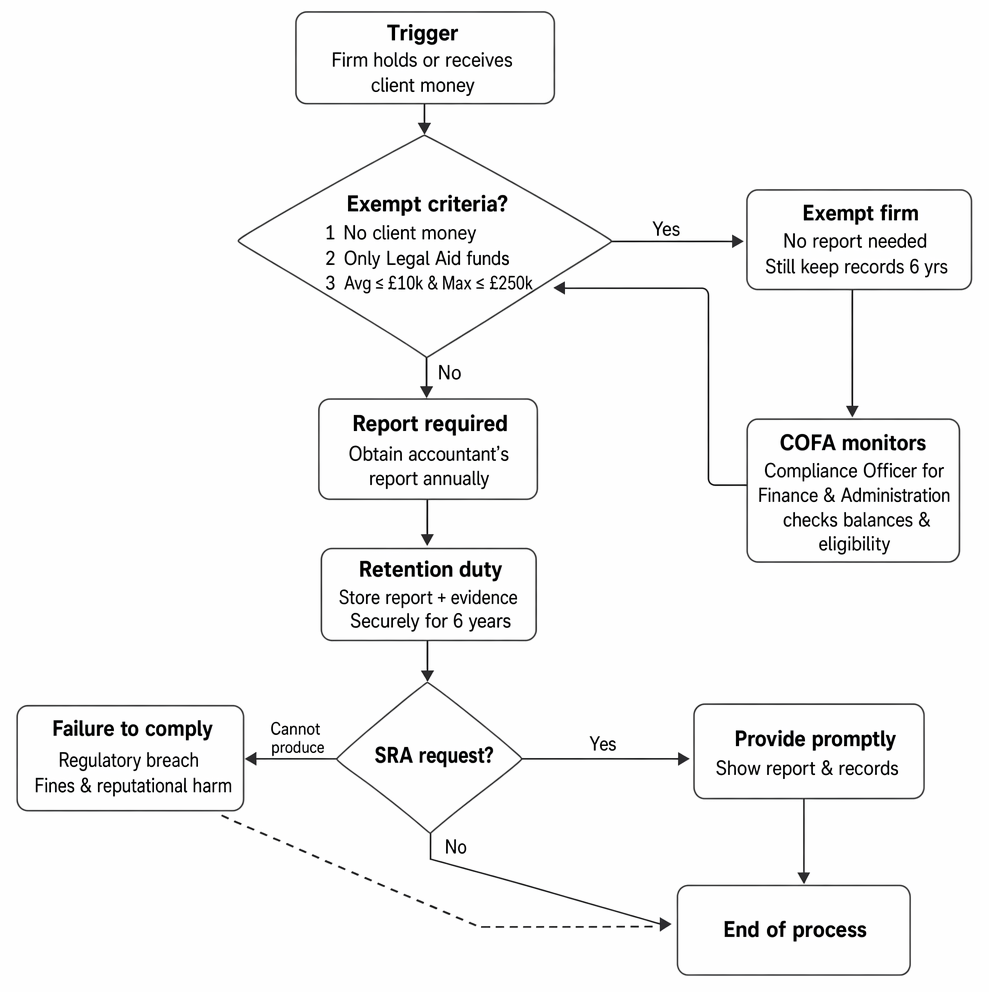

Accountants' reports are independent assessments of a firm's compliance with the SRA Accounts Rules. They are usually prepared annually by a qualified accountant and must be obtained by most firms that hold or receive client money, or operate joint accounts or clients' own accounts as signatory. The “accounting period” is typically twelve months and the report must be obtained within six months of the end of that period. If the accountant concludes the Rules were not complied with such that client money has been, is, or is likely to be at risk, the report is “qualified” and the firm must deliver a copy to the SRA within six months of period end. Where breaches are minor and do not put client money at risk, a report may be unqualified and need not be delivered, though it must still be obtained and retained.

Key Term: accountants' report

An independent report prepared by a qualified accountant confirming a firm's compliance with the SRA Accounts Rules, especially regarding client money. Key Term: accounting period

The period, normally twelve months, used for financial reporting. Firms must obtain an accountant’s report within six months of the end of the accounting period. Key Term: qualified accountant’s report

An accountant’s report that identifies failures to comply with the Accounts Rules such that money belonging to clients or third parties has been, is, or is likely to be placed at risk. Qualified reports must be delivered to the SRA.

Storage and Retention of Accountants' Reports

The SRA requires firms to keep accountants' reports and all supporting documentation for a minimum of six years. This retention period ensures that records are available for regulatory inspections, audits, or investigations, and aligns with the limitation period for most civil claims. Retention applies regardless of whether a firm was required to deliver its report to the SRA—if the firm was obliged to obtain a report, it must retain it.

Key Term: retention period

The minimum length of time (six years) that a firm must securely store accountants' reports and supporting records, as required by the SRA.

Retention is not limited to the report itself. Firms should retain all accounting records relevant to the period, including:

- client ledgers and cash sheets (showing receipts and payments of client money)

- business ledgers (for firm money)

- bank statements for client and business accounts obtained at least every five weeks

- reconciliation statements signed by the COFA or a manager at least every five weeks

- a central record of all bills or written notifications of costs

- interest calculations and payments (sum in lieu of interest; separate designated deposit client account records, where applicable)

- records of transfers (client to business; business to client; inter-client)

- statements and records for joint accounts, clients’ own accounts, and TPMAs (where relevant)

- any documentation supplied to the accountant preparing the report

Key Term: reconciliation statement

A record confirming that bank statements and internal accounting records have been compared and any differences resolved. It must be signed off at least every five weeks by the COFA or a manager.

Firms may store these records in paper or electronic form, provided they are secure, accessible, and protected from unauthorised access or loss. Good practice includes robust access controls, encrypted backups, documented data retention schedules, and periodic tests that records can be retrieved promptly. Migration to new systems must be carefully managed to preserve the audit trail and ensure records remain readable for six years. The SRA expects prompt production of records when requested; delay or inability to produce is a serious compliance issue.

Worked Example 1.1

A firm receives an SRA request to produce its accountant's report for the accounting period ending four years ago. The firm has switched to a new IT system and cannot retrieve the report or supporting records.

Answer:

The firm is in breach of the SRA Accounts Rules. It must retain accountants' reports and supporting documentation for at least six years and be able to produce them promptly on request. Failure to do so may result in regulatory action.

Worked Example 1.2

Over a one-year accounting period, a firm’s reconciled client money totals recorded at five-week intervals were £8,000, £9,000, £12,500, £7,500, £10,000, £11,000, £9,500, £8,500, and £12,000. The highest single reconciled total was £12,500. Does the firm qualify for the “low balances” exemption?

Answer:

Add the reconciled totals and divide by the number of reconciliations to find the average. Here, the average is below £10,000 and the maximum is below £250,000, so both thresholds are met. The firm qualifies for the exemption for that period, but must still retain all accounting records for six years and continue to monitor balances in subsequent periods.

Exemptions from Accountants' Reports

Not all firms are required to obtain or deliver an accountant's report. The main exemptions are:

- Firms that only hold or receive money from the Legal Aid Agency during the accounting period.

- Firms whose average client account balance does not exceed £10,000 and whose maximum balance does not exceed £250,000 during the accounting period. Both thresholds must be satisfied.

- Firms that do not hold or receive any client money, or do not operate joint accounts or clients' own accounts as signatory.

Key Term: exemption (accountants' report)

A situation where a firm is not required to obtain or deliver an accountant's report due to meeting specific SRA criteria.

When assessing the “low balances” exemption, the firm must use reconciled totals obtained at least every five weeks across all client accounts—including pooled client accounts, any separate designated deposit client accounts, and the client money held in joint accounts or clients’ own accounts operated by the firm. If either the average or the maximum threshold is exceeded at any point in the accounting period, the exemption does not apply for that period. If a firm only holds LAA payments for its costs and no other client money during the accounting period, the LAA-only exemption applies; the presence of any non-LAA client money, however small, will normally disqualify the firm from that exemption.

Even if a firm is exempt, it must still comply with all other SRA Accounts Rules, including maintaining accurate records, obtaining bank statements and reconciling at least every five weeks, and monitoring whether it continues to meet the exemption criteria.

Key Term: compliance officer for finance and administration (COFA)

The individual responsible for ensuring a firm's compliance with the SRA Accounts Rules, including record-keeping and reporting breaches.

Worked Example 1.3

A small firm holds an average client account balance of £8,000 and a maximum of £200,000 during the accounting period. It only holds client money for a few weeks each year.

Answer:

The firm is exempt from obtaining an accountant's report for that period, as it meets both the average and maximum balance thresholds. However, it must still keep all records for six years and monitor its balances in future periods.

Worked Example 1.4

A firm does mainly criminal LAA-funded work but also briefly holds £2,000 in a client account from a private conveyancing client pending completion. Does the LAA-only exemption apply?

Answer:

No. The LAA-only exemption applies only where all client money held or received during the accounting period consists of LAA payments. Holding any non-LAA client money disqualifies the firm from the LAA-only exemption for that period. The firm must obtain an accountant’s report and retain all records for six years.

Worked Example 1.5

A small practice decides to use a TPMA for all matters and never holds or receives client money itself. It does not operate joint accounts or clients’ own accounts. Must it obtain an accountant’s report?

Answer:

Where a firm does not hold or receive client money and does not operate joint accounts or clients’ own accounts as signatory, it is outside the scope of the duty to obtain an accountant’s report for that period. The firm must still comply with SRA Standards and Regulations, ensure the TPMA provider is FCA-regulated, notify the SRA of TPMA use, and obtain regular TPMA statements. The SRA may still require a report in the public interest in rare circumstances.

Compliance Duties and Risks

The COFA is responsible for ensuring that accountants' reports and supporting records are stored securely and retained for the required period. This includes:

- obtaining bank or building society statements for all client and business accounts at least every five weeks

- preparing reconciliation statements at least every five weeks and ensuring discrepancies are investigated and resolved promptly

- keeping a central record of all bills and written notifications of costs in a readily accessible form

- ensuring that, where the firm is within scope, an accountant’s report is obtained within six months of the end of the accounting period, and delivered to the SRA if qualified

If the SRA requests a report or supporting documentation, the firm must be able to produce it promptly. Failure to do so may result in regulatory action, disciplinary proceedings, conditions on practice, or reputational harm. In some cases, the SRA may require a report even where an exemption might otherwise apply—for example, on closure of a firm or where it is in the public interest.

Accountants preparing the report must be appropriately qualified (members of recognised chartered accountancy bodies and registered auditors). They must exercise professional judgment and, under statute, immediately report to the SRA any evidence of theft or fraud of client money, or concerns about whether a firm is fit and proper to hold client money. Firms must provide the accountant with all necessary information—including details of all bank accounts used during the period—to enable completion of the report.

Worked Example 1.6

A firm ceases practice and closes its client account. It had been exempt on low balances for the last period. Must it obtain and deliver a final report?

Answer:

The SRA may require a report on closure even if an exemption applied during the period. If required, the firm must obtain the report within six months of period end and deliver it to the SRA if qualified. All accounting records must still be retained for six years.

Worked Example 1.7

During a five-weekly reconciliation, the COFA notes a £200 discrepancy between the client account bank statement and the cash sheet totals. The COFA plans to investigate later, but does not record the reconciliation or resolve the discrepancy for several months.

Answer:

Reconciliation must be performed and signed off at least every five weeks. Discrepancies must be investigated and resolved promptly. Delayed investigation and incomplete records are breaches of the Accounts Rules and increase the risk of a qualified report. The firm should correct the breach, document the reconciliation, and, if serious, consider reporting to the SRA.

Worked Example 1.8

A firm relied on the low balances exemption without calculating the average/maximum using five-weekly reconciled totals across its general client account and a small separate designated deposit client account. It later discovers the maximum exceeded £250,000 at one point.

Answer:

Both thresholds must be calculated using reconciled totals at least every five weeks across all client money accounts. Exceeding the maximum at any point disapplies the exemption for that period. The firm should obtain the report for that accounting period and review its monitoring controls. Key Term: third-party managed account (TPMA)

An arrangement where a regulated third party holds and manages client funds for a firm. Money held in a TPMA is not “client money” for the purposes of the SRA Accounts Rules, but firms must notify the SRA of TPMA use and obtain regular statements.Exam Warning: If a firm qualifies for an exemption in one accounting period but later exceeds the exemption thresholds, it must obtain an accountant's report for the period in which the thresholds are breached. Failing to do so is a breach of the SRA Accounts Rules.

Revision Tip: Always check the firm's client account balances at each reconciliation to ensure ongoing eligibility for exemption. If in doubt, obtain an accountant's report.

Key Point Checklist

This article has covered the following key knowledge points:

- Accountants' reports are required for most firms holding or receiving client money, or operating joint accounts or clients’ own accounts as signatory.

- Firms must store accountants' reports and supporting records securely for at least six years and produce them promptly on request.

- Reports must be obtained within six months of the end of the accounting period; qualified reports must be delivered to the SRA within the same timeframe.

- Exemptions apply for firms holding only Legal Aid Agency money, or with low client account balances (both average and maximum thresholds), or not holding client money at all.

- When assessing the low balances exemption, use reconciled totals obtained at least every five weeks across all relevant accounts.

- The COFA is responsible for compliance, including five-weekly bank statements and reconciliation, record-keeping, and reporting breaches.

- Failure to retain or produce reports and records promptly may result in regulatory action; the SRA may require a report in the public interest (e.g., on closure).

- Where a firm uses a TPMA and does not hold or receive client money, it may be outside the reporting duty, but must still meet notification and safeguarding obligations.

Key Terms and Concepts

- accountants' report

- retention period

- exemption (accountants' report)

- compliance officer for finance and administration (COFA)

- accounting period

- qualified accountant’s report

- reconciliation statement

- third-party managed account (TPMA)