Learning Outcomes

This article explains the accounting procedures and double-entry postings required when solicitors submit, reduce, and receive payment of bills, so you can map each transaction accurately across the client, cash, profit costs and HMRC‑VAT ledgers for SQE1 purposes. It explains how profit costs, VAT and disbursements are reflected when a bill is delivered, distinguishing clearly between money on account and billed sums, and highlighting the different entries needed for direct client payments, client-account transfers under Rule 4.3, and mixed receipts requiring prompt allocation under Rule 4.2. It details the treatment of VAT on disbursements using the agency and principal methods, including when input VAT may be reclaimed and when output VAT must be charged to the client. It examines how to record abatements of bills, both before and after payment, and how to correct mistakes in a way that complies with the SRA Accounts Rules and avoids using the client account as a banking facility. It reviews frequent exam traps, such as omitting VAT entries, posting to the wrong side of the client ledger, or transferring round sums, and links each procedural step back to the underlying regulatory requirements and SQE1-style problem questions.

SQE1 Syllabus

For SQE1, you are required to understand the accounting procedures and entries for billing in legal practice, including VAT treatment, with a focus on the following syllabus points:

- the process and accounting entries for submitting a bill to a client (profit costs and VAT)

- how to record reductions (abatements) of bills and the correct double entries

- the accounting entries for payment of bills, including from client funds and direct payments

- the distinction between money on account and billed sums

- VAT treatment of profit costs and disbursements, including agency and principal methods

- compliance with SRA Accounts Rules for all billing and VAT transactions

- mixed receipts and prompt allocation to the correct account (Rule 4.2)

- client-to-business transfers for costs following delivery of a bill (Rule 4.3)

- maintaining a central, readily accessible record of bills (Rule 8.4)

- the prohibition on using the client account as a banking facility (Rule 3.3)

- duty to correct breaches promptly upon discovery (Rule 6.1)

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the correct double-entry accounting entries when a law firm submits a bill for profit costs and VAT to a client?

- How should a reduction (abatement) of a bill be recorded in the ledgers?

- What is the difference between the agency and principal methods for VAT on disbursements?

- When can money held on account in the client account be transferred to the business account?

Introduction

Legal billing procedures require strict compliance with the SRA Accounts Rules and accurate accounting entries at each stage: submitting a bill, reducing (abating) a bill, and recording payment. VAT must be correctly applied to profit costs and, in some cases, to disbursements. Understanding the correct double-entry bookkeeping for each transaction is essential for SQE1 and for legal practice.

Solicitors’ bill accounting from delivery to settlement, including abatement entries, disbursement VAT treatment, and payment received directly or from client account.

Billing interacts with several core Rules:

- client money must be paid promptly into a client account (Rule 2.3), kept separate from business money (Rule 4.1), and never used as a banking facility (Rule 3.3)

- you may only transfer client money to business account to pay costs after a bill (or written notification of costs) has been delivered and for the specific amount billed (Rule 4.3)

- mixed receipts must be allocated promptly to the correct account (Rule 4.2)

- any breach must be corrected promptly on discovery (Rule 6.1)

- firms must keep a central, readily accessible record of bills and notifications of costs (Rule 8.4)

Key Term: profit costs

The firm’s charges for legal work performed for the client, excluding disbursements. Key Term: VAT

Value Added Tax, currently 20% on most legal services in England and Wales. Most firms must register for VAT once taxable turnover exceeds the registration threshold (currently £85,000).

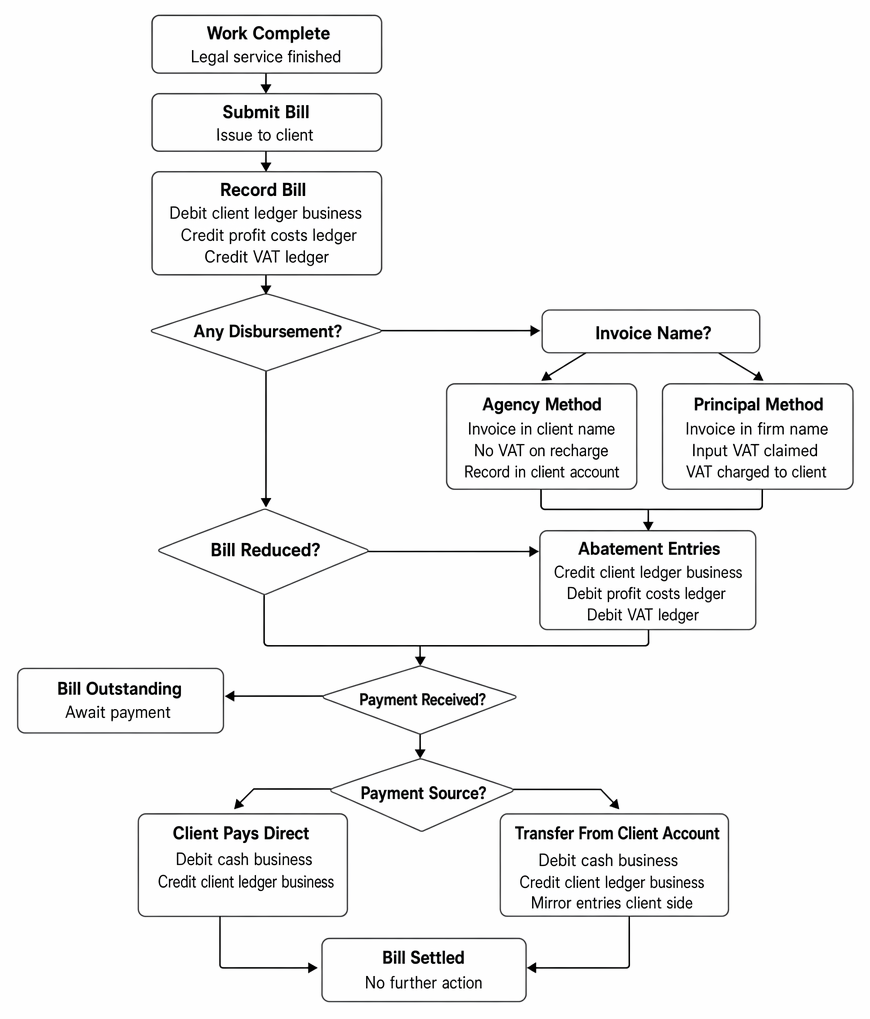

SUBMITTING A BILL: PROFIT COSTS AND VAT

When a law firm completes work for a client, it submits a bill for its profit costs (fees for legal services) and any applicable VAT. The bill may also include disbursements (payments to third parties on the client’s behalf). Only the profit costs and VAT elements of the bill are recorded in the profit costs ledger and HMRC-VAT ledger on submission; disbursements are dealt with in the ledgers when paid and, depending on the circumstances, may attract VAT using either the agency or principal method.

VAT is chargeable on the supply of services at the point of supply, which for solicitors’ services is typically when the bill is delivered. Practical VAT time-of-supply rules apply, but billing contemporaneously with completion of work ensures the correct tax point is used and that output VAT is recorded in the HMRC-VAT ledger when due.

Key Term: disbursement

A payment made by the firm to a third party on behalf of the client, such as court fees or expert reports. Whether VAT is charged to the client depends on the nature of the supply and whether the invoice is in the client’s or firm’s name.

When a bill is submitted, the firm must record the transaction in its ledgers. The correct double-entry bookkeeping is:

- Debit (DR) the client ledger (business account) for the profit costs and VAT.

- Credit (CR) the profit costs ledger for the profit costs amount.

- Credit (CR) the VAT ledger for the VAT amount.

No entry is made in the cash account at this stage, as no money has yet been received. Firms must also ensure a central record of bills is maintained and readily accessible (Rule 8.4).

Revision Tip: Quote profit costs “plus VAT”. If VAT is not expressly stated to be extra, the quoted total will be treated as VAT-inclusive, reducing net fee income.

Worked Example 1.1

A firm submits a bill to a client for £1,000 profit costs plus £200 VAT.

Answer:

DR client ledger (business account) £1,000 (profit costs) DR client ledger (business account) £200 (VAT) CR profit costs ledger £1,000 CR VAT ledger £200

Worked Example 1.2

A firm submits a bill comprising £500 profit costs and £100 VAT. The bill also shows a Land Registry fee of £150 (non-VAT disbursement) previously paid from client funds.

Answer:

DR client ledger (business account) £500 (profit costs) DR client ledger (business account) £100 (VAT) CR profit costs ledger £500 CR VAT ledger £100 No ledger entry is made on submission for the Land Registry fee; it was recorded when paid from the client account.Revision Tip: When revising, memorise that submitting a bill involves only the client ledger (business account), profit costs ledger, and VAT ledger. No cash entries are made until payment is received. Ensure the HMRC-VAT ledger reflects output VAT at the correct tax point.

REDUCING A BILL (ABATEMENT)

Sometimes a bill is reduced after submission, for example, due to a client complaint or negotiation. This reduction is called an abatement.

Key Term: abatement

An agreed reduction in a client’s bill, including the VAT element.

To record an abatement, reverse part of the original entries:

- Credit (CR) the client ledger (business account) for the abated profit costs and VAT.

- Debit (DR) the profit costs ledger for the abated profit costs.

- Debit (DR) the VAT ledger for the abated VAT.

Worked Example 1.3

A firm reduces a previously submitted bill by £200 profit costs and £40 VAT.

Answer:

CR client ledger (business account) £200 (profit costs) CR client ledger (business account) £40 (VAT) DR profit costs ledger £200 DR VAT ledger £40

Worked Example 1.4

A firm submitted a bill for £600 + £120 VAT. It later agrees to reduce the bill to £500 + £100 VAT. What are the abatement entries?

Answer:

CR client ledger (business account) £100 (profit costs) CR client ledger (business account) £20 (VAT) DR profit costs ledger £100 DR VAT ledger £20Exam Warning: When recording an abatement, always enter the reduction amount, not the new total. For example, if a bill is reduced from £1,200 to £1,000, the abatement is £200 (plus VAT), not £1,000.

If an abatement is agreed after payment has been received, refund the abated amount to the client (or set it off with written authority) by a business-to-client cash transfer:

- DR client ledger (business) for the refund amount

- CR cash account (business) for the bank payment

- CR client ledger (client account) and DR cash account (client) if refunding via client account to be used on the matter.

PAYMENT OF A BILL

Once a bill has been submitted, the client may pay by bank transfer, cheque, or from funds already held in the client account. The accounting entries depend on the source of payment.

Under Rule 4.3, you may transfer client money to the business account for payment of costs only after delivering a bill (or written notification of costs), and only for the specific sum billed. Never transfer round sums or use client money for other purposes.

Payment by Client (Direct to Business Account)

If the client pays the bill directly (e.g., by bank transfer), the entries are:

- Debit (DR) the cash account (business side) for the amount received.

- Credit (CR) the client ledger (business account) for the same amount.

Payment from Client Account (Money on Account)

If the firm is holding client money on account (received before the bill was submitted), the firm may transfer the relevant amount to the business account after submitting the bill. The entries are:

- Debit (DR) the client ledger (client account) for the amount transferred.

- Credit (CR) the cash account (client side) for the same amount.

Then:

- Debit (DR) the cash account (business side) for the amount received from the client account.

- Credit (CR) the client ledger (business account) for the same amount.

Key Term: money on account

Client money received in advance of a bill, to be held in the client account until a bill is submitted.

Worked Example 1.5

A client pays £1,200 directly to the business account in settlement of a bill.

Answer:

DR cash account (business) £1,200 CR client ledger (business account) £1,200

If the firm holds £1,200 in the client account and transfers it after submitting the bill:

DR client ledger (client account) £1,200 CR cash account (client) £1,200 DR cash account (business) £1,200 CR client ledger (business account) £1,200

Worked Example 1.6

A bill of £900 + £180 VAT (£1,080 total) is issued. The client has £800 held on account. The client pays the remaining £280 by bank transfer to the business account.

Answer:

Client-to-business transfer for £800: DR client ledger (client account) £800 CR cash account (client) £800 DR cash account (business) £800 CR client ledger (business account) £800 Direct payment of £280: DR cash account (business) £280 CR client ledger (business account) £280

Mixed receipts and prompt allocation

If a single receipt includes both client money and business money (e.g., payment of a bill plus additional funds on account), Rule 4.2 requires prompt allocation to the correct accounts. Many firms pay mixed receipts into the client bank account and promptly transfer the business element to business account.

Worked Example 1.7

The firm receives £1,000 into the client account: £600 to settle a billed sum (£500 profit costs + £100 VAT) and £400 on account of future costs.

Answer:

Receipt into client account: DR cash account (client) £1,000 CR client ledger (client account) £1,000 (annotate split internally) Prompt transfer of £600 to business account to settle the bill: DR client ledger (client account) £600 CR cash account (client) £600 DR cash account (business) £600 CR client ledger (business account) £600 Remaining £400 stays in the client account as money on account.

VAT ON DISBURSEMENTS: AGENCY AND PRINCIPAL METHODS

Disbursements may or may not attract VAT, depending on the nature of the expense and the name on the supplier’s invoice.

Key Term: disbursement

A payment made by the firm to a third party on behalf of the client, such as court fees or expert reports. Key Term: agency method

The firm pays a third party on behalf of the client (invoice in client’s name); VAT is not charged by the firm to the client. The client may reclaim VAT if VAT-registered using the supplier’s invoice. Key Term: principal method

The firm pays a third party for services supplied to the firm (invoice in firm’s name); the firm may reclaim input VAT and must charge output VAT to the client on the disbursement when the bill is submitted.

Agency Method

If the invoice is in the client’s name, the firm pays the supplier and reclaims the exact amount from the client. No additional VAT is charged by the firm. The payment can be made from the client account (if funds are available) or the business account. The ledger entries are VAT-inclusive (one figure), and no entry is made in the HMRC-VAT ledger.

Conditions for treatment as a disbursement for VAT purposes typically include: acting as agent; client receives/uses the supply; client is responsible for paying the supplier; the client authorised payment; and the outlay is separately itemised. Items such as post, phone, photocopying, bank transfer fees, and property searches are usually treated as office expenses and not disbursements for VAT purposes and are subject to VAT as part of the firm’s supply.

Principal Method

If the invoice is in the firm’s name, the firm pays the supplier (including VAT), records input VAT in the HMRC-VAT ledger, and charges the client VAT on the disbursement when submitting the bill. The payment must be made from the business account. Ledger entries occur in two stages:

- Stage 1: pay supplier (DR client ledger business account for the net fee; DR HMRC-VAT ledger for input VAT; CR cash account business for the gross sum)

- Stage 2: bill the client (DR client ledger business account for profit costs and for the VAT on profit costs and disbursement; CR profit costs ledger; CR HMRC-VAT ledger for output VAT)

Worked Example 1.8

A firm pays a surveyor’s invoice for £500 + £100 VAT. The invoice is in the client’s name (agency method).

Answer:

If paid from client funds (sufficient client account balance): DR client ledger (client account) £600 CR cash account (client) £600 No HMRC-VAT ledger entry. If paid from the business account (insufficient client funds): DR client ledger (business account) £600 CR cash account (business) £600 No HMRC-VAT ledger entry.

Worked Example 1.9

An accountant’s report invoice for £2,000 + £400 VAT is in the firm’s name (principal method). The firm pays the supplier, and later bills the client £5,000 profit costs plus VAT on both profit costs and the disbursement.

Answer:

Stage 1 – pay supplier: DR client ledger (business account) £2,000 (net fee) DR HMRC-VAT ledger £400 (input VAT) CR cash account (business) £2,400 (gross payment) Stage 2 – bill client: DR client ledger (business account) £5,000 (profit costs) CR profit costs ledger £5,000 DR client ledger (business account) £1,400 (output VAT: £1,000 on profit costs + £400 on disbursement) CR HMRC-VAT ledger £1,400

Practical points

- Where counsel’s fees are involved, check up-to-date HMRC guidance. Historically, there has been an extra-statutory concession allowing agency treatment in some circumstances, but firms must follow current rules and invoice particulars.

- For disbursements not subject to VAT (e.g., Court fees, Land Registry fees, Stamp Duty Land Tax), pay from the client account if sufficient funds are held; otherwise pay from business account and recover from the client as client money, without VAT.

COMMON ERRORS AND SRA ACCOUNTS RULES

Exam Warning (Common Errors)

Never transfer money from the client account to the business account in payment of a bill unless a bill has been submitted. Money on account must remain in the client account until a bill is delivered.

Other frequent errors:

- Using the client account to make non-legal payments for client convenience (breach of Rule 3.3)

- Withdrawing more client money than is held for that client (breach of Rule 5.3)

- Failing to allocate mixed receipts promptly to the correct account (breach of Rule 4.2)

- Not keeping a central, readily accessible record of bills (breach of Rule 8.4)

- Not correcting breaches immediately upon discovery (Rule 6.1 requires prompt remedy; where client account is short, replace funds immediately—often via business-to-client cash transfer)

Revision Tip (Common Errors)

For SQE1, memorise the correct ledgers for each entry:

- Submitting a bill: client ledger (business), profit costs ledger, VAT ledger

- Abatement: reverse the above

- Payment: cash account and client ledger

- Disbursements: agency or principal method determines VAT treatment

- Client-to-business transfers for costs require a bill and must match the billed sum (Rule 4.3)

Key Point Checklist

This article has covered the following key knowledge points:

- Submitting a bill requires double entries in the client ledger (business), profit costs ledger, and VAT ledger.

- VAT is charged at 20% on most legal services; the tax point typically occurs when the bill is delivered.

- Reducing a bill (abatement) reverses part of the original entries for the reduction amount, including the VAT element.

- Payment of a bill is recorded in the cash account and client ledger; the source of payment (client account or direct payment) determines the ledgers used.

- Money on account must remain in the client account until a bill is submitted; then client-to-business transfers can be made for the specific billed sum (Rule 4.3).

- Mixed receipts must be allocated promptly to the correct account (Rule 4.2).

- VAT on disbursements depends on whether the agency or principal method applies; principal method requires HMRC-VAT ledger entries for input and output VAT.

- The client account must not be used to provide banking facilities (Rule 3.3).

- Maintain a central, readily accessible record of all bills and written notifications of costs (Rule 8.4).

- Correct breaches promptly upon discovery (Rule 6.1), replacing client money immediately where necessary.

Key Terms and Concepts

- profit costs

- VAT

- abatement

- money on account

- disbursement

- agency method

- principal method