Learning Outcomes

This article explains how to recognise, correct, and document breaches of the SRA Accounts Rules for SQE1 FLK2, including:

- distinguishing correctly between client money and business money, and identifying common causes of breaches and client account shortfalls

- applying double-entry bookkeeping to reverse incorrect postings and enter the correct cash transfers and inter-client (paper) transfers

- rectifying errors where client money is paid into or out of the wrong bank account, including mixed receipts

- correcting premature withdrawals for profit costs and disbursement posting errors using the agency and principal methods

- dealing with dishonoured cheques, uncleared funds, and overdrawn client ledgers by restoring shortfalls promptly from business money

- allocating and returning residual client balances, and complying with SRA requirements when clients cannot be traced

- preventing and remedying improper use of the client account as a banking facility and recognising related exam‑style pitfalls

- maintaining clear narratives, audit trails, and reconciliation records that evidence timely rectification and protect other clients’ funds

- understanding the COFA’s responsibilities for monitoring breaches, updating controls, and assessing when matters require reporting to the SRA

- practising exam-focused analysis of fact patterns to select the correct journal entries, regulatory responses, and risk‑management steps.

SQE1 Syllabus

For SQE1, you are required to understand how to rectify breaches of the SRA Accounts Rules, with a focus on the following syllabus points:

- The overriding duty to correct breaches promptly upon discovery, including immediate replacement of client money where required (Rule 6.1), and the responsibility on the part of the COFA and all managers to take prompt remedial action.

- Procedures for identifying and handling a shortfall in the client account (client account shortfall), including obligations to protect other clients’ money and the correct process for tracing and reconciling deficits.

- Accounting entries for reversing incorrect transactions, including reclassifying receipts or payments from the wrong bank account, both in practice (e.g. adjusting physical bank balances) and in the ledgers, while maintaining a clear audit trail.

- Correct entries necessary after a reversal to ensure that the relevant transaction is properly reflected in the records, including the use of cash transfers and inter-client transfers and their accounting implications.

- The requirements for using firm’s own (business) money to rectify shortages in the client account, and the converse where business money has been incorrectly placed in the client account, with particular attention to the prohibition on the use of client money as a banking facility or credit buffer for the firm.

- Maintaining accurate records to ensure that breaches can be identified, corrected, and subsequently audited for regulatory compliance. This involves an understanding of the different types of ledgers (client, business, profit costs, HMRC-VAT, interest), cash sheets, and reconciliation procedures.

- Steps to remedy breaches where client money has been wrongly paid into or out of a business account, or where mixed or inter-client receipts require allocation. Be able to identify the correct treatment for mixed receipts, disbursements, and allocation of monies for costs, particularly when bills have not yet been delivered.

- The process for rectifying shortfalls caused by drawing against uncleared funds or the dishonour of deposited cheques, including recognition of the risks and the necessity for prompt correction.

- Correct application of ‘paper’ (ledger-only) transfers to reallocate client money between ledgers or matters, with no cash sheet entries, and an understanding of the limits of such transfers (for example, when moving funds between clients or between a client's multiple matters).

- Strict prohibition on use of client accounts for banking facilities or to accommodate personal or business payments unconnected to regulated legal services (Rule 3.3), and proper rectification if this occurs, including the prompt return of non-permissible funds and considering the potential for disciplinary action.

- Obligations and procedures for returning client money promptly when no longer needed (Rule 2.5), including special treatment of residual balances, the steps required to trace unclaimed clients, payment of small balances to charity, and the authority needed from the SRA for sums above the threshold.

- Internal and external reporting obligations relating to breaches, including the role of the COFA, the criteria for qualifying and delivering accountants’ reports to the SRA where serious breaches are identified, and the need to document steps taken to prevent recurrence.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

According to Rule 6.1 of the SRA Accounts Rules, when must breaches be corrected?

- a) Within 14 days of discovery.

- b) Promptly upon discovery.

- c) At the end of the accounting period.

- d) When instructed by the SRA.

-

If £100 of client money is incorrectly used to pay a firm's business expense, what is the immediate action required regarding the client account?

- a) Notify the client immediately.

- b) Obtain SRA authorisation before acting.

- c) Replace the £100 in the client account immediately using business money.

- d) Wait for the next bank reconciliation before correcting.

-

Which ledger account is typically debited when correcting a client account shortfall using the firm's own funds?

- a) Client ledger client account.

- b) Client ledger business account.

- c) Cash sheet client account.

- d) Interest payable ledger.

-

A payment covering both a delivered bill (£900) and further funds on account (£300) is received into the business bank by mistake. What should be done promptly?

- a) Transfer £1,200 from client to business bank.

- b) Transfer £300 from business to client bank, and retain £900 in business bank.

- c) Leave as is and reclassify on the ledgers only.

- d) Return the whole payment and ask for two separate transfers.

Introduction

Compliance with the SRA Accounts Rules is essential for all firms and individuals authorised by the SRA who handle client money. The principal principle is the absolute safeguarding of client funds, and errors must be remedied as a matter of urgency. Rule 6.1 places a clear and unqualified obligation to correct any breach of the Rules promptly upon discovery; this is especially important where the breach involves the client bank account or misapplication of client funds.

This duty extends to robust operation of internal accounting systems, including using double-entry bookkeeping and performing regular and timely reconciliations between ledgers and bank statements (required at least every five weeks), so that errors can be detected and rectified at the earliest opportunity. The role of the COFA (Compliance Officer for Finance and Administration) is significant in maintaining the accuracy of client accounting procedures, addressing systems weaknesses, and ensuring the firm meets all regulatory requirements.

Robust systems and procedures—including clear separation of client and business money, prompt allocation of mixed receipts, and vigilant attention to the principles of double-entry bookkeeping—are necessary to prevent breaches. The SRA expects firms not only to establish such controls but to continually monitor compliance, immediately investigate discrepancies, and take all reasonable steps to avoid recurrence.

Key Term: Breach

A failure to comply with any requirement set out in the SRA Accounts Rules, including payment, withdrawal, transfer, or record-keeping errors relating to client or business money. Key Term: Rectification

The process by which a breach of the SRA Accounts Rules is put right, involving necessary accounting corrections, restoration of client funds, revision of records, and, where appropriate, reporting or notification to the SRA or other stakeholders.

Operationally, the approach to all breaches—even administrative or technical ones without an immediate shortfall—must be swift and systematic: identify, assess risk, determine required entries, restore the position, and document both the reason and correction for audit purposes. Prompt documentation is essential, both for regulatory compliance and for ensuring that future problems can be prevented or quickly resolved.

Test Tip: In SQE-style questions on Accounting entries required to rectify breaches, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Exam Warning: Do not rely on a familiar phrase from Accounting entries required to rectify breaches alone; check whether the facts satisfy every condition, exception, and timing requirement.

The Duty to Correct Breaches Promptly

Rule 6.1 of the SRA Accounts Rules is unequivocal: upon discovery of a breach, the firm must remedy it promptly. The duty is non-negotiable and immediate where client money has been improperly withheld, misapplied, or wrongly withdrawn. For example, if a payment is made from a client account on behalf of an individual who lacks sufficient funds, thereby misusing other clients' money, the missing amount must be restored—using the firm's resources—without delay.

Promptness, in the context of the Rules, is interpreted in light of the degree of risk to which client money has been exposed and whether, as a result of the breach, a client or third party might have become disadvantaged. Delays in recognition or response—even where the breach is inadvertent—can aggravate the regulatory seriousness of the situation. The SRA and reporting accountants view any unjustified delay or continued non-compliance as exacerbating the breach, especially when the issue is process-related and has caused repeat errors or risks to client money.

Firms must ensure that staff at all levels are regularly trained in recognising breaches and understand their obligation to bring matters to the attention of the COFA or a partner promptly. The manager(s) of a firm bear personal responsibility for ensuring that systems are robust, that corrections are made expediently, and that record-keeping is sufficient to allow for later scrutiny.

Key Term: COFA

The Compliance Officer for Finance and Administration, a designated senior individual within the firm responsible for ensuring regulatory compliance, investigating breaches, rectifying weaknesses, and reporting serious breaches to the SRA in accordance with the Codes of Conduct.

In practice, prompt rectification is only the first stage. A root cause analysis should follow: was this a one-off human error or symptomatic of system weakness (e.g. inadequate segregation of duties, weak sign-off controls for withdrawals, or unclear mixed receipt procedures)? The COFA should record the breach on the internal breach register, note materiality, and confirm whether the matter requires reporting to the SRA or inclusion in an accountant’s qualified report. Where control changes are implemented (policy revisions, additional training, enhanced reconciliations), firms should evidence these steps for future assurance.

Common Breaches and Rectification Entries

A range of common breaches demand rapid and precise rectification, and each requires specific accounting entries made in the firm’s ledgers. These include, but are not limited to:

Breaches of the SRA Accounts Rules require immediate replacement of client money, corrective ledger entries, records, and reporting of material breaches.

- Payment of client money into the wrong bank account (e.g., the business account instead of a client account), thereby breaching Rules 2.3 and 4.1.

- Payment of a business expense from client money, usually in breach of Rule 5.1, especially where insufficient funds are held on behalf of the specific client for whom the payment is made.

- Use of other clients’ money to cover a withdrawal (client account shortfall), representing a breach of fiduciary duty as well as Rule 5.3.

- Incorrect transfer of costs before billing (premature withdrawal for profit costs), which is not permitted under Rule 4.3.

- Posting errors, mixed receipts, or attribution of funds to the wrong client or matter; failure to return client funds promptly when the reason for holding them has ended; and providing prohibited banking facilities using the client account.

- Failures in the timely identification or correction of errors during routine reconciliations, or in accordance with internal control policies and procedures.

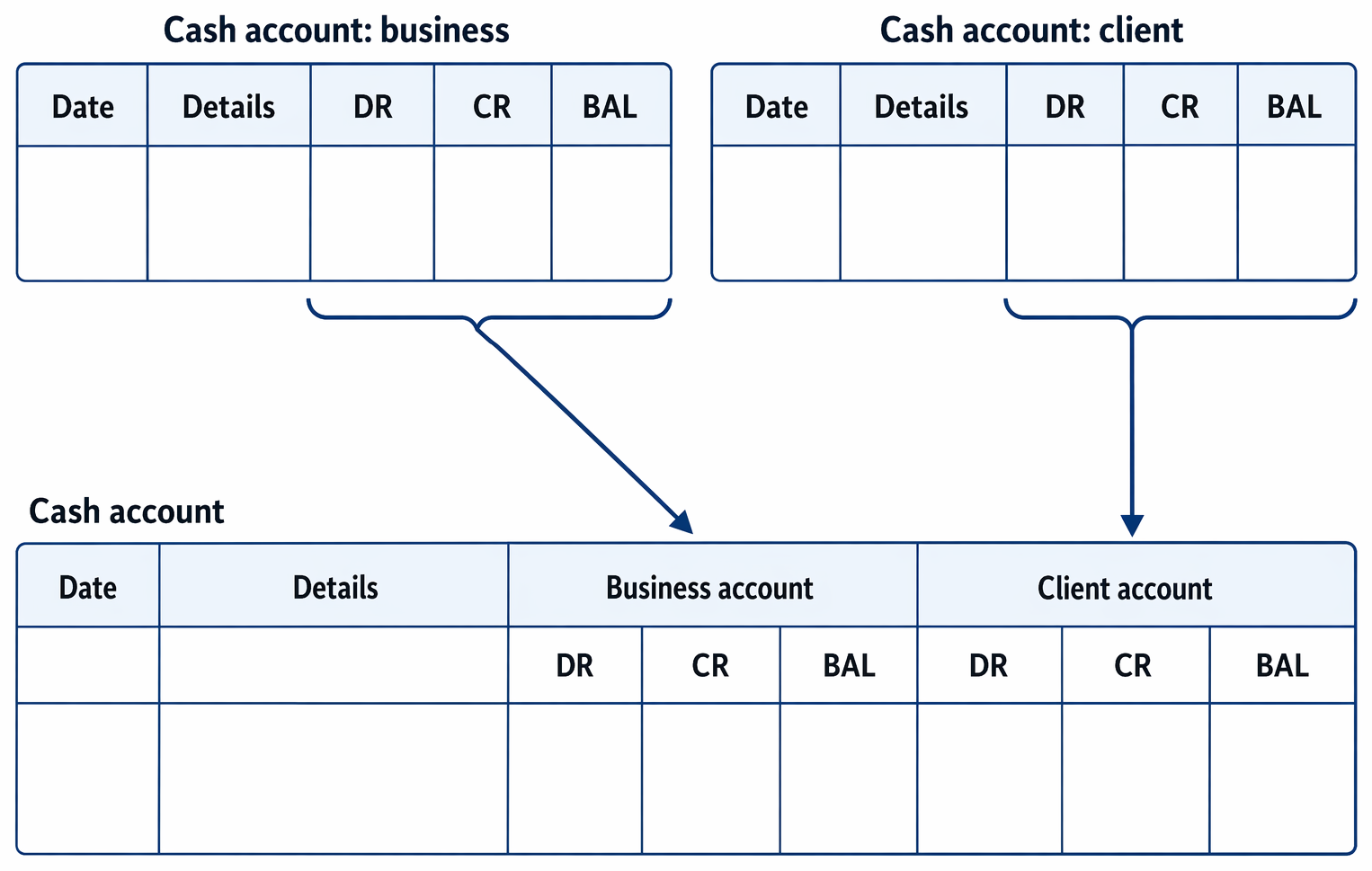

To rectify, the firm must generally reverse the initial incorrect entry and then enter the correct transaction. This may entail moving funds between bank accounts (business to client, or vice versa) and making corrections on both the client and business ledgers and the cash sheet. The two essential mechanisms are "cash transfers" (actual movements of funds between accounts) and "inter-client transfers" (paper transfers) for correcting ledger postings only.

Key Term: Cash transfer

A dual-entry, cross-account movement of money between business and client accounts to correct a prior error, involving simultaneous entries on both the client and the cash (bank) ledgers. Key Term: Inter-client transfer

The reattribution of funds between client ledgers or matters (e.g., correcting money posted to the wrong client), made solely as journal entries with no physical movement of cash between actual client or business bank accounts.

For each type of breach, the correct journal entries are essential to both restoring the firm’s compliance and providing an audit trail for future scrutiny, including by reporting accountants and the SRA. The guiding principle is always immediate replenishment (not simply adjustment in the ledgers) of any sums that have been withdrawn, withheld, or misapplied.

Use of Client Money for Business Payments

One of the most serious and frequently examined breaches is the use of client account balances to pay for a business expense, especially where insufficient funds are held on behalf of the specific client for whom the payment is made. This not only violates Rules 5.1 and 5.3 but risks exposing the firm to breach of fiduciary duty and possible claims in breach of trust.

Immediate rectification demands that the firm restores the missing client money by:

- Transferring the identical amount from the business bank to the client bank account, irrespective of any arrangements with the specific client, as the duty is to all clients whose funds were exposed, not only the one for whom the payment was made.

- Recording the corresponding correcting entries in the relevant ledgers, ensuring both the cash movement and the true attribution of liability appear clearly in the client ledger business columns.

The correct double entries for this restoration (cash transfer, business to client) are as follows:

- DR (debit) Client Ledger Business Account (reflecting a firm receivable—the debt due from the client for the business expense paid)

- CR (credit) Cash Sheet Business Account (money leaving business bank)

- CR Client Ledger Client Account (money arriving in client ledger)

- DR Cash Sheet Client Account (money entering client bank)

Narratives must be explicit (e.g. “Rectification of breach: business expense wrongly paid from client account on [date]; replacement from business bank”). Never net-off corrections or hide breaches by internal re-coding without visible audit trail.

Worked Example 1.1

A firm pays its £500 electricity bill using a cheque drawn on the general client bank account by mistake. The error is discovered the next day.

Answer:

This constitutes an improper withdrawal in breach of Rule 5.1 and Rule 5.3. The firm must immediately replace the £500 by transferring it from the business bank account. Accounting Entries:

- DR Client Ledger Business Account (Electricity Expense) £500

- CR Cash Sheet Business Account £500

- CR Client Ledger Client Account (for the client from whose account the funds were wrongly used) £500

- DR Cash Sheet Client Account £500

It is essential for the audit trail that the initial incorrect posting is not simply deleted but is reversed, and the correcting entries are clear and cross-referenced in the narrative. Internal policy should require contemporaneous explanations for such rectification entries, referencing the breach and the correction, for both compliance review and ensuing reconciliations.

Client Account Overdrawn (Shortfall)

A “client account shortfall” arises where withdrawals are made for a particular client, but there are insufficient funds held on their behalf in the client bank account. This indicates that money belonging to other clients has been used (improperly) to make the payment in violation of Rule 5.3, and is always regarded as a serious breach, requiring immediate action.

Whether the shortfall results from an error, a delay in funds clearing, or a posting mistake, the procedure is always the same:

- Calculate the precise deficit on the client ledger for the matter concerned.

- Transfer the matching sum from the business bank account to the client bank account, thus restoring all other clients to their full entitlement.

- Document the cause of the breach and the rectification taken.

The accounting entries for this business-to-client cash transfer are:

- DR Client Ledger (affected client) Business Account (showing a debt to the firm)

- CR Cash Sheet Business Account

- CR Client Ledger (affected client) Client Account

- DR Cash Sheet Client Account

Worked Example 1.2

A solicitor pays counsel's fees of £1,200 for Client X from the client bank account, but the client ledger for Client X only shows a credit of £1,000—creating a £200 shortfall.

Answer:

This is a breach of Rule 5.3. £200 belonging to other clients has been wrongly used. The breach is rectified by replacing the £200 from the business bank account immediately. Accounting Entries:

- DR Client Ledger (Client X) Business Account £200

- CR Cash Sheet Business Account £200

- CR Client Ledger (Client X) Client Account £200

- DR Cash Sheet Client Account £200

Now, Client X’s business-side entry reflects a debt to the firm, and the client bank account is restored to compliance for all clients.

Dishonoured Cheques and Uncleared Funds

When a client’s cheque is paid into the client account and payments are made before it clears, a dishonour creates a shortfall for that client. Rule 6.1 requires the immediate replacement of any resulting deficit in the client bank account using the firm’s own resources.

The standard sequence is:

- Reverse the earlier receipt on the ledgers (to remove the credit for funds that ultimately did not clear).

- Transfer enough business money to correct any debit now shown in the client ledger.

Firms should adopt a policy to not draw against uncleared cheques (or to restrict this to low-value and low-risk items where appropriate). Many modern systems flag uncleared items so fee earners cannot authorise withdrawals until cleared balances show on the cash sheet.

Worked Example 1.3

On Monday, the firm receives a £500 cheque from Client V on account and pays it into client bank account. On Tuesday, the firm pays a £100 court fee from the account for Client V. By Thursday, the bank notifies the cheque is dishonoured.

Answer:

Reverse the earlier receipt for £500 and then immediately replace the £100 shortfall from business money.

- DR Client Ledger (Client V) Client Account £500

- CR Cash Sheet Client Account £500

- DR Client Ledger (Client V) Business Account £100

- CR Cash Sheet Business Account £100

- CR Client Ledger (Client V) Client Account £100

- DR Cash Sheet Client Account £100

The end result is that the shortfall has been made good, and future payments from the client account for Client V must not be made until sufficient cleared funds are present. Internal control procedures should flag uncleared funds and prohibit premature withdrawals.

Client Money Paid into the Business Account

If a receipt that is client money is incorrectly paid into the business bank account instead of the client account (in breach of Rule 2.3), the error must be corrected by transferring the money promptly, even if only a short time elapses.

The necessary journal entries:

- DR Client Ledger Business Account

- CR Cash Sheet Business Account

- CR Client Ledger Client Account

- DR Cash Sheet Client Account

This brings the physical funds and the audit trail back into compliance.

Worked Example 1.4

The firm receives £400 on account of costs and unpaid disbursements for Ms Lee but banks it into the business account in error, with no bill delivered.

Answer:

The £400 is client money, so must be transferred into the client account immediately.

- DR Client Ledger (Ms Lee) Business Account £400

- CR Cash Sheet Business Account £400

- CR Client Ledger (Ms Lee) Client Account £400

- DR Cash Sheet Client Account £400

This ensures the firm is not holding client money in the wrong account and avoids further breach. The narrative in the ledger and on the cash sheet should state the rectification and the date the breach was discovered.

Business Money Paid into the Client Account

The reverse situation occurs when business money (e.g. in payment of a bill) is credited to the client bank account, often inadvertently. The SRA Accounts Rules (Rule 4.1) require that business money must be transferred promptly out of the client account.

The correct accounting entries for the transfer are:

- DR Client Ledger Client Account (to clear the client’s liability in the client ledger)

- CR Cash Sheet Client Account (money leaves client bank)

- DR Cash Sheet Business Account (money enters business bank)

- CR Client Ledger Business Account (the client’s liability is cleared)

Worked Example 1.5

A client pays a £360 bill (including VAT) via bank transfer, but it arrives in the client bank account.

Answer:

This is business money, so must be transferred promptly into the business bank account.

- DR Client Ledger (client) Client Account £360

- CR Cash Sheet Client Account £360

- DR Cash Sheet Business Account £360

- CR Client Ledger (client) Business Account £360

After this, the outstanding bill is cleared, and the client account is restored to the correct position.

Costs Taken Without Entitlement (No Bill Delivered)

No transfer may be made from client to business account to pay for profit costs until a bill (or written notification of costs) has been delivered to the client (see Rule 4.3). If money is withdrawn for costs without this entitlement, it is a clear breach.

The correct remedy is:

- Replace the amount withdrawn by transferring it from business to client, as per previous cash transfer patterns, and record the correction in both the client and cash ledgers.

- After proper billing, make a compliant transfer from client to business account.

In addition, note the SRA guidance on billing for future work/anticipated disbursements: although a bill may include anticipated items, any unincurred disbursement billed should remain in the client account until it is paid to the third party. Prematurely removing such sums to the business account would be a breach; rectify as above.

Worked Example 1.6

£900 is withdrawn from a client ledger for profit costs, but no bill is delivered.

Answer:

Replace £900 immediately into the client bank account.

- DR Client Ledger (client) Business Account £900

- CR Cash Sheet Business Account £900

- CR Client Ledger (client) Client Account £900

- DR Cash Sheet Client Account £900

Subsequently, a proper bill must be delivered and only then may a correct client-to-business transfer be completed. It is essential that records show both the premature withdrawal and its rectification.

Disbursement Posting Errors (Agency vs Principal Method)

Errors can occur where the distinction between agency and principal disbursements is overlooked. When an invoice is in the firm's name (principal method), it must be paid from the business bank account, with VAT entered into the firm’s records. If the payment is instead made from the client account, client money is misapplied and must be restored.

Key Term: Agency method

For invoices in the client’s name; the total (including VAT) is paid from the client account, and no entry is made to the firm’s VAT account or ledger. Key Term: Principal method

For invoices in the firm’s name; the payment is made from the business account, both input and output VAT are recorded by the firm, and the costs are recharged to the client through billing.

If, for example, a surveyor’s fee (invoice addressed to the firm) is paid out of client account, both the sum and associated VAT must be restored to the client bank account from the business bank account, with VAT properly accounted for.

Rectification when the principal method is breached:

- Restore client funds via a cash transfer (business to client) for the full VAT-inclusive amount.

- Post the business-side entries, including VAT, as if the firm had paid correctly from the business account.

Worked Example 1.7

A surveyor’s invoice (£1,200 + £240 VAT) is addressed to the firm, but is paid from the client bank account.

Answer:

Restore the client account immediately, then post business-side and VAT entries correctly.

- DR Client Ledger (client) Business Account £1,440

- CR Cash Sheet Business Account £1,440

- CR Client Ledger (client) Client Account £1,440

- DR Cash Sheet Client Account £1,440

Post the proper principal method: CR Cash Sheet Business Account £1,200; DR Client Ledger Business Account £1,200; DR HMRC/VAT Ledger £240; CR Cash Sheet Business Account £240.

Subsequent recharging to the client is done when issuing the bill.

Mixed Receipts Paid into the Wrong Account

Mixed receipts—such as a payment covering both a delivered bill (i.e. business money) and further sums on account (client money)—must be split appropriately. If all the money is initially paid into the wrong account (usually the client account), an immediate transfer of the business money to the business account must be made.

Best practice when receiving mixed receipts:

- Option 1: Ask the payer to split the transfer (ideal).

- Option 2: If one bank account receives the whole sum, promptly transfer the portion that belongs to the other bank.

If paid wholly into the client account:

- Transfer the business portion from client to business account.

If paid wholly into the business account:

- Transfer the client portion from business to client account.

Worked Example 1.8

£750 is received into the client bank account: £550 is payment of a delivered bill (business money), and £200 is on account (client money).

Answer:

Promptly transfer £550 to the business account (client-to-business transfer). £200 remains as client money.

- DR Client Ledger Client Account £550

- CR Cash Sheet Client Account £550

- DR Cash Sheet Business Account £550

- CR Client Ledger Business Account £550

This maintains compliance in treatment and prevents commingling of funds.

Inter-Client Misposting (Wrong Ledger/Matter)

Where a receipt or payment is attributed to the wrong client ledger (e.g., attributed to Matter B when intended for Matter A), this is corrected by a paper transfer—making debit and credit entries in the affected ledgers, but no entries on the cash sheet.

Correction entries:

- DR the client ledger that is owed funds (correct matter/client)

- CR the client ledger that incorrectly received funds

A paper transfer must never be used to disguise improper withdrawals or loans between clients. It can only reattribute money already in the client bank to the correct ledger owner.

Worked Example 1.9

£1,000 due to Client R (Matter A) is incorrectly credited to Client S (Matter B).

Answer:

Paper transfer (inter-client): DR Client R – Matter A Client Account £1,000; CR Client S – Matter B Client Account £1,000. No cash sheet entries are required, preserving the accuracy of the client bank account while correcting the ledger allocation.

Returning Client Money Promptly and Residual Balances

Rule 2.5 enforces the duty to return client money as soon as there is no longer a proper reason to retain it. In transaction closures, probate, or concluded litigation, the firm must pay balances to the client as soon as the legal work is complete, absent any justified retention (such as outstanding costs, anticipated disbursements, or instructions to hold pending further matters).

Where the client (or beneficiary) cannot be traced or where the balance is not claimed despite reasonable steps, the SRA authorises payment of residual balances under specific conditions:

- Balances up to £500 per client/matter may be paid to charity after documented, reasonable efforts to trace the client.

- A central register of such payments and evidence of tracing must be kept for audit purposes; receipts from the charity and any indemnity provided must be retained.

- For sums above £500, SRA authorisation is required (see current SRA guidance for the procedure).

- No deduction may be made for tracing costs from the residual balance itself.

- Keep thorough records for at least six years.

Key Term: Residual client balance

An amount held for a client or third party which remains unreturned after completion of the engagement and exhaustion of reasonable efforts to contact or trace the client.

Practical tracing steps typically include: checking the client file for updated contact details, internet and directory searches, electoral roll checks, letter-forwarding services, and contacting known intermediaries. The breadth of steps should be proportionate to the amount and age of the balance and the details available.

Worked Example 1.10

£325 remains on a closed matter for over a year; the client cannot be traced.

Answer:

Pay the £325 to a charity, ensuring compliance by updating the central register and retaining all documentation of tracing steps and the charity’s receipt.

- DR Client Ledger (matter) Client Account £325

- CR Cash Sheet Client Account £325

If the client later emerges, the charity indemnifies the firm so that the rightful owner may reclaim the sum. The central register should show date, matter, charity, and amount, along with details of the tracing attempts undertaken.

Banking Facilities Prohibition (and How to Rectify)

Rule 3.3 strictly prohibits any use of the client account as a personal or business banking facility. The only permissible movement of funds is linked directly to a matter in which the firm is providing regulated legal services. It is not sufficient for the instruction to come from the client; there must be a clear link to a legal transaction being handled by the firm.

If a client requests that their funds be held to pay unrelated expenses (such as monthly rental payments not arising from a legal matter, or payments to unrelated third parties), the firm must refuse, return the funds, and cease acting if necessary.

Correction entries:

- Return non-permissible funds to the client: DR Client Ledger Client Account; CR Cash Sheet Client Account.

If improper payments have already been made, ensure full replacement using business funds, as for any other shortfall. Document the breach and the steps taken to avoid similar risks in future, as improper use of the client account not only breaches the Rules, but potentially gives rise to risks of money laundering, regulatory penalties, and disciplinary sanctions.

Firms must also assess whether such misuse of the client account constitutes a material breach, requiring notification in their accountant’s report and possible direct reporting to the SRA, especially where there are indicators of external pressure, insolvency risk, or attempted circumvention of law or regulation.

Worked Example 1.11

After a sale completes, a client instructs the firm to retain £20,000 in the general client account and to pay their monthly school fees of £2,000 for the next 10 months. No related legal work is ongoing.

Answer:

This would breach Rule 3.3 (banking facilities). The firm should refuse and return the £20,000 promptly to the client. If any fee payments were already made, immediately replace the withdrawn sums from the business bank, post the corrective cash transfer, and record the breach and remedial steps.

Worked Example 1.12

A firm receives £1,200 into the business bank account by transfer. The payer intended £900 as payment of an issued bill and £300 on account for a new matter.

Answer:

£900 is business money; £300 is client money. Promptly transfer £300 from the business bank to the client bank and record the journal entries:

- DR Client Ledger (new matter) Business Account £300

- CR Cash Sheet Business Account £300

- CR Client Ledger (new matter) Client Account £300

- DR Cash Sheet Client Account £300

The £900 receipt is recorded as: CR Client Ledger (billed matter) Business Account £900; DR Cash Sheet Business Account £900.

Worked Example 1.13

A valuation invoice for £600 + £120 VAT is addressed to the client. The cashier mistakenly posts input VAT and pays it from the business bank.

Answer:

Agency method applies (invoice in client’s name). Reverse the improper VAT postings (business-side) and reimburse the business bank from the client bank:

- If the firm paid from business bank: DR Client Ledger Business Account £720; CR Cash Sheet Business Account £720; then CR Client Ledger Client Account £720; DR Cash Sheet Client Account £720; pay the third party from client account. Remove any incorrect VAT entries in HMRC-VAT ledger (narrative cross-reference).

Worked Example 1.14

A counsel fee £1,800 + VAT is in the firm’s name. It is paid from client account in error and no bill has yet issued.

Answer:

Replace £2,160 to the client account from business bank immediately (business-to-client cash transfer), then post the principal method correctly:

- DR Client Ledger Business Account £2,160; CR Cash Sheet Business Account £2,160; CR Client Ledger Client Account £2,160; DR Cash Sheet Client Account £2,160 (rectification)

- CR Cash Sheet Business Account £1,800; DR Client Ledger Business Account £1,800; DR HMRC-VAT Ledger £360; CR Cash Sheet Business Account £360 (principal method postings)

- Bill and recover from client in due course.

Worked Example 1.15

A mortgage advance is received into the buyer’s client ledger using the single-ledger method. By mistake, £500 is posted to the seller’s ledger within the same client. No money left the bank.

Answer:

Correct by inter-client/matter paper transfer only (no cash entries):

- DR Buyer’s client ledger client account £500

- CR Seller’s client ledger client account £500

Add narrative: “Paper transfer—correcting misposting of receipt; no cash movement.”

Worked Example 1.16

A firm withdrew £2,000 from the client account to cover costs based on an estimate. Later, the bill is reduced after an abatement to £1,500 + VAT (£1,800).

Answer:

The excess £200 must be returned to client account promptly:

- DR Client Ledger Business Account £200

- CR Cash Sheet Business Account £200

- CR Client Ledger Client Account £200

- DR Cash Sheet Client Account £200

Ensure the client ledger reflects the abated bill values and the remaining £1,800 business-side entries are accurate.

Worked Example 1.17

A client’s cheque for £2,000 on account is banked and the firm pays £350 court fee the next day. Two days later the cheque bounces. A second payment of £700 for a search fee is also made before the dishonour is known.

Answer:

Reverse the £2,000 receipt; immediately replace the combined shortfall of £1,050 from business funds:

- DR Client Ledger Client Account £2,000; CR Cash Sheet Client Account £2,000 (receipt reversal)

- DR Client Ledger Business Account £1,050; CR Cash Sheet Business Account £1,050

- CR Client Ledger Client Account £1,050; DR Cash Sheet Client Account £1,050

Review policy on drawing against uncleared funds.

Worked Example 1.18

A mixed receipt (£1,000) is paid into client bank: £700 is a billed amount; £300 is on account for future disbursements. The cashier mistakenly transfers £1,000 to business bank.

Answer:

Correct the £300 error immediately by cash transfer business-to-client:

- DR Client Ledger (client) Business Account £300

- CR Cash Sheet Business Account £300

- CR Client Ledger (client) Client Account £300

- DR Cash Sheet Client Account £300

Ensure narratives state “rectification of mixed receipt allocation error”.

Worked Example 1.19

Following completion, the firm receives an instruction to pay a £10,000 supplier wholly unrelated to the legal work, from sale proceeds still held.

Answer:

Decline the instruction (Rule 3.3) and return the net proceeds to the client promptly. If payment was mistakenly made, replace the amount from business bank immediately and record the breach and remediation.

Worked Example 1.20

A firm holds client money (£100,000) in a separate designated deposit client account (SDDCA). On closure, £300 bank interest has accrued. Funds are transferred back to the general client account.

Answer:

Record receipt into the general client account for the full amount including interest as client money:

- CR Client Ledger Client Account £100,300

- DR Cash Sheet Client Account £100,300

Later, distribute or apply according to the client’s matter and interest policy.

Controls, Reconciliations and Documentation When Rectifying Breaches

Rectifying entries must be matched by robust control behaviours:

- Reconciliations: Obtain bank statements and reconcile the client bank to the cash sheet and client ledgers at least every five weeks. Differences must be investigated and resolved promptly before the reconciliation statement is signed by the COFA or a manager.

- Segregation of duties: Authorisation for withdrawals should be restricted to appropriately trained individuals; consider dual authorisation for higher values.

- Narratives and cross-references: Every rectification entry should state why it was necessary, the original breach date, and cross-reference to the original ledger line(s). Never post net entries that conceal the error.

- Breach register: Maintain a central log of breaches (including whether material), the cause, remedial steps, and any control improvements implemented.

- Training and policy updates: Where a pattern arises (e.g., mixed receipts frequently misallocated; repeated premature costs withdrawals), update procedures and deliver targeted training.

Breaches discovered at reconciliation require immediate action. If reconciliation reveals that the balance on the cash sheet exceeds or is less than the total of clients’ ledger balances, identify mispostings, uncleared items, or bank errors. Until resolved, the firm should not draw any surplus unless it has been fully explained and is agreed to be business money. A deficit must be made good immediately from business funds while investigating.

Record-Keeping and Reporting Responsibilities

Accurate records underpin all rectifications:

- Ledgers: Maintain client ledgers for each client/matter, and ensure the running balance in both client and business columns is readily ascertainable.

- Cash sheet: Record every receipt and withdrawal in the correct bank columns with clear narratives.

- VAT and profit costs ledgers: Ensure only business items appear; never post VAT entries for agency disbursements.

- Interest payable ledger: Where sums in lieu of interest are due to clients (general client account), record as a business expense before transferring business-to-client.

Reporting obligations:

- Accountant’s report: Most firms that hold client money must obtain an accountant’s report within six months of the end of their accounting period. A report is delivered to the SRA only if qualified (serious breaches or risks to client money).

- Immediate SRA notification: Serious breaches or suspected dishonesty must be reported promptly to the SRA in line with the Codes of Conduct.

- COFA role: The COFA should ensure that breaches are recorded, assessed for materiality, and escalated promptly where required.

Interest Errors and Rectification

Where the firm’s interest policy requires a payment in lieu of interest from the business account (for money held in the general client account):

-

Step 1: Record the business expense:

- DR Interest Payable Ledger (business)

- CR Client Ledger Business Account (for the client entitled to the sum)

-

Step 2: Transfer the sum from business to client:

- DR Client Ledger Business Account; CR Cash Sheet Business Account

- CR Client Ledger Client Account; DR Cash Sheet Client Account

If the firm misclassifies such payments or posts them only in the client ledgers, rectify to ensure the business expense and the cash transfer are both correctly recorded. For SDDCAs, interest received is client money and is credited in the client account columns (no business interest payable ledger is used).

Additional Pitfalls and How to Correct Them

- Cheques payable to the client or third parties: A cheque not made payable to the firm is not client money unless converted to cash—do not bank it; forward it promptly. If incorrectly banked, reverse and rectify.

- Private loans between clients: Do not use the client account to facilitate a private loan unless both lender and borrower give appropriate written authorities, and even then consider whether the transaction risks breaching Rule 3.3.

- Duplicate receipts or payments: If a receipt is posted twice (ledger error), reverse the duplicate. If a payment is posted twice, replace any client shortfall via business-to-client cash transfer while resolving bank recovery for the duplicate.

- Reversals vs corrections: Use reversal entries to remove incorrect postings and then enter correct ones. Avoid overwriting historic entries; the audit trail is essential.

Key Point Checklist

This article has covered the following key knowledge points:

- The SRA Accounts Rules require all breaches to be corrected promptly upon discovery, with immediate replacement of client money where required, regardless of how the error occurred or by whom.

- Breaches of accounting rules are most frequently due to misapplication of client funds, improper withdrawals, mispostings between ledgers or accounts, improper receipt or late return of balances (including residual balances), premature transfer to the business account, or providing banking facilities.

- Rectification of a client account shortfall is achieved by transferring the necessary funds from the business bank account to the client bank account and making corresponding accounting entries in the correct ledgers, with additional documentation explaining the breach and the correction.

- Cash transfers between business and client accounts require careful journal entries in both the business and client columns of the cash sheet and client ledger, and the corresponding correction must be made promptly (not delayed until routine reconciliation).

- Where client money is paid into the business account in error (e.g., receipt on account before a bill is delivered), the identical amount must be transferred into the client account immediately using a business-to-client transfer, properly referenced and cross-referenced to the original error.

- If business money is received into the client bank account, the relevant sum must be promptly transferred to the business bank account to avoid commingling and to ensure transparency in the treatment of client and firm funds.

- Dishonoured client cheques and withdrawals against uncleared funds resulting in negative client ledger balances trigger an immediate duty to make good the client account with business money, and prevent the use of other clients’ funds to cover specific client payments.

- Sums transferred from the client account as fees or costs before entitlement arises (no bill delivered) must be replaced at once, with accurate rectification entries and proper billing procedure thereafter, and the records must demonstrate the chronology and rationale of transactions for any auditor or regulator.

- Disbursement posting errors involving the agency/principal distinction require immediate correction to restore client money (including, for principal method errors, proper posting to the VAT and business ledgers and, if necessary, clarifying entries in all affected ledgers).

- Mixed receipts (business and client money) must be allocated and transferred to the correct accounts without delay. Failure to act promptly is a breach of Rule 4.2.

- Mispostings between client ledgers are rectified solely by inter-client or inter-matter transfers (paper transfers); these do not involve physical movement of funds but must be supported by clear narrative and internal documentation.

- Client monies must be returned without delay at the end of matters once there is no longer any proper reason to retain them; residual balances where the client cannot be traced are dealt with under specific SRA-authorised procedures (including the £500 charity route and central register requirements).

- Use of client accounts as banking facilities is strictly prohibited; breaches must be rectified promptly by ceasing the practice, returning money to the client, and reviewing controls to prevent recurrence. Failures to comply may trigger both qualification of the accountant’s report and direct SRA investigation.

- Firms must maintain and regularly reconcile records to ensure client accounts are never overdrawn, and that shortfalls are identified and fixed promptly.

- The COFA and all managers have a continuing duty to monitor for breaches, ensure documentation is up-to-date and accurate, act rapidly upon breach, and escalate material issues to the SRA or auditors where appropriate.

- All procedures and corrections must be well documented and auditable—secure retention of records for a minimum of six years is required under the Rules.

Key Terms and Concepts

- Breach

- Rectification

- Client Account Shortfall

- COFA

- Cash transfer

- Inter-client transfer

- Agency method

- Principal method

- Residual client balance

Key Term: Client Account Shortfall

A situation where a client's ledger card or matter is in debit—indicating that more money has been withdrawn on a client's account than is held for that client, meaning other clients' money is at risk. It must be rectified immediately by replacing the shortfall from the firm's own funds. Key Term: Residual client balance

An unreturned sum of client money left after the conclusion of a matter or transaction, including situations where the client or beneficiary cannot be traced. Specific SRA procedures govern the withdrawal of such balances, especially those over £500. Key Term: COFA

Compliance Officer for Finance and Administration—an individual responsible within a law firm for monitoring and ensuring its compliance with the SRA Accounts Rules and ready correction of breaches. Key Term: Cash transfer

The transfer of funds between client and business bank accounts, accompanied by appropriate double entries in the cash sheet and ledgers to ensure the accuracy of the accounting records. Key Term: Inter-client transfer

A process for reallocating funds between client ledgers or matters without the movement of physical cash between accounts, achieved solely through offsetting entries in the ledgers. Key Term: Agency method

Payment of a third-party invoice addressed to the client, paid from the client account. The firm acts as agent, and records are kept only in the client ledger and cash sheet (VAT-inclusive amount); no entry to the firm’s VAT records. Key Term: Principal method

Payment of a third-party invoice addressed to the firm (business), paid from the business account. The firm records both input and output VAT, and sells the service onward to the client when billing. Key Term: Breach

Any instance of non-compliance, whether administrative or substantive, with the SRA Accounts Rules including improper handling of client money, delays or errors in returns or withdrawals, and failures in recording or reporting.

Summary

Rectifying breaches of the SRA Accounts Rules is a practical, ledger-driven task governed by a clear regulatory imperative: act promptly and restore client money immediately. Most corrections fall into a few patterns—cash transfers between client and business accounts, paper transfers between ledgers, and reversals of incorrect postings—each requiring accurate journal entries and meticulous narratives. Robust reconciliations, COFA oversight, and well-documented processes ensure not only that mistakes are fixed but that they do not recur. By understanding the entries set out above and applying them without delay, firms protect client funds and demonstrate the professional standards required by the SRA.