Learning Outcomes

This article explains the accounting treatment of client account transactions for SQE1 FLK2, focusing on how to post accurate double-entry records in the client ledger and cash account. It explains the distinction between client money and business money, how to record receipts on account of costs, payments of disbursements and other third-party outgoings, and how to deal with transfers to the business account once a bill or written notification of costs has been delivered. It covers mixed receipts that contain both client and business elements, inter-client transfers between matters, and client-to-business transfers, ensuring that no client ledger becomes overdrawn. It outlines the SRA Accounts Rules that govern prompt banking of client money, proper withdrawals, allocation and reconciliation requirements, and the prohibition on using the client account as a banking facility. It also details the VAT treatment of disbursements under the agency and principal methods, stakeholder versus agent status for deposits and mortgage advances in property work, and how to calculate and record sums in lieu of interest. Finally, it reviews how to identify and correct common breaches, including dishonoured cheques and mispostings, using appropriate business-to-client transfers.

SQE1 Syllabus

For SQE1, you are required to understand the correct accounting entries for client account transactions and associated SRA compliance, with a focus on the following syllabus points:

- the distinction between client money and business money, and how each is recorded

- the double-entry bookkeeping system as applied to client account transactions

- the correct accounting entries for receipts and payments involving client accounts

- handling mixed receipts (client and business money in one payment)

- compliance with SRA Accounts Rules for client account transactions

- the requirements for record-keeping, reconciliation, and prompt allocation of funds

- transfers from client to business accounts following delivery of a bill

- inter-client transfers (paper transfers) between client ledgers

- treatment of VAT on disbursements (agency and principal methods) and related entries

- stakeholder versus agent handling of deposits in property transactions

- accounting for interest due to clients on money held

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the correct double-entry accounting entries for receiving client money on account of costs?

- How should a law firm record a payment made from the client account on behalf of a client?

- What is the required treatment when a firm receives a mixed payment containing both client money and business money?

- True or false? Client money can be paid into the business account if it is more convenient for the firm.

Introduction

Client account transactions are a core part of solicitors’ accounts and are strictly regulated by the SRA Accounts Rules. For SQE1, you must be able to identify and apply the correct accounting entries for receipts and payments involving client money, ensure compliance with the rules, and understand the principles of double-entry bookkeeping as they apply to legal practice. Accuracy in the ledgers is supported by robust systems and controls: firms must maintain contemporaneous records showing all receipts and payments on both the client and business sides of the client ledger, and keep a cash account for each bank account operated. Regular reconciliations of client accounts are required at least every five weeks and must be signed off by an appropriate manager or the COFA, with differences promptly investigated and resolved.

Key Term: client money

Money held or received by a solicitor relating to regulated services delivered to a client, or on behalf of a third party in relation to regulated services, or as a trustee or holder of a specified appointment, or in respect of fees and unpaid disbursements before a bill is delivered. Key Term: business money

Money belonging to the law firm, including fees received after a bill is delivered, reimbursements for paid disbursements, and other firm income. Key Term: COFA

The Compliance Officer for Finance and Administration is responsible for ensuring the firm complies with the SRA Accounts Rules, including monitoring systems and controls and signing reconciliation records.

Client money must be available on demand unless alternative arrangements are agreed in writing with the client or third party. When there is no longer a proper reason to hold client money, it must be returned promptly. Firms must not use the client account to provide banking facilities to clients or third parties—payments into and out of client account must relate to the delivery of regulated legal services in the matter concerned.

Test Tip: In SQE-style questions on Accounting entries required for client account transactions, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Client Money and Business Money: The Distinction

Solicitors regularly handle money belonging to clients as part of legal transactions. It is essential to keep client money separate from the firm’s own business money at all times. Receipts of client money must be banked promptly into a client account (unless a specific exception applies). By contrast, business money is paid into a business account.

Money on account of costs and unpaid disbursements (before a bill is delivered) is client money. Once a bill is delivered, amounts paid in settlement of that bill are business money. Reimbursements for disbursements already paid out of the firm’s business account are also business money, even if received before or alongside a bill.

Key Term: fees

The firm’s own charges (profit costs), including any VAT element, for legal services provided. Key Term: disbursements

Costs or expenses paid or to be paid to a third party on behalf of the client or trust (including any VAT element), excluding office expenses like postage and courier fees.

Certain limited exceptions permit client money to be withheld from a client account: for example, payments from the Legal Aid Agency for the firm’s costs, or where the only client money handled is on account of costs and unpaid disbursements and the firm otherwise does not maintain a client account (provided the client has been informed in advance where and how the money will be held).

Key Term: Legal Aid Agency (LAA)

The government body that funds specified legal services for eligible clients. Payments from the LAA for the firm’s costs fall within an exception permitting banking in the business account.

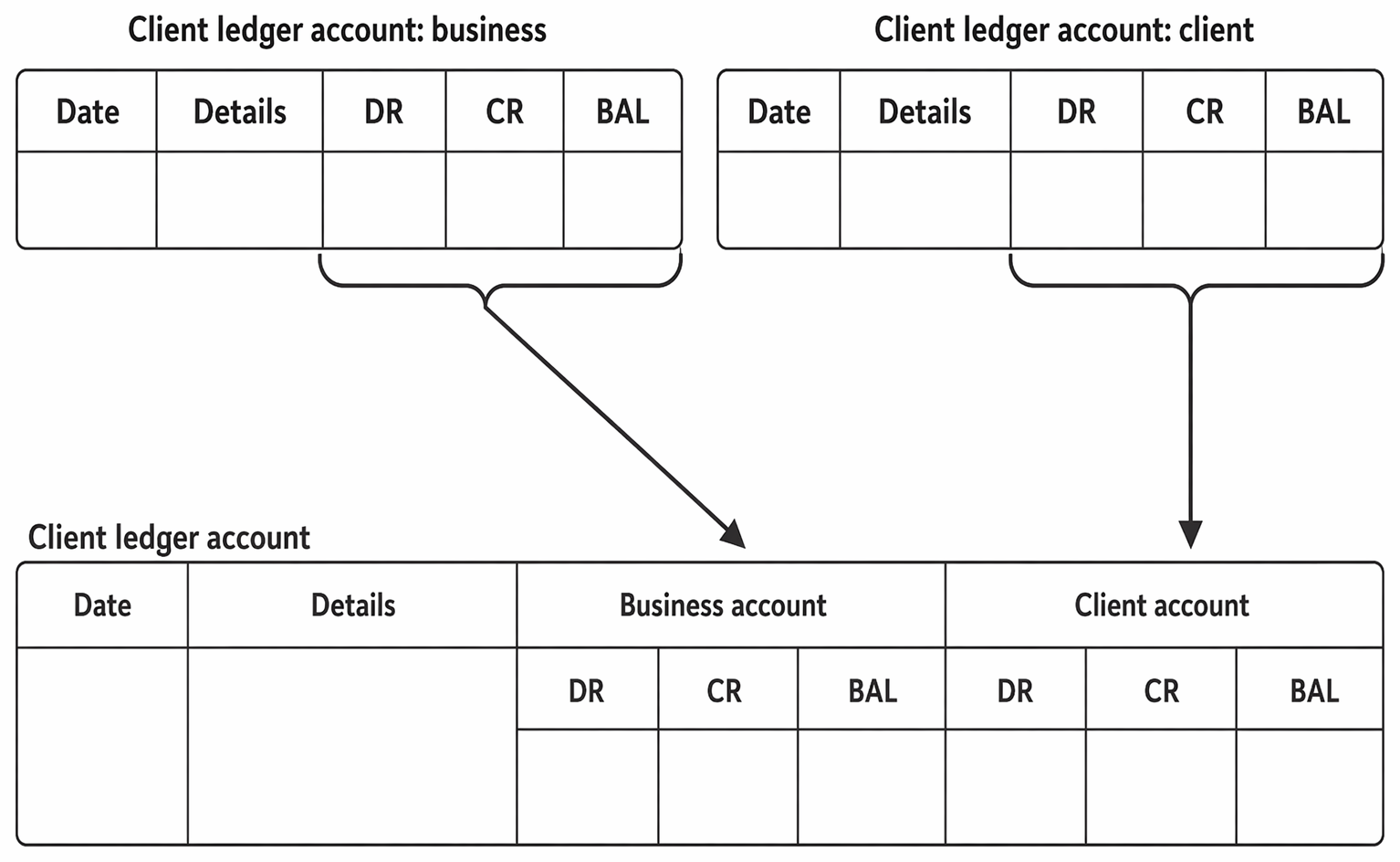

Double-Entry Bookkeeping and Ledgers

All accounting entries in solicitors’ accounts are made using the double-entry bookkeeping system. Every transaction must be recorded as a debit (DR) in one account and a credit (CR) in another, ensuring the books remain balanced. For client transactions, firms typically maintain dual ledgers, showing side-by-side the business and client columns for each client matter, and a cash account with separate columns for business and client bank accounts.

Client money transferred to and from a separate deposit account, with interest and withdrawals, is recorded by corresponding double-entry postings.

Key Term: double-entry bookkeeping

An accounting system where every transaction is entered twice: once as a debit and once as a credit, in two different accounts. Key Term: client ledger

A record for each client matter showing all receipts and payments of client and business money relating to that client. Key Term: cash account

The record of all money received into and paid out of the firm’s bank accounts, with separate columns for business and client accounts.

On the client ledger, money received (held for the client) appears as a credit (CR) in the client columns; money paid out appears as a debit (DR) in those columns. On the cash account, money received is a debit (DR), and money paid out is a credit (CR). A client account must not be overdrawn: a persistent or uncorrected overdrawn position indicates improper use of funds and must be remedied immediately.

Recording Receipts of Client Money

When a firm receives client money (for example, a retainer or funds for a transaction), the money must be paid promptly into the client account. The correct double-entry is:

- Debit (DR) the cash account (client side)

- Credit (CR) the client ledger (client side)

“Promptly” is not defined; firms should adopt policies reflecting the need to bank receipts without delay (for example, same day or next working day), consistent with robust risk controls.

Worked Example 1.1

A client pays £2,000 on account of costs by bank transfer. What are the correct accounting entries?

Answer:

Debit (DR) £2,000 to the cash account (client side); Credit (CR) £2,000 to the client ledger (client side) for that client matter.

Worked Example 1.2

A firm receives £900 from the LAA in respect of its costs in a criminal matter. How should this be recorded?

Answer:

Debit (DR) £900 to the cash account (business side); Credit (CR) £900 to the client ledger (business side) for that matter. LAA payments for the firm’s costs are an exception and may be paid into the business account.

Recording Payments from the Client Account

When making a payment from the client account on behalf of a client (such as paying a disbursement or sending funds to a third party), the entries are:

- Debit (DR) the client ledger (client side)

- Credit (CR) the cash account (client side)

Withdrawals must only be made for the purpose for which the money is held, in accordance with client instructions (or SRA authorisation), and only if sufficient funds are held for that client (Rule 5.3). Where insufficient client funds are held, payment should be made from business money (or after the client provides additional funds); using money held for other clients breaches the rules.

Worked Example 1.3

A solicitor pays £500 from the client account to a surveyor on behalf of a client. What are the correct entries?

Answer:

Debit (DR) £500 to the client ledger (client side) for the client; Credit (CR) £500 to the cash account (client side).

Worked Example 1.4

A firm holds £300 in the client account for a client. A search fee of £350 becomes payable. What must the firm do?

Answer:

The firm cannot withdraw more than is held for that client. It must either request a further £50 from the client, or pay the £350 from the business account and then seek reimbursement. If paid from business money, entries are: Debit (DR) £350 to the client ledger (business side); Credit (CR) £350 to the cash account (business side).

Recording Receipts and Payments of Business Money

Business money (such as payment of a bill or reimbursement for a paid disbursement) must be paid into the business account. The entries are:

- Debit (DR) the cash account (business side)

- Credit (CR) the client ledger (business side)

Worked Example 1.5

A client pays £1,200 in settlement of a bill after it is delivered. How should this be recorded?

Answer:

Debit (DR) £1,200 to the cash account (business side); Credit (CR) £1,200 to the client ledger (business side) for that client. Key Term: petty cash

A small amount of cash held by the firm for minor expenses. Petty cash is always business money; payments from petty cash are recorded on business ledgers, not the client cash account.

Worked Example 1.6

The firm pays a £25 taxi fare from petty cash to attend a hearing for Client A (no client funds are held). What are the entries?

Answer:

Credit (CR) £25 to the petty cash account; Debit (DR) £25 to Client A’s client ledger (business side), showing the client owes the firm for the expense.

Handling Mixed Receipts

A mixed receipt is a payment that includes both client money and business money (for example, a payment covering both a bill and funds for a transaction). The SRA Accounts Rules require the firm to allocate the funds promptly to the correct accounts.

Key Term: mixed receipt

A payment received by the firm that contains both client money and business money.

The firm may either split the payment between the client and business accounts or pay the whole amount into one account and promptly transfer the relevant part to the other account. While “promptly” is not defined, previous practice used indicative timescales (for example, within 14 days for client-to-business transfers). Firms should set and follow internal policies that ensure timely, accurate allocation.

Worked Example 1.7

A client sends a cheque for £5,500, comprising £5,000 for a property completion (client money) and £500 for the firm’s bill (business money). How should this be dealt with?

Answer:

The firm can either split the cheque and pay £5,000 into the client account and £500 into the business account, or pay the whole amount into one account and promptly transfer the appropriate sum to the other account. The entries must ensure that client money is not kept in the business account and business money is not kept in the client account.

Worked Example 1.8

A client makes a bank transfer of £1,000 consisting of £600 to settle a delivered bill (business money) and £400 on account of future costs (client money). The firm’s policy is to bank mixed receipts first into the client account, then transfer the business element. What are the entries?

Answer:

Receipt into client account: Debit (DR) £1,000 cash account (client side); Credit (CR) £1,000 client ledger (client side). Transfer of business element: Credit (CR) £600 cash account (client side); Debit (DR) £600 cash account (business side); Debit (DR) £600 client ledger (client side); Credit (CR) £600 client ledger (business side).

SRA Accounts Rules: Key Requirements

The SRA Accounts Rules set out strict requirements for handling client account transactions:

- Client money must be paid promptly into a client account.

- Only client money (and limited permitted sums) may be held in a client account.

- Withdrawals from the client account must only be made for the proper purpose and only if sufficient funds are held for that client.

- Mixed receipts must be allocated promptly to the correct account.

- All dealings must be recorded in the client ledger and cash account, with accurate, contemporaneous details and running balances readily ascertainable.

- Regular reconciliations of client accounts (at least every five weeks) are required and must be signed off; discrepancies must be investigated and resolved.

- Client money must be available on demand unless otherwise agreed in writing, and returned promptly when there is no longer a proper reason to hold it.

Key Term: inter-client transfer

A paper transfer between client ledgers reallocating money held in the client account from one client (or matter) to another, with no movement on the cash account. Key Term: stakeholder

Money held jointly on behalf of buyer and seller (typically a deposit on exchange). It remains jointly owned until completion, then belongs to the seller. Key Term: sum in lieu of interest

A fair amount paid to a client to reflect the interest their client money would reasonably earn while held by the firm. Key Term: agency method

VAT treatment when the third-party invoice is addressed to the client; the firm pays the VAT-inclusive amount on the client’s behalf and does not record VAT in its own HMRC ledger. Key Term: principal method

VAT treatment when the third-party invoice is addressed to the firm; the firm pays from business money, records input VAT, and recharges the VAT to the client on the firm’s bill.

VAT on disbursements

Where a third party’s invoice is addressed to the client (agency method), the firm pays the VAT-inclusive sum using client money if available (or business money if not) and records the total on the client ledger and cash account—no entry is made on the firm’s HMRC/VAT ledger. Where the invoice is addressed to the firm (principal method), it must be paid from business money; the net fee is recorded on the client ledger (business side), input VAT is recorded on the HMRC ledger, and the VAT is later recharged on the firm’s bill.

Worked Example 1.9

After delivering a bill of £900 (profit costs £750 + VAT £150), the firm transfers the sum from client to business account where funds are held on account. What are the entries?

Answer:

Client to business cash transfer requires two pairs of entries: Payment out of client account: Debit (DR) £900 client ledger (client side); Credit (CR) £900 cash account (client side). Receipt into business account: Debit (DR) £900 cash account (business side); Credit (CR) £900 client ledger (business side).

Worked Example 1.10

Client X asks the firm to transfer £2,000 held for her sale matter to her will-drafting matter (same client). What are the entries?

Answer:

Inter-client transfer (between matters): Debit (DR) £2,000 to Client X’s sale matter ledger (client side); Credit (CR) £2,000 to Client X’s will matter ledger (client side). No entry is made on the cash account.

Worked Example 1.11

A client’s cheque for £500 paid into the client account on account of costs is later dishonoured. Before the bank advises of the dishonour, the firm has paid a £100 court fee from the client account for that client. How should the breach be corrected?

Answer:

Reverse the original receipt: Debit (DR) £500 client ledger (client side); Credit (CR) £500 cash account (client side). The ledger will show a deficit of £100 due to the payment made. Correct the breach immediately by transferring £100 business money into the client account: Debit (DR) £100 cash account (business side); Credit (CR) £100 client ledger (client side).

Property deposits and mortgage advances

Stakeholder deposits should be recorded so they are clearly identified as jointly held (for example, in a stakeholder ledger in both parties’ names). On completion, the deposit is transferred (inter-client transfer) to the seller’s client ledger. Where a deposit is held as agent for the seller, it belongs to the seller from exchange and is recorded directly on the seller’s client ledger.

Mortgage advances belong to the lender until completion. Firms may record receipt of the advance either on a separate lender’s client ledger (then transfer to the buyer on completion) or in the buyer’s ledger with a clear note in the details column naming the lender and identifying the sum as “mortgage advance.”

Worked Example 1.12

A lender’s £100,000 mortgage advance is received before completion. The firm records on a separate lender ledger and, at completion, transfers to the buyer. What are the entries?

Answer:

Receipt: Debit (DR) £100,000 cash account (client side); Credit (CR) £100,000 lender’s client ledger (client side). Inter-client transfer on completion: Debit (DR) £100,000 lender’s client ledger (client side); Credit (CR) £100,000 buyer’s client ledger (client side). Completion payment to seller solicitors: Debit (DR) £100,000 buyer’s client ledger (client side); Credit (CR) £100,000 cash account (client side).

Accounting for interest

Firms must pay clients a fair sum of interest on client money held unless different arrangements are agreed in writing with informed consent. Interest arising on designated deposit client accounts belongs to the client and should be credited directly to their deposit ledger and deposit cash account. For general client account holdings, a fair sum in lieu of interest is treated as a business expense and then transferred from the business to client account.

Worked Example 1.13

The firm calculates £80 due to a client as a sum in lieu of interest on money held in the general client account. How are the entries recorded?

Answer:

Record the expense: Debit (DR) £80 interest payable ledger; Credit (CR) £80 client ledger (business side). Transfer the sum to client account: Debit (DR) £80 cash account (business side); Credit (CR) £80 client ledger (client side); and Debit (DR) £80 cash account (client side); Credit (CR) £80 client ledger (business side) to reflect the two sides of the cash transfer. Payment to the client: Debit (DR) £80 client ledger (client side); Credit (CR) £80 cash account (client side).Exam Warning: The SRA prohibits using the client account as a banking facility for clients or third parties. Payments into and out of the client account must relate to the delivery of regulated legal services. Do not accept funds for convenience or unrelated purposes. Any overdrawn client ledger or improper withdrawal must be remedied immediately by replacing client money.

Summary Table: Typical Accounting Entries

| Transaction | Debit (DR) Entry | Credit (CR) Entry |

|---|---|---|

| Receipt of client money | Cash account (client side) | Client ledger (client side) |

| Payment from client account | Client ledger (client side) | Cash account (client side) |

| Receipt of business money (after bill issued) | Cash account (business side) | Client ledger (business side) |

| Payment from business account | Client ledger (business side) | Cash account (business side) |

| Mixed receipt (split) | Cash account (client/business) | Client ledger (client/business) |

| Client to business transfer (after bill) | Cash account (business side) | Client ledger (business side) |

| Inter-client transfer | Client ledger (source, client side) | Client ledger (destination, client side) |

| Disbursement (agency method) | Client ledger (client side) | Cash account (client side) |

| Disbursement (principal method) | Client ledger (business side) and HMRC ledger (input VAT) | Cash account (business side) |

Key Point Checklist

This article has covered the following key knowledge points:

- Client money and business money must always be kept separate and recorded in the correct accounts.

- Double-entry bookkeeping requires every transaction to be entered as a debit and a credit in two accounts; money in/out entries differ between the client ledger and cash account.

- Receipts of client money are debited to the cash account (client side) and credited to the client ledger (client side).

- Payments from the client account are debited to the client ledger (client side) and credited to the cash account (client side); withdrawals require sufficient client funds.

- Mixed receipts must be allocated promptly to the correct account; firms should adopt clear internal policies and record transfers accurately.

- Transfers from client to business account are permitted only after a bill or written notification of costs is given and must match the specific sums billed.

- Inter-client transfers (paper transfers) adjust client ledgers without cash account movement, and must be clearly referenced between ledgers.

- VAT on disbursements: use agency method when the invoice is addressed to the client, and principal method when addressed to the firm, with correct cash and VAT ledger entries.

- Stakeholder deposits must be recorded as jointly held until completion; agent-held deposits belong to the seller from exchange and are recorded on the seller’s ledger.

- Firms must pay a fair sum in lieu of interest on client money held (or agree different arrangements in writing) and record the expense and cash transfer correctly.

- The client account must not be used as a banking facility; breaches such as dishonoured cheques must be corrected immediately by replacing client money.

Key Terms and Concepts

- client money

- business money

- double-entry bookkeeping

- client ledger

- cash account

- mixed receipt

- COFA

- fees

- disbursements

- inter-client transfer

- stakeholder

- sum in lieu of interest

- agency method

- principal method

- petty cash

- Legal Aid Agency (LAA)