Learning Outcomes

This article explains the obligation under the SRA Accounts Rules 2019 preventing solicitors from using client accounts to provide banking facilities. It clarifies the scope of Rule 3.3, the meaning of “in respect of the delivery of regulated services”, and the distinction between legitimate handling of client money within a matter and impermissible use of client account for convenience or commercial purposes. It develops the rationale behind the prohibition, identifies indicators from the SRA’s warning notice and recent disciplinary cases, outlines typical permitted and prohibited scenarios, and sets out practical steps and remedial actions. It also connects Rule 3.3 with related duties under Rules 2.4 and 2.5 (availability and prompt return of client money), Rule 5 (withdrawals), Rules 9–11 (joint accounts, client’s own account, third-party managed accounts), and anti-money laundering obligations. This understanding will assist in tackling multiple-choice questions focused on client money handling and professional conduct.

SQE1 Syllabus

For SQE1, you are required to understand the prohibition on using client accounts to provide banking facilities under Rule 3.3 of the SRA Accounts Rules 2019, with a focus on the following syllabus points:

- The precise requirement of Rule 3.3 SRA Accounts Rules 2019 and the need for a proper connection between movements on client account and delivery of regulated legal services.

- The meaning of “banking facilities” in professional context, including escrow-only arrangements and routine bill payment services for convenience.

- How Rule 3.3 interacts with related provisions: Rules 2.4 (client money available on demand), 2.5 (prompt return), Rule 5 (withdrawals), Rule 4.2 (mixed receipts), and Rules 9–11 (joint accounts, client’s own account, TPMAs).

- Recognition of typical red flags noted in the SRA warning notice (eg unrelated third-party funds, payments to family members, use in insolvency contexts, and “execution-only” escrow).

- The rationale for the prohibition: integrity, public trust, anti-money laundering risk, and insolvency law concerns, including the risk of preferential payments and potential consequences under the Insolvency Act 1986.

- Practical compliance controls: questioning instructions, documenting the legal transaction, using TPMAs where appropriate, client due diligence, returning residual balances, and COFA oversight.

- Consequences of breach: disciplinary sanctions, reporting duties, remediation steps, and potential criminal/civil exposure.

- Distinguishing permitted uses (eg stakeholder deposit in conveyancing, holding completion monies, paying disbursements within a live matter) from prohibited uses (eg ongoing bill payment services post-completion, escrow-only retainers unrelated to legal work).

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

According to Rule 3.3 SRA Accounts Rules 2019, payments into and withdrawals from a client account must be in respect of what?

- a) Any instruction from the client.

- b) The delivery of regulated services.

- c) Any related commercial transaction.

- d) Payments approved by the firm's COFA.

-

Which of the following scenarios is LEAST likely to constitute providing banking facilities through a client account?

- a) Holding proceeds of sale for a client indefinitely after completion while they decide how to invest it.

- b) Paying a client's routine household bills from money held in the client account.

- c) Receiving funds from a third party unconnected to any legal service the firm is providing, and then paying them out as directed.

- d) Holding a deposit as stakeholder between exchange and completion in a conveyancing transaction.

-

A solicitor receives a large sum from a client with instructions to hold it and make various payments to the client's family members over the next year. The payments are unrelated to any legal services the firm is providing. What is the solicitor's primary obligation?

- a) Follow the client's instructions as part of client care.

- b) Refuse the instructions as it breaches Rule 3.3.

- c) Seek SRA authorisation before making the payments.

- d) Transfer the money to the firm's business account first.

Introduction

The SRA Accounts Rules 2019 ('the Rules') govern how solicitors and firms regulated by the Solicitors Regulation Authority (SRA) must handle money belonging to clients and others. A fundamental requirement is the proper use of the client account. This article focuses on the specific obligation found in Rule 3.3, which prohibits the use of a client account to provide banking facilities, exploring its scope, rationale, and practical application for SQE1 candidates. It also addresses the SRA’s warning notice on improper use of client accounts as banking facilities and the regulatory expectations that surround handling funds in different contexts.

Conditions for accepting client money into a client account under Rule 3.3, including regulated services, due diligence, and timely payment out.

The Purpose of Client Accounts

A client account is a specific type of bank or building society account maintained by a firm authorised by the SRA. Its primary purpose is to hold client money separate from the firm's own money (business money), as mandated by Rule 4.1.

Key Term: Client Money

Money held or received by a firm relating to regulated services, including money held on behalf of third parties (eg stakeholder money), as a trustee, or for fees and unpaid disbursements prior to billing (Rule 2.1). Key Term: Business Money

Money belonging to the authorised body (the firm). Key Term: Client Account

A bank or building society account in England and Wales (Rule 3.1) bearing the firm’s name and the word “client” (Rule 3.2), used solely to hold client money in connection with regulated legal services.

This separation is essential for safeguarding client funds, ensuring they are available when needed for the client's matter and protected in the event of the firm's insolvency. The Rules expect a proper accounting system, periodic reconciliation (at least every five weeks), and accurate client ledgers, supporting the overarching duty to keep client money safe.

The Prohibition: Rule 3.3 SRA Accounts Rules 2019

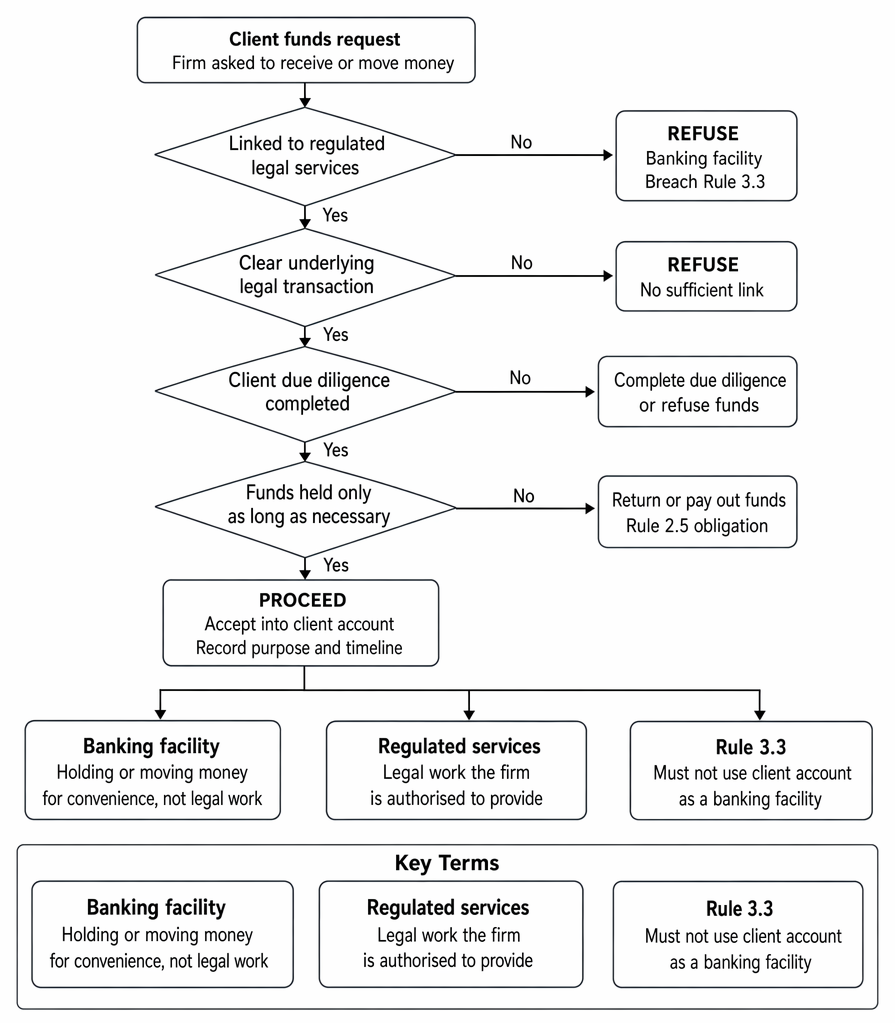

Rule 3.3 states: "You must not use a client account to provide banking facilities to clients or third parties. Payments into, and transfers or withdrawals from a client account must be in respect of the delivery by you of regulated services."

This means that the movement of money through the client account must have a direct and necessary link to the legal services the firm is providing in a specific matter. Holding or moving funds simply for the client's convenience, or for transactions unrelated to the firm's legal work, is prohibited.

Key Term: Banking Facilities

In the context of Rule 3.3, this refers to services typically offered by banks, such as holding deposits indefinitely, making payments unrelated to legal services, or enabling transactions that should occur through the client's own bank account, including “escrow-only” arrangements where the firm merely receives and releases funds without advising on a relevant legal transaction. Key Term: Regulated Services

Legal and other professional services provided by a firm that are regulated by the SRA. The movement of funds must be connected to the delivery of these services. A mere retainer or general relationship with a client is not enough; there must be a proper nexus between the payment and the particular legal work.

The SRA warning notice emphasises that it is objectionable in itself for a solicitor to act as a banker and that movements on client account must be in respect of instructions relating to a relevant transaction forming part of accepted legal services. The exemption under the Financial Services and Markets Act 2000 (FSMA) that solicitors may rely on when handling client money in connection with legal work is likely to be lost if deposits are accepted in circumstances that do not form part of regulated services. Rule 3.3 operates independently of the anti‑money laundering regime: a breach can be established without any evidence of actual laundering.

Leading Cases

The SRA's warning notice was originally prompted by a series of High Court decisions concerning misuse of the client account as a banking facility, which remain the principal illustrations of how the courts approach the prohibition now captured in Rule 3.3.

- Fuglers LLP and others v Solicitors Regulation Authority [2014] EWHC 179 (Admin) — the High Court upheld findings of misconduct where a firm had allowed its client account to be used to receive and disburse substantial sums for a commercial client unconnected to any underlying legal transaction the firm was carrying out. The court emphasised two core concerns: (i) using a client account as a banking facility trades on the solicitor's regulated status without corresponding banking‑sector oversight, and (ii) it carries an obvious and unacceptable risk that the account may be exploited for money laundering, even where laundering is not in fact proved.

- Premji Naram Patel v Solicitors Regulation Authority [2012] EWHC 3373 (Admin) — the High Court confirmed that facilitating movements of money through client account without a genuine underlying legal matter is a serious regulatory breach attracting significant sanction, reinforcing that convenience for the client is never a justification.

These authorities underpin the SRA's position that breaches of Rule 3.3 are material in themselves, regardless of whether the funds are ultimately traced to unlawful activity.

Key Term: Escrow-only retention

An arrangement where a firm is instructed only to receive and release funds according to conditions, without advising on a relevant legal transaction. This is generally impermissible under Rule 3.3.

Rationale Behind the Prohibition

The prohibition in Rule 3.3 is supported by several key regulatory and ethical considerations:

Maintaining Trust and Integrity

Solicitors are not banks and are not regulated as such. Using the client account for banking-type transactions trades on the trust and reputation associated with the legal profession without the corresponding regulatory oversight applied to financial institutions. It undermines public confidence (SRA Principle 2) and the integrity of the profession (SRA Principle 5). Courts have repeatedly confirmed that providing banking facilities through a client account falls outside proper legal practice.

Preventing Money Laundering and Financial Crime

Client accounts can be attractive to money launderers seeking to legitimise illicit funds by passing them through a regulated entity. Restricting client account use to transactions linked directly to legal services helps mitigate this risk and supports compliance with anti-money laundering legislation (including the Proceeds of Crime Act 2002 and Money Laundering Regulations). The SRA warning notice stresses that limited retainers and execution-only escrow arrangements often reveal red flags; firms must understand the transaction and conduct appropriate checks before accepting funds.

Avoiding Insolvency Complications

Allowing a client account to be used as a general banking facility, particularly in insolvency scenarios (eg where a client’s bank has withdrawn facilities after a winding-up petition), may enable preferential payments to certain creditors or shelter assets. There is a risk that transactions could be unwound under insolvency legislation, and solicitors could face personal liability if they facilitate payments during periods when the client is insolvent or at risk of insolvency. Rule 3.3 aims to prevent misuse of client account in these contexts.

Key Term: COFA

The Compliance Officer for Finance and Administration is responsible for overseeing compliance with the Accounts Rules, including monitoring and reporting material breaches, ensuring proper systems and controls, and supervising withdrawals from client account.

Identifying Improper Use

Determining whether a transaction breaches Rule 3.3 requires careful consideration of the connection between the movement of funds and the regulated service being provided. The SRA expects firms to question why they are being asked to receive or pay money and assess whether the client could make or receive payments directly.

Absence of a Relevant Legal Transaction or Connection

Receiving funds into, or making payments from, the client account where there is no relevant legal transaction upon which the firm is instructed, or where the movement of funds is not intrinsically linked to that transaction, is likely a breach. A retainer alone is not sufficient to justify using the client account; there must be a genuine legal matter to which each movement of money relates.

Examples of Red Flags

- Requests to hold large sums without a clear linked matter or specific legal purpose.

- Instructions to pay routine household bills, salaries, or travel expenses over time.

- Payments to unrelated third parties (including family members or companies) where the firm is not advising on a transaction that requires those payments.

- Using client account to bypass banking restrictions when the client is insolvent or facing a winding-up petition.

- Acting merely as “escrow agent” for funds in investment schemes or other commercial deals without advice on the relevant legal transaction.

Legitimate Contexts

- Holding stakeholder deposits between exchange and completion and transferring them to the seller on completion in accordance with the contract.

- Holding completion monies and paying disbursements in a live conveyancing transaction where the firm is acting on the legal work.

- Payment of disbursements related to a matter (eg court fees, Land Registry fees), within Rule 5.1.

- Inter-client transfers where funds are properly reallocated within the general client account to reflect a change in who the money is held for (with no cash movement), for example, from executors to a beneficiary once the estate is finalised.

Holding Funds Post-Completion

Retaining client money in the client account after a matter has substantially concluded, without a proper reason related to ongoing regulated services, risks breaching both Rule 3.3 and Rule 2.5 (requiring prompt return of client money). Holding funds merely for the client’s convenience or future unspecified use is improper.

Worked Example 1.1

A solicitor acts for a client in the sale of their house. Completion occurs, and the net proceeds (£250,000) are received into the client account. The client asks the solicitor to hold the funds for six months while they travel and decide what to do with the money. During this time, the client asks the solicitor to pay their monthly gym membership fee from the funds held.

Should the solicitor comply with these instructions?

Answer:

The solicitor should not comply. Holding the funds indefinitely after completion without a specific purpose related to ongoing legal services breaches Rule 2.5 and risks breaching Rule 3.3. Paying the gym membership fee is clearly providing a banking facility, as it is unrelated to the legal services provided (the conveyancing transaction), and is a breach of Rule 3.3. The solicitor should return the net proceeds to the client promptly.

Worked Example 1.2

A firm is asked to act as escrow-only agent for a currency investment scheme. The client instructs the firm to receive £500,000, hold it until certain non-legal conditions are met, and then release the funds. The firm is not instructed on any relevant legal transaction and provides no legal advice.

Is this acceptable?

Answer:

No. Acting purely as an escrow-only agent without advising on a relevant legal transaction breaches Rule 3.3. The firm would be providing banking facilities through client account and risking involvement in financial crime. Refuse the instruction and, if appropriate, consider reporting obligations.

Worked Example 1.3

A property developer asks the firm to hold proceeds from a completed development and, over the next year, pay various contractors, taxes, and a sales consultant in relation to a different project. The firm is not acting on that subsequent development and provides no legal services in connection with those payments.

Should the firm agree?

Answer:

No. Once the original development matter has concluded, the proceeds must be returned to the client promptly (Rule 2.5). Using client account for ongoing payments on unrelated projects where the firm is not instructed on the legal work constitutes providing banking facilities in breach of Rule 3.3.

Worked Example 1.4

A private client living overseas asks the firm to hold funds in client account to pay UK household utilities and personal outgoings for administrative convenience. The firm also provides tax advice and acts on a small probate matter.

Can the firm hold and use client account for ongoing utilities?

Answer:

No. Routine bill payment services are not connected to delivering regulated legal services and are prohibited as providing banking facilities. The firm may account to the client for any sums due for legal advice or disbursements within the probate matter, but should not run a general payments service from client account.

Worked Example 1.5

A company’s bank withdraws facilities following a winding-up petition. The company asks its solicitors to use client account to receive and make payments to creditors while the petition is pending. The firm is not instructed on insolvency proceedings.

Should the firm accept?

Answer:

No. Using client account as a banking facility to substitute for withdrawn commercial banking services is prohibited. It risks preferential payments and potential unwinding under insolvency law. Decline the instruction and advise the client to seek appropriate insolvency advice.

Worked Example 1.6

A client sends £200,000 asking the firm to “hold it for philanthropic distributions” and to make ad hoc donations over the next year. The firm is not acting on any charity setup or legal transaction requiring such payments.

Is it permissible to comply?

Answer:

No. There is no linked regulated service and the firm would be providing banking facilities. The funds should be returned and the client advised to conduct donations from their own bank account or through an appropriate charitable structure on which the firm may advise. Key Term: Stakeholder Deposit

Money held jointly for buyer and seller between exchange and completion; it is client money held for both parties until completion and may be transferred to the seller on completion. Key Term: Third-Party Managed Account (TPMA)

An account operated by a regulated third-party provider (eg FCA-regulated) that can hold funds for clients where a firm chooses not to operate a client account. Using a TPMA can be a practical alternative when funds need to be administered without forming part of regulated legal services.Exam Warning: Be alert to scenarios where a client asks a solicitor to handle payments that could easily be made through the client’s own bank account. Convenience for the client is not a valid reason to use the client account. Also, watch for funds being held after a matter concludes without justification linked to the legal service. If there is no relevant legal transaction, or no proper nexus between the payment and the legal services being delivered, Rule 3.3 is likely engaged.

Consequences of Breach

Breaching Rule 3.3 is a serious matter with significant potential consequences:

- Disciplinary action: The SRA may take action against the firm and individuals involved, potentially leading to fines, conditions on practice, suspension, or striking off.

- Breach of SRA Principles: Improper use of the client account often involves breaches of Principles, including integrity (Principle 5), maintaining public trust (Principle 2), and acting in clients’ best interests (Principle 4).

- Enabling crime: A firm that misuses the client account may be implicated in money laundering or other financial crime, leading to reporting obligations and potential criminal liability. Firms must understand the transaction, conduct client due diligence, and make reports where appropriate.

- Insolvency risks: Enabling payments for insolvent clients may involve preferential payments or void dispositions; funds movements could be challenged and unwound. Solicitors risk personal liability where they knowingly facilitate improper payments.

- Civil liability: If a client or third party suffers loss due to misuse of client account, the firm may face civil claims. Insurance may respond, but firms are expected to replace missing or misapplied client money immediately.

- Remediation and reporting: COFAs should record breaches, prompt rectification must occur, and material breaches must be reported to the SRA. Where misuse is detected, replace funds from business account without delay and cease improper activity.

Practical Steps for Compliance

To ensure compliance with Rule 3.3, firms and solicitors should:

- Scrutinise instructions: Question why funds should be received or paid via client account. Confirm there is a specific legal matter and that each movement is directly connected to the delivery of regulated services in that matter.

- Understand the transaction: Do not accept funds unless you understand the relevant legal transaction. If the matter is unclear or inconsistent with usual legal services, refuse the instruction.

- Use the right vehicle: Where funds administration is needed but does not form part of legal work, consider referring the client to a TPMA or their bank. Do not improvise bank-like services via client account.

- Link to Rule 5: Only withdraw client money for permitted purposes: the purpose for which it is held, on client/third-party instructions within a matter, or with SRA authorisation in prescribed circumstances. Check that sufficient funds are held for the specific client before withdrawals.

- Return funds promptly: Apply Rule 2.5 rigorously. Once there is no proper reason to hold client money, return it. Avoid prolonged retention post-completion.

- Due diligence and AML: Verify client identity, source of funds (especially for large or unusual transactions), and watch for red flags. Make appropriate reports under AML legislation where suspicions arise.

- Governance and records: Keep detailed records demonstrating the link between funds movements and the legal service. Ensure regular reconciliations, COFA oversight, and training for staff. Document refusal of inappropriate requests.

- Engagement and terms: Explain at the outset that the firm will not provide banking facilities and set boundaries in terms of engagement.

- Residual balances: For small residual balances where the client cannot be traced, follow the prescribed process for withdrawal to charity (within limits) or seek SRA authorisation. Record steps taken.

- Mixed receipts: Allocate promptly to the correct accounts under Rule 4.2. Do not leave business money in client account or vice versa.

Key Term: Client’s Own Account

An account in the client’s name operated by the solicitor as signatory (eg under a power of attorney). Different record-keeping duties apply, but funds are not “client money” unless received into the firm’s account. Operating a client’s own account must be necessary for the client’s affairs and is not a route to provide general banking facilities.Revision Tip: When faced with an SQE1 scenario involving client money movement, always ask: 'Is this payment/receipt directly and necessarily linked to the specific legal service this firm is providing in this matter?' If the answer is no, or if it's merely for convenience, it's likely a breach of Rule 3.3.

Key Point Checklist

This article has covered the following key knowledge points:

- Rule 3.3 SRA Accounts Rules 2019 prohibits using a client account to provide banking facilities.

- Movements on the client account must be linked to the delivery of regulated legal services in a specific matter; a general retainer alone is insufficient.

- The rationale includes protecting client money, preventing financial crime, avoiding insolvency risks, and maintaining professional integrity and public trust.

- Using the client account for client convenience or transactions unrelated to legal services is a breach, including escrow-only arrangements and routine bill payment services.

- Holding funds unnecessarily after a matter concludes can breach the Rules (Rule 2.5 and potentially Rule 3.3).

- Legitimate uses include stakeholder deposits, completion monies, and disbursements within active matters, with strict adherence to Rule 5.

- Breaches can lead to SRA disciplinary action, AML reporting issues, insolvency law complications, and potential civil liability.

- Compliance requires questioning instructions, understanding transactions, proper withdrawals, prompt return of funds, robust records, and COFA oversight.

- Where funds need to be administered outside legal work, consider a TPMA rather than client account usage.

- Red flags include unrelated third-party payments, large sums without clear purpose, insolvency contexts, and attempts to bypass commercial banking restrictions.

Key Terms and Concepts

- Client Money

- Business Money

- Client Account

- Banking Facilities

- Regulated Services

- Escrow-only retention

- Stakeholder Deposit

- Third-Party Managed Account (TPMA)

- COFA

- Client’s Own Account