Learning Outcomes

This article explains the application of double-entry bookkeeping to solicitors' accounts, including:

- the core principles of debits and credits and how they ensure that client and business ledgers always balance

- the distinction between client money and business money under the SRA Accounts Rules and the need for separate bank accounts

- the structure and purpose of the cash sheet, client ledgers, profit costs, VAT and other key ledgers used in legal practice

- how to record simple and mixed receipts, payments, transfers between client and business accounts, and corrections of errors

- the correct journal entries for common transactions such as bills, disbursements (agency and principal methods), and interest

- the regulatory limits on when client money can be withdrawn, checks for sufficient funds, and typical breach scenarios tested in SQE1

- reconciliation, record-keeping and COFA oversight requirements that support accurate, compliant client account management

- how these accounting rules and controls are tested in SQE1 multiple-choice questions and practical scenarios involving client accounts.

SQE1 Syllabus

For SQE1, you are required to understand the basic principles of double-entry bookkeeping and how these apply to the management of client and business money within a law firm. This includes the requirements set out in the SRA Accounts Rules. A core understanding of these principles is necessary to correctly interpret scenarios involving financial transactions in legal practice, with a focus on the following syllabus points:

- the concept of double-entry bookkeeping (debits and credits)

- the distinction between client money and business money

- the requirement to keep client money separate from business money

- the basic operation of client and business accounts within ledgers

- recording simple receipts and payments accurately

- how journal entries summarise the required double entries for common transactions

- issuing and reducing bills (profit costs and VAT) and the related ledger entries

- SRA rules for withdrawals from client account and checks of sufficient funds

- the prohibition on using a client account to provide banking facilities

- interest on client money and basic reconciliation and record-keeping obligations.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which accounting principle states that every transaction must be recorded with both a debit and a credit entry?

- a) Accruals concept

- b) Prudence concept

- c) Double-entry bookkeeping

- d) Going concern concept

-

Which of the following is generally considered 'client money' under the SRA Accounts Rules?

- a) Money received from a client in payment of a bill already delivered.

- b) Money received from a client on account of costs before a bill is delivered.

- c) Money belonging solely to the law firm for its operational expenses.

- d) Interest earned on the firm's business bank account.

-

A firm receives £5,000 from a client specifically to be held for a property purchase deposit. Which is the correct initial double entry?

- a) DR Cash Sheet (Business), CR Client Ledger (Business)

- b) DR Client Ledger (Client), CR Cash Sheet (Client)

- c) DR Cash Sheet (Client), CR Client Ledger (Client)

- d) DR Cash Sheet (Business), CR Client Ledger (Client)

Introduction

Understanding how law firms manage money is fundamental to legal practice. Solicitors frequently handle funds belonging to clients and must do so with accuracy and integrity, adhering to strict regulatory requirements. This involves applying basic accounting principles, particularly double-entry bookkeeping, within the framework of the Solicitors Regulation Authority (SRA) Accounts Rules. The primary aim of these rules is to ensure client money is kept safe and handled properly.

This article introduces the core concepts of double-entry bookkeeping and its application in recording solicitors' accounts transactions, focusing on the key distinction between client money and the firm's own business money. It also clarifies how the Rules require entries to be made and supervised, how ledgers and cash sheets are structured, and how to deal correctly with common events such as billing, paying disbursements, handling mixed receipts, and paying interest. Managers and the Compliance Officer for Finance and Administration (COFA) have specific responsibilities for oversight, including regular reconciliations of client bank accounts and keeping readily accessible records of bills and ledger balances.

Test Tip: In SQE-style questions on Solicitors' account entries and double-entry bookkeeping principles, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Double-Entry Bookkeeping Explained

Double-entry bookkeeping is the standard system used worldwide for recording financial transactions. Its core principle is that every transaction has two equal and opposite effects on a business's financial position. To reflect this duality, each transaction is recorded twice in the accounts: once as a debit (DR) in one account, and once as a credit (CR) in another account.

Key Term: Double-Entry Bookkeeping

An accounting system where every transaction is recorded with equal debit and credit entries, ensuring the accounts always balance.

The terms 'debit' and 'credit' simply refer to the left-hand side (DR) and right-hand side (CR) of an account ledger, respectively. The rules determining whether an entry is a debit or credit depend on the type of account and the nature of the transaction:

- Debits (DR) record: increases in assets, increases in expenses, decreases in liabilities, decreases in equity/capital, decreases in income.

- Credits (CR) record: decreases in assets, decreases in expenses, increases in liabilities, increases in equity/capital, increases in income.

A helpful view is that ledgers are prepared from the point of view of the firm. For example, if the firm receives business money (a client pays a bill), the firm’s cash increases (DR on the business side of the cash sheet) and the client’s business balance reduces (CR on the client’s business ledger). Conversely, when the firm receives client money (e.g. on account of costs before a bill), the client account columns are used: cash increases (DR cash sheet – client side) and the client’s liability increases (CR on the client ledger – client side).

To make these rules usable in practice, law firms often summarise each required pair of ledger entries as a journal entry, stating which ledger and which side (DR/CR) is used for each part of the double entry.

Key Term: Journal Entries

A concise way of describing the double entries required for a transaction, identifying which ledger(s) are used and which side (DR/CR) each entry is posted to.

Understanding which side to use for different transaction types is critical for accurate record-keeping and for preventing breaches, especially when dealing with client money under the SRA Accounts Rules.

Business Money vs Client Money

A fundamental requirement of the SRA Accounts Rules is the strict separation of money belonging to the firm (business money) from money the firm holds or receives for clients or other third parties (client money).

Key Term: Business Money

Money belonging to the law firm itself, used for its operational costs, partner drawings, or profits. Key Term: Client Money

Money held or received by a firm relating to regulated services, including money held for clients, third parties (e.g., as stakeholder), as trustee, or for fees and unpaid disbursements before a bill is delivered.

Client money includes four main categories under Rule 2.1:

- money held for a client in relation to regulated services

- money held for a third party in relation to regulated services (such as stakeholder deposits)

- money held when acting in specified roles (e.g., trustee, attorney, Court of Protection deputy)

- money held for the firm’s fees and unpaid disbursements prior to delivery of a bill.

There are limited exceptions to using a client account. If a firm only receives money for its fees and unpaid disbursements (for which the firm is liable) and it does not otherwise operate a client account, it may, with appropriate advance written information to the client, hold such money outside a client account (Rule 2.2). Additionally, payments from the Legal Aid Agency may follow special handling arrangements in practice.

This separation ensures client funds are protected and are not used for the firm's own purposes. To achieve this, firms must maintain separate bank accounts: a business bank account for business money and a client bank account for client money.

Key Term: Business Bank Account

A bank account held by the firm for its own money. Key Term: Client Bank Account

A bank account held by the firm solely for holding client money, named to include the firm's name and the word 'client'. It must be held at a bank or building society in England or Wales and must not be used to provide banking facilities to clients or third parties (Rule 3.3).

Client money should be available on demand unless an alternative arrangement is agreed in writing with the client or third party (Rule 2.4). It must also be returned promptly when there is no longer a proper reason to hold it (Rule 2.5).

Ledger Accounts in Practice

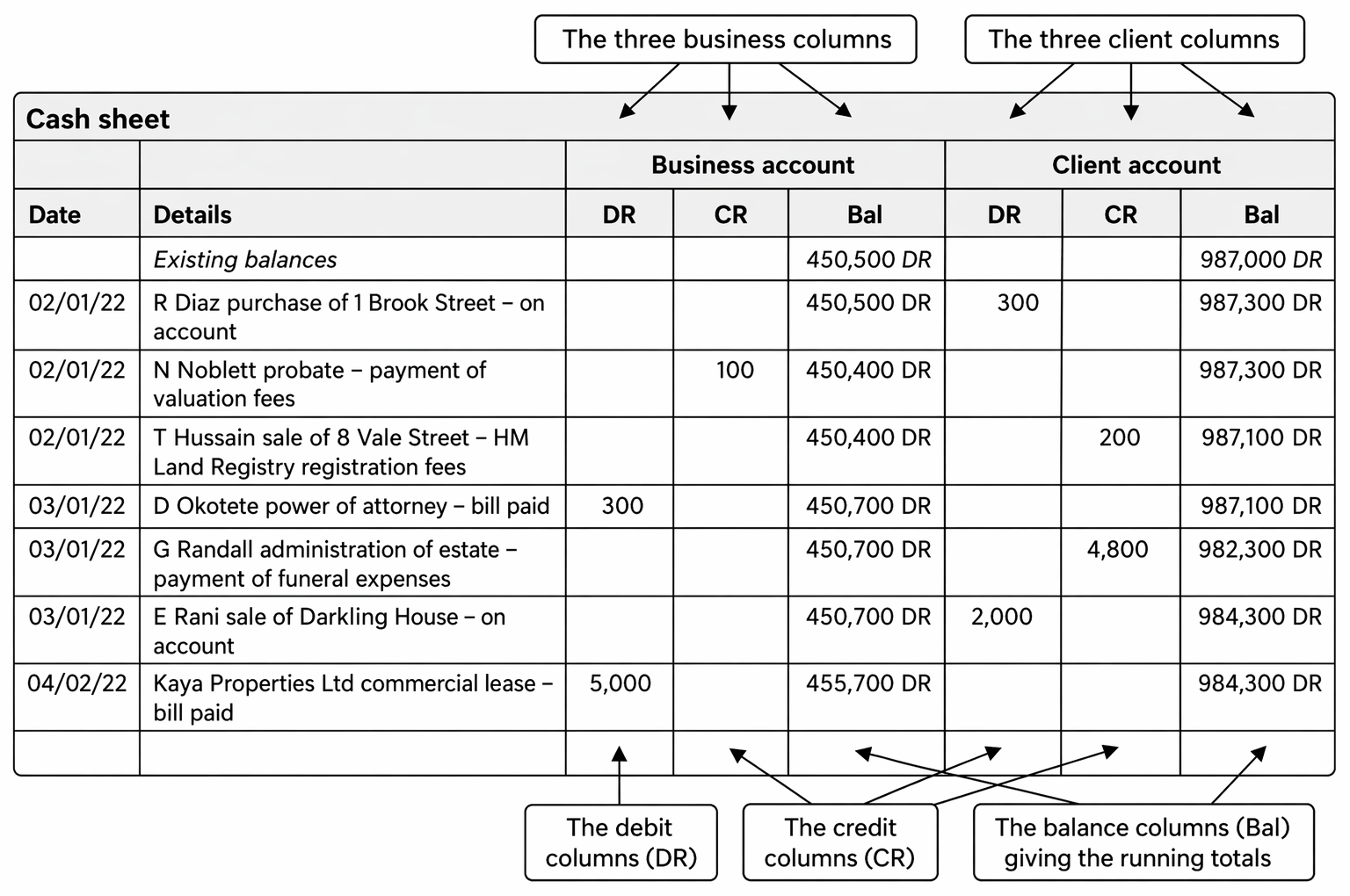

To track transactions accurately, firms use ledger accounts. For solicitors' accounts, a dual system is common, particularly for the Cash Account (often called the Cash Sheet or Cash Book) and individual Client Ledger Accounts. These ledgers have separate columns to record transactions affecting the business account and the client account.

Solicitors' accounts comprise a dual-ledger framework of an office cash register, matter-specific client ledgers, and compliance monitoring requirements.

- Cash Sheet: Records all money received into and paid out of the firm's bank accounts. The business columns track movements in the business bank account, and the client columns track movements in the client bank account.

Key Term: Cash Sheet

The ledger recording receipts and payments for both business and client bank accounts, typically presented with parallel business and client columns.

- Client Ledger: A separate ledger is maintained for each client matter. It also has dual columns (business and client) to track the firm's financial relationship with that specific client, showing both money owed to the firm by the client (in the business columns) and money held by the firm for the client (in the client columns).

Other ledgers, such as Profit Costs (recording income earned from fees) or specific tax ledgers, typically only require business columns as they relate solely to the firm's own finances.

Key Term: Profit Costs

The firm’s professional charges for legal services. A profit costs ledger records amounts billed to clients for those services. Key Term: HMRC-VAT Ledger

The ledger used to record VAT output tax charged to clients and input tax paid by the firm, supporting periodic VAT returns. Key Term: Petty Cash

A small, controlled amount of cash kept in the office for minor business expenses. Petty cash is always business money; client money must never be kept as petty cash.

Robust systems and controls are required by the Rules. Firms must:

- obtain statements for all client accounts at least every five weeks, reconcile the client account statement balance to the cash book and client ledger totals, and promptly investigate differences

- keep a central record of all bills or written notifications of costs and make it readily accessible

- retain accounting records securely for at least six years.

These activities must be signed off by the COFA or a manager.

Key Term: Compliance Officer for Finance and Administration (COFA)

The individual responsible for ensuring the firm’s compliance with the SRA Accounts Rules, including oversight of client account reconciliations and remedial action for any breaches.

In the context of client money held for extended periods or in substantial sums for a specific matter, firms may use an account designated for that client.

Key Term: Separate Designated Deposit Client Account (SDDCA)

A deposit account designated to a particular client/matter for holding client money (often to earn interest). Transfers into and out of the SDDCA must be recorded in the ledgers and cash sheet, and any interest arising belongs to the client.

Recording Basic Transactions

Applying double-entry principles to solicitors' accounts requires identifying whether a transaction involves business or client money and making the correct DR and CR entries in the appropriate ledgers and columns. Many questions in practice (and in assessments) use journal entries to summarise the required double entries.

Receipts of Money

-

Receipt of Client Money: When money is received from or on behalf of a client to be held by the firm (e.g., money on account of costs, purchase deposit), it must be paid promptly into the client bank account.

- The double entry is: DR Cash Sheet (Client columns) / CR Client Ledger (Client columns).

- This reflects an increase in the asset (cash in the client bank account) and an increase in the liability (money owed to the client).

-

Receipt of Business Money: When money is received that belongs to the firm (e.g., payment of a delivered bill), it must be paid into the business bank account.

- The double entry is: DR Cash Sheet (Business columns) / CR Client Ledger (Business columns).

- This reflects an increase in the asset (cash in the business bank account) and a decrease in another asset (the debt owed by the client).

-

Mixed Receipts: A single receipt may contain both client money (e.g., on account of future costs/disbursements) and business money (e.g., payment of a billed amount). The firm must allocate the mixed receipt promptly to the correct accounts. In practice, the full amount is often paid into the client account first, and the business money element is transferred to the business account shortly thereafter. Alternatively, firms may pay the full amount into the business account first and promptly transfer the client element to the client account. Direct cheque splits are less common.

Worked Example 1.1

A firm receives a cheque for £500 from a new client, Mrs Patel, generally on account of costs and future disbursements for a litigation matter.

How should this receipt be recorded?

Answer:

This is client money as no bill has been delivered. It must be paid promptly into the client bank account. The double entry is: DR Cash Sheet (Client) £500 CR Mrs Patel Client Ledger (Client) £500

Payments of Money

Money can only be withdrawn from the client account for the specific purposes permitted by the Rules (Rule 5.1):

- for the purpose for which the money is held (e.g., paying a disbursement for the client, completing a purchase, returning money to the client)

- following instructions from the client or relevant third party

- on SRA authorisation (e.g., residual balances paid to charity after reasonable steps to return the money).

Rule 5.2 requires appropriate authorisation and supervision. Rule 5.3 is critical: a firm may only withdraw client money for a specific client if sufficient funds are held for that client. Using one client’s money for another’s is a serious breach. If a mistake occurs, it must be rectified immediately (Rule 6.1), typically by transferring business money to the client account to restore the shortfall.

-

Payment from Client Account:

- The double entry is: DR Client Ledger (Client columns) / CR Cash Sheet (Client columns).

- This reflects a decrease in the liability (money owed to the client) and a decrease in the asset (cash in the client bank account).

-

Payment from Business Account:

- Where there are insufficient client funds or where the transaction involves business money (e.g., a billed disbursement paid by the firm as principal), payment comes from the business bank account.

- The double entry is: DR Client Ledger (Business columns) / CR Cash Sheet (Business columns).

- This reflects an increase in an asset (money owed by the client to the firm) and a decrease in another asset (cash in the business bank account).

Disbursements may involve VAT depending on the invoice and the nature of the supply:

- Agency method (invoice in the client’s name): pay the VAT-inclusive amount; no entry in the HMRC-VAT ledger is needed. Use client money if sufficient funds are held, or business money if not.

- Principal method (invoice in the firm’s name): the firm pays the supplier from the business account; record the net fee on the client’s business ledger and the VAT in the HMRC-VAT ledger. The firm then recharges the client the net fee plus VAT when billing. There is an exception for counsel’s fees where the firm may replace its name with the client’s name and treat the payment under the agency method.

Worked Example 1.2

The firm acting for Mrs Patel (from Example 1.1) needs to pay a court fee of £150. The firm currently holds £500 for Mrs Patel in the client account.

How should this payment be recorded?

Answer:

The firm holds sufficient funds (£500) for Mrs Patel in the client account to cover the £150 court fee. Therefore, the payment must be made from the client bank account. The double entry is: DR Mrs Patel Client Ledger (Client) £150 CR Cash Sheet (Client) £150 The client ledger balance for Mrs Patel (client columns) will now be £350 CR (£500 CR - £150 DR).

Issuing and Reducing Bills; VAT

When a bill is issued, the entries are made in business columns, with no cash movement at that point:

- Profit costs: DR Client Ledger (Business) / CR Profit Costs ledger.

- VAT: DR Client Ledger (Business) / CR HMRC-VAT ledger.

Any later abatement (bill reduction) reverses part of those entries:

- Profit costs abated: CR Client Ledger (Business) / DR Profit Costs ledger.

- VAT abated: CR Client Ledger (Business) / DR HMRC-VAT ledger.

When a client pays a bill, the receipt is business money:

- DR Cash Sheet (Business) / CR Client Ledger (Business).

Money on account held in the client account for fees/disbursements can only be transferred to the business account after a bill or written notification of costs is given, and only to the extent of the billed amount (Rule 4.3). Money for anticipated disbursements may remain in the client account until paid.

Worked Example 1.3

A firm issues a bill to Mr Green for £600 profit costs plus £120 VAT (£720 total).

What are the ledger entries to record the bill?

Answer:

Record the bill in business columns only: Profit costs: DR Mr Green Client Ledger (Business) £600 / CR Profit Costs ledger £600. VAT: DR Mr Green Client Ledger (Business) £120 / CR HMRC-VAT ledger £120. No cash entry is made at this stage.

Worked Example 1.4

A client sends £1,000 by bank transfer comprising £600 to clear a billed amount (£500 profit costs + £100 VAT) and £400 on account of future costs and disbursements.

How should this mixed receipt be allocated and recorded?

Answer:

Pay the mixed receipt into the client account promptly. Then transfer £600 to the business account for the billed amount: Step 1 (receipt): DR Cash Sheet (Client) £1,000 / CR Client Ledger (Client) £1,000. Step 2 (transfer for billed amount): DR Client Ledger (Client) £600 / CR Cash Sheet (Client) £600; and DR Cash Sheet (Business) £600 / CR Client Ledger (Business) £600. The remaining £400 stays in the client account (client columns) as money on account.

Worked Example 1.5

A firm receives an invoice addressed to the firm for a surveyor’s fee of £200 + £40 VAT. There are insufficient client funds at present.

What entries are needed using the principal method?

Answer:

Pay from the business bank account and record both the net fee and VAT: Payment to supplier: DR Cash Sheet (Business) £240 / entries analysed as DR HMRC-VAT ledger £40 and DR Mr Lee Client Ledger (Business) £200. When billing Mr Lee, the surveyor’s fee and VAT will be included with profit costs; record DR Client Ledger (Business) for the fee and VAT, with CR entries to the Profit Costs ledger (for profit costs) and HMRC-VAT ledger (for VAT charged).

Worked Example 1.6

A firm holds significant client money in the general client account for Ms Khan for several weeks. The firm’s interest policy indicates a fair sum in lieu of interest of £25 should be paid to Ms Khan.

What entries are needed?

Answer:

Interest payable is a business expense. Record and transfer the sum from business to client: Step 1 (record expense): DR Interest payable ledger £25 / CR Ms Khan Client Ledger (Business) £25. Step 2 (transfer to client account): DR Cash Sheet (Business) £25 / CR Ms Khan Client Ledger (Business) £25; and DR Cash Sheet (Client) £25 / CR Ms Khan Client Ledger (Client) £25. Finally, pay £25 from the client account to Ms Khan if you are not netting it off against monies otherwise due.

Worked Example 1.7

A firm receives a 10% deposit of £20,000 on exchange of contracts, held as stakeholder for buyer and seller, with completion to follow.

How should the firm record receipt of the stakeholder deposit?

Answer:

As stakeholder money, it is held jointly for both parties until completion. Record a client money receipt: DR Cash Sheet (Client) £20,000 / CR Stakeholder ledger (Client) £20,000. On completion, transfer to the seller’s client ledger: DR Stakeholder ledger (Client) £20,000 / CR Seller’s Client Ledger (Client) £20,000; and then pay to the seller from the client account.Exam Warning: A common error is making payments from the client account when insufficient funds are held for that specific client. This results in using other clients' money and is a serious breach of the SRA Accounts Rules. Always check the individual client ledger balance before authorising a payment from the client account. If funds are insufficient, the payment must be made from the business account and recorded in the business columns. If a client’s cheque bounces after a payment has already been made from the client account, you must immediately replace the shortfall with business money to restore the client account. The client account must never be overdrawn, and the client account balance on the cash sheet should not show a credit (CR) balance; a CR balance in client account columns indicates a breach. Firms must not use the client account to provide banking facilities unrelated to the provision of regulated legal services (Rule 3.3). Where client money is held, return it promptly at the end of the matter unless a proper reason exists to retain it.

Key Point Checklist

This article has covered the following key knowledge points:

- Double-entry bookkeeping requires every transaction to have equal debit (DR) and credit (CR) entries.

- Solicitors must strictly separate client money from the firm's business money, using separate bank accounts.

- Client money is money held for clients or third parties relating to regulated services, or for unbilled fees/disbursements.

- Business money belongs to the firm.

- Firms use dual-column ledgers (Cash Sheet, Client Ledgers) to track business and client transactions separately.

- Receipt of client money: DR Cash Sheet (Client), CR Client Ledger (Client).

- Receipt of business money: DR Cash Sheet (Business), CR Client Ledger (Business).

- Payment from client account: DR Client Ledger (Client), CR Cash Sheet (Client) – requires sufficient funds for that client and permitted purposes under Rule 5.1.

- Payment from business account: DR Client Ledger (Business), CR Cash Sheet (Business).

- Issuing a bill: DR Client Ledger (Business) for profit costs and VAT; CR Profit Costs ledger and CR HMRC-VAT ledger.

- Abatement of a bill: reverse part of those entries (CR Client Ledger (Business); DR Profit Costs ledger and DR HMRC-VAT ledger for the abated amounts).

- Mixed receipts must be allocated promptly to the correct accounts; commonly receive into client account and transfer the business element.

- Disbursements: use the agency method when the invoice is addressed to the client; use the principal method when the invoice is addressed to the firm; note the counsel fee exception.

- Client money must be available on demand (unless agreed otherwise) and returned promptly when no longer properly held; firms must not use client accounts as banking facilities.

- Interest: pay a fair sum in lieu of interest on money held in the general client account; interest arising on SDDCAs belongs to the client.

- Controls: reconcile client accounts at least every five weeks; retain records for at least six years; keep a central record of bills; COFA oversight is required.

Key Terms and Concepts

- Double-Entry Bookkeeping

- Business Money

- Client Money

- Business Bank Account

- Client Bank Account

- Cash Sheet

- Petty Cash

- Journal Entries

- Profit Costs

- HMRC-VAT Ledger

- Compliance Officer for Finance and Administration (COFA)

- Separate Designated Deposit Client Account (SDDCA)