Learning Outcomes

This article explains the definition of 'client money' according to the SRA Accounts Rules 2019 and clarifies how that definition operates for SQE1 FLK2 purposes. It distinguishes client money from money belonging to the firm (business money) and sets out the four main categories in Rule 2.1, with emphasis on common transactional contexts such as conveyancing, litigation, probate, and Legal Aid-funded work. It addresses the treatment of third-party funds, stakeholder deposits, money held to the sender’s order, and funds received when acting as trustee, executor, deputy, or attorney. It highlights how money received on account of costs and unpaid disbursements is classified, and contrasts this with receipts for billed costs or reimbursement of disbursements already paid from the business account. It focuses on mixed payments and the obligation to allocate promptly to the correct account under Rule 4.2, and links these classifications to typical SQE1-style questions on client account management, compliance, and application of Rules 2, 4, 5, and 7.

SQE1 Syllabus

For SQE1, you are required to have a precise understanding of what constitutes client money, which underpins the application of almost all other SRA Accounts Rules and is essential for managing client accounts correctly and ensuring compliance, with a focus on the following syllabus points:

- the definition of client money as set out in Rule 2.1 of the SRA Accounts Rules 2019

- the four main categories of client money

- the distinction between client money and money belonging to the firm (business money)

- examples of money that fall into each category, particularly in common legal transactions.

- the limited exception in Rule 2.2 for firms that only receive money under Rule 2.1(d) and do not otherwise maintain a client account

- how stakeholder deposits, agency holdings, and money held to the sender’s order fall within Rule 2.1(b)

- the treatment of mixed payments and the duty to allocate promptly to the correct account (Rule 4.2).

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is generally considered client money under the SRA Accounts Rules 2019?

- a) Money received from a client specifically in payment of a bill already delivered by the firm.

- b) Money received from a client to reimburse the firm for a disbursement already paid out of the firm's own business account.

- c) Money received from a client on account of costs and disbursements not yet billed.

- d) Interest earned on the firm's general business bank account.

-

A solicitor acts as a Court of Protection deputy for Peter. The solicitor receives money belonging to Peter as part of managing his financial affairs. How should this money be classified under the SRA Accounts Rules 2019?

- a) Business money

- b) Client money under Rule 2.1(c)

- c) Office money

- d) Out-of-scope money

-

A firm receives a single payment from a client which includes £500 for costs already billed and £2,000 as funds required for a property purchase completion. Which category best describes this receipt?

- a) Entirely business money

- b) Entirely client money

- c) A mixed payment containing both business and client money

- d) Stakeholder money

Introduction

A fundamental aspect of solicitors' accounts is the correct identification and handling of money received by the firm. The Solicitors Regulation Authority (SRA) Accounts Rules 2019 ('the Rules') establish strict requirements for dealing with money belonging to clients and others, distinct from the firm's own funds. The primary purpose is to safeguard money entrusted to the firm. Central to this is understanding the definition of 'client money'. Failure to correctly identify and handle client money can lead to serious breaches of the Rules and disciplinary action. This article focuses specifically on Rule 2 of the SRA Accounts Rules 2019, which defines client money. In practice, this classification determines where the money must be paid, when it may be withdrawn, what records are kept, and how mixed receipts are allocated. Managers and the Compliance Officer for Finance and Administration (COFA) must ensure systems and controls are robust enough to maintain these distinctions consistently.

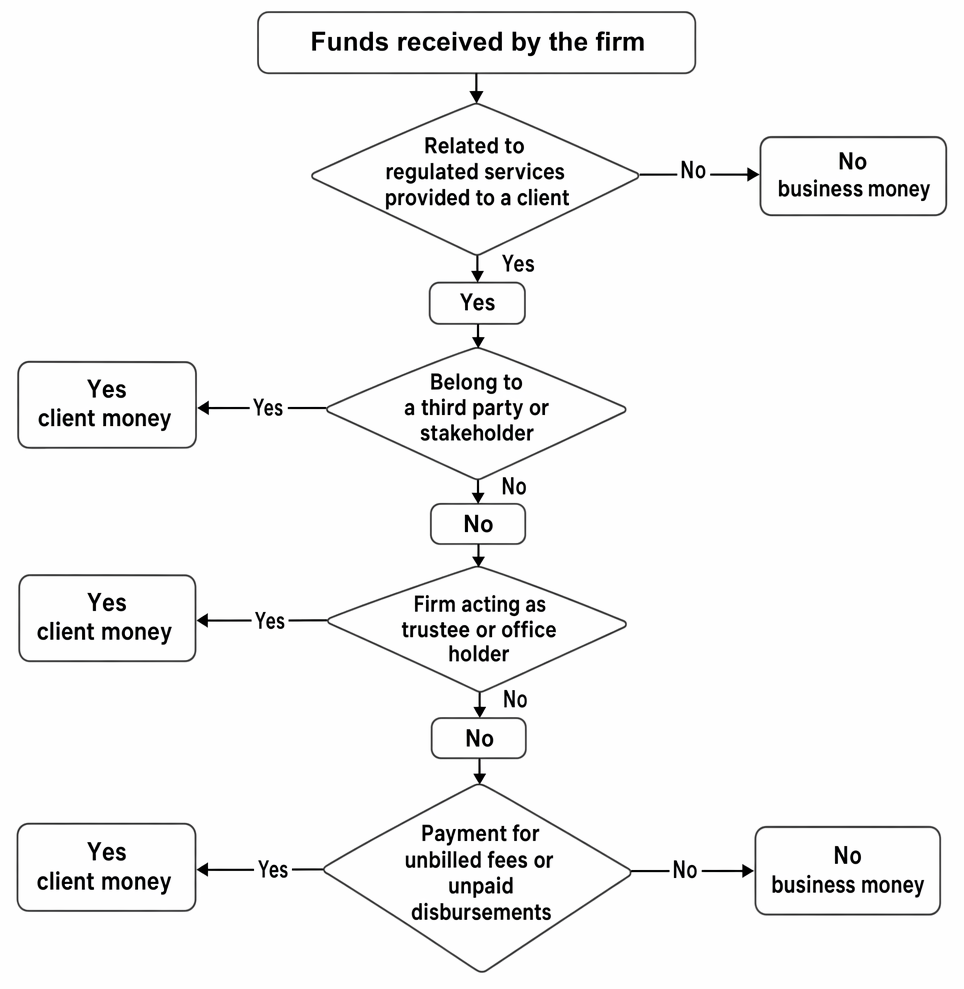

Client money under r 2.1 SRA Accounts Rules 2019 is identified by reference to regulated services, ownership, capacity, and unbilled costs.

Key Term: Client Money

Rule 2.1 defines client money as money held or received by a firm relating to regulated services delivered to a client; on behalf of a third party in relation to regulated services; as a trustee or holder of a specified office or appointment; or in respect of fees and unpaid disbursements prior to delivery of a bill. Key Term: Business Money

Money that belongs to the firm itself, as opposed to money held for clients or third parties. This includes money received in payment of delivered bills or reimbursement for disbursements already paid by the firm.

Rule 2.1 provides four main categories under which money held or received by a firm constitutes client money:

Test Tip: In SQE-style questions on Definition of client money, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

1. Money Relating to Regulated Services (Rule 2.1(a))

This is the most common category. It covers money held or received for a client in the context of the legal services being provided. The source of funds is not limited to the client; it may be paid by third parties (e.g., buyers, insurers, or lenders) provided the receipt is connected to the regulated services.

Key Term: Regulated Services

Legal and other professional services provided by a firm that are regulated by the SRA. This includes acting as a trustee or holder of a specified office.

Examples include:

- sale proceeds in conveyancing

- purchase monies (including mortgage advances held for completion)

- litigation damages received for onward payment to the client

- settlement sums in employment disputes, personal injury, or commercial litigation

- estate assets collected during probate for administration and onward distribution.

Note an important boundary: funds only become “held or received” by the firm if the firm has control over them. A cheque addressed to the client (or a third party) that is merely forwarded is not client money, because it has not been “held or received” by the firm. By contrast, settlement funds received into the firm’s account for distribution are client money.

Worked Example 1.1

A firm acts for Sarah in the purchase of a house. Sarah transfers £250,000 to the firm, which represents the purchase price to be paid to the seller on completion. Is this client money?

Answer:

Yes. The £250,000 relates directly to the regulated service (conveyancing) being delivered by the firm to the client (Sarah). It falls under Rule 2.1(a).

Worked Example 1.2

An insurer pays £30,000 to the firm following a settlement in a personal injury claim. The firm must deduct its fees later, but at receipt the sum is held for the client pending final account and payment. Is this client money?

Answer:

Yes. This is money held in connection with regulated services and is therefore client money under Rule 2.1(a). The subsequent transfer of the firm’s costs will be handled in accordance with Rules 4 and 5 after a bill or written notification of costs.

2. Money Held for Third Parties (Rule 2.1(b))

This category covers money held or received by the firm on behalf of someone other than the client, but in relation to the regulated services being provided. Common examples include:

- Stakeholder Money: Such as a deposit held in a property transaction on behalf of both buyer and seller until completion.

- Agent Money: Money held as agent solely on behalf of a third party.

- Money Held to Sender's Order: Funds received from a third party with instructions to hold them until the sender consents to their release.

Key Term: Stakeholder Deposit

A buyer’s deposit held jointly for buyer and seller (as stakeholder) pending completion. Until completion, the deposit does not belong exclusively to either party. Key Term: Sender’s Order

Money sent to the firm to be held on the sender’s terms pending consent to release, return, or specified use. The firm holds the money for the third party’s order, not for the client.

Stakeholder deposits frequently arise on exchange of contracts in conveyancing. While often recorded within the seller’s transaction ledger for practical control, the deposit must be clearly identified as stakeholder money until completion to prevent improper application for the seller’s costs or disbursements.

Worked Example 1.3

A firm acting for the seller in a property transaction receives a 10% deposit from the buyer's solicitor, to be held as stakeholder pending completion. How is this deposit money classified?

Answer:

This is client money under Rule 2.1(b). Although the firm's client is the seller, the money is held on behalf of a third party (the buyer, jointly with the seller) in relation to the conveyancing service.

Worked Example 1.4

A company sends the firm £15,000 “to the sender’s order,” instructing the firm to hold the funds until the company authorises release to a supplier when certain contractual conditions are certified. Is the £15,000 client money?

Answer:

Yes. The firm is holding money on behalf of a third party (the company) in connection with regulated legal services. This falls within Rule 2.1(b) (money held to the sender’s order).

3. Money Held as Trustee or Office Holder (Rule 2.1(c))

This applies when a solicitor or firm holds money due to a specific role they occupy, such as:

- Trustee of a trust.

- Executor or administrator of an estate (often administered through dedicated estate accounts).

- Donee of a power of attorney (for property and financial affairs).

- Court of Protection deputy.

- Trustee of an occupational pension scheme.

- Liquidator or trustee in bankruptcy.

The money belongs to the trust, estate, donor, or protected person, not the firm. Classification as client money under Rule 2.1(c) does not oblige the use of the firm’s general client account if that would conflict with role-specific requirements (Rule 2.3(a)). For example, deputies commonly operate separate deputyship bank accounts for the protected person to avoid mixing funds; firms should comply with the Office of the Public Guardian’s expectations and any applicable statutory frameworks while maintaining accurate records.

Worked Example 1.5

A solicitor is an executor of an estate. The buyer completes on the sale of the deceased’s property and sends the net sale proceeds to the solicitor to hold pending distribution to beneficiaries. Is this client money?

Answer:

Yes. The funds are held by the solicitor in a specified office (executor) capacity and are client money under Rule 2.1(c). The solicitor should keep appropriate ledger records and handle withdrawals in line with Rule 5.

4. Money for Fees and Unpaid Disbursements Pre-Bill (Rule 2.1(d))

This category covers money received from a client specifically intended to cover the firm's future fees or disbursements that the firm has not yet paid.

Key Term: Fees

The firm's own charges or profit costs (including VAT) for legal services provided. Key Term: Disbursements

Costs or expenses paid or to be paid to a third party on behalf of the client or trust (e.g., court fees, counsel's fees, search fees), excluding general office overheads like postage.

Key principles:

- Money received on account of the firm’s fees and unpaid disbursements before a bill (or written notification of costs) is delivered is client money and must be held in the client account unless the Rule 2.2 exception applies.

- Money received to reimburse a disbursement already paid by the firm from its business account is business money (not client money), because the firm is being repaid.

- Once a bill has been delivered for specific fees and disbursements, receipts expressly for payment of that bill are business money and should be paid into the business account. Money billed for anticipated disbursements that have not yet been incurred may remain in the client account until paid out, to safeguard the client’s position.

Exam Warning: Distinguishing between money received for billed versus unbilled costs, and paid versus unpaid disbursements, is a frequent source of confusion. Money for costs/disbursements is client money only if received before a bill for those specific items is delivered, or if it relates to disbursements the firm has not yet paid. Money received after a bill is delivered for those items, or to reimburse already paid disbursements, is business money.

Worked Example 1.6

A firm requests £500 from a client on account of future costs. The client pays the £500 before any bill is issued. Later, the firm issues a bill for £300 profit costs and £50 for a Land Registry search fee which the firm paid yesterday from its business account. The client then sends a further £350 specifically stating it is to pay this bill. How is the initial £500 and the subsequent £350 classified?

Answer:

- The initial £500 received before the bill was delivered is client money under Rule 2.1(d). It must be paid into the client account.

- The subsequent £350 is received after the bill was delivered and is specifically for payment of that bill. The £300 element for profit costs is business money. The £50 element is also business money because it reimburses a disbursement already paid by the firm. Therefore, the entire £350 is business money and should be paid into the business account.

Worked Example 1.7

A client pays £1,000 on account of costs and disbursements before any bill is issued. The firm then pays £400 of court fees from the client account and £200 for counsel from the business account (invoice addressed to the firm). The firm delivers a bill for £600 profit costs plus VAT and the £200 counsel fee. The client sends £720 to settle the billed profit costs and VAT. How are the receipts and balances treated?

Answer:

The initial £1,000 is client money. The £400 court fees may properly be paid from the client account (unpaid disbursement at the time of receipt). The £200 counsel fee was paid from the business account under the principal method (invoice addressed to the firm); recovery of that £200 after the bill is delivered is business money. The subsequent £720 (settlement of the billed £600 plus VAT) is also business money. Any remaining client account balance from the initial £1,000 continues to be client money until used for the purpose for which it is held or returned under Rule 2.5.

Distinguishing from Business Money

Correctly identifying client money requires distinguishing it from the firm's own business money. Business money includes:

- Money belonging solely to the firm (e.g., partner capital, bank loans, sales of office equipment).

- Money received in payment of a bill already delivered for fees and any disbursements that have been paid (or are billed under the principal method).

- Money received to reimburse the firm for disbursements already paid from the firm's business account.

- Interest earned on the firm’s general client account (the firm keeps this interest, but must account to clients for a fair sum in lieu of interest under Rule 7).

- Payments received from the Legal Aid Agency (LAA) for the firm’s costs, which may be held outside the client account under the Rules when certain conditions apply.

Key Term: Mixed Payment

A single receipt containing both business money (e.g., payment of a delivered bill) and client money (e.g., funds on account of completion or future disbursements). Mixed payments must be allocated promptly to the correct accounts (Rule 4.2).

Two related provisions help in practice:

- Rule 2.2 (limited exception) allows firms that only receive money within Rule 2.1(d) (fees and unpaid disbursements prior to billing), and that do not operate a client account for any other reason, to hold such money outside a client account if certain conditions are met (including informing the client in advance where and how the money will be held). This exception does not change the classification under Rule 2.1—it is still “client money”—but alters the obligation to hold it in a client account.

- Rule 4.2 requires mixed receipts to be allocated promptly to the correct bank account. Firms may pay mixed receipts into either account first, provided they promptly transfer the element belonging to the other account.

Edge case reminders:

- A cheque made payable to the client (or a third party) and forwarded is not client money because it is not held or received by the firm.

- Stakeholder deposits must be identified clearly to prevent inadvertent use for the seller’s costs before completion.

- Money billed for anticipated disbursements not yet incurred should remain protected in the client account until paid (to avoid exposing the client’s funds to business risks).

Worked Example 1.8

A firm receives a bank transfer of £10,000 comprising £8,500 for completion monies (client money) and £1,500 in settlement of a bill delivered last week (business money). The transfer lands in the client account. What must the firm do?

Answer:

The firm must promptly transfer the £1,500 business element from the client account to the business account and retain the £8,500 as client money for completion. This satisfies Rule 4.2 on allocation of mixed payments and preserves the separation required by Rule 4.1.

Key Point Checklist

This article has covered the following key knowledge points:

- Client money must be kept separate from the firm's business money.

- Rule 2.1 defines client money, which generally falls into four categories: money relating to regulated services, money held for third parties, money held as trustee/office holder, and money for unbilled fees/unpaid disbursements.

- Money received on account of fees and unpaid disbursements before a bill is delivered is client money; reimbursement for disbursements already paid is business money.

- Once a bill is delivered for specific costs, money received expressly to pay that bill is business money.

- Stakeholder deposits and money held to the sender’s order are client money under Rule 2.1(b).

- Money held by a solicitor acting as trustee, executor, attorney, or deputy is client money under Rule 2.1(c), noting Rule 2.3(a) may require different banking arrangements for that office/appointment.

- Mixed payments must be allocated promptly to the correct account (Rule 4.2).

- A cheque addressed to the client that is forwarded is not “held or received” by the firm and is not client money.

- Rule 2.2 provides a limited exception for firms that only receive money under Rule 2.1(d) and do not otherwise operate a client account, provided clients are informed in advance where and how money will be held.

- Distinguishing between client money and business money is essential for compliance with the SRA Accounts Rules.

Key Terms and Concepts

- Client Money

- Business Money

- Regulated Services

- Fees

- Disbursements

- Stakeholder Deposit

- Sender’s Order

- Mixed Payment