Learning Outcomes

This article explains the burden and incidence of Inheritance Tax (IHT) in the context of grants of representation and lifetime transfers, equipping you to handle SQE1-style problem questions on who is liable to HMRC and which beneficiaries ultimately bear the tax. It explains the distinction between liability and burden, how statute allocates liability between PRs, trustees, and recipients of property passing outside the estate, and how express will directions can vary the default position. It examines apportionment in wholly and partially exempt estates, including the treatment of exempt and non-exempt residue, specific legacies, survivorship property, PETs and CLTs. It details how to calculate estate rates and apply grossing-up and grossing-down to non-exempt gifts, including "free of tax" and "subject to tax" legacies. It also reviews payment deadlines, the availability and mechanics of the instalment option for qualifying assets, and the effect of business and agricultural property relief and the reduced charity rate on incidence, enabling accurate computations and confident application of the rules in timed assessments.

SQE1 Syllabus

For SQE1, you are required to understand the burden and incidence of Inheritance Tax in the context of estate administration, with a focus on the following syllabus points:

- the rules determining who is liable to pay IHT on death and on lifetime gifts

- how the burden of IHT is apportioned among beneficiaries and assets

- the statutory rules and the effect of express directions in a will regarding IHT

- the practical implications for personal representatives (PRs) and beneficiaries

- the impact of partially exempt estates and the calculation of IHT in such cases

- the timing of payment on death and lifetime transfers, and the instalment option for certain assets

- how business and agricultural property relief affect incidence and apportionment

- the reduced 36% IHT rate where 10% of the baseline passes to charity and its effect on burden

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Who is primarily liable to pay Inheritance Tax on a deceased’s estate?

- If a will is silent, which part of the estate bears the burden of IHT on a specific legacy to a non-exempt beneficiary?

- What is the effect of an express direction in a will that a legacy is “free of tax”?

- How is IHT apportioned between exempt and non-exempt shares of residue?

Introduction

Inheritance Tax (IHT) is a central consideration in the administration of estates. When a person dies, IHT may be payable on the value of their estate, and the responsibility for paying this tax falls on specific parties. Understanding who is liable, how the burden is allocated, and the statutory rules that apply is essential for effective estate administration and for answering SQE1 questions on grants of representation. It is important to distinguish liability (who must account to HMRC) from burden (who ultimately bears the economic cost). That distinction runs through death estates, property passing outside the grant, and lifetime transfers (including potentially exempt transfers (PETs) and chargeable lifetime transfers (CLTs)).

It presents allocation of IHT liability, ultimate burden, and apportionment between PRs, trustees, recipients, and beneficiaries under testamentary and statutory rules.

Key Term: personal representatives (PRs)

The executors or administrators responsible for administering the deceased’s estate and paying debts, taxes, and distributing assets. Key Term: settled property

Property held in trust, where the trustees may be liable for IHT attributable to that property. Key Term: residue

The part of the estate remaining after payment of debts, expenses, and specific gifts.

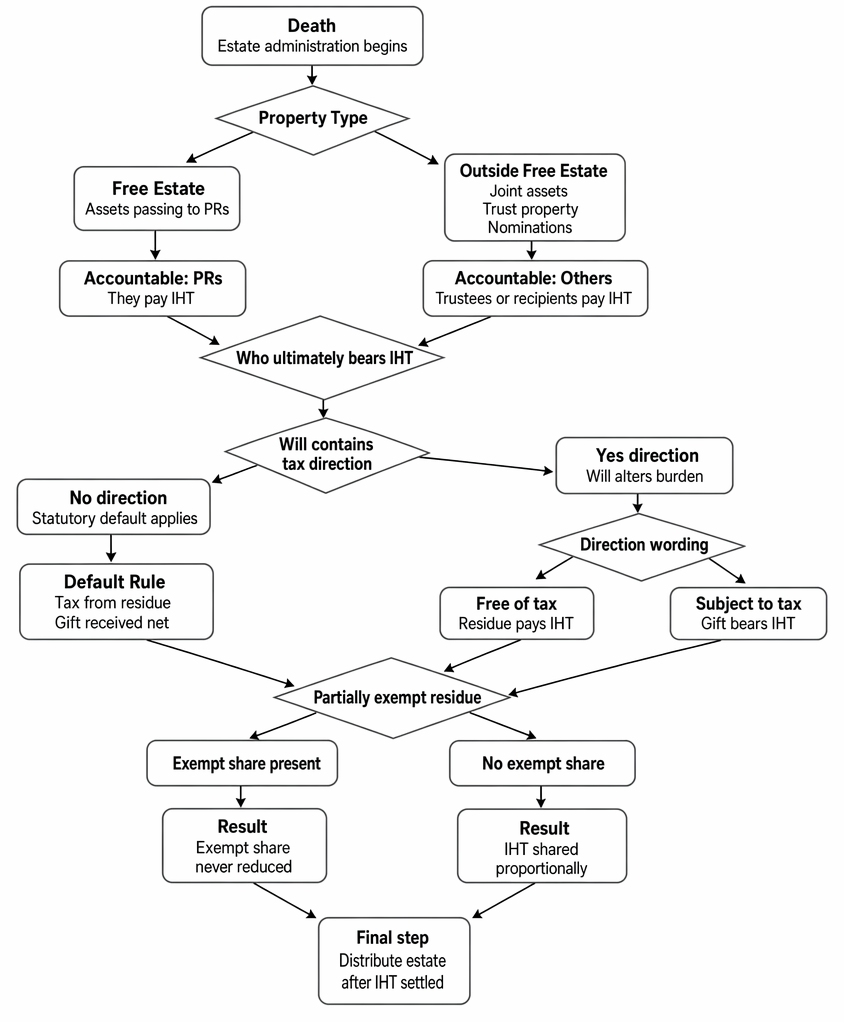

Liability for Inheritance Tax

The liability for IHT on death is set out in statute. The main categories of persons accountable for IHT are:

- PRs are primarily liable for IHT on the deceased’s free estate (assets that pass under the will or intestacy). Their liability is limited to the value of assets they receive or would have received but for their own neglect or default. PRs must ensure the tax is paid before distribution, and in practice, a grant will not issue until HMRC has confirmed receipt of tax due at the grant stage.

- Trustees are liable for IHT on settled property (e.g., trust funds aggregated to a life tenant’s death estate or subject to relevant property charges).

- Beneficiaries who receive property directly outside the free estate (e.g., joint property passing by survivorship, nominated property, or life assurance proceeds payable outside the estate) may be accountable for IHT attributable to that property if PRs do not pay and the statute shifts liability to recipients.

- Lifetime transfers:

- PETs: If the donor dies within seven years, IHT may be due; liability falls on the transferee of the PET, but HMRC has recourse to the donor’s PRs if tax on the PET remains unpaid after prescribed periods.

- CLTs: At the time of transfer, liability is on the transferor. If further tax is due on death within seven years (reassessment at death rates with taper relief if applicable), liability falls on trustees; HMRC may pursue other liable persons if trustees fail to pay.

Key Term: undisposed-of property

Property in the estate not specifically given by the will; used first to meet testamentary and administration expenses, including IHT where applicable.

Time for payment is a practical aspect of liability. On death, IHT is due six months after the end of the month of death; interest runs thereafter on unpaid amounts. PETs becoming chargeable on death and additional tax on death for earlier CLTs are also due six months after the end of the month of death. Certain assets qualify for payment by instalments (10 yearly instalments), which affects cash flow planning by PRs.

Key Term: instalment option property

Property for which IHT attributable may be paid over 10 annual instalments (e.g., land, certain business interests, and qualifying shareholdings), subject to statutory conditions. Key Term: estate rate

The effective IHT rate applied to taxable estate values after allowances and reliefs (used for apportionment and grossing calculations).

Burden of Inheritance Tax: Who Ultimately Pays?

The “burden” of IHT refers to which part of the estate (and which beneficiaries) ultimately bears the cost of the tax. This is distinct from “liability,” which concerns who must pay HMRC.

Statutory Default Rules

If a will is silent, the statutory rules apply:

- IHT on property passing to the PRs (the free estate) is treated as a testamentary and administration expense. It is paid primarily from undisposed-of property (if any), then from residue.

- IHT on property not passing to the PRs (e.g., joint property passing by survivorship, nominated property, or settled property) is borne by the recipient of that property.

Where residue is partly, or wholly, exempt (for example, a spouse/civil partner or charity), statutory apportionment ensures exempt residuary shares do not bear IHT attributable to non-exempt gifts or non-exempt shares of residue. In practice, this can require grossing-down or recovery of tax from recipients of non-exempt gifts where there is no non-exempt residuary fund to shoulder the burden.

Express Directions in the Will

A testator can alter the statutory rules by including an express direction in the will. For example, a legacy may be given “free of tax,” meaning the tax on that gift is paid from the estate rather than borne by the recipient. Conversely, a legacy “subject to tax” means the beneficiary bears the tax. Directions can also address charges (e.g., mortgage debt on a devised property) and costs associated with specific gifts.

Key Term: exempt beneficiary

A person or entity (such as a spouse, civil partner, or charity) who is not liable to IHT on gifts received from the estate.

Worked Example 1.1

A testator leaves £100,000 to his nephew and the residue to his spouse. The will is silent on tax. The nephew is not exempt from IHT.

Answer:

Because the residue is wholly exempt, statutory apportionment prevents the burden of IHT falling on the spouse’s residuary share. The IHT attributable to the nephew’s pecuniary legacy is borne by the nephew’s gift (the recipient bears the burden). In practice, PRs calculate the tax attributable to the £100,000 and recover it from the legacy (grossing-down) or require payment from the legatee; the spouse’s residuary share is not reduced.

Apportionment of IHT: Partially Exempt Estates

Where an estate is divided between exempt (e.g., spouse or charity) and non-exempt beneficiaries, the burden of IHT is apportioned according to statutory rules:

- Exempt beneficiaries (e.g., spouse, charity) do not bear any part of the IHT attributable to non-exempt gifts or non-exempt shares of residue, even if the will says otherwise. Statute disapplies contrary directions that would throw the burden onto exempt shares.

- Non-exempt beneficiaries’ shares are reduced by the IHT attributable to them.

Where residue contains property qualifying for business or agricultural relief, relief can affect the estate rate used for apportionment. For property eligible for relief but not specifically bequeathed, relief is allocated pro rata through the estate by formula, which changes the effective rate used when calculating burden across gifts and residuary shares.

Worked Example 1.2

A testator leaves half the residue to his wife and half to his son. The estate is £800,000, with a nil rate band of £325,000. There are no specific gifts.

Answer:

The wife’s share is exempt. The son’s share bears all the IHT on the taxable estate above the nil rate band. The wife’s share is not reduced by IHT. The estate rate is computed on the taxable portion, and the son’s half of residue is reduced accordingly.

Specific Gifts and Grossing-Up

If a specific legacy to a non-exempt beneficiary is directed to be “free of tax” (or the will is silent and there is a non-exempt residuary fund available to bear tax), the IHT on that gift is paid from the estate rather than by the recipient. The amount payable is “grossed up” to ensure that the beneficiary receives the stated net amount and the appropriate tax is discharged.

Key Term: grossing-up

The process of increasing a net gift to calculate the total amount (including tax) that must be paid from the estate to satisfy the legacy and the IHT due.

Grossing-up uses the estate rate: grossed-up cost of a net legacy = net amount ÷ (1 − estate rate). If residue is wholly exempt, statutory apportionment prevents using exempt residue to bear this cost; in that case, the recipient bears the burden (grossing-down rather than grossing-up).

Worked Example 1.3

A will leaves £120,000 to a friend (not exempt) and residue to a spouse. The nil rate band is exhausted. The will is silent on tax.

Answer:

Because the residue is wholly exempt, the IHT attributable to the £120,000 cannot be thrown onto the spouse’s residuary share. The burden falls on the friend’s gift. PRs compute the tax attributable using the estate rate and either reduce the legacy by the tax (grossing-down) or require the legatee to fund the tax; the spouse’s residue remains intact.

Worked Example 1.4

A property held jointly by the deceased and a sibling passes by survivorship to the sibling. The estate has taxable value above the nil rate band.

Answer:

Liability for IHT attributable to the deceased’s share passing by survivorship is on the recipient. The burden is likewise borne by the recipient of the survivorship property; the free estate (residue) does not bear this tax unless the will expressly directs otherwise and statute permits.

Worked Example 1.5

A testator leaves “£200,000 to P subject to tax” and the residue to Q (a non-exempt beneficiary). The estate rate is 40%.

Answer:

“Subject to tax” means P bears the burden of IHT on the £200,000. P’s entitlement is reduced by the tax attributable to that legacy (40% of £200,000 = £80,000), leaving P £120,000 net. Q’s residuary share is unaffected by the tax on P’s gift.

Business/Agricultural Relief and Apportionment

Where property qualifying for business property relief (BPR) or agricultural property relief (APR) is not specifically given but forms part of residue, relief is allocated pro rata through the estate using the statutory formula. This reduces the estate rate applied to non-exempt gifts and shares, affecting burden calculations. If relief is attached to a specific gift of qualifying property, the relief reduces or eliminates IHT attributable to that gift.

Charity Rate and Incidence

If at least 10% of the baseline value passes to charity, the rate of IHT on the estate (or relevant merged component) is reduced from 40% to 36%. This changes the estate rate used for apportionment and thus the burden borne by non-exempt recipients. PRs may elect to merge components to test the 10% threshold. If the reduced rate applies, the non-exempt beneficiaries bear tax at 36% on the taxable values; exempt beneficiaries still do not bear any burden.

Practical Implications for Personal Representatives

PRs must ensure that IHT is paid before distributing the estate. They may need to:

- Deduct IHT from legacies if the will directs the beneficiary to bear the tax (“subject to tax”) or where statutory apportionment requires the recipient of a non-exempt gift to bear the burden (including grossing-down where residue is exempt).

- Pay IHT from undisposed-of property and residue if the will is silent and statutory rules allow (for example, where there is a non-exempt residuary fund), including grossing-up for net “free of tax” gifts.

- Recover IHT from recipients of property passing outside the estate (e.g., survivorship, nominations, settled property) if required, and warn transferees of PETs or trustees of CLTs of potential death charges where the donor dies within seven years.

- Manage timing: IHT on death is due six months after the end of the month of death; PETs and CLTs becoming chargeable on death follow the same timing. On CLTs made in a tax year, lifetime IHT is due at set statutory dates (and additional tax on death is due six months after the month of death).

- Consider instalments: For instalment option property, attribute tax using the estate rate and arrange instalment payment over 10 years, noting that interest treatment differs between land vs business/agricultural property.

- Fund the liability before the grant: use the Direct Payment Scheme (IHT423) to transfer funds directly from the deceased’s bank/building society accounts to HMRC; where this is not possible, consider loans from beneficiaries or bank borrowing secured against estate assets and undertake to repay from first available proceeds.

- Be alert to reliefs: where BPR/APR apply, confirm whether relief attaches to specific gifts or must be allocated pro rata through residue; this can materially change apportionment and burden.

Key Term: instalment option property

Property for which IHT attributable may be paid in instalments (e.g., land, certain business interests, and qualifying shareholdings). Key Term: estate rate

The effective IHT rate applied to taxable estate values after allowances and reliefs; used for apportionment and in grossing calculations.

PRs should not distribute the estate until satisfied that all IHT has been paid, especially where there are lifetime gifts that may become chargeable on death. They should also be aware that HMRC can, in certain circumstances, seek payment from PRs if transferees/trustees fail to pay tax attributable to lifetime transfers; PRs may then have rights to recover from the persons primarily liable.

Exam Warning: In partially exempt estates, do not assume that IHT is shared equally between exempt and non-exempt beneficiaries. Statutory rules ensure that exempt beneficiaries’ shares are not reduced by IHT on non-exempt shares, regardless of the will’s wording.

Revision Tip: Always check for express directions in the will regarding the burden of IHT. If none, apply the statutory rules. Be prepared to calculate grossed-up amounts for net legacies and to gross down where residue is wholly exempt.

Key Point Checklist

This article has covered the following key knowledge points:

- PRs are primarily liable for IHT on the deceased’s free estate; trustees may be liable for settled property; recipients are accountable for property passing outside the estate.

- The burden of IHT (who ultimately pays) is determined by statutory rules unless the will provides otherwise; liability and burden are distinct.

- In the absence of an express direction, IHT on legacies to non-exempt beneficiaries cannot be thrown onto exempt residue; recipients may bear the burden (grossing-down).

- Exempt beneficiaries’ shares of residue are not reduced by IHT on non-exempt shares; statutory apportionment ensures the burden falls on non-exempt parts only.

- Grossing-up is required when a net legacy is given “free of tax” and there is a non-exempt fund to bear the burden; grossing-down applies where the residue is wholly exempt and recipients must bear tax.

- Payment timing and instalment options affect administration; IHT on death is due six months after month of death, and certain property allows payments by instalments.

- Reliefs (BPR/APR) and the reduced charity rate change the estate rate and thus the incidence and apportionment of IHT.

- PRs must ensure IHT is paid before distributing the estate and may need to recover tax from beneficiaries of property passing outside the estate; use the Direct Payment Scheme (IHT423) and other funding methods to secure payment prior to the grant.

Key Terms and Concepts

- personal representatives (PRs)

- settled property

- residue

- exempt beneficiary

- grossing-up

- undisposed-of property

- instalment option property

- estate rate