Learning Outcomes

This article outlines the valuation of estate assets and liabilities for grants of representation, including:

- Identifying the assets and liabilities that fall within the probate and IHT estate, including deemed property.

- Applying the statutory open market value test and recognising when death itself alters value under IHTA 1984.

- Distinguishing valuation approaches for land, joint property, bank accounts, quoted and unquoted shares, business interests, chattels, life policies, foreign assets, and trust interests.

- Recognising when discounts or related property rules affect fractional interests, pairs and sets, and joint holdings.

- Determining which liabilities are deductible for IHT, which are restricted or disallowed, and how secured debts interact with charged property.

- Calculating the net estate after liabilities, exemptions, and reliefs, and understanding its role in IHT and beneficiary entitlement.

- Explaining the order of payment of debts in solvent and insolvent estates and the impact on legacies, abatement, and marshalling.

- Completing and using IHT forms (IHT205, IHT400, IHT421) and appreciating their link with obtaining the grant.

- Evaluating how valuation choices and evidence affect PR protections, estate accounts, appropriations, and potential challenges by HMRC or beneficiaries.

- Practising SQE1-style multiple-choice reasoning using typical valuation and liability scenarios.

SQE1 Syllabus

For SQE1, you are required to understand the valuation of assets and liabilities when applying for a grant of representation. This includes the legal rules for determining the value of estate assets and debts, the order of payment of liabilities, and the consequences for inheritance tax and distribution to beneficiaries, with a focus on the following syllabus points:

- the legal definition and types of grants of representation (probate, administration)

- the rules for valuing assets in the estate (market value, date of death, special rules for certain assets)

- the identification and deduction of liabilities from the gross estate

- the impact of asset and liability valuation on inheritance tax calculations

- the order of payment of debts and liabilities in estate administration

- the IHT definitions of estate, deemed property, and excluded property (IHTA 1984)

- special valuation rules: joint property discounts, related property rules, quoted shares methodology, unquoted/business interests

- trust interests and gifts with reservation of benefit included in the estate

- IHT forms and processes (IHT205 excepted estates; IHT400 account; IHT421 probate summary)

- abatement of legacies, marshalling, and appropriation of assets for beneficiaries

- PR protections against unknown or missing claimants (Trustee Act 1925, s27; Benjamin orders)

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the general rule for valuing assets in a deceased’s estate for probate and inheritance tax purposes?

- Which liabilities can be deducted from the value of the estate when calculating inheritance tax?

- How are jointly owned assets treated for valuation in the estate?

- In what order must debts and liabilities be paid out of the estate?

Introduction

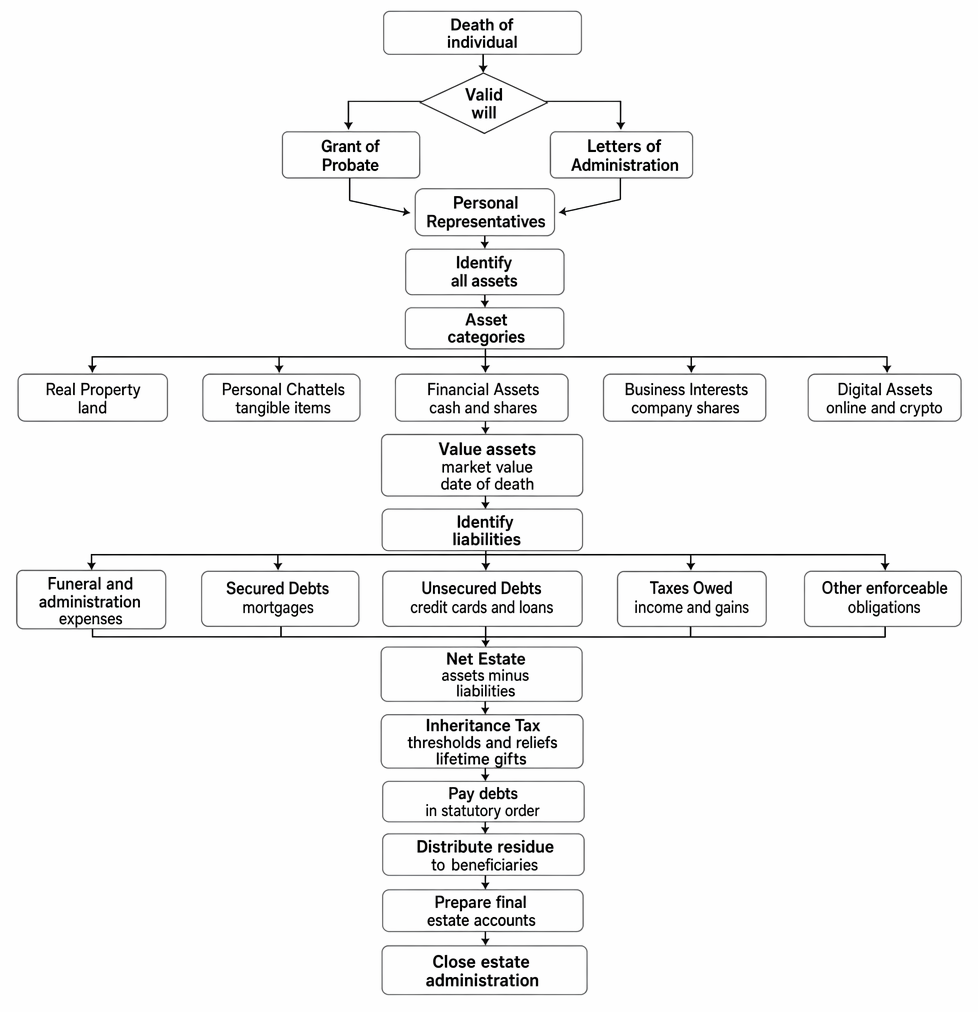

When a person dies, their estate must be administered by personal representatives (PRs) who are authorised by a grant of representation. Before assets can be collected and distributed, the PRs must value all assets and liabilities in the estate. Accurate valuation is essential for inheritance tax, payment of debts, and ensuring beneficiaries receive their correct entitlement. Because the IHT definition of “estate” includes certain deemed property (such as gifts with reservation and qualifying interests in possession of trust property) as well as assets beneficially owned immediately before death, PRs need to be clear about what is inside and outside the tax estate and how each item is valued. Valuations are as at the date of death and must be supported by evidence appropriate to the asset type.

Estate administration from death to final accounts, including grants of representation, valuation of assets and liabilities, inheritance tax, debt payment and distribution.

Key Term: grant of representation

The legal document authorising personal representatives to collect, manage, and distribute a deceased person’s estate. Key Term: probate value

The open market value of an asset at the date of death used for inheritance tax and probate purposes, determined under IHTA 1984 valuation principles.

Types of Grant of Representation

A grant of representation is the legal authority issued by the probate registry to administer a deceased person’s estate.

There are two main types:

- Grant of probate: Issued when there is a valid will and executors are appointed.

- Grant of letters of administration: Issued when there is no valid will or no executor able or willing to act.

Where there is a valid will but no proving executor (e.g., renunciation or incapacity), letters of administration with will annexed may be granted to the person entitled under the Non-Contentious Probate Rules to administer the estate in accordance with the will. In specific circumstances (e.g., administration interrupted), the court may issue a grant de bonis non to continue administration. The type of grant determines who is entitled to administer the estate but does not affect the valuation rules.

Valuation of Assets

All assets in the estate must be valued as at the date of death. The value of the estate is used to determine inheritance tax liability, the probate fee, and the amount available for distribution to beneficiaries.

Key Term: market value

The price an asset might reasonably be expected to fetch if sold on the open market at the date of death. Key Term: related property rules

IHTA 1984 rules that modify valuation where the deceased and another person (often a spouse/civil partner) hold matching assets forming a pair or set or interests that must be valued by reference to the whole, restricting certain discounts. Key Term: qualifying interest in possession

An interest in possession in settled property that is treated for IHT as if the life tenant owned the capital, so the trust fund is aggregated with the life tenant’s estate on death in specified cases (e.g., IPDIs).

General Rule

Assets are valued at their open market value at the date of death (IHTA 1984, s160). If death itself changes an asset’s value, the post-death effect is taken into account (IHTA 1984, s171). The valuation is a snapshot at death; later market movements do not alter probate value, though they may be relevant for IHT loss on sale reliefs if PRs sell certain assets at a loss within the statutory period.

Special Rules for Certain Assets

-

Real property (land and buildings): Value is based on the price a willing buyer would pay at the date of death, ignoring any forced sale or special purchaser. If the deceased co-owned land, the deceased’s undivided share may attract a discount (commonly 10–15% for residential property) to reflect the difficulty of selling a fractional interest to occupy with another owner. However, where the related property rules apply (e.g., spouses’ matching interests), valuation may be as a proportion of the whole without discount.

-

Jointly owned property and accounts: For IHT, the deceased’s beneficial share is included in the estate. In many joint bank accounts the presumption is equal shares unless evidence shows otherwise. For land, discounts for undivided shares may be available unless related property rules apply. Survivorship governs title transfer of beneficial joint tenancies, but valuation for tax is of the deceased’s share immediately before death.

-

Quoted shares: Use the Stock Exchange Daily Official List for the date of death (or nearest trading day). The standard method is “quarter-up”: take one-quarter of the difference between the lower and higher quoted prices and add it to the lower price to obtain per-share value.

-

Unquoted shares and business interests: These require specialist valuation, considering factors such as earnings, asset backing, prospects, and the degree of control (e.g., minority discounts). Personal goodwill and the impact of the proprietor’s death may reduce value.

-

Trust interests: If the deceased had a qualifying interest in possession (e.g., an immediate post-death interest under a will, or a pre-2006 qualifying IIP), the trust fund may be treated as part of the deceased’s estate for IHT purposes and must be valued.

-

Gifts with reservation of benefit: Property given away during lifetime but still enjoyed or occupied by the deceased is treated as part of the estate at death and valued accordingly.

-

Pairs and sets (related property): Items forming a set (e.g., matching vases) may be worth more together than separately; valuation rules may require proportionate valuation by reference to set value, particularly where spouses hold related items.

-

Personal chattels: Items such as jewellery, art, and vehicles are valued at their second-hand sale price (auction/private sale), not insurance or replacement value. For intestacy classification purposes “personal chattels” exclude money/securities and items held mainly for business use or investment, but for IHT valuation everything within the tax estate is valued at market value.

-

Life assurance: If the policy benefits are payable to the estate, the value at death reflects the maturity value rather than surrender value because death has changed the value (IHTA 1984, s171). If the policy is written in trust or assigned, proceeds may fall outside the estate.

-

Foreign assets: Valued in local currency and converted to sterling at the date-of-death exchange rate. Consider local saleability and any restrictions affecting market value.

Revision Tip: Probate value is determined at the date of death. The IHT account typically rounds asset values down and liabilities up to the nearest pound. Keep documentary support for every valuation, particularly for real property (estate agent/RICS report) and unquoted shares (accountant’s valuation).

Worked Example 1.1

A deceased owned a house (sole name), a joint bank account with her spouse, and a collection of paintings. How should these be valued for probate?

Answer:

The house is valued at its open market value at the date of death. The deceased’s share of the joint bank account is included (usually 50% if two account holders, unless evidence shows otherwise). The paintings are valued at their likely sale price at auction or by private sale.

Worked Example 1.2

On the date of death, DEF plc shares were quoted at 102p/106p. The deceased held 5,000 shares. What is the probate value?

Answer:

Quarter-up method: 102p + (1/4 × (106 − 102)) = 103p per share. Probate value = 5,000 × 103p = £5,150.

Worked Example 1.3

The deceased gifted a flat to his daughter six years ago but continued to live there rent-free until death. Is the flat included in the estate and at what value?

Answer:

Yes. This is a gift with reservation of benefit, so the flat is treated as part of the deceased’s estate at death and valued at its open market value at that date.

Worked Example 1.4

A testator’s will created a life interest for the surviving spouse over a trust fund, with remainder to children. The spouse has just died. Is the trust fund part of the spouse’s estate for IHT?

Answer:

If the spouse had a qualifying interest in possession (for example, an immediate post-death interest under the testator’s will), the trust capital is aggregated with the spouse’s estate at death and is valued at open market value for IHT.

Valuation of Liabilities

Liabilities reduce the value of the estate for inheritance tax and probate purposes. Only certain debts can be deducted, and there are anti-avoidance restrictions for liabilities linked to excluded property.

Key Term: deductible liability

A debt or obligation that may be subtracted from the gross value of the estate when calculating inheritance tax and the net estate. Key Term: excepted estate

An estate meeting prescribed criteria so that a full IHT account is not required; typically completed on form IHT205 with limited valuation detail where the estate is below thresholds or consists of exempt transfers and specified categories.

Deductible Liabilities

The following may generally be deducted (subject to IHTA restrictions):

- Funeral expenses (reasonable costs only)

- Debts incurred for full consideration (e.g., loans, credit cards, utility bills), including accrued interest to the date of death

- Mortgages and secured loans (deducted from the value of the charged asset unless the will provides contrary intention, e.g., “free of mortgage”)

- Unpaid taxes and rates due at death

- Professional fees incurred before death (e.g., legal/accountancy), due at death

- Overpaid pension or benefits repayable by the estate

Secured debts should, as a starting point, be discharged from the property against which they are secured unless the will directs otherwise. Where a will gifts property “free of mortgage” the burden may fall on residue.

Non-Deductible Liabilities

Some debts cannot be deducted, including:

- Debts forgiven by the creditor

- Debts not legally enforceable at death

- Certain debts incurred to acquire excluded property (e.g., loans used to acquire assets that are excluded from IHT), restricted by IHTA anti-avoidance rules

- Debts for which the estate is not liable (e.g., third-party obligations)

- Loans attributable to financing non-residents’ foreign currency accounts (subject to statutory restriction)

Anti-avoidance provisions restrict deductibility of liabilities:

- Loans or liabilities used to acquire, maintain, or improve excluded property (e.g., certain foreign assets of a non-domiciled individual) may be disallowed or limited (IHTA 1984 anti-avoidance).

- Where liabilities relate to financing the balance on certain foreign currency accounts of individuals not domiciled or resident in the UK immediately before death, deduction is restricted to the excess over the account balance, with further limitations to prevent tax advantage arrangements.

PRs must also adjust the IHT account if an arm’s length liability reported as deducted is not actually repaid.

Worked Example 1.5

The deceased owed £10,000 on a credit card, had an outstanding mortgage of £50,000 on her house, and had made a gift to her son with a reservation of benefit. Which liabilities are deductible?

Answer:

The credit card debt and the mortgage are deductible. Any liability relating to the gift with reservation of benefit is not deductible for inheritance tax purposes.

Worked Example 1.6

The deceased (resident and domiciled in the UK) took a loan used to buy an offshore portfolio that qualifies as excluded property. The debt remains outstanding at death. Can PRs deduct the full loan for IHT?

Answer:

No. Deductibility of liabilities is restricted where the debt funded excluded property. The loan is disallowed or limited under IHTA anti-avoidance provisions, and the PRs should not deduct the full amount when calculating the estate’s IHT.

Net Estate and Inheritance Tax

The net estate is the value of all assets less deductible liabilities. This figure is used to calculate inheritance tax (IHT).

Key Term: net estate

The value of the estate after deducting all allowable liabilities from the gross value of assets.

IHT is charged on the net estate, subject to exemptions and reliefs (e.g., spouse/civil partner and charity exemptions, business property relief (BPR), agricultural property relief (APR), nil rate band and, where conditions are met, residence nil rate band).

Key Term: residence nil rate band

An additional nil rate band on death where a qualifying residential interest is closely inherited by direct descendants, subject to tapering for larger estates and qualifying conditions.

PRs must submit the appropriate IHT account:

- IHT205 for excepted estates (broadly where the gross estate plus specified transfers do not exceed thresholds, or transfers fall into specified exempt categories and other criteria are met).

- IHT400 for non-excepted estates owing tax or requiring a full account. Associated schedules may be needed (e.g., lifetime gifts, business/agricultural reliefs). Asset values are rounded down, liabilities rounded up. HMRC issues IHT421 (probate summary) to the probate registry on receipt of payment/account.

Note that a grant of representation cannot be obtained until any IHT due before grant is paid. Funding may be arranged via the Direct Payment Scheme from bank/building society accounts, by loans from beneficiaries or financial institutions, or by realising assets where possible.

Worked Example 1.7

A deceased’s estate consists of a house (£400,000), bank accounts (£50,000), and personal chattels (£10,000). Debts include a mortgage (£100,000), funeral expenses (£5,000), and a personal loan (£15,000). What is the net estate for IHT?

Answer:

Total assets: £400,000 + £50,000 + £10,000 = £460,000. Deduct liabilities: £100,000 + £5,000 + £15,000 = £120,000. Net estate: £460,000 – £120,000 = £340,000.

Worked Example 1.8

The deceased leaves the entire estate to a surviving spouse and a gift of £50,000 to a registered charity. How do exemptions affect IHT?

Answer:

Transfers to a spouse/civil partner and to qualifying charities are exempt. If the whole estate passes to the spouse except for the charity gift, both transfers are exempt, and no IHT is payable (subject to any deemed property within the estate). The PRs still file the appropriate account (IHT205 or IHT400) depending on whether the estate is excepted.

Order of Payment of Debts

The Administration of Estates Act 1925 sets out the order in which debts must be paid:

- Funeral, testamentary, and administration expenses

- Secured debts (e.g., mortgages)

- Preferential debts (e.g., certain employee wages)

- Unsecured debts (e.g., credit cards, personal loans)

- Beneficiaries’ entitlements

PRs must ensure all debts are paid before distributing the estate. Failure to do so can result in personal liability.

In a solvent estate, unsecured creditors are paid from the estate’s assets in the statutory order. Where debts cannot be satisfied from residue because the will exonerates residue, other funds may be used in sequence: property specifically given for paying debts, property charged with debts, pecuniary legacy fund (legacies abate rateably), then specific devises/bequests rateably according to value. The equitable doctrine of marshalling may compensate beneficiaries whose legacies were used to pay debts from categories that ought not to bear them as between beneficiaries. Testamentary directions may alter the default position (e.g., residue “subject to” or “after” payment of debts; gifts “free of mortgage”).

If the estate is insolvent (insufficient assets to pay expenses and debts/liabilities in full), beneficiaries receive nothing. PRs must follow the insolvency order carefully: funeral/testamentary/administration expenses first, then preferred debts (as defined in insolvency law), then ordinary debts (including HMRC), then interest, and finally deferred debts (e.g., certain loans from a spouse). PRs must not prefer one creditor over another within the same class and may be personally liable if they pay lower-ranking debts knowing higher-ranking debts exist or act with undue haste.

Exam Warning: If PRs distribute the estate before all debts are paid, they may be personally liable to unpaid creditors. Always check for outstanding liabilities before making distributions.

Worked Example 1.9

An estate has assets of £120,000. Funeral/admin costs are £10,000. Preferred employee wage claims total £8,000. Ordinary unsecured debts total £130,000. How are payments made?

Answer:

Pay funeral/admin £10,000 first, leaving £110,000. Pay preferred debts next (£8,000) leaving £102,000. The remaining ordinary unsecured debts (£130,000) abate proportionately across creditors from the £102,000 available. Beneficiaries receive nothing because the estate is insolvent.

Impact on Beneficiaries and Estate Accounts

The valuation of assets and liabilities affects the amount available for beneficiaries. PRs must prepare estate accounts showing:

- Gross value of assets

- Liabilities paid

- Net estate available for distribution

Beneficiaries are entitled to see these accounts and may challenge valuations or deductions if they believe them to be incorrect. Where appropriate, PRs may appropriate assets in satisfaction of beneficiaries’ shares (with consents and valuations), rather than selling them, which can be useful for family homes or specific assets. Income apportionment rules may be excluded by will clauses to simplify administration; otherwise, the Apportionment Act may require splitting income arising around the date of death between capital and income beneficiaries.

PRs should protect themselves against unknown creditors or beneficiaries by advertising under Trustee Act 1925, s27 in the London Gazette and appropriate local newspapers and conducting standard searches. For missing known beneficiaries or creditors, PRs may seek indemnities, insurance, pay into court, or apply for a Benjamin order to distribute on an assumed basis (e.g., treating the missing person as having predeceased), which protects PRs. PRs should wait six months after the grant before distribution to guard against claims under the Inheritance (Provision for Family and Dependants) Act 1975.

Post-death disclaimers and variations can alter entitlements for succession and, if compliant, for tax (IHT “reading back” requires written instrument within two years and other conditions). These arrangements may impact how assets are appropriated and valued for distribution but do not change the probate valuation principles.

Revision Tip: Always use the date of death for asset valuations, ensure all liabilities are supported by documentary evidence, and record the rationale and evidence for any discounts or special valuation approaches (joint shares, minority interests, related property).

Key Point Checklist

This article has covered the following key knowledge points:

- The grant of representation authorises PRs to administer the estate.

- All assets are valued at open market value at the date of death (IHTA 1984, s160), with changes caused by death reflected (s171).

- Special valuation rules apply to joint property, quoted shares, unquoted/business interests, pairs and sets, trust interests, and gifts with reservation.

- Only legally enforceable and deductible liabilities may be subtracted from the gross estate; liabilities linked to excluded property may be restricted.

- The net estate is used to calculate inheritance tax and for distribution to beneficiaries, applying exemptions and reliefs (including spouse/civil partner and charity exemptions, BPR/APR, nil rate bands).

- PRs must file the correct IHT account (IHT205 or IHT400) and obtain IHT421 before the grant; payment may be needed pre-grant.

- Debts must be paid in the statutory order before beneficiaries receive their share; understand the distinctions between solvent and insolvent estates, abatement, marshalling, and contrary will provisions.

- PRs should use s27 advertisements and consider Benjamin orders/insurance to protect against unknown or missing claimants.

- Accurate valuation, careful deduction of liabilities, and full estate accounts are essential for proper estate administration and SQE1 success.

Key Terms and Concepts

- grant of representation

- market value

- probate value

- related property rules

- qualifying interest in possession

- deductible liability

- excepted estate

- net estate

- residence nil rate band