Learning Outcomes

This article examines IHT anti-avoidance provisions for lifetime transfers and transfers on death, including:

- Gifts with reservation of benefit (GROB) rules for lifetime gifts and death estates, and their operation under Finance Act 1986, ss 102–102C

- Circumstances in which a donor’s continued enjoyment of gifted property is caught, and valid carve-outs (full market rent, genuine co-occupation)

- Treatment of ending a reservation as a further transfer (typically a PET) and the effect of surviving or dying within seven years of cessation

- Associated operations, aggregation of ostensibly separate steps, and determination of the true loss to the donor to counter avoidance

- The pre-owned assets tax (POAT) regime: scope for land, chattels and derived property, thresholds, and interaction with GROB (including the availability of the POAT IHT election)

- IHT consequences of settlor-interested trusts and how anti-avoidance rules keep trust assets in the estate

- Incorporation of these rules into IHT calculations on lifetime transfers and on death, including double charge relief principles and practical planning implications

SQE1 Syllabus

For SQE1, you are required to understand the anti-avoidance provisions relevant to inheritance tax on lifetime transfers and transfers on death, with a focus on the following syllabus points:

- the operation and effect of the gifts with reservation of benefit (GROB) rules (FA 1986, ss 102–102C), including value at death and when the reservation ends

- the concept of associated operations (IHTA framework) and how HMRC may treat connected transactions as a single transfer to reflect the true loss to the donor

- the pre-owned assets tax (POAT) regime (FA 2004, Sch 15): scope, annual benefit charge, de minimis thresholds, exclusions, and its relationship to IHT

- the co-ownership exemption and the conditions for genuine shared occupation without reservation of benefit

- the effect of releasing a reservation of benefit (treated as a PET or CLT as appropriate) and timelines for seven-year survivorship

- double taxation relief principles to prevent both lifetime and death charges on the same value where GROB applies

- settlor-interested trusts and how retained benefit by the settlor/spouse can keep trust assets within the settlor’s estate for IHT

- practical anti-avoidance measures beyond GROB and POAT, including HMRC’s use of associated operations and targeted rules such as same-day additions for relevant property trusts

- the interaction between these rules and the calculation of IHT on death and during lifetime, including cumulation and taper relief on PETs

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is a gift with reservation of benefit and how does it affect the donor’s estate for IHT purposes?

- Which anti-avoidance provision allows HMRC to treat a series of related transactions as a single transfer for IHT?

- What is the pre-owned assets tax (POAT) and when might it apply?

- True or false? If a donor gives away their house but continues to live in it rent-free, the house is excluded from their estate for IHT.

Introduction

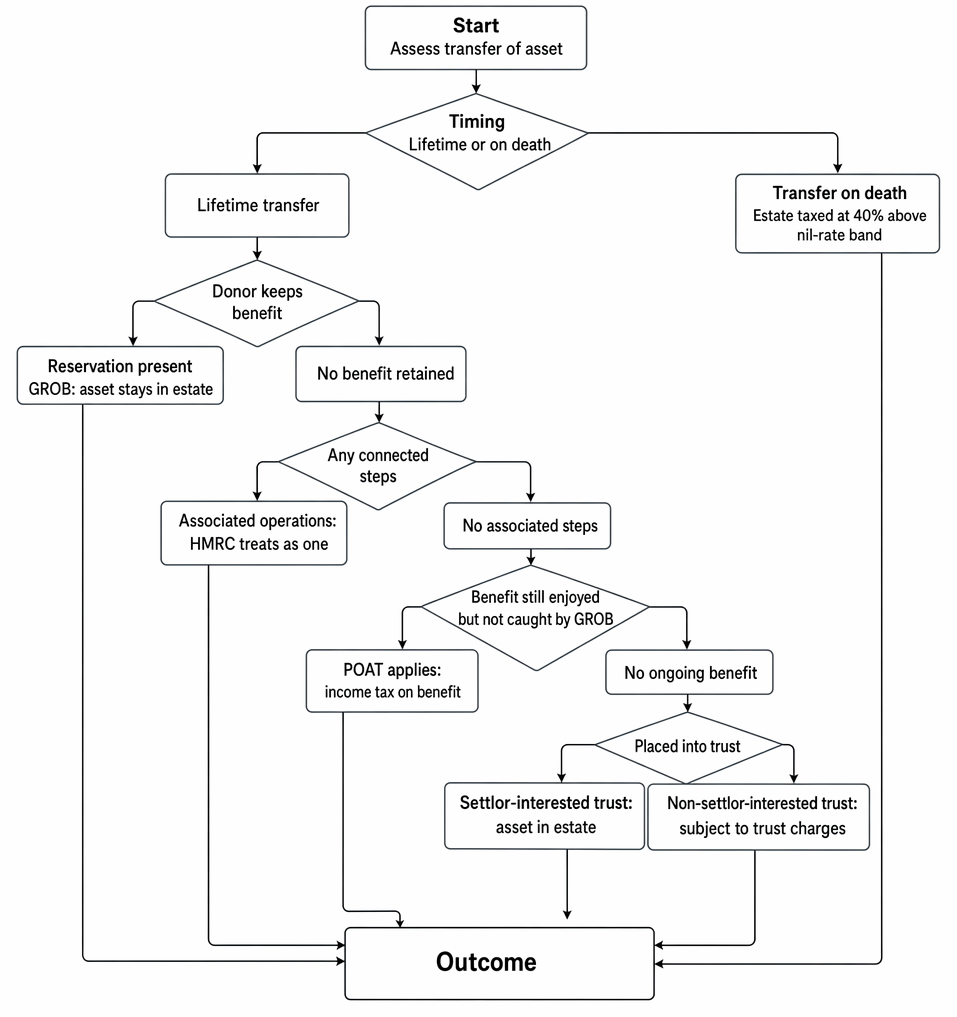

Inheritance tax (IHT) is charged on transfers of value made during a person’s lifetime and on death. The law contains targeted anti-avoidance provisions to prevent individuals from reducing their IHT liability by giving away assets while continuing to benefit from them, or by using composite arrangements to avoid tax. For SQE1, you must be able to identify and apply the main anti-avoidance rules, especially gifts with reservation of benefit, associated operations, and the pre-owned assets tax. These operate alongside broader anti-abuse concepts, with HMRC empowered to look at the substance of arrangements and their combined effect when calculating the true loss to the donor for IHT purposes.

Inheritance tax anti-avoidance treatment of lifetime transfers and transfers on death, including GROB, associated operations, POAT and trust treatment, is summarised.

Key Term: gift with reservation of benefit (GROB)

A gift made by an individual who retains some benefit or enjoyment from the property given away. For IHT, the asset is treated as remaining in the donor’s estate.

Gifts with Reservation of Benefit (GROB)

A common IHT strategy is to make gifts during lifetime so that the value of the gift is removed from the donor’s estate, provided the donor survives seven years. However, the law prevents this from working if the donor continues to benefit from the asset. The rules are found in sections 102–102C of the Finance Act 1986. In broad terms, if the donor does not part with possession and enjoyment or is not excluded from any benefit, the property is treated as remaining part of the donor’s estate at death. The asset is brought back at its value at the date of death, not at the date of the original gift.

Continuing benefit includes occupation of land rent-free, use of chattels retained for personal enjoyment, or access to income or capital from a trust of which the donor is not excluded. The reservation can be direct or indirect. What matters is whether the donor has continued enjoyment or benefit attributable to the gifted property.

If a person gives away an asset but continues to use or enjoy it (for example, gifting a house to children but continuing to live there rent-free), the asset is still included in the donor’s estate for IHT purposes.

Worked Example 1.1

Aisha gives her house to her son but continues to live in it without paying market rent. She dies five years later. Is the house included in her estate for IHT?

Answer:

Yes. This is a gift with reservation of benefit. The house is treated as part of Aisha’s estate at death (at its then market value) and is subject to IHT.

Avoiding a GROB

The GROB rules do not apply if the donor pays full market rent for continued use of the asset, or if the donor ceases to benefit from the asset at least seven years before death. To be effective, rent must be at arm’s length, reviewed as appropriate, actually paid, and not funded by circular payments from the donee or connected parties. It must cover occupation and, typically, the donor should meet normal tenant outgoings rather than the owner’s.

Key Term: market rent

The rent that would be paid for the use of the property on the open market between unconnected parties. Key Term: full consideration

Payment or value given in return for the use or enjoyment of an asset, equivalent to what would be agreed at arm’s length.

A further important carve-out is genuine co-occupation following a gift of an undivided share. Where the donor gives a share of a home to, say, an adult child and both genuinely occupy the property, the donor’s continued occupation can be attributed to their retained share, provided the arrangement is not engineered and the donor pays their fair share of expenses.

Key Term: co-ownership exemption

A carve-out where a donor gifts an undivided share of a property and thereafter genuinely co-occupies with the donee. The donor’s occupation is treated as attributable to their retained share if the conditions are met, so GROB does not apply.

Worked Example 1.2

Ben gifts his holiday cottage to his daughter but continues to use it for two weeks each year, paying a fair market rent for those weeks. Does the GROB rule apply?

Answer:

No. As Ben pays full market rent for his use, there is no reservation of benefit and the cottage is not included in his estate.

Worked Example 1.3

Priya gifts her home to her nephew. She signs a tenancy at a nominal rent that is plainly below market levels and the nephew reimburses Priya for utilities. Priya dies three years later. Is there a reservation?

Answer:

Yes. Below-market rent coupled with continued subsidised occupation is a reservation of benefit. The house is included in Priya’s death estate at its value at death.Exam Warning: If the donor only pays a token or below-market rent, the GROB rules will still apply. Always check if the benefit retained is more than negligible. Ensure rent is arm’s length and not funded by circular gifts.

Releasing a Reservation and Double Charge Relief

If the donor ceases to enjoy the benefit (e.g., moves out or starts paying full market rent), the reservation ends. The ending of a reservation is generally treated as a further transfer at that point (commonly a PET to the original donee). If the donor survives seven years after the cessation, no IHT arises. If the donor dies within seven years of cessation, the PET becomes chargeable, with taper relief potentially applying.

To prevent double taxation, where the gifted property is brought into the death estate by GROB but there was also a lifetime charge (e.g., a CLT into trust), statutory mechanisms ensure credit or disregard so that the property is not taxed twice on the same value. Practically, the death inclusion displaces the lifetime charge or grants credit for lifetime IHT paid to arrive at a just outcome.

Worked Example 1.4

Ravi gave his home to his daughter in 2010 but continued to live there rent-free. In 2018 he moved into rented accommodation and the reservation ended. He dies in 2024. What is the IHT position?

Answer:

The cessation in 2018 is treated as a PET. Ravi survived more than seven years after the original gift but fewer than seven years after the cessation. The PET (2018) becomes chargeable on death. The house is not included under GROB because the reservation had ended; instead the PET is brought into the death calculation, with taper relief if death occurred more than three years after cessation.

Worked Example 1.5

Fatima gifts a 50% share of her home to her adult son. They both live there and share bills proportional to their shares. Fatima dies six years later. Does GROB apply?

Answer:

No. This falls within the co-ownership exemption. Fatima’s occupation is referable to her retained 50% share and there is genuine shared occupation. The gifted share is not brought back under GROB.

Associated Operations

The anti-avoidance rules also target arrangements where a series of transactions are used to achieve a tax advantage. HMRC can treat connected steps as a single transfer to reflect the true substance of what has been achieved.

Key Term: associated operations

Two or more transactions or arrangements that together affect the same property or are designed to achieve a particular outcome for IHT.

Where, for example, a donor gives away an asset but arranges – through side agreements, sham contracts or reciprocal gifts – to continue benefiting, HMRC may view the steps as one composite transaction. The combined effect is assessed to determine the real “loss to the donor,” preventing the arrangement from defeating IHT.

Associated operations often arise in cases of disguised benefits: non-arm’s length “consultancy” payments tied to a gift of shares, reciprocal gifts of houses between family members followed by occupation, or lease-back arrangements which are not commercially justifiable. They can also be relevant when computing reliefs or cumulation where steps form part of a planned sequence.

Worked Example 1.6

Clare gives her shares in a family company to her brother. At the same time, her brother agrees to pay Clare an annual sum for “consultancy services” that is not genuinely for work done. Can HMRC treat this as an associated operation?

Answer:

Yes. If the payments are not genuine, HMRC may treat the arrangement as a single transaction designed to avoid IHT. The combined steps can be assessed to conclude that Clare has not parted with benefit, undermining the effectiveness of the gift.

Worked Example 1.7

Two siblings, Omar and Leila, each gift their home to the other and continue to live in their respective homes rent-free. They execute mirror deeds a week apart. Is this likely to be challenged?

Answer:

Yes. HMRC can treat the steps as associated operations or a composite transaction. The reciprocal gifts do not achieve genuine divestment; each sibling retains the benefit of occupation. GROB would apply to each home.

Pre-Owned Assets Tax (POAT)

Where the GROB rules do not apply, the pre-owned assets tax (POAT) may impose an income tax charge if a person continues to benefit from assets they previously owned or provided the funds to acquire. POAT is found in FA 2004, Sch 15. It is designed to catch arrangements falling outside GROB but where the person derives ongoing enjoyment of previously owned property or property derived from funds they provided.

Key Term: pre-owned assets tax (POAT)

An income tax charge on individuals who benefit from assets they previously owned or funded but have given away, where the GROB rules do not apply.

POAT is most relevant to land, chattels, and certain intangible arrangements involving “derived property.” Common triggers include a parent gifting cash to an adult child who uses it to buy a house in which the parent then lives rent-free, or gifting art but retaining it at home. POAT charges an annual amount based on the value of the benefit enjoyed (often by reference to a notional rental value for land), subject to a de minimis threshold. If the annual benefit is £5,000 or less (after deducting any genuine consideration paid), POAT does not apply. If POAT applies, the person reports and pays the income tax charge annually.

Key Term: chattel

A moveable item of personal property (not land).

Where the GROB rules do apply, POAT does not. Conversely, where GROB is avoided (e.g., because the asset gifted was not the same asset now enjoyed), POAT may bite. There is a statutory election to opt out of POAT by accepting that the property will be treated as subject to IHT at death (effectively reinstating GROB treatment).

Key Term: POAT election

An election to disapply POAT by agreeing that the relevant property will be treated as subject to IHT on death (broadly, reinstating GROB inclusion). This avoids ongoing income tax charges but may increase IHT on death.

Worked Example 1.8

David gives his art collection to his children but keeps the paintings hanging in his home. The GROB rules do not apply because he claims to have given up ownership. Does POAT apply?

Answer:

Yes. If David continues to enjoy the chattels, POAT may apply and he may have to pay income tax on the annual value of the benefit, unless a POAT election is made to accept IHT inclusion on death.

Worked Example 1.9

Marta gifts £300,000 to her son, who buys a flat. Marta moves in and pays no rent. POAT or GROB?

Answer:

GROB does not apply because Marta did not own the flat before the gift; she funded its purchase by her son and now enjoys occupation. POAT is likely to apply to charge income tax on the annual benefit (subject to the £5,000 de minimis and any genuine consideration paid). Marta could make a POAT election to avoid the annual charge, accepting IHT inclusion at death.

Worked Example 1.10

Sophie gave her holiday home to a trust 12 years ago, excluding herself from benefit. The trustees later appointed it to her adult daughter, who invites Sophie to stay occasionally for a week, with Sophie paying market rent. Does POAT arise?

Answer:

No. The original gift excluded Sophie. Occasional stays for which she pays market rent constitute full consideration for use. Neither GROB nor POAT applies.

Settlor-Interested Trusts

If a person sets up a trust and can still benefit from it, the trust assets may be included in their estate for IHT. This commonly arises as a GROB issue: the settlor is not excluded from benefit or retains enjoyment of trust property.

Key Term: settlor-interested trust

A trust where the settlor or their spouse/civil partner can benefit from the trust property.

For IHT, if the settlor retains an interest or enjoyment (or fails to exclude themselves and their spouse/civil partner from benefit), the value of the trust assets may be included in their estate at death. This interacts with other tax anti-avoidance regimes (e.g., income tax attribution for settlor-interested trusts), but the key IHT point is that failing to exclude the settlor and spouse/civil partner risks the trust being ineffective to remove value from the estate.

Worked Example 1.11

Noah settles a property into a discretionary trust for his children and spouse. He keeps the right to occupy the property if he wishes. Noah dies eight years later, having lived there for much of that time. IHT position?

Answer:

The trust is settlor-interested; Noah retained enjoyment of the property. Under GROB, the property’s value at death is included in Noah’s estate and subject to IHT.

Practical Impact on IHT Planning

The anti-avoidance rules mean that common strategies to reduce IHT, such as giving away assets but continuing to use them, are unlikely to be effective unless the donor genuinely gives up all benefit. HMRC has wide powers to challenge arrangements that are artificial or designed to avoid tax, including treating connected steps as associated operations and scrutinising whether rent and consideration are truly at market levels.

Key planning points include:

- ensuring full and genuine arm’s length consideration for any continued use of gifted assets, with proper documentation and actual payment

- using the co-ownership exemption only where there is genuine shared occupation and fair sharing of expenses; engineered arrangements are likely to fail

- if a reservation exists, ending it as early as practicable; note that cessation is treated as a further transfer (usually a PET), with the seven-year clock starting from cessation

- considering whether a POAT election is preferable to ongoing annual POAT charges, balancing income tax against likely IHT on death

- excluding the settlor and their spouse/civil partner from benefit under lifetime trusts intended to remove value from the estate

- avoiding reciprocal or circular arrangements that leave the donor with effective enjoyment despite apparent transfers; associated operations can collapse such structures

- being aware of targeted rules beyond GROB/POAT, such as the same-day additions rules for relevant property trusts, which affect periodic charges and exits, limiting multi-trust strategies that artificially multiply nil-rate bands

- the General Anti-Abuse Rule (GAAR) applies to IHT arrangements. Under the GAAR, a tax arrangement is abusive if it satisfies both the "main purpose" test—it is reasonable in all the circumstances to conclude that obtaining a tax advantage is the main purpose, or one of the main purposes, of the arrangement—and the "abusive" test—entering into the arrangement cannot reasonably be regarded as a reasonable course of action in relation to the relevant tax provisions, having regard to all the circumstances. The GAAR empowers HMRC to counteract the tax advantage obtained by abusive arrangements, and a GAAR Advisory Panel provides non-binding opinions on whether specific cases fall within the rule

Worked Example 1.12

In 2015, Ava had created three pilot discretionary trusts on separate days, each initially with £10. In 2023 she adds £100,000 to each trust on the same day. Does any anti-avoidance rule affect periodic charge calculations?

Answer:

Yes. Same-day additions rules aggregate relevant property added on the same day when calculating the rate for 10-year anniversaries and exit charges. The additions are brought into account across the trusts to limit the benefit of multiple settlements.Revision Tip: Always check if the donor has retained any benefit, directly or indirectly, from the asset given away. If so, the GROB or POAT rules may apply. Consider whether cessation of a reservation has occurred and when, and assess whether rent or consideration is genuinely at market level.

Key Point Checklist

This article has covered the following key knowledge points:

- gifts with reservation of benefit (GROB) prevent assets being removed from the estate if the donor retains benefit; inclusion is at value at death

- paying full market rent for continued use of an asset may avoid the GROB rules; ensure the rent is arm’s length and not funded indirectly by the donee

- genuine co-occupation after gifting an undivided share can fall within the co-ownership exemption if conditions are met

- ending a reservation is treated as a further transfer (commonly a PET); surviving seven years after cessation avoids IHT on that transfer

- double taxation relief principles prevent both lifetime charges and death inclusion on the same value where GROB applies

- associated operations allow HMRC to treat a series of steps as a single transfer for IHT, countering contrived arrangements

- pre-owned assets tax (POAT) imposes an income tax charge where GROB does not apply but the donor continues to benefit; a POAT election can opt for IHT inclusion on death instead

- settlor-interested trusts may result in trust assets being included in the settlor’s estate for IHT if the settlor or spouse/civil partner can benefit

- targeted anti-avoidance rules such as same-day additions limit multi-trust strategies for relevant property periodic and exit charges

Key Terms and Concepts

- gift with reservation of benefit (GROB)

- market rent

- full consideration

- associated operations

- pre-owned assets tax (POAT)

- chattel

- settlor-interested trust

- co-ownership exemption

- POAT election