Learning Outcomes

This article explains the IHT treatment of lifetime transfers and transfers on death, focusing on PETs and LCTs, including:

- The distinction between PETs and LCTs and when each arises

- The seven-year rule and the separate cumulation period for each transfer

- Correct application of the annual exemption and other lifetime-only exemptions to PETs and LCTs

- Computation of IHT on failed PETs, including the effect of earlier LCTs in the donor’s cumulative total (the “14-year effect”)

- Recalculation of IHT on LCTs on death, credit for lifetime tax paid, and application of taper relief

- Taper relief applied to tax (not value), time bands, and common boundary pitfalls

- Chronological application of the nil‑rate band across multiple lifetime transfers and the death estate, and the death‑only nature of the residence nil‑rate band

- Business property relief (BPR) and agricultural property relief (APR) on lifetime gifts and withdrawal on death

- Gifts with reservation taxed in the death estate and consequences for taper relief and cumulation

- Liability and payment rules for IHT on failed PETs and LCTs, timing, and availability of instalments

SQE1 Syllabus

For SQE1, you are required to understand the inheritance tax treatment of lifetime transfers and transfers on death, particularly the effect of death on PETs and LCTs, with a focus on the following syllabus points:

- the distinction between Potentially Exempt Transfers (PETs) and Lifetime Chargeable Transfers (LCTs)

- how death within seven years of a PET or LCT affects IHT liability

- the operation and calculation of taper relief

- the order and interaction of gifts and the nil-rate band

- credit for lifetime tax paid on LCTs

- practical calculation of IHT in scenarios involving multiple gifts and death

- cumulation across transfers and the “14-year effect” where earlier LCTs impact later PETs on death

- interaction of business and agricultural property relief with lifetime transfers and death

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What happens to a PET if the donor dies within seven years of making the gift?

- How is IHT calculated on an LCT if the donor dies within seven years of the transfer?

- What is the effect of taper relief, and when does it apply?

- If a person makes several gifts in the seven years before death, how is the nil-rate band applied?

Introduction

Inheritance Tax (IHT) is charged on transfers of value made during a person’s lifetime and on their death. For SQE1, you must understand how death affects the IHT treatment of gifts made during life—especially Potentially Exempt Transfers (PETs) and Lifetime Chargeable Transfers (LCTs). The seven-year rule, taper relief and the chronological application of the nil-rate band are central. You must also be able to handle more detailed points: earlier LCTs can reduce the nil‑rate band available for later PETs that fail on death (the “14‑year effect”); reliefs such as business property relief (BPR) and agricultural property relief (APR) can reduce the value transferred if the qualifying conditions remain satisfied; and gifts with reservation of benefit (GWR) are brought into the death estate rather than taxed as failed PETs.

Key Term: Potentially Exempt Transfer (PET)

A lifetime gift by an individual to another individual (or a qualifying trust) that is exempt from IHT if the donor survives seven years, but becomes chargeable if the donor dies within that period. Key Term: Lifetime Chargeable Transfer (LCT)

A lifetime gift (usually to a trust or company) that is immediately chargeable to IHT at 20% on the excess above the nil-rate band, with a further charge if the donor dies within seven years. Key Term: nil-rate band

The threshold up to which IHT is charged at 0%. Gifts and estates above this amount are taxed at 40% (subject to reliefs and exemptions). Key Term: taper relief

A reduction in the IHT payable on gifts made three to seven years before death, based on the time elapsed between gift and death. Key Term: residence nil-rate band (RNRB)

An additional 0% band (subject to conditions and taper for estates over £2m) that applies only on death to a qualifying residence closely inherited; it does not apply to lifetime transfers.

Potentially Exempt Transfers (PETs)

A PET is a gift by an individual to another individual (or to certain qualifying trusts for disabled persons or bereaved minors). At the date of the gift no IHT is due. If the donor survives seven years, the PET is ignored for IHT. If they die within seven years, the PET “fails” and becomes chargeable. The loss to the donor’s estate (after applying any reliefs and lifetime exemptions) is then fitted into the cumulative total and set against the nil‑rate band available at the time of that transfer.

Lifetime-only exemptions reduce PETs at the time of the gift:

- annual exemption of £3,000 per tax year (with one-year carry‑forward)

- small gifts exemption (£250 per donee per tax year; not usable against larger gifts to the same donee)

- normal expenditure out of income (regular, from income, and without reducing the donor’s normal standard of living)

- marriage/civil partnership gifts (limits depend on relationship)

Reliefs (e.g., BPR or APR) also reduce the value transferred if applicable and if the qualifying conditions remain satisfied up to death. If a PET is of relevant business or agricultural property, relief may be withdrawn on death if the donee no longer owns qualifying property.

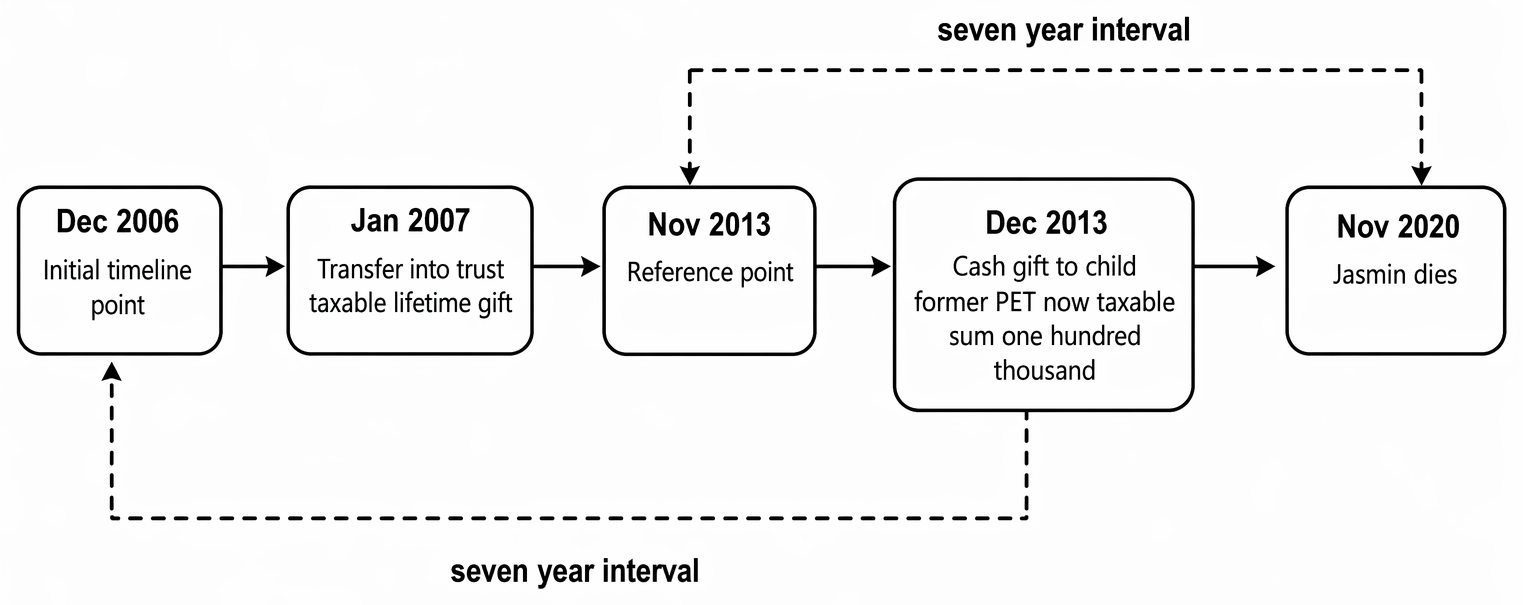

Effect of Death on PETs

The timeline presents a chargeable lifetime transfer into trust, a potentially exempt transfer, and death, with separate seven-year periods for IHT.

- If the donor dies within seven years, each PET in the seven years before death becomes chargeable. They are considered in chronological order from oldest to newest, with earlier transfers using the nil-rate band first.

- For each failed PET, recalculate the chargeable amount: start with the loss to the estate at the date of the gift, deduct lifetime-only exemptions and apply any available reliefs. Determine how much nil-rate band remained at the date of that transfer after cumulating earlier chargeable transfers.

- Any excess above the remaining nil-rate band is taxed at the death rate (40%), and taper relief may reduce that tax if more than three years had elapsed between gift and death.

- The residence nil-rate band cannot be set against lifetime transfers; it applies only to qualifying interests on death.

- Gifts with reservation of benefit are not taxed as failed PETs. The gifted property is treated as part of the donor’s death estate. No taper relief applies to such property, and the property is not counted as a failed PET for cumulation.

In all calculations, apply exemptions and reliefs before considering the nil-rate band, and apply the nil-rate band strictly in chronological order across transfers within the relevant cumulation period.

Worked Example 1.1

Scenario: In 2017, Alice gives £200,000 to her son. In 2021, she gives £200,000 to her daughter. Alice dies in 2023, having made no other gifts.

Answer:

Both gifts are PETs. Alice died within seven years of both gifts, so both become chargeable. The gifts are applied in chronological order against the nil-rate band (£325,000):

- The 2017 gift (£200,000) uses £200,000 of the nil-rate band, leaving £125,000.

- The 2021 gift (£200,000) uses the remaining £125,000 of the nil-rate band; the excess £75,000 is taxed at 40%.

- IHT on the second gift: £75,000 × 40% = £30,000 (before taper relief).

Lifetime Chargeable Transfers (LCTs)

An LCT is immediately chargeable at the lifetime rate (20%) on the portion above the nil‑rate band after taking into account chargeable transfers made in the previous seven years. The small gifts exemption does not apply to LCTs, but the annual exemption does. Reliefs such as BPR and APR reduce the value transferred before the rate is applied.

If the donor pays the lifetime tax (rather than the trustees), a “grossing‑up” calculation may be required because IHT is charged on the value transferred (the donor’s loss), which includes the tax the donor pays. If the trustees pay the tax out of the property they receive, grossing‑up is not needed.

If the donor survives seven years after an LCT, no further charge arises. If the donor dies within seven years, the transfer is recalculated at the death rate, and credit is given for tax already paid. Taper relief may apply to reduce the recalculated tax.

Effect of Death on LCTs

- Recompute the charge as at death rates (40%), taking into account any earlier chargeable transfers in the seven years before the LCT and any PETs within seven years before the LCT that have now become chargeable on death.

- Give credit for lifetime tax already paid. If the recalculated tax is lower (typically because of taper relief), there is no refund.

- Apply BPR/APR again as at death if relevant conditions are still satisfied. Relief can be withdrawn if conditions are not met.

Worked Example 1.2

Scenario: Ben transfers £500,000 into a discretionary trust in 2019. He pays IHT of 20% on £175,000 (£500,000 - £325,000) = £35,000. Ben dies in 2022.

Answer:

The LCT is recalculated at 40%: £175,000 × 40% = £70,000. Ben died three years after the transfer, so no taper relief applies. Credit for lifetime tax paid: £70,000 - £35,000 = £35,000 additional IHT due.

Worked Example 1.3

Scenario: Clare gives £400,000 to her brother in 2018. She dies in 2023. No other gifts were made.

Answer:

Clare died five years after the gift. The nil-rate band (£325,000) is applied to the gift, leaving £75,000 chargeable. Tax at 40% = £30,000. Taper relief for 4–5 years: 60% of £30,000 = £18,000 IHT payable.

Worked Example 1.4

Scenario: David gives £200,000 to his daughter in 2016, and £200,000 to his son in 2020. He dies in 2022.

Answer:

The 2016 gift (£200,000) uses £200,000 of the nil-rate band. The 2020 gift (£200,000) uses the remaining £125,000 of the nil-rate band; the excess £75,000 is taxed at 40%. IHT on the second gift: £75,000 × 40% = £30,000 (before taper relief).

Taper Relief

Taper relief reduces the IHT payable on failed PETs and on LCTs recalculated on death if the donor dies more than three years but less than seven years after the transfer. It does not reduce the value of the gift—only the tax payable on that gift. It does not apply to tax on the death estate.

| Years between gift and death | % of full tax payable |

|---|---|

| 0–3 years | 100% |

| 3–4 years | 80% |

| 4–5 years | 60% |

| 5–6 years | 40% |

| 6–7 years | 20% |

| 7+ years | 0% (gift is exempt) |

Practical points:

- Measure the period precisely by date; boundary cases turn on whether more than 3/4/5/6 years elapsed between the gift and the date of death.

- Apply taper relief to the tax due on the particular gift, after allocating the nil-rate band to earlier gifts first.

- For LCTs, apply taper relief to the recalculated death‑rate tax and then credit any lifetime tax paid. If the lifetime tax exceeds the tapered tax, no refund is given.

Order of Gifts and the Nil-Rate Band

When a person makes multiple gifts in the seven years before death, gifts are applied against the nil-rate band in chronological order. Earlier gifts reduce the nil-rate band available for later gifts and for the death estate. The residence nil-rate band is available only on the death estate (subject to conditions) and is not used against lifetime transfers.

- For each failed PET or LCT, determine the remaining nil-rate band by looking back seven years from the date of that transfer and cumulating earlier chargeable transfers within that period.

- The “14‑year effect”: when a PET fails on death, you may have to consider LCTs made more than seven years before death if they were within seven years before the PET. This can reduce the nil‑rate band available for the PET, even though the earlier LCT itself is outside the seven-year window before death.

Worked Example 1.5

Scenario: In October 2010, Nora made an LCT of £300,000 to a discretionary trust (after annual exemptions and reliefs). In December 2013, she made a PET of £250,000 to her son. Nora dies in November 2020.

Answer:

The December 2013 PET is within seven years of death and is now chargeable. To compute its tax, look back seven years from December 2013. The October 2010 LCT falls just within that seven‑year look‑back, so it uses £300,000 of the nil‑rate band when assessing the PET.

- Remaining nil‑rate band at December 2013: £325,000 − £300,000 = £25,000.

- Chargeable portion of the PET: £250,000 − £25,000 = £225,000.

- Tax at 40% = £90,000.

- Time between gift and death is nearly seven years; taper relief at 20% applies, so tax payable on the PET is £18,000. The 2010 LCT itself is outside seven years before death, so it is not re‑charged. It affects the PET only through cumulation.

Worked Example 1.6

Scenario: In May 2019, Priya gifts 100% of her trading business (qualifying for BPR at 100%) to her daughter (a PET). The daughter sells the business in 2021 and holds the proceeds in cash. Priya dies in July 2024. Assume no other gifts.

Answer:

At the date of the gift, BPR would reduce the value transferred to nil if conditions are met. On death, to retain BPR the donee must still own qualifying business property (or permitted replacement property) at the donor’s death. Because the daughter sold the business and holds cash, BPR is withdrawn for the PET.

- PET value brought into charge: full market value at May 2019 (no BPR).

- Apply the nil-rate band first; any excess is taxed at 40%.

- Time between gift and death is over five but under six years, so taper relief reduces the tax on the PET to 40% of the full charge attributable to that gift.

Worked Example 1.7

Scenario: On 1 March 2021, Omar creates a discretionary trust with £450,000 cash (no reliefs). He agrees to pay the lifetime IHT himself. He dies on 15 June 2025. No other transfers.

Answer:

Lifetime charge (grossed up because Omar pays the tax):

- Amount above the nil‑rate band: £450,000 − £325,000 = £125,000.

- If trustees paid, lifetime tax would be 20% × £125,000 = £25,000.

- Because Omar pays, gross up the transfer so that after 20% tax the trustees still receive £450,000. Grossed‑up tax ≈ £31,250 (i.e., £125,000 × 20% ÷ 80%). On death, recalculate at 40% on £125,000 = £50,000, apply taper relief (between four and five years → 60% payable), so £30,000. Credit lifetime tax paid (£31,250). No additional tax is due and there is no refund.

Credit for Lifetime Tax Paid

If IHT was paid at the time of an LCT, credit is given when recalculating IHT on death. If taper relief reduces the recalculated amount below the lifetime tax paid, there is no refund. The credit is given gift-by-gift after computing the recalculated death‑rate tax on that transfer.

Practical Implications for Estate Planning

- PETs to individuals are often effective for IHT planning if the donor survives seven years; use annual exemptions, marriage exemptions and, where available, the normal expenditure out of income exemption to reduce PET values.

- Reliefs on lifetime gifts (BPR/APR) can be powerful but can be withdrawn on death if qualifying conditions are not met by the donee; consider replacement property provisions where available and the risk of disposal by the donee.

- LCTs (e.g., transfers into discretionary trusts) can crystallise lifetime tax and, if the donor dies within seven years, further death‑rate tax (subject to taper) after credit for lifetime tax. Consider who will pay lifetime tax (donor vs trustees) and the grossing‑up consequences.

- Gifts with reservation are brought back into the death estate rather than taxed as failed PETs; no taper relief applies. If the reservation ceases during life, a new PET may arise at cessation, starting a fresh seven‑year period.

- Administration and payment: the transferee is primarily liable for tax on a failed PET; trustees are primarily liable for LCTs; personal representatives can become liable if tax remains unpaid 12 months after the end of the month of death. Tax on failed PETs and recalculated LCTs is generally due six months after the end of the month of death. Instalments may be available for certain assets (e.g., land, qualifying business interests) attributable to the failed transfer.

- Ordering and records matter: keep a timeline of all transfers with dates, values, exemptions, and reliefs. Cumulation is assessed separately for each transfer; earlier LCTs can affect the nil‑rate band for later PETs even when the LCT itself falls outside the seven years before death.

Exam Warning: For SQE1, always check the date of each gift and the date of death. Apply the nil-rate band in chronological order, and remember that taper relief applies only to the tax, not the value of the gift.

Revision Tip: When answering calculation questions, write out the gifts and dates in order, apply the nil-rate band step by step, and show all working for taper relief and credits.

Key Point Checklist

This article has covered the following key knowledge points:

- PETs are exempt from IHT if the donor survives seven years; if not, they become chargeable.

- LCTs are immediately chargeable to IHT; if the donor dies within seven years, a further charge arises at the death rate.

- Taper relief reduces the IHT payable on gifts made three to seven years before death; it applies to tax, not value.

- The nil-rate band is applied in chronological order; earlier transfers reduce the band for later ones and for the death estate.

- Earlier LCTs can reduce the nil-rate band available for later PETs that fail on death (the “14‑year effect”).

- Credit is given for lifetime tax paid on LCTs if a further charge arises on death; no refund if tapered death‑rate tax is lower.

- BPR/APR can reduce lifetime gift values, but relief may be withdrawn on death if conditions are not met.

- Gifts with reservation are taxed in the death estate rather than as failed PETs; no taper relief applies to such property.

- The residence nil-rate band applies only on death to qualifying residential interests and is not available for lifetime transfers.

- Liability for tax on failed PETs rests primarily with donees; trustees are liable for LCTs; PRs can be secondarily liable if unpaid.

Key Terms and Concepts

- Potentially Exempt Transfer (PET)

- Lifetime Chargeable Transfer (LCT)

- nil-rate band

- taper relief

- residence nil-rate band (RNRB)