Learning Outcomes

This article outlines Inheritance Tax on lifetime transfers and transfers on death, including:

- The scope of IHT on lifetime and death transfers, distinction between PETs and CLTs, and what constitutes a transfer of value and loss to the donor

- Application of the nil rate band (NRB) and residence nil rate band (RNRB), transferability and tapering rules, and cumulation of lifetime gifts affecting the IHT position on death

- Key exemptions and reliefs—spouse and charity exemptions, annual exemption, small gifts, gifts out of income, gifts on marriage, business relief, and agricultural relief—and interaction of reliefs

- IHT treatment of trusts (bare, interest in possession, and discretionary/relevant property trusts), and computation of entry, periodic, and exit charges including related-settlements and same-day-additions considerations

- IHT calculations in common scenarios, including charity reduced rate computations, RNRB downsizing additions, and grossing when the donor pays lifetime tax, and identification of the liable payer and payment timing with instalment options

- Anti-avoidance risks (gifts with reservation of benefit and pre-owned asset income tax) and the 14‑year cumulation trap involving earlier CLTs and later PETs

SQE1 Syllabus

For SQE1, you are required to understand Inheritance Tax on lifetime transfers and transfers on death, with a focus on the following syllabus points:

- the distinction between potentially exempt transfers (PETs) and chargeable lifetime transfers (CLTs)

- the operation of the nil rate band and residence nil rate band (RNRB)

- the effect of lifetime gifts on the available nil rate band at death

- the main IHT exemptions and reliefs (including spouse exemption, annual exemption, small gifts, gifts out of income, business and agricultural relief)

- the IHT treatment of trusts, including entry, periodic, and exit charges

- calculation of IHT liabilities in typical exam scenarios

- who is liable to pay IHT and when it is due, including the instalment option

- the charity reduced rate (36%) and how to test the baseline amount

- transferable NRB and transferable RNRB, and RNRB downsizing addition

- taper relief bands and credit for lifetime tax paid

- anti-avoidance: gifts with reservation of benefit (GWR) and pre-owned asset tax (POAT)

- cumulation principles and the “14‑year” effect where CLTs precede PETs

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is a potentially exempt transfer (PET), and when does it become chargeable to IHT?

- How does the nil rate band operate in relation to lifetime gifts and transfers on death?

- Name three main exemptions from IHT that can apply to lifetime gifts.

- What is the maximum IHT rate on a discretionary trust’s ten-year anniversary charge?

- How does the residence nil rate band (RNRB) increase the IHT threshold, and when does it apply?

Introduction

Inheritance Tax (IHT) is a tax on the transfer of wealth, charged on certain gifts made during a person’s lifetime and on the value of their estate at death. For SQE1, you must be able to distinguish between the different types of transfers, apply the correct exemptions and reliefs, and calculate the IHT liability in common scenarios. This article provides an overview of the key rules and concepts.

Key Term: transfer of value

Any disposition by an individual that causes the value of their estate immediately after the disposition to be less than it would be but for the disposition. The amount of the reduction is the value transferred (loss to the donor). Key Term: loss to donor principle

The value for IHT is measured by the reduction in the donor’s estate caused by the transfer, not necessarily the market value of the asset given (for example, where related property rules increase or decrease values).Test Tip: In SQE-style questions on Overview of Inheritance Tax (IHT), identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Lifetime Transfers: PETs and CLTs

IHT can arise on transfers made during a person’s lifetime. There are two main categories:

- Potentially Exempt Transfers (PETs): Gifts made by an individual to another individual (or to certain trusts for disabled persons or bereaved minors). PETs are not immediately chargeable to IHT, but become chargeable if the donor dies within seven years of the gift.

- Chargeable Lifetime Transfers (CLTs): Gifts made to most types of trusts (e.g., discretionary trusts) or companies. CLTs are immediately chargeable to IHT if they exceed the available nil rate band.

Key Term: potentially exempt transfer (PET)

A gift made by an individual to another individual (or certain qualifying trusts) that is exempt from IHT if the donor survives seven years, but becomes chargeable if the donor dies within that period. Key Term: chargeable lifetime transfer (CLT)

A gift made during lifetime (usually to a trust or company) that is immediately chargeable to IHT if it exceeds the nil rate band. Key Term: annual exemption

Each individual can give away up to £3,000 per tax year free of IHT. Unused exemption can be carried forward one year and must be used in chronological order (current year before prior year). Key Term: small gifts exemption

Gifts of up to £250 per recipient per tax year are exempt, provided the recipient does not also receive part of the annual exemption. Key Term: gifts on marriage

Certain lifetime wedding gifts are exempt: up to £5,000 by a parent, £2,500 by a grandparent or remoter ancestor, and £1,000 by others. Key Term: gifts out of income

Regular gifts made out of surplus income, which do not affect the donor’s normal standard of living, are exempt from IHT.

The Seven-Year Rule and Taper Relief

If the donor survives seven years after making a PET, the gift is exempt from IHT. If the donor dies within seven years, the PET becomes chargeable and uses up part of the nil rate band. If death occurs more than three years after the gift, taper relief reduces the tax payable on the PET. Taper relief reduces the tax on the gift, not the value of the transfer for cumulation.

Key Term: taper relief

A reduction in the IHT payable on a PET or CLT if the donor dies more than three years but less than seven years after the gift (bands at 80%, 60%, 40%, and 20% of the death rate for years 3–4, 4–5, 5–6, 6–7 respectively). Key Term: cumulation

The process of aggregating chargeable transfers made in the seven years before a given transfer to determine how much of the nil rate band is available.

Worked Example 1.1

Aisha gives £250,000 to her son in April 2016. She makes no other gifts. She dies in May 2022. What is the IHT position?

Answer:

The gift is a PET. Aisha died just over six years after the gift, so the PET becomes chargeable. The gift uses up £250,000 of the nil rate band available at death. Taper relief applies (since death was more than five but less than six years after the gift), so only 40% of the full IHT rate is payable on any part of the PET above the nil rate band.

Worked Example 1.2

Maya makes three gifts to her niece: £1,500 on 1 May 2022, £2,000 on 1 November 2022, and £1,000 on 1 June 2023. She made no other gifts. How does the annual exemption apply?

Answer:

The annual exemption is applied chronologically within each tax year. For 2022/23 tax year, the first two gifts total £3,500; £3,000 is covered by the annual exemption and £500 is a PET. For 2023/24, the £1,000 gift is covered by that year’s annual exemption (up to £3,000 available). No carry-forward is available into 2023/24 because 2022/23’s exemption was fully used.

Transfers on Death and Nil Rate Bands

On death, IHT is charged on the value of the deceased’s estate, including assets in their sole name and certain trust interests. The nil rate band (NRB) is the threshold below which no IHT is payable.

Key Term: nil rate band (NRB)

The amount of an estate (or chargeable transfers) that is taxed at 0% for IHT purposes. The standard NRB is £325,000.

An individual’s NRB can be increased by any unused percentage from a predeceasing spouse’s NRB (the transferable nil rate band). This is claimed by the personal representatives and applied as a percentage uplift to the survivor’s NRB.

Key Term: transferable nil rate band (TNRB)

The portion of a predeceasing spouse’s or civil partner’s unused NRB (as a percentage) that can be transferred to the survivor’s estate, increasing their available NRB at death.

The Residence Nil Rate Band (RNRB)

If a person leaves a qualifying residence to direct descendants, an additional residence nil rate band (RNRB) may apply, increasing the IHT-free threshold.

Key Term: residence nil rate band (RNRB)

An additional IHT-free allowance (up to £175,000) when a home is left to direct descendants, subject to tapering for estates over £2 million.

The RNRB can also be transferred between spouses as a percentage if unused by the first to die, and a downsizing addition may be available if the deceased sold or downsized their home and left equivalent assets to descendants.

Key Term: transferable residence nil rate band (TRNRB)

The unused percentage of a predeceasing spouse’s RNRB transferable to the survivor, to be applied to the RNRB at the survivor’s death. Key Term: downsizing addition

An additional amount of RNRB available where a person sold, gifted or downsized their residence and at death leaves other assets to direct descendants; the addition broadly preserves RNRB up to the lost value. Key Term: excluded property

Property excluded from the UK IHT charge, notably certain foreign assets of non‑UK domiciled persons, or specific trust property, subject to statutory rules.

Worked Example 1.3

John dies in 2023/24, leaving an estate of £600,000, including his house worth £300,000, to his children. He made no lifetime gifts. What is the IHT liability?

Answer:

The estate benefits from the standard NRB (£325,000) and the full RNRB (£175,000), giving a total threshold of £500,000. The taxable estate is £600,000 – £500,000 = £100,000. IHT at 40% is £40,000.

Worked Example 1.4

Eleanor dies in 2024 with an estate of £2.3 million. Her main residence worth £500,000 passes to her grandchildren. She made no lifetime gifts. Does RNRB apply, and if so, how?

Answer:

RNRB tapers away £1 for every £2 of estate above £2 million. Excess over £2 million is £300,000, taper is £150,000. Starting RNRB is £175,000; £175,000 – £150,000 = £25,000 RNRB available. NRB of £325,000 also applies. Total threshold is £350,000. Taxable estate is £2,300,000 – £350,000 = £1,950,000 at 40% (subject to any charity exemptions or other reliefs).

Exemptions and Reliefs

Certain gifts and transfers are exempt from IHT, either in whole or in part.

Key Term: spouse exemption

Transfers between spouses or civil partners are exempt from IHT, regardless of amount or timing. Special rules apply where the recipient spouse is non‑UK domiciled (limited exemption, with election possible to be treated as UK‑domiciled). Key Term: charity exemption

Transfers to UK charities are exempt from IHT. Charitable legacies may also reduce the rate of IHT if the 10% test is met. Key Term: charitable reduced rate (36%)

If 10% or more of the net baseline amount in a component of the estate is left to charity, the IHT rate on that component is reduced from 40% to 36%. Key Term: baseline amount

For charity reduced rate, the net value of a component (after debts, NRB/TNRB, reliefs and exemptions other than charity) used to test whether the charitable legacy equals at least 10% of that amount. Key Term: annual exemption

Each individual can give away up to £3,000 per tax year free of IHT. Unused exemption can be carried forward one year. Key Term: small gifts exemption

Gifts of up to £250 per recipient per tax year are exempt, provided the recipient does not also receive part of the annual exemption. Key Term: gifts out of income

Regular gifts made out of surplus income, which do not affect the donor’s standard of living, are exempt from IHT.

Other important exemptions include gifts in consideration of marriage (up to specified limits), gifts to charities, and gifts for family maintenance.

Worked Example 1.5

Fatima gives £2,000 to each of her four grandchildren in one tax year. How much of these gifts is exempt from IHT?

Answer:

The first £3,000 is covered by the annual exemption. The remaining £5,000 (£8,000 – £3,000) is covered by the small gifts exemption (£250 per recipient × 4 = £1,000). The balance (£4,000) is a PET.

Reliefs: Business and Agricultural Property

Certain business and agricultural assets attract relief from IHT, reducing or eliminating the tax payable.

Key Term: business relief

A relief reducing the value of relevant business property for IHT purposes by 50% or 100%, provided qualifying conditions (including trading and ownership periods) are met. Key Term: agricultural relief

A relief reducing the value of qualifying agricultural property for IHT purposes by 50% or 100%, subject to conditions such as agricultural use and ownership period.

Reliefs can apply to lifetime transfers and transfers on death. Ensure the ownership period and qualifying nature of activities are satisfied; relief may be withdrawn if the transferee disposes of the asset before the transferor’s death in PET cases.

The Cumulative Principle and Lifetime Gifts

When calculating IHT on death, all chargeable transfers made in the seven years before death are cumulated with the death estate. PETs that become chargeable and CLTs are deducted from the nil rate band first, reducing the threshold available for the death estate. Where a CLT occurs before a PET, death within seven years of the PET can bring the earlier CLT into the PET’s cumulation period—a common “14‑year” trap.

Inheritance Tax on lifetime transfers and transfers on death is presented through PETs, CLTs, nil-rate bands, reliefs, exemptions, trust charges, and rates.

Worked Example 1.6

Omar made a CLT of £200,000 to a discretionary trust in 2018. He dies in 2024, leaving an estate of £400,000. What is the available nil rate band for his estate?

Answer:

The CLT uses up £200,000 of the NRB. Only £125,000 of the NRB remains for the death estate. The taxable estate is £400,000 – £125,000 = £275,000.

Worked Example 1.7

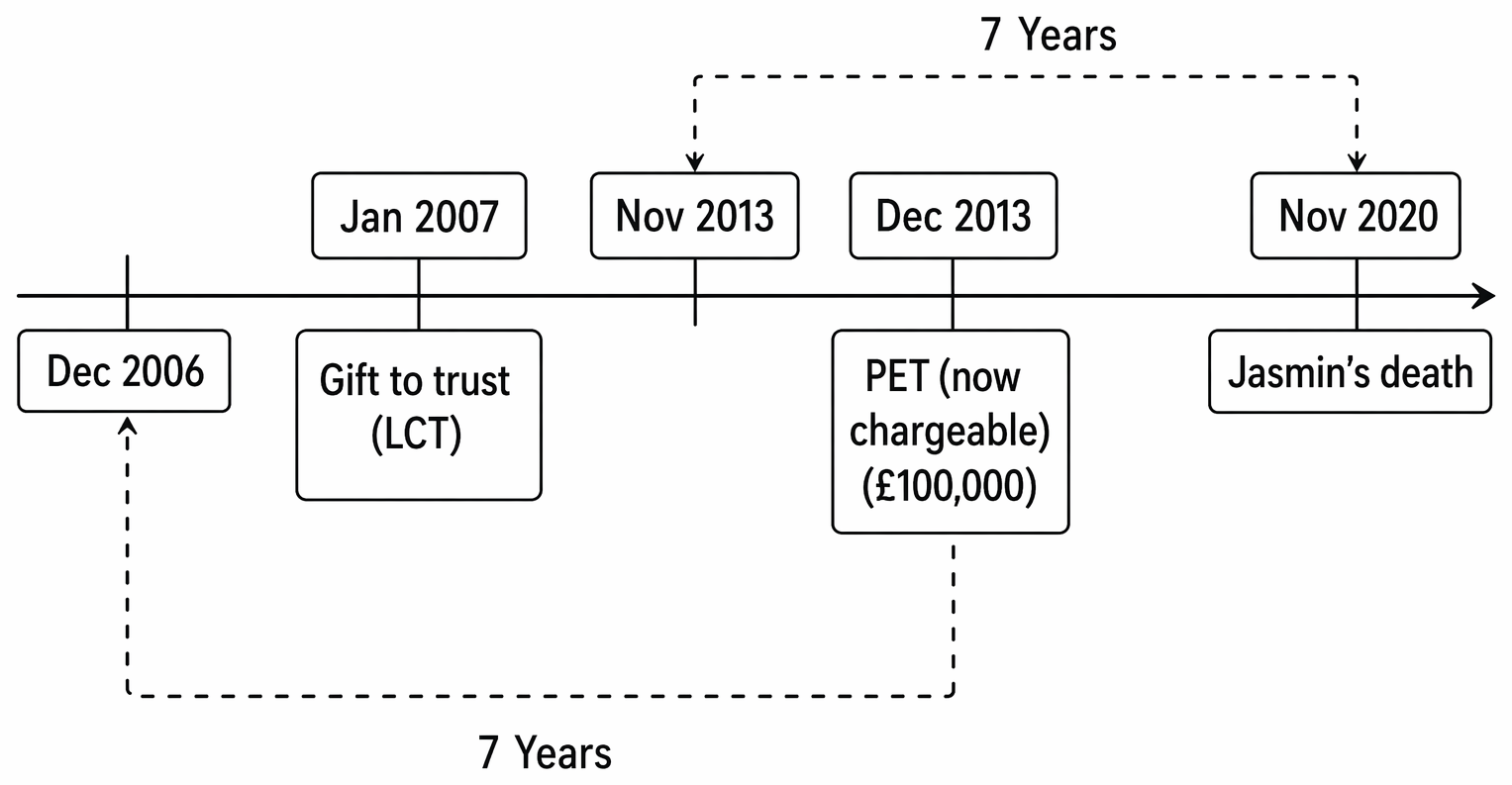

Li made a CLT of £300,000 in January 2010 and a PET of £200,000 in December 2016. Li dies in December 2023. How do these transfers affect the death estate NRB?

Answer:

The 2016 PET is within seven years of death and becomes chargeable. Look back seven years from the PET (December 2016) to cumulate earlier chargeable transfers: the CLT in 2010 is within that look-back and counts for cumulation when taxing the PET (even though it is more than seven years before death). The CLT itself is not rechargeable (Li survived seven years from 2010), but it reduces the NRB available to the PET; the PET may therefore suffer tax. For the death estate, look back seven years from December 2023: only the PET in 2016 is counted (the 2010 CLT is outside seven years), so the PET reduces the NRB for the death estate accordingly.

IHT and Trusts

Trusts are subject to special IHT rules. The main types are:

- Bare trusts: The beneficiary is treated as owning the assets outright for IHT.

- Interest in possession trusts: The beneficiary with a right to income is treated as owning the trust assets for IHT in certain cases.

- Discretionary trusts (relevant property trusts): The trust itself is subject to entry, periodic (ten-year), and exit charges.

Key Term: interest in possession

A present right to present enjoyment of trust income or property. For IHT, some such interests are treated as the beneficiary owning the capital. Key Term: immediate post-death interest (IPDI)

An interest in possession arising on death under a will or intestacy; the life tenant is treated as beneficially entitled to the trust assets for IHT, and the settled property aggregates with the life tenant’s estate at their death. Key Term: transitional serial interest

A post‑22 March 2006 interest following a pre‑22 March 2006 qualifying IIP in limited circumstances (including spouse succession), treated like a pre‑2006 IIP for IHT. Key Term: relevant property regime

The IHT regime for most post‑2006 lifetime trusts, charging entry (lifetime) tax above NRB, ten‑year periodic charges (up to 6%), and proportionate exit charges when property leaves the trust. Key Term: related settlements

Settlements created by the same settlor on the same day; values may be aggregated for trust charges to prevent multiple NRBs. Key Term: same-day additions

Transfers increasing the value of one or more settlements on the same day; anti-avoidance rules may aggregate them when calculating trust charges. Key Term: entry charge

An immediate IHT charge (at 20%) on assets transferred into a discretionary trust above the nil rate band. Key Term: periodic charge

A charge (up to 6%) on the value of trust assets above the nil rate band every ten years. Key Term: exit charge

A proportionate charge on assets leaving a discretionary trust between ten-year anniversaries. Key Term: grossing

Increasing the value of a lifetime transfer to reflect that the donor has chosen to pay the IHT rather than the trustees; the gross amount (loss to donor) is taxed.

Worked Example 1.8

Priya settles £500,000 into a discretionary trust in 2022. She has made no previous gifts. What is the IHT entry charge?

Answer:

The first £325,000 is covered by the NRB. The excess (£175,000) is charged at 20%, so the entry charge is £35,000.

Worked Example 1.9

Arun settles £400,000 into a discretionary trust when his NRB is fully used. He wants the trust to receive the full £400,000 and agrees to pay the lifetime IHT himself. What is the grossing effect?

Answer:

Because Arun pays the IHT, the loss to his estate exceeds £400,000. The net to the trustees is £400,000; the gross (loss to Arun) is £400,000 × 100/80 = £500,000. Lifetime IHT at 20% on £500,000 is £100,000, paid by Arun; trustees receive £400,000. If Arun dies within seven years, recalculation at death rates applies with credit for lifetime tax paid (taper relief may apply).

Anti-avoidance: Gifts with Reservation and POAT

Gifts intended to remove assets from the estate but where the donor retains benefits can be caught.

Key Term: gift with reservation of benefit (GWR)

Lifetime gifts where the donor retains enjoyment (e.g., continues to live rent‑free in a gifted house). The gifted asset is treated as part of the donor’s death estate unless the reservation is fully given up or full market consideration is paid. Key Term: pre-owned asset tax (POAT)

An income tax charge that may apply where arrangements avoid the GWR rules but the donor enjoys benefits from assets they previously owned.

If a reservation is released before death, the release is treated as a PET at that time based on the asset’s then value. In rare cases of double charge (a PET and a GWR), HMRC applies double charges relief to ensure the higher single charge prevails.

Worked Example 1.10

Sofia gifts her house (worth £600,000) to her son in 2018 but continues to live there rent-free. She dies in 2023. What is the IHT position?

Answer:

The gift is caught by GWR; the house is treated as part of Sofia’s death estate at its value at death. The 2018 gift is ignored for PET purposes. If Sofia had ceased her occupation or paid full market rent before death, the gift could have been a PET at the date she ceased the reservation.

Calculation of IHT

The main steps in calculating IHT are:

- Identify all chargeable transfers (lifetime and on death) in the seven years before death, and the death estate components.

- Apply available exemptions and reliefs (spouse and charity exemptions, annual exemption, small gifts, gifts out of income, business and agricultural relief).

- Deduct chargeable transfers from the nil rate band; consider TNRB and RNRB (including TRNRB and downsizing additions) for qualifying death estates.

- Apply the charity reduced rate if the 10% baseline test is met for any component.

- Calculate IHT at 40% on the taxable estate (or 36% if charity reduced rate applies), and at 20% for CLTs (grossing where donor pays).

- Apply taper relief to PETs and rechargeable CLTs if death occurs more than three but less than seven years after the transfer.

- Give credit for lifetime tax already paid on CLTs; no refunds where recalculated tax is lower.

Key Term: quick succession relief

A relief reducing IHT where an estate suffers IHT on assets received from another estate that paid IHT within the previous five years, proportionate to the time elapsed and tax borne. Key Term: instalment option

IHT on certain assets (e.g., land) may be paid in up to ten annual instalments. Interest may accrue; the first instalments due must be paid before the grant issues. Key Term: liability and burden of IHT

Liability (who pays to HMRC) and burden (who ultimately bears the tax) can differ. PRs are liable for death tax; trustees for trust charges; donees for PET tax. The burden falls per will direction or statutory default (often residue), subject to specific-legacies bearing their own tax if so directed.

Timing: IHT on CLTs is due by the later of six months from the end of the month of the transfer and 30 April after the tax year in which the CLT was made. Additional tax on death is generally due six months after the end of the month of death. For the death estate, payment is required before the grant of representation (subject to instalments for qualifying assets and direct payment arrangements with banks).

Exam Warning: Always check the order and timing of gifts and their effect on the nil rate band. PETs only become chargeable if the donor dies within seven years; CLTs are chargeable when made. Be alert to the “14‑year” effect where a PET within seven years of death brings earlier CLTs (within seven years of that PET) into cumulation for the PET calculation. Confirm RNRB conditions (closely inherited, estate value tapering above £2 million, downsizing addition) and remember the charity reduced rate applies only if the 10% baseline test is met for the relevant component.

Summary Table: Key IHT Thresholds and Rates

| Threshold/Rate | Value (2023/24) |

|---|---|

| Nil rate band (NRB) | £325,000 |

| Residence nil rate band (RNRB) | £175,000 |

| IHT rate on death | 40% |

| IHT rate on CLTs (lifetime) | 20% |

| Max periodic trust charge | 6% (every 10 years) |

| Taper relief (3-7 years) | 20–80% of full rate |

Key Point Checklist

This article has covered the following key knowledge points:

- The distinction between potentially exempt transfers (PETs) and chargeable lifetime transfers (CLTs) for IHT.

- The operation of the nil rate band (NRB), transferable NRB (TNRB), and residence nil rate band (RNRB), including tapering above £2 million and downsizing additions.

- The main IHT exemptions and reliefs, including spouse exemption, annual exemption, small gifts, gifts out of income, gifts on marriage, business and agricultural relief.

- The charity reduced rate (36%), baseline amount test, and how it affects the death rate.

- The IHT treatment of trusts, including entry, periodic, and exit charges, related settlements, same‑day additions, and grossing when donors pay lifetime tax.

- Anti-avoidance rules: gifts with reservation of benefit (GWR) and pre‑owned asset tax (POAT), and the availability of double charges relief.

- The calculation of IHT liabilities, including cumulation, the “14‑year” effect, taper relief, credit for lifetime tax, and who is liable to pay and when (including instalment options).

Key Terms and Concepts

- transfer of value

- loss to donor principle

- potentially exempt transfer (PET)

- chargeable lifetime transfer (CLT)

- taper relief

- cumulation

- nil rate band (NRB)

- transferable nil rate band (TNRB)

- residence nil rate band (RNRB)

- transferable residence nil rate band (TRNRB)

- downsizing addition

- excluded property

- spouse exemption

- charity exemption

- charitable reduced rate (36%)

- baseline amount

- annual exemption

- small gifts exemption

- gifts on marriage

- gifts out of income

- business relief

- agricultural relief

- interest in possession

- immediate post-death interest (IPDI)

- transitional serial interest

- relevant property regime

- related settlements

- same-day additions

- entry charge

- periodic charge

- exit charge

- grossing

- gift with reservation of benefit (GWR)

- pre-owned asset tax (POAT)

- quick succession relief

- instalment option

- liability and burden of IHT