Learning Outcomes

This article explains how to interpret and classify testamentary gifts in order to determine whether ademption or abatement applies in typical SQE1 FLK2 problem questions. It distinguishes between specific, general, demonstrative, pecuniary and residuary gifts, and shows how correct characterisation affects the likelihood that a gift will fail, be reduced, or be protected in the administration of an estate. It explains the operation of the doctrine of ademption in relation to missing or substituted assets, lifetime disposals by the testator, transactions carried out by attorneys or deputies, and changes in form such as corporate reorganisations, insurance proceeds or replacement property. It then explains the doctrine of abatement in solvent estates, setting out the statutory and common law order in which different classes of gifts are reduced when assets are insufficient, and the treatment of demonstrative legacies, secured debts and partial intestacy. It also highlights key executor responsibilities in identifying assets and liabilities, applying the proper order of payment, managing competing beneficiary expectations, and using drafting and construction techniques to minimise the risk of failed gifts and personal liability.

SQE1 Syllabus

For SQE1, you are required to understand the legal consequences when gifts in a will cannot be made as intended, with a focus on the following syllabus points:

- the classification of testamentary gifts (specific, general, demonstrative, pecuniary, residuary)

- the doctrine of ademption and when a specific gift will fail

- the doctrine of abatement and the statutory/common law order in which gifts abate

- the practical implications for executors and beneficiaries when assets are insufficient

- how to advise on drafting to reduce the risk of ademption and unintended abatement

- the effect of “will speaks from death” (construction of gifts at the date of death) and contrary intention

- the distinction between abatement in solvent estates and the insolvency regime for insolvent estates

- interaction with secured debts and charges where an asset is specifically gifted

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which type of testamentary gift is at risk of ademption, and what is the result if the item is missing at death?

- What is the statutory order in which gifts abate if the estate cannot pay all debts and legacies?

- If a will leaves "my car" to A, but the car is sold before death, what does A receive?

- How can careful will drafting reduce the risk of ademption or unintended abatement?

Introduction

When interpreting a will, you must know what happens if the estate cannot provide all gifts as written. Two key doctrines—ademption and abatement—determine whether a beneficiary receives their intended gift. Ademption deals with the failure of specific gifts that are no longer in the estate at death. Abatement governs how gifts are reduced if the estate is insufficient to pay all debts and legacies. Both are frequently tested in SQE1 and have practical consequences for executors and beneficiaries.

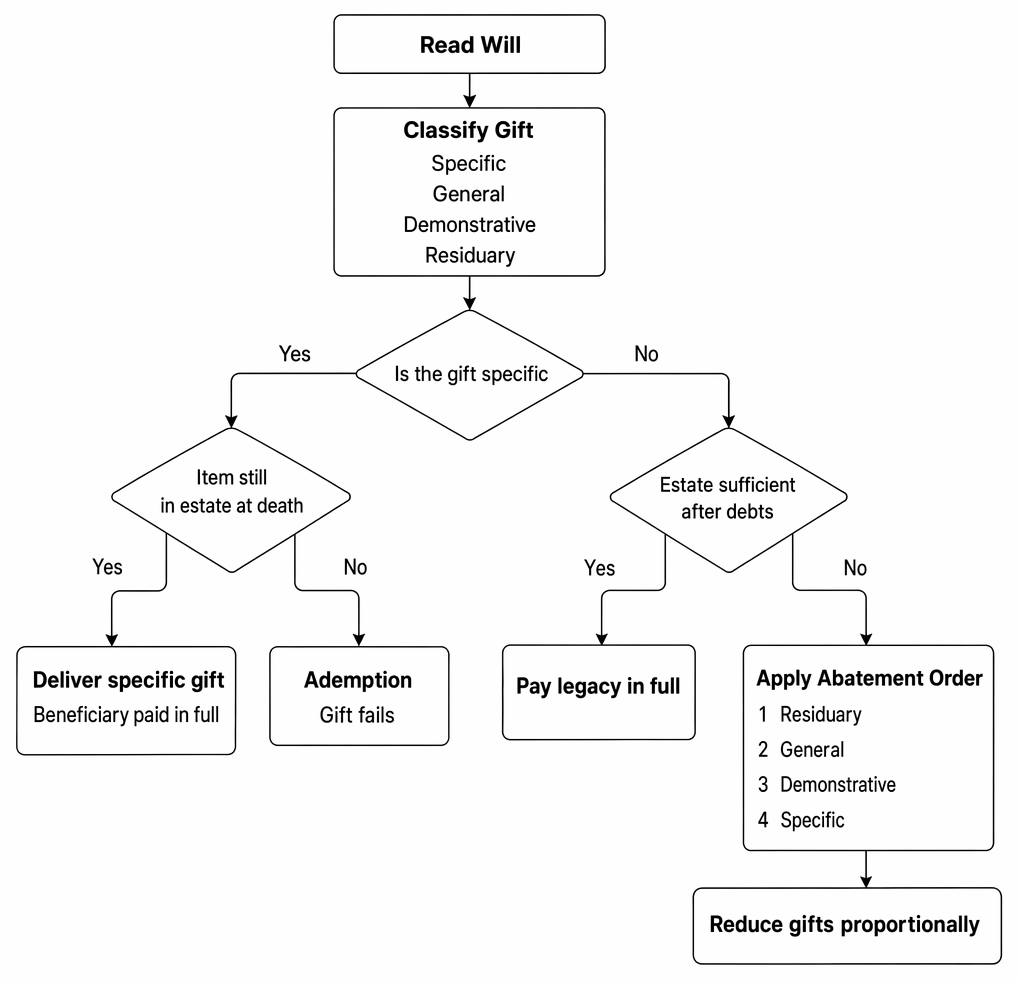

Classification of testamentary gifts determines whether a gift is delivered, adeemed, paid in full, or reduced by the order of abatement.

The analysis always begins with correct classification of the gift and, where necessary, construction of the wording of the will as it “speaks from death” unless a contrary intention appears. Executors then apply the rules on payment of liabilities and the default order of abatement, unless displaced by the will.

Classification of Testamentary Gifts

Before applying ademption or abatement, you must classify the type of gift in the will. The main categories are:

- Specific gifts: a particular item or asset, clearly identified and separated from the rest of the estate (e.g., "my diamond ring to Sarah").

- General gifts: a gift from the general assets of the estate, not tied to a specific item (e.g., "£5,000 to Tom"). A gift of “100 shares in X plc” is typically general: the executors must buy the shares if the testator did not own them at death.

- Demonstrative gifts: a monetary gift to be paid primarily from a specified fund or source (e.g., "£2,000 to be paid from my Barclays account"). If the fund exists to that extent, it is paid from that fund; any shortfall is treated as a general pecuniary legacy.

- Pecuniary gifts: a gift of a sum of money (can be general or demonstrative).

- Residuary gifts: the remainder of the estate after all debts, expenses, and other gifts have been paid.

Correct characterisation affects both the risk of ademption and the order and extent of abatement. For example, a gift of “the £5,000 standing to the credit of my Barclays account number 123456” is specific and will fail if that balance is not in that account at death. By contrast, “£5,000 to be paid out of my Barclays account number 123456” is demonstrative and will not fail if that account is empty; it will be payable from the general estate if necessary.

Key Term: specific gift

A testamentary gift of a particular, identified item or asset, distinguished from the rest of the estate. Key Term: ademption

The failure of a specific gift in a will because the item is not part of the testator's estate at death. Key Term: abatement

The reduction of gifts under a will when the estate is insufficient to pay all debts, expenses, and legacies, following a prescribed order.

Ademption: When a Specific Gift Fails

Ademption applies only to specific gifts. If the exact item is not in the estate at the testator's death, the gift is said to "adeem" and the beneficiary receives nothing.

When Does Ademption Occur?

A specific gift will adeem if, before death:

- The testator sells, gives away, or otherwise disposes of the item.

- The item is destroyed or lost and not replaced.

- The item is fundamentally changed so it is no longer the same asset (e.g., a uniquely described chattel replaced with a different item).

- The gift is of a specific fund and the fund has ceased to exist in that form by death (e.g., “the balance in account X” where that account has been closed and the balance transferred elsewhere).

The testator's intention is generally irrelevant—if the item is not in the estate, the gift fails. Focus on the form and identity of the asset at death, applying normal principles of construction to the will.

Construction and “will speaks from death” As a general rule, a will speaks from death as to property, so a generic description such as “my car” can be construed as referring to the car owned at death. However, where wording indicates a specific identified article (e.g., “my limited‑edition print no. 163”), a later replacement is not the same item and the gift will adeem. The wording and context determine whether the gift is to an identified thing at the date of the will or to the item of that kind owned at death.

When Does Ademption Not Occur?

There are important limits and qualifications:

- Corporate reconstructions: where specific shares are converted into shares in another company under a takeover or reorganisation, the beneficiary may take the replacement shares if the change is one of name or form rather than substance. If the change is so substantial that it is not the same property in substance, the gift may adeem.

- Replacement property within a generic description: a gift of “my car” will normally be satisfied by the car owned at death, even if not the same car owned when the will was made. By contrast, a gift of “my 2018 red Ford Fiesta, registration AB12 CDE” refers to that specific vehicle; a later replacement car will not satisfy the gift.

- Sale or disposal by an attorney or deputy: where a specific asset is sold by an attorney under a lasting power of attorney or by a court‑appointed deputy because the testator lacked capacity, ademption may be avoided. The beneficiary can, in appropriate cases, claim the traceable proceeds or property acquired with those proceeds if they remain identifiable in the estate at death. This protects specific legatees from an involuntary sale made on the testator’s behalf.

- Insurance or compensation proceeds: where a specifically gifted item is destroyed and insurance or compensation proceeds are received and remain identifiable in the estate at death, the beneficiary may be entitled to those proceeds if, on construction, the gift extends to such proceeds (or the will provides for this). If the proceeds have been mixed with general funds, the claim may be lost absent clear wording.

Where only part of a specifically gifted item is disposed of during lifetime (e.g., the testator gifts “my 1,000 XYZ plc shares” and sells 400 shares before death), the gift is satisfied by what remains (600 shares), with no right to the proceeds of the 400 sold, unless another principle applies (such as sale by attorney/deputy as above).

Worked Example 1.1

A will leaves "my painting by Turner to my niece, Emma." Before death, the testator sells the painting and does not buy another. What does Emma receive?

Answer:

The gift is a specific gift. As the painting is no longer in the estate, the gift adeems and Emma receives nothing.

Worked Example 1.2

A will leaves "my shares in ABC Ltd to my brother." Before death, ABC Ltd is taken over and the shares are converted into shares in XYZ Plc. What does the brother receive?

Answer:

If the new shares are a direct substitution for the original shares, the brother may receive the replacement shares. If the change is so substantial that the original asset no longer exists, the gift may adeem.Exam Warning: Ademption applies only to specific gifts. General or pecuniary gifts do not adeem, even if the testator's assets have changed form.

Worked Example 1.4

T gives “my 1,000 shares in BlueCo plc to U.” Before death, T sells 300 of those shares personally. At death, T still owns 700 BlueCo shares. What does U take?

Answer:

The gift is specific. It is satisfied by the 700 shares remaining. There is no right to the proceeds of the 300 sold by T.

Worked Example 1.5

W leaves “the balance in my Lloyds account no. 123456 to P.” W closes that account in life and moves the funds into a new NatWest account. What does P receive?

Answer:

This is a specific gift of the balance of a specified account. Because that account does not exist at death, the gift adeems and P receives nothing (unless the will provides otherwise). If the wording had been “£X to P to be paid from my Lloyds account,” it would be demonstrative and payable from the general estate if the account is empty.

Worked Example 1.6

A will leaves “my car” to K. Two years later, the testator trades in that car and buys a newer vehicle. At death, the newer car is in the garage. Does K receive the newer car?

Answer:

A court is likely to construe “my car” as referring to the car owned at death (the will speaking from death). K should receive the newer car. If the will had identified a specific vehicle by registration, the gift would have been to that vehicle and would have adeemed when sold.

Worked Example 1.7

B’s will leaves “my flat at 1 Green Street to R.” During B’s incapacity, B’s attorney sells the flat to fund care fees and invests the net proceeds into an identifiable deposit account in B’s sole name. At death, that account remains. Is the gift adeemed?

Answer:

A sale by an attorney during the donor’s incapacity will not necessarily cause ademption. If the proceeds remain identifiable in the estate, R may claim the traceable proceeds (or property purchased with them), subject to the precise facts and any contrary intention in the will.

Abatement: When the Estate Is Insufficient

Abatement determines how gifts are reduced if the estate is insufficient to pay all debts, expenses, and legacies. The order of abatement is governed by statute and common law and can be displaced by the will.

Abatement operates in solvent estates when assets are not enough to satisfy all gifts after paying liabilities. If the estate is insolvent (liabilities exceed assets), the insolvency regime applies and beneficiaries receive nothing. In insolvent estates, secured creditors and statutory priorities under insolvency legislation take precedence over legatees.

The Order of Abatement

If the estate is insufficient, gifts abate in the following order (unless the will provides otherwise):

- Property not disposed of by the will (partial intestacy)

- Residuary estate

- General pecuniary legacies

- Demonstrative legacies (to the extent not covered by the specified fund)

- Specific gifts and devises (including demonstrative legacies to the extent covered by the specified fund)

Within each class, abatement is usually rateable (pro rata) if assets in that class are insufficient to meet all gifts in full.

Key Term: general pecuniary legacy

A gift of a sum of money from the general assets of the estate, not tied to a specific fund or item. Key Term: demonstrative legacy

A gift of a sum of money to be paid primarily from a specified fund or source, but not failing if the fund is insufficient. Key Term: residuary estate

The remainder of the estate after all debts, expenses, and other gifts have been paid. Key Term: partial intestacy

Where a will does not dispose of the whole estate, so the undisposed-of property is distributed under the intestacy rules.

Practical Application

- Debts, funeral expenses and testamentary/administration expenses are paid first.

- The abatement order is then applied to gifts.

- Demonstrative legacies are treated as specific out of the identified fund to the extent it exists at death; any shortfall is treated as a general pecuniary legacy and abates in that category.

- If assets run out partway through a class, gifts in that class abate proportionally.

- Secured debts: where an asset is specifically devised or bequeathed subject to a mortgage or other charge, the asset normally passes subject to that charge unless the will shows a contrary intention. The residue is not automatically used to pay off that secured debt.

Worked Example 1.3

A will leaves:

- "My gold watch to Anna" (specific gift)

- "£10,000 to Ben" (general pecuniary legacy)

- Residue to Carla

The estate has debts of £12,000 and £3,000 cash. What do the beneficiaries receive?

Answer:

Debts are paid first (£12,000), leaving £3,000 cash. The general pecuniary legacy to Ben abates: he receives £3,000 (pro rata reduction). The specific gift (the watch) is paid in full if still in the estate. Carla receives nothing as there is no residue.

Worked Example 1.8

A will leaves:

- “£30,000 to X to be paid from my Nationwide savings account” (demonstrative)

- “£20,000 to Y” (general pecuniary)

- Residue to Z

At death, the Nationwide account contains £18,000; other free cash is £10,000 after settling all liabilities. How are gifts satisfied?

Answer:

X’s gift is demonstrative. £18,000 is satisfied specifically from the Nationwide account. The £12,000 shortfall is treated as a general pecuniary legacy. The general category thus contains £12,000 (X’s shortfall) and £20,000 (Y). Only £10,000 is available, so general gifts abate rateably. X receives £18,000 + £10,000 × (12/32) = £18,000 + £3,750 = £21,750; Y receives £10,000 × (20/32) = £6,250. Residue is nil, so Z receives nothing.

Worked Example 1.9

A will leaves:

- “My antique piano to L” (specific chattel)

- “£50,000 to M” (general pecuniary)

- Residue to N

The estate has paid all debts. There is £40,000 cash and the piano worth £10,000. How do the gifts abate?

Answer:

The general pecuniary legacy to M must abate to £40,000. The specific gift of the piano to L is protected until last and is delivered in full. There is no residue for N.

Worked Example 1.10

A will leaves:

- “My house at 20 Oak Road to R” (specific devise; the house is mortgaged for £100,000)

- “£100,000 to S”

- Residue to T

After paying debts and costs (other than the mortgage), there is £100,000 free cash. How do the gifts abate and who bears the mortgage?

Answer:

The house passes to R subject to its mortgage unless the will shows a contrary intention. The residue is not automatically used to clear that secured debt. The £100,000 cash funds S’s general pecuniary legacy; if cash is inadequate, S’s legacy abates before the specific devise. T receives residue only if anything remains after satisfying gifts and liabilities, which here is unlikely once S is paid.

Exam Warning (Abatement)

Demonstrative legacies are treated as specific gifts to the extent the specified fund exists, and as general legacies for any shortfall. This affects the order of abatement.

Additional Abatement Points Frequently Tested

- Rateable abatement within a class: where there are multiple general pecuniary legacies and the available fund is insufficient, they abate proportionally based on the amounts.

- Prior payments: if a personal representative overpays one general legatee before discovering a shortfall, they may be personally liable to make good the excess to ensure other general legatees receive their proper pro rata share.

- Contrary intention: the will can vary the default order (e.g., by directing that certain general legacies or a particular fund are to abate last), but clear wording is needed.

- Insolvent estates: if liabilities exceed assets, the insolvency rules apply. Secured creditors look to their security first, preferred debts take priority, and ordinary unsecured creditors rank ahead of beneficiaries. Legacies will not be paid.

Executor Duties and Practical Issues

Executors must:

- Identify and value all estate assets and liabilities.

- Classify each gift in the will and construe the wording to determine whether a gift is specific, general, demonstrative or residuary.

- Identify secured debts and whether assets are to pass subject to charges or to be exonerated under the will.

- Apply the correct order of abatement if assets are insufficient.

- Communicate with beneficiaries if gifts are reduced or fail.

- Keep demonstrative funds under review: quantify what part of a demonstrative legacy is satisfied from the specified fund, and what part is to be treated as general.

- Avoid premature distributions: wait until liabilities are known and the abatement position is clear, or retain sufficient funds and use protections such as statutory advertisements to limit personal liability.

- Consider appropriation where appropriate: with necessary consents, assets can be appropriated in or towards satisfaction of legacies, ensuring fair value where cash is short.

Key Term: executor

The person appointed by a will to administer the estate, pay debts, and distribute gifts to beneficiaries.

Practical points:

- Evidence and records: keep clear records of corporate reorganisations, bonus issues, and conversions affecting specific share gifts to demonstrate whether a change is in form only (supporting non‑ademption).

- Attorneys and deputies: if a specific asset has been sold by an attorney or deputy, identify and ring‑fence the traceable proceeds if they remain in the estate.

- Asset sales during administration: selling a specifically gifted asset after death (for administration reasons) does not cause ademption; the beneficiary is entitled to the net proceeds of sale.

- Insolvent estates: if the estate appears insolvent, executors should follow the statutory order for insolvent administration and avoid paying legacies.

Drafting to Reduce the Risk of Ademption and Abatement

Careful will drafting can help avoid unintended ademption or abatement:

- Use broader descriptions for gifts (e.g., "the car I own at my death" rather than identifying a specific registration), if the testator’s intention is to benefit the class of item rather than a unique chattel.

- For volatile or changeable assets, link gifts to replacements and proceeds (e.g., “I give my [identified item], or any direct replacement of it acquired before my death, and any insurance or compensation proceeds then held by my estate, to X”).

- Include substitution or fallback clauses (e.g., "If I do not own my piano at my death, I give £5,000 to X").

- For bank accounts, prefer demonstrative wording where appropriate (“£X to be paid out of account Y”) rather than a specific gift of “the balance in account Y,” which is vulnerable to ademption if the account is closed or moved.

- Manage secured debts by stating whether property is left “subject to any charge” (default position) or “free of any charge,” the latter expressing a contrary intention that residue should bear the debt.

- State preferences for the order of abatement if you wish to depart from the default order (e.g., “my charitable legacies are to abate last”).

- Regularly review and update the will to reflect changes in assets and circumstances.

Revision Tip: When advising on a will, always check if the testator's assets are likely to change, and warn about the risk of ademption for specific gifts.

Key Point Checklist

This article has covered the following key knowledge points:

- Ademption applies only to specific gifts; if the item is not in the estate at death, the gift fails.

- Construction matters: the will “speaks from death” as to property unless a contrary intention appears; generic descriptions may capture replacements owned at death.

- Ademption may be avoided where a sale was made by an attorney/deputy during the testator’s incapacity and traceable proceeds remain in the estate.

- Corporate reorganisations can produce replacement shares; whether a gift adeems depends on whether the change is one of form or substance.

- Demonstrative legacies are satisfied first from the identified fund and, as to any shortfall, abate as general pecuniary legacies.

- Abatement determines the order in which gifts are reduced if the estate is insufficient: property not disposed of, residue, general pecuniary legacies, demonstrative shortfall, specific gifts.

- Within a class, abatement is rateable; executors must avoid preferring one legatee within a class to the detriment of others.

- Specific devises generally pass subject to existing charges unless the will shows a contrary intention; residue is not automatically used to discharge secured debts.

- Distinguish abatement in a solvent estate from the application of insolvency rules in an insolvent estate.

- Executors must classify gifts, construe wording, apply abatement correctly, and protect themselves against personal liability.

- Careful drafting (replacements, proceeds, demonstrative wording, abatement directions) reduces the risk of ademption and unintended abatement.

Key Terms and Concepts

- specific gift

- ademption

- abatement

- general pecuniary legacy

- demonstrative legacy

- residuary estate

- partial intestacy

- executor